# The First Quarter Without 25D: Residential Solar CPL Reset, TPO Migration, and the Lead-to-Install Math Operators Are Repricing in 2026

> **Canonical:** https://www.leadgen-economy.com/blog/first-quarter-without-25d-solar-credit-cpl-reset/

> **Published:** 2026-06-25

> **Author:** Alex Paddington

> **Source:** LeadGen Economy – https://www.leadgen-economy.com

---

*Six months after the federal homeowner tax credit ended, residential solar lead generation is repricing every variable that mattered for two decades – and the numbers visible in Q1 2026 are only the dress rehearsal.*

---

## The first clean look at a post-25D residential market

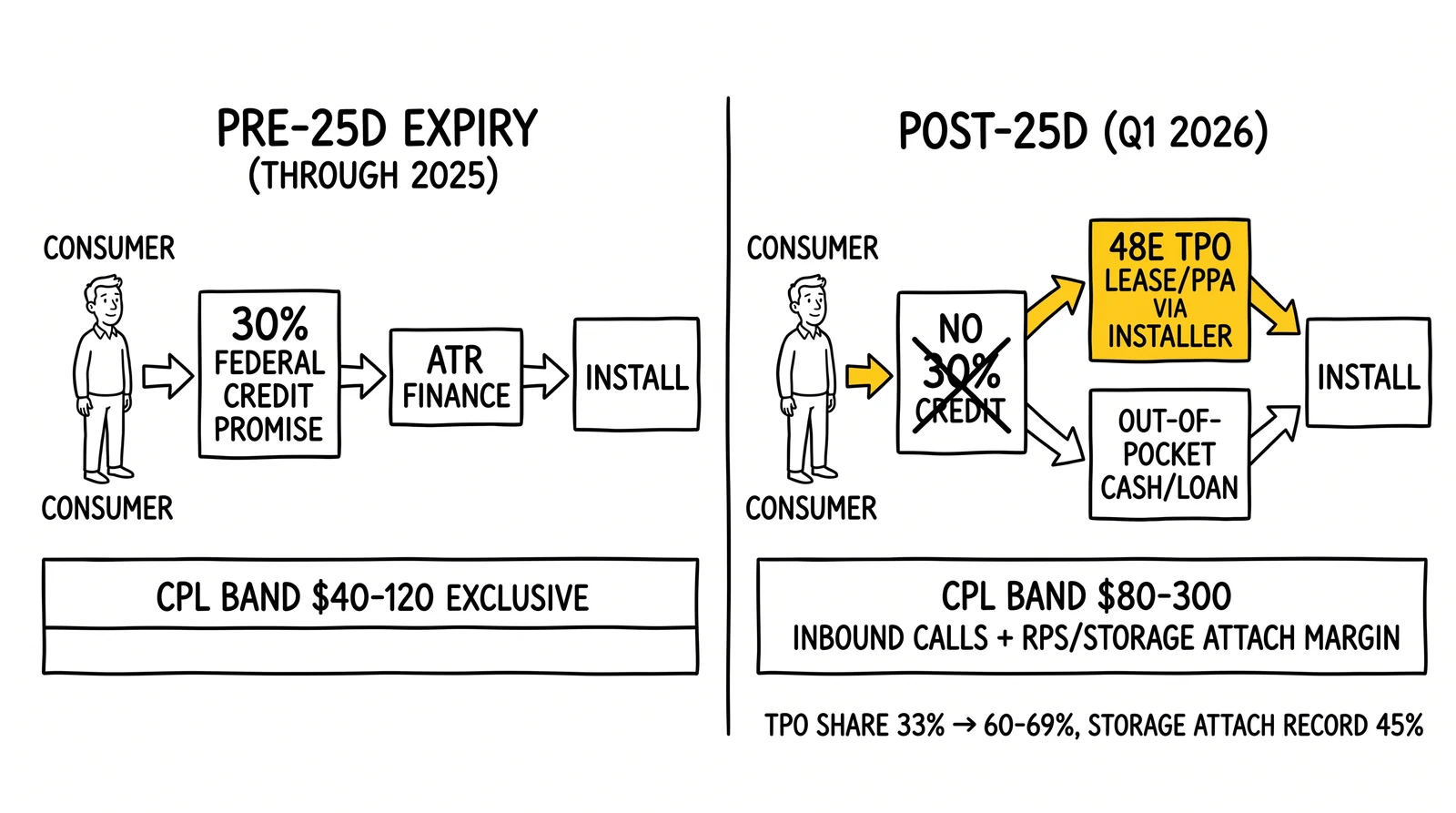

Section 25D of the Internal Revenue Code, the Residential Clean Energy Credit, terminated for any system placed in service after December 31, 2025. Public Law 119-21, the One Big Beautiful Bill Act signed July 4, 2025, removed the 30 percent federal credit that had subsidized homeowner-owned residential solar since the original Energy Policy Act of 2005 and its successor extensions. IRS guidance under Section 25D(e)(8)(A) is mechanical: the expenditure is treated as made when original installation is completed, so a system commissioned January 1, 2026 receives no federal credit even if equipment was paid for in 2024.

The lead-gen value migrates to the 48E TPO route – installer-financed leases and PPAs are now the conversion path that survives the credit expiry.

Q1 2026 is the first quarter in which the lead-generation funnel has had to function without that subsidy on the homeowner side. The numbers are misleading on a single read. SEIA and Wood Mackenzie's Q2 2026 U.S. Solar Market Insight reported 1,179 MWdc of residential capacity installed, a 6 percent year-over-year gain. That print does not represent post-25D demand. It represents the tail of customer-owned projects that signed contracts in the fall of 2025 and had to interconnect before December 31 to claim the credit. Interconnection queues stretched at most utilities, and overflow bled into January, February, and March installs that still qualified under the placed-in-service rule applied to pre-deadline commencement.

The Q1 quarter-over-quarter print is the more honest read: residential installs fell 15 percent against Q4 2025, and Wood Mackenzie's full-year 2026 residential forecast cuts 21 percent from 2025 levels. The pulled-forward demand of late 2025 is now an inverse vacuum at the top of the funnel. Solar operators with revenue plans built on 2024-vintage close-rate and install-rate assumptions are watching the inputs collapse one cohort at a time. The CPL that worked at a 6.7-year payback no longer works at a 9.6-year payback, and that 43 percent extension of the simple-payback figure is what the homeowner-credit removal actually does to consumer economics absent a financing workaround.

The lead-to-install ratio is the variable most operators are mis-pricing. Pre-25D economics carried roughly stable conversion through the funnel: lead-to-appointment in a 25 to 40 percent band, appointment-to-sale in a 20 to 35 percent band, sale-to-install in the high 80s. Post-25D, the same lead specs are converting 15 to 30 percent worse at the appointment and sale tiers, because direct-sale loan underwriting and TPO underwriting reject the same lead profile at different rates. A FICO 640 lead with a $60 utility bill that closed against a Mosaic-backed loan in 2024 will not pass GoodLeap or Sunrun lease underwriting in 2026.

This is the structural picture as of June 25, 2026. The credit died. Demand pulled forward. TPO absorbed the survival case. Lead specs broke. Bankruptcies concentrated buyer rosters. A nine-day window remains before the next federal deadline closes. Every other section of this article unpacks one of those facts in operator detail.

---

## Why Q1 2026's headline number lied

The SEIA and Wood Mackenzie quarterly report is the canonical source for residential solar installation volume, and the Q1 2026 print needs to be read carefully. The 1,179 MWdc total is real. The 6 percent year-over-year gain is real. Neither describes Q1 demand. Both describe pre-deadline backlog clearing into the new tax year.

Customer-owned projects that signed in October or November 2025 ran into a wall of interconnection delays at utilities including Pacific Gas and Electric, Southern California Edison, Eversource, and most of the southeastern IOUs. The deadline rule under Section 25D treats the credit as available when original installation is completed, which IRS guidance ties to the placed-in-service date for tax purposes. Installers that completed physical commissioning before December 31, 2025 but did not receive utility permission to operate until January or February could still claim 25D under documented good-faith adherence to the placed-in-service standard, but most customer-owned projects were structured around the cleaner standard and had to commission and interconnect before year-end. The overflow that did push into January saw projects bunched in the 1.5 to 6 percent of the residential install pipeline. That is roughly 18 to 70 MWdc of the Q1 1,179 MWdc figure attributable directly to deadline-driven catch-up.

The quarter-over-quarter print is what to track. Q4 2025 residential installs ran at roughly 1,387 MWdc, the highest single quarter on record because the deadline pulled every viable customer-owned project into commissioning. Q1 2026's 15 percent quarterly decline is mathematically the cliff. Q2 2026 will be the first quarter with no significant pre-deadline tailwind in either direction. The Q2 print, which Wood Mackenzie typically releases in early September, is the first real read on what post-25D demand looks like on its own merits.

Battery storage attach data inside Q1 2026 is the part of the report that surprised most installers. A record 45 percent of residential solar installations paired with battery energy storage, the highest attach rate ever recorded. The storage attach is a Section 48E play even on customer-owned systems when storage is charged predominantly by solar PV, and the residential customer-side credit on standalone storage came in under different statutory treatment that Q1 buyers were exploiting. The practical signal for lead operators is that solar-plus-storage leads now carry a 10 to 25 percent CPL premium over solar-only and convert at higher rates in California NEM 3.0, Hawaii NEM, and any market where time-of-use rate spreads exceed 35 cents per kWh peak-to-off-peak.

Wood Mackenzie's full-year 2026 residential forecast of a 21 percent decline maps the rest of the year against four scenarios. The base case assumes Section 48E TPO project flow holds at 60 to 65 percent of the market by mid-Q3, that the July 4, 2026 begin-construction deadline produces a one-time bulge in 48E originations, and that Q4 settles into a steady-state running rate roughly 30 percent below the 2025 cadence on a customer-owned basis but with TPO substitution filling more than half the gap. Operators planning lead-buy commitments for the second half of 2026 should write to a residential install base of roughly 4.0 to 4.5 GWdc full-year, against 5.1 GWdc in 2025 – and treat that band as forecast risk that resolves only after the September Q2 print.

---

## The Section 48E rail and the July 4 deadline that runs the clock

Section 48E is the technology-neutral commercial investment tax credit that survived the 25D termination. It applies to solar systems owned by third parties, which in the residential context means systems owned by a TPO provider and leased or sold under a power purchase agreement to the homeowner. The 30 percent credit is claimed by the TPO sponsor, monetized through tax equity or transferability under Section 6418, and passed through to the homeowner as lower monthly payments below the equivalent loan-financed installed cost. The structure is not new. What is new is that it is now the only way most residential customers can access any federal tax benefit on a solar installation.

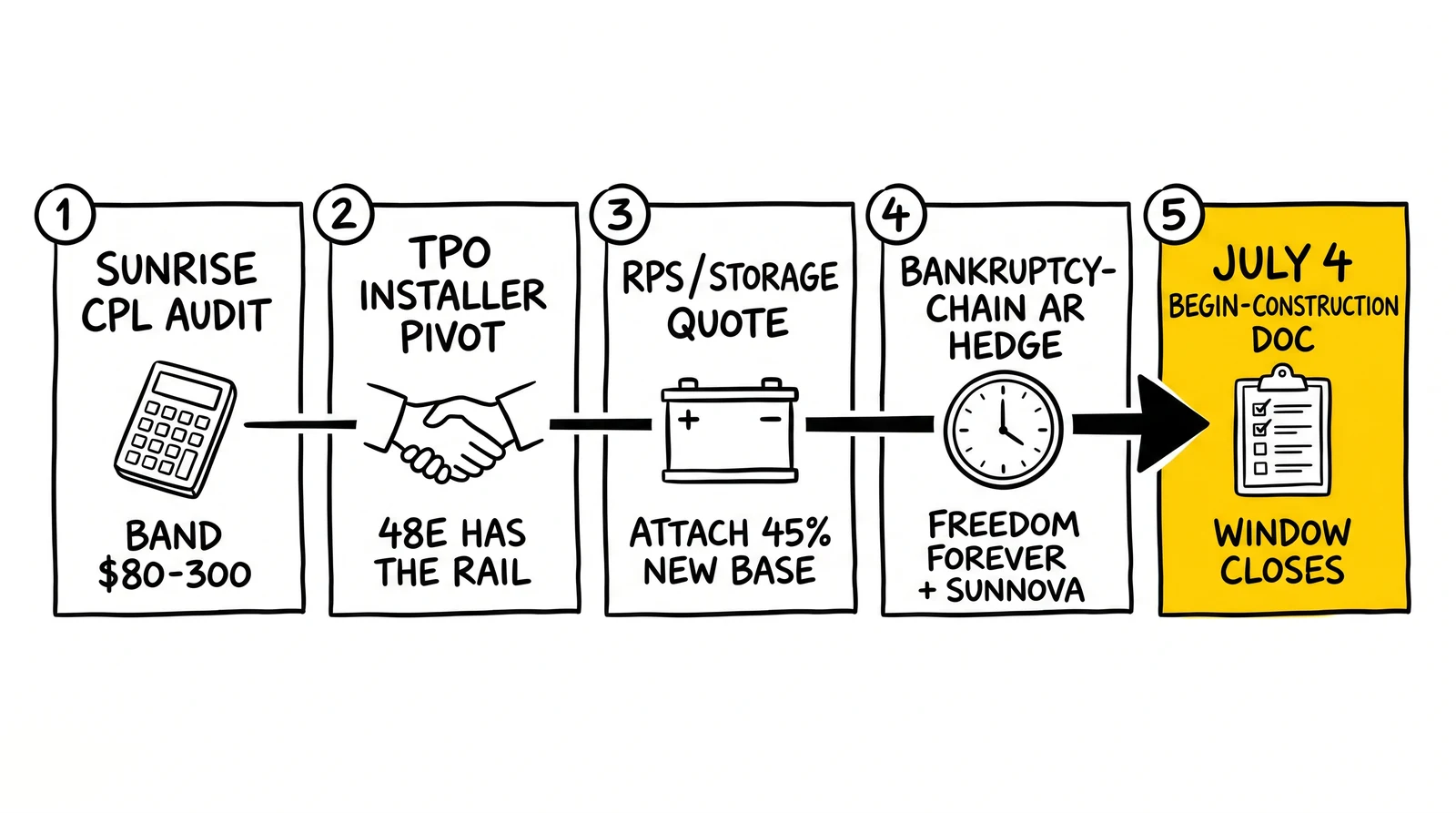

The deadline matters. Public Law 119-21's transition rules require that 48E projects begin construction before July 4, 2026 to qualify under current rules. Projects that begin construction by that date can be placed in service within four years, meaning until 2030. After July 4, 2026, the credit phases down on a schedule tied to greenhouse-gas emissions targets in the underlying Inflation Reduction Act framework that survived OBBBA. The practical result is that every TPO provider, downstream installer, and lead-gen operator selling against 48E is in a sprint to originate, document, and structure begin-construction status on the maximum possible project pipeline before July 4. As of late June 2026, nine days remain.

Begin-construction is a defined term under existing Treasury guidance applied to 48E by reference. Two safe harbors exist. The Physical Work Test treats construction as begun when physical work of a significant nature begins on a project. For residential solar, this can include site grading, ground-mount foundation excavation, on-site or off-site fabrication of racking components specific to the project, or other tangible work that integrates into the system. The Five Percent Safe Harbor treats construction as begun when the taxpayer pays or incurs at least 5 percent of total project cost. The 5 percent test is the workhorse for residential portfolios. TPO providers pre-purchase modules, inverters, and balance-of-system components in pooled inventory allocated to identified residential projects and book the costs against specific contracts to clear the safe-harbor threshold.

The lead-gen implication of the deadline is direct. Lead aggregators and installer-buyers are bidding higher for in-cycle residential leads through the first week of July to fill the pre-deadline pipeline. PPC bids for "solar panels near me," "free solar quotes," and "solar incentives 2026" spiked roughly 15 to 30 percent on Google and Meta inventory in the first three weeks of June, with some California and Texas zip codes showing 40 percent bid escalation. Lead resellers report inbound calls clearing at the top of the $100 to $300 range, with $400-plus reported on exclusive same-day calls in NEM 3.0 California metros. Operators that hit the deadline window with prepared lead pools and disciplined buyer-tier matching are realizing 6-month margin in 9 days. Operators that delayed media spend on uncertainty about TPO underwriting acceptance are watching the window close.

What happens after July 4 depends on Treasury and IRS issuance of begin-construction continuity and 48E phase-down guidance, neither of which had been finalized as of June 2026. The market will continue to flow projects into late 2026 and into 2027 under 48E, but at lower per-project credit value if phase-down triggers fire on the IRA framework's emissions schedule. Operators should plan lead programs for Q3 and Q4 under two scenarios: a continuing 30 percent 48E credit if phase-down does not fire, and a 60 to 70 percent fade in TPO sponsor willingness-to-pay if phase-down fires at 6 percent or 0 percent on accelerated schedules.

---

## TPO absorption: who's actually buying leads now

The buyer-roster for residential solar lead aggregators has compressed and concentrated since the credit expired. Direct-sale loan installers – the model that drove the Sunnova-Mosaic-Freedom-Forever-Lumio-PosiGen wave – have either filed Chapter 11, exited markets, or repositioned as TPO dealers. The capacity that remains sits in roughly six TPO platforms with publicly disclosed funding stacks and investment-grade or near-IG sponsor capital.

The July 4 begin-construction safe-harbor deadline is the immovable anchor. Operators who run all five actions in 90 days enter Q4 with priced exposure rather than absorbed loss.

Sunrun is the structural winner. The company's Q1 2026 earnings presentation, dated May 6, 2026, reported approximately 19,000 customers added in the quarter against a strategy that explicitly anticipates consolidation. Sunrun represents roughly one-third of national subscription volumes on solar product and more than 50 percent of the residential storage market. The Q1 operating and financial results highlighted execution against the post-25D environment, including pricing changes that raised average system price per watt to TPO-friendly levels and storage attach gains that boost project NPV under Section 48E sponsor economics. Sunrun's lead-buying behavior in Q2 2026 has shifted toward national exclusive programs rather than the dealer-network distribution model that drove its 2020 through 2023 growth, which compresses CPL inflows to legacy dealer aggregators but creates new direct-to-source channels for lead generators with the volume to support exclusive specs.

GoodLeap remains the dominant residential loan platform and has positioned its lease and PPA products as the alternative to the discontinued Mosaic stack that Forbright Bank absorbed in 2025. Palmetto LightReach holds meaningful share in the southeast and the Mid-Atlantic where Sunrun's brand penetration is weaker. EverBright, the NextEra subsidiary, holds share in markets where utility-affiliated capital can underwrite TPO sponsor commitments at lower equity cost than independent platforms. Sungage Financial holds share in the long-tail installer-by-installer dealer market. Solar Servicing, the Forbright Bank subsidiary that acquired Mosaic's loan platform in 2025, services the existing Mosaic-originated portfolio and is positioned to re-enter origination as a TPO sponsor in late 2026 if Treasury phase-down guidance permits.

The aggregator-side lead-spec rewrite required to match TPO underwriting boxes is non-trivial. Direct-sale loan boxes accepted FICO 640-plus with $60-plus utility bills. TPO boxes require FICO 650 minimum for lease, 680 minimum for PPA, homeowner-of-record, and an $80 minimum monthly utility bill that benchmarks against TPO escalator economics. Lead aggregators that filtered to the legacy loan box will see TPO acceptance rates collapse without spec rewrites. The TPO box also weights factors the loan box ignored: roof age, roof material, shading from on-property trees, HOA approval status, and panel-eligible roof square footage. Each of those factors needs to be captured at the lead level or qualified into the appointment stage, which raises CPL on raw inputs but improves lead-to-install ratios enough to offset the cost.

A small group of regional EPC installers continue buying leads against a residual customer-owned-cash-purchase market. The cash-purchase segment is roughly 12 to 15 percent of residential installations and runs without dependency on the federal credit. CPL in this segment has held flat at $40 to $80 for exclusive real-time leads but margin on the buyer side has tightened as system prices per watt held steady at roughly $2.58 nationally (EnergySage Q1 2026 marketplace data, with quotes through the platform averaging $2.75 per watt before incentives) while installer customer acquisition cost climbed against the broader market contraction. Cash-purchase lead programs are the right home for installer-buyers with strong balance sheets and disciplined CPL ceilings; they are the wrong home for aggregators chasing volume.

---

## The bankruptcy chain and what it means for installer aggregation receivables

The post-25D residential solar buyer roster carries embedded counterparty risk that exceeds anything in U.S. lead generation history. Ten major installers and one $15 billion loan platform filed Chapter 11 between February 2024 and April 2026.

The chain runs in roughly this order: SunPower (August 2024), Lumio (September 2024), Titan Solar Power (early 2025), Solar Mosaic (June 2025), PosiGen (mid-2025), Sunnova (June 8, 2025 in the U.S. Bankruptcy Court for the Southern District of Texas, reporting $10 billion to $50 billion in both assets and liabilities and total debt of roughly $10.67 billion at end of 2024), and Freedom Forever (April 15, 2026 in the District of Delaware, with $100 million to $500 million in assets and $500 million to $1 billion in liabilities; Mosaic was its single largest creditor at approximately $110 million). Smaller installer failures including ADT Solar's residential wind-down, Pink Energy, Vision Solar, Brightplanet Solar, and others bookend the period.

Sunnova's collapse was the structural inflection. The company operated the second-largest TPO portfolio in the country at the petition date and had carried a debt stack swollen by elevated inflation, sustained high interest rates that compressed lease and PPA sponsor IRRs, and policy uncertainty that culminated in the OBBBA 25D termination. The sale process, conducted under court supervision, allocated the operating platform to a strategic buyer and left general unsecured creditors with fractional recovery prospects. For lead aggregators that had carried Sunnova receivables, the practical outcome is a write-down of pre-petition AR at recovery rates closer to 1 to 5 percent of face. Aggregators carrying concentration above 10 percent of monthly revenue from Sunnova in mid-2025 took direct margin damage on Q3 and Q4 2025 reporting.

Freedom Forever was the second-largest U.S. residential installer at the petition date, with 6.1 percent of national market share by 2025 and operations in over 30 states. Its hybrid dealership-plus-TPO model – selling systems owned and financed by third parties, including Sunrun, GoodLeap, and Mosaic – produced concentrated exposure to Mosaic's financing-partner failure in June 2025. When Mosaic's financing stack collapsed, Freedom Forever lost a primary funding lifeline, then absorbed downstream demand contraction from the 25D sunset, then exited 10 of its markets and laid off roughly 20 percent of its workforce in early 2026, then drew a Texas Attorney General Civil Investigative Demand on April 3, 2026, and filed in Delaware nine business days later. The signals were observable in real time. Aggregators that ran D&B PAYDEX monitoring, tracked WARN notices, scraped state AG dockets, and read public market-exit announcements had a 90 to 120 day warning window.

For 2026 forward, lead aggregators should treat residential solar counterparty risk as a baseline operating discipline, not a special case. Three rules apply. First, the 10/25/40 diversification rule: no single buyer above 10 percent of monthly revenue, no single finance tier above 25 percent, no single state above 40 percent. Second, contract terms should compress payment from net-30 or net-45 to ACH-on-delivery for any buyer below a credit threshold, with weekly settlement above it; personal guarantees from controlling owners on smaller installer buyers; performance bonds or escrow deposits equal to 30 days of historical purchases. Third, accounting policy: write down 100 percent of pre-petition exposure on the petition date and reverse the charge if and when a distribution occurs, which produces accurate period reporting and avoids margin restatements when plans confirm later than expected.

Trade credit insurance from Allianz Trade, Coface, Atradius, and AIG Trade Credit prices solar-installer concentration toward the upper end of the 0.10 to 0.50 percent of insured turnover band given the post-2024 loss history. For a $20 million annual solar lead operation with $1.5 million in average outstanding AR, full coverage runs roughly $30,000 to $75,000 per year. Non-recourse factoring at roughly 1 percent per month plus a factor's guarantee fee is the alternative for operators wanting both credit protection and liquidity in a single instrument.

---

## The CPL reset: what operators are actually pricing now

Solar CPL has not collapsed. It has bifurcated. Real-time exclusive residential leads still clear at the $40 to $120 range that has defined the market for three years, with the upper end clustered in California NEM 3.0 markets, Texas competitive-retail markets with high summer rates, and Hawaii. Inbound calls clear $100 to $300 with $400-plus reported on same-day exclusive in the highest-value zips. Aged leads remain priced as they were: 30 to 85 days at $0.60 to $1.50, 86 to 365 days at $0.35 to $0.40, 366-plus days at $0.17 to $0.20. The cost of inputs has not moved much. What has moved is the conversion math through the funnel.

Lead-to-appointment conversion has compressed 15 to 30 percent on legacy lead specs that no longer match TPO underwriting boxes. A lead aggregator running a $60 utility bill, FICO 640-plus filter that ran a 32 percent lead-to-appointment ratio in 2024 is now running roughly 22 to 27 percent because TPO underwriting throws back leads at the qualifier stage that direct-sale loan underwriting would have accepted. Appointment-to-sale conversion has compressed similarly because the homeowner-perceived savings on a TPO lease are smaller than the homeowner-perceived savings on a 25D-credited loan, and sales reps trained on the loan pitch are losing the close to "let me think about it" at higher rates.

The net effect on customer acquisition cost is a 25 to 45 percent increase against 2024 baseline. Industry CAC benchmarks for surviving installers now sit at $3,000 to $7,000 for residential solar installations, against $2,400 to $5,200 in 2024 on the same segments. TPO providers running national exclusive programs absorb more of that spend internally and report installer-equivalent CAC in the $4,200 to $5,800 range, which is the benchmark lead operators should use when pricing exclusive specs into Sunrun, GoodLeap, and EverBright direct programs.

The lead spec rewrite is where margin is being defended. Three changes matter. First, the utility-bill threshold needs to move from $60 to $80 minimum on any TPO-routed lead, because the lease economics break below that bill level and TPO providers reject the leads at the qualifier stage rather than the appointment stage, which forces the lead operator to eat the rejection rather than the installer. Second, the FICO threshold needs to move to 650 minimum for lease-routed leads and 680 for PPA-routed leads, and the lead capture form needs to gather the credit-score self-report explicitly. Third, the homeowner-of-record check needs to run against a property-records data source (ATTOM, DataTree, or equivalent) at lead capture rather than at appointment, because the false-positive homeowner rate at appointment is the single largest source of TPO rejection.

The PPC and media-buying side is repricing too. Google Ads and Meta CPC for solar keywords spiked 15 to 30 percent through the first three weeks of June 2026 against the July 4 deadline. CPC peaks of $40 to $65 on terms including "solar tax credit 2026," "solar panels free quote," and "best solar installer near me" reflect installer-buyer panic-buying against pipeline goals. Operators with disciplined budget pacing have been moving spend to Q3 to capture the post-deadline pricing reset that should arrive in the second half of July as the deadline-driven bid pressure releases. The arbitrage opportunity for operators who held inventory and lead pools through June is to sell into the deadline spike at premium and rebuild pools at lower CPC through August.

---

## What operators should be doing in the next 90 days

The structural shift is identified. The remaining question is operator action. Three categories of decision apply, in priority order.

**Lead-spec and buyer-roster discipline.** Rewrite lead specs to TPO underwriting boxes before Q3 begins. FICO 650 minimum for lease, 680 minimum for PPA, homeowner-of-record verified at capture, $80 minimum monthly utility bill, roof age and material captured in qualifier flow. Rebuild the buyer roster around the six surviving TPO platforms: Sunrun (largest by share), GoodLeap (largest residual loan-to-lease pivot), Palmetto LightReach (southeast and Mid-Atlantic strength), EverBright (utility-affiliated capital), Sungage (long-tail dealer market), Solar Servicing (re-entering origination). De-emphasize direct-sale loan installers as primary buyers until the second wave of bankruptcies clears, which most analysts expect through year-end 2026.

**CPL and pricing repositioning.** Reprice lead-buy commitments to a TPO-centric installer CAC of $4,200 to $5,800 rather than the 2024 direct-sale baseline of $2,400 to $5,200. Move exclusive real-time real-time pricing to the $80 to $120 band for TPO-quality leads in NEM 3.0 California, ERCOT Texas, and Hawaii. Move inbound calls into the $200 to $400 band for the same markets. Push aged-lead pricing as the conversion buffer for installers running working-capital-constrained operations, and price aged-call programs separately because the conversion math on aged calls runs different than aged data leads.

**Counterparty and contract discipline.** Apply the 10/25/40 diversification rule across the buyer roster. Compress payment terms to ACH-on-delivery for any buyer below a credit threshold, with weekly settlement above it. Require personal guarantees from controlling owners on smaller installer buyers. Either buy trade credit insurance at the 0.30 to 0.50 percent of insured turnover band given solar concentration, or set up non-recourse factoring at 1 percent per month plus the factor's guarantee fee. Write down 100 percent of pre-petition AR on any future Chapter 11 petition date and reverse the charge if distributions land. This is the discipline that separates solar lead operations that survive Q4 2026 from those that don't.

A fourth category – pipeline diversification – applies to lead-gen operators that built single-vertical residential solar businesses through the 2021 to 2023 boom. The post-25D residential market will likely not return to 2024 install volumes inside a five-year window even on the optimistic Wood Mackenzie forecast track. Operators with the capability to extend into adjacent verticals – battery-only storage, commercial-and-industrial solar lead programs, residential EV-charger installation lead programs, electrification and weatherization rebate-driven programs – should treat 2026 as the diversification window. The lead-capture infrastructure, installer relationships, and homeowner data assets that drove residential solar lead-gen in the 25D era translate cleanly into those adjacencies. The operators that do not diversify will run smaller residential solar lead businesses through 2027 and beyond, which is a viable strategy but a strategy that requires repricing the business at a smaller revenue base.

---

## Key Takeaways

- Section 25D expired December 31, 2025 under Public Law 119-21. No phase-down, no grace period. Systems placed in service after that date are ineligible for the homeowner credit. Carryforward of unused credits from earlier installations is preserved.

- Q1 2026's 1,179 MWdc residential install print and 6 percent year-over-year gain were inflated by pre-deadline backlog. The quarter-over-quarter decline of 15 percent is the honest read; Wood Mackenzie's full-year 2026 forecast cuts 21 percent.

- Section 48E remains in effect for TPO leases and PPAs. The 30 percent credit is claimed by the TPO sponsor and passed through to the homeowner. Begin-construction must occur before July 4, 2026 to qualify under current rules; placed-in-service can extend to 2030.

- TPO market share is shifting from roughly 45 percent of residential installs in 2025 to 60 to 69 percent in 2026 by industry-analyst projections. 65 percent of installer salespeople expect TPO to account for more than half of 2026 project volume, against 44 percent in 2025.

- Solar CPL did not collapse but bifurcated. Real-time exclusive leads still clear $40 to $120; inbound calls $100 to $400. Lead-to-appointment conversion compressed 15 to 30 percent on legacy specs as TPO underwriting rejects leads the loan model accepted.

- The bankruptcy chain – SunPower, Sunnova ($10 billion-plus debt), Mosaic, Lumio, PosiGen, Titan, Freedom Forever ($500 million-plus liabilities, 6.1 percent share at petition), and seven others – concentrates residual capacity in roughly six TPO platforms. Counterparty discipline is now baseline operating practice.

- Sunrun is the structural winner: roughly one-third of national subscription volumes, more than 50 percent of residential storage attach, 19,000 customers added in Q1 2026.

- Lead specs must be rewritten to TPO underwriting boxes: FICO 650 lease / 680 PPA, homeowner-of-record verified at capture, $80 minimum monthly utility bill, roof age and material captured in qualifier flow.

- The 10/25/40 diversification rule, ACH-on-delivery payment terms below credit thresholds, and trade credit insurance or non-recourse factoring are the contract changes that protect cash flow through the next wave of installer distress.

- Operators with single-vertical residential solar businesses should treat 2026 as the diversification window into storage-only, C&I solar, residential EV-charger, and electrification rebate programs. The lead-capture infrastructure translates cleanly; the residential solar market will not return to 2024 install volumes inside a five-year window on any reasonable forecast track.

---

## Sources

- [IRS FAQs for Modification of Sections 25C, 25D, 25E, 30C, 30D, 45L, 45W, and 179D under Public Law 119-21 (One Big Beautiful Bill, July 4, 2025)](https://www.irs.gov/newsroom/faqs-for-modification-of-sections-25c-25d-25e-30c-30d-45l-45w-and-179d-under-public-law-119-21-139-stat-72-july-4-2025-commonly-known-as-the-one-big-beautiful-bill-obbb)

- [IRS Residential Clean Energy Credit (Section 25D) program page](https://www.irs.gov/credits-deductions/residential-clean-energy-credit)

- [26 USC 25D: Residential Clean Energy Credit (U.S. Code, House Office of the Law Revision Counsel)](https://uscode.house.gov/view.xhtml?req=(title:26+section:25D+edition:prelim))

- [Congressional Research Service – Expiration and Carryforward Rules for the Residential Clean Energy Credit (Insight IN12611)](https://www.congress.gov/crs-product/IN12611)

- [SEIA and Wood Mackenzie – U.S. Solar Market Insight (Q2 2026 release and prior quarterly reports)](https://seia.org/research-resources/us-solar-market-insight/)

- [pv magazine USA – Sunnova Files for Bankruptcy (June 10, 2025)](https://pv-magazine-usa.com/2025/06/10/sunnova-files-for-bankruptcy/)

- [pv magazine USA – Residential Solar Company Freedom Forever Files Chapter 11 Bankruptcy (April 15, 2026)](https://pv-magazine-usa.com/2026/04/15/residential-solar-company-freedom-forever-files-chapter-11-bankruptcy/)

- [Latitude Media – Why Did Residential Solar Installer Freedom Forever Go Under?](https://www.latitudemedia.com/news/what-freedom-forevers-bankruptcy-says-about-residential-solar-today/)

- [Aurora Solar – TPO, OBBB, and Solar: Why Third-Party Ownership Has Never Been More Important](https://aurorasolar.com/tpo-obbb-and-solar-why-third-party-ownership-has-never-been-more-important/)

- [Sunrun Q1 2026 Operating and Financial Results (Earnings Presentation, May 6, 2026)](https://investors.sunrun.com/)

- [Sunrun Q1 2026 Earnings Transcript (Motley Fool)](https://www.fool.com/earnings/call-transcripts/2026/05/06/sunrun-run-q1-2026-earnings-transcript/)

- [pv magazine USA – Expiring Incentives Led to Record Demand, More Diverse Market for Residential Solar in 2025 (EnergySage data)](https://pv-magazine-usa.com/2026/02/27/expiring-incentives-led-to-record-demand-more-diverse-market-for-residential-solar-in-2025-says-energysage/)

- [One Big Beautiful Bill Act (H.R. 1, 119th Congress, Public Law 119-21)](https://www.congress.gov/bill/119th-congress/house-bill/1)

- [pv-tech – Third-Party Ownership and Strong Market Fundamentals Drive 'New Shape of Solar' in US Residential Sector](https://www.pv-tech.org/third-party-ownership-strong-market-fundamentals-drive-new-shape-of-solar-us-residential/)

- [Solar Power World – Solar Layoffs and Closures Run Rampant in Trump's First Year Back (January 2026)](https://www.solarpowerworldonline.com/2026/01/solar-layoffs-and-closures-run-rampant-in-trumps-first-year-back/)