Master the distinct requirements, economics, and operational realities of selling leads to direct carriers versus independent agencies. Understanding these buyer differences determines whether you build sustainable relationships or burn through partners.

When Progressive spent $3.5 billion on advertising in 2024 – nearly tripling their investment from the prior year – they were not simply buying television commercials. They were fueling a sophisticated lead acquisition machine that operates by fundamentally different rules than the independent agent down the street purchasing 50 leads monthly to grow their book of business.

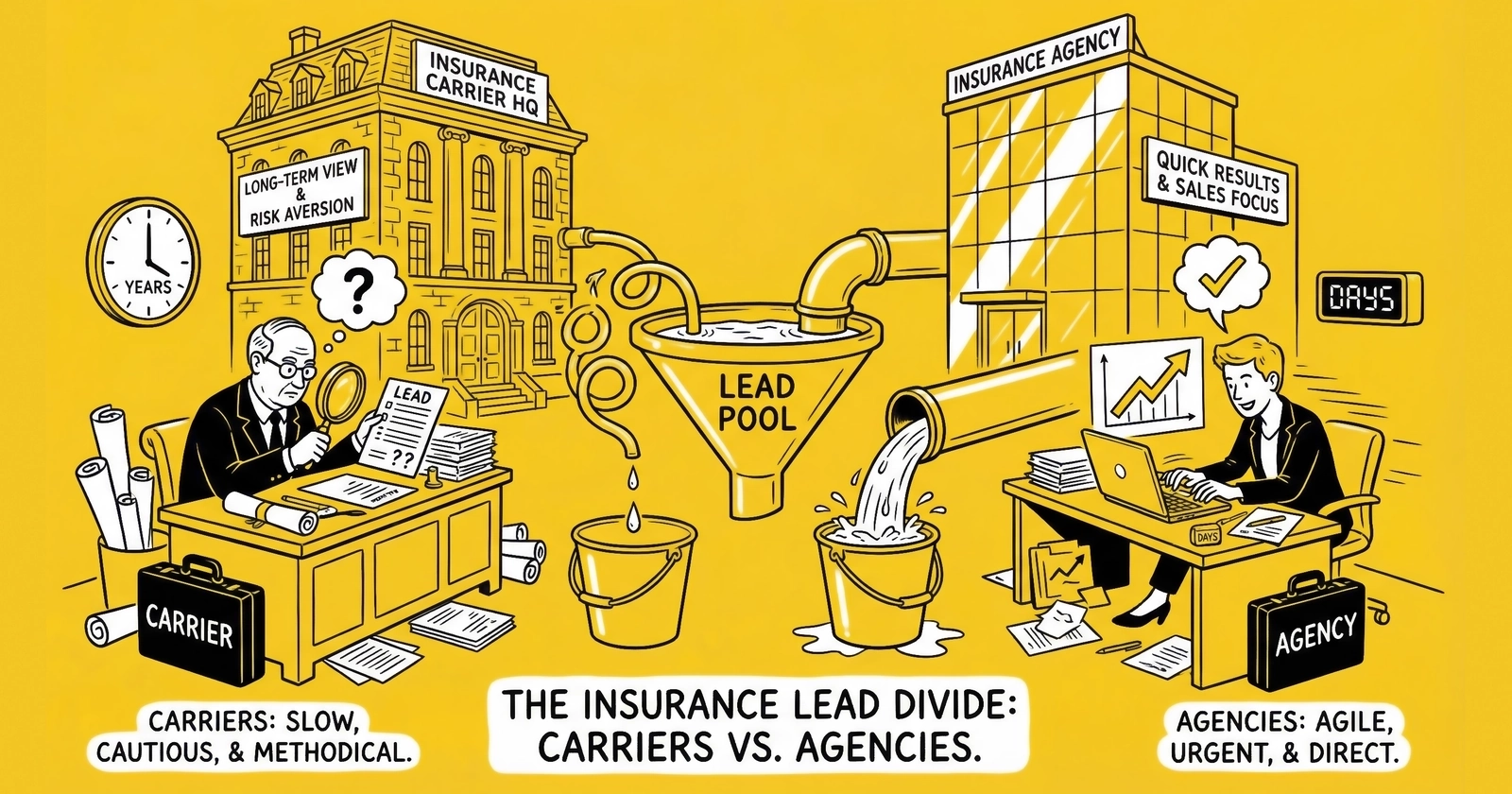

These two buyer types represent the extremes of insurance lead distribution. One operates massive call centers staffed around the clock, processes thousands of leads daily, and negotiates pricing through procurement departments with spreadsheets measuring performance to the third decimal place. The other works from a local office, builds relationships over coffee meetings, and decides on lead purchases based on gut feel and last month’s close rate.

If you generate or broker insurance leads, you will eventually sell to both. Those who thrive understand that these buyers have different requirements, different economics, and different definitions of success. What delights a carrier buyer frustrates an agency buyer – and vice versa. Building a sustainable lead business requires fluency in both languages.

This guide provides the operational intelligence you need to serve both buyer types effectively: the technical requirements, the commercial dynamics, the relationship patterns, and the strategic considerations that determine whether partnerships last months or years.

Understanding the Insurance Lead Buyer Landscape

The insurance lead market supports an estimated $5.2-6.8 billion in annual transaction value across all sub-verticals, with auto insurance alone representing $3-4 billion. This demand flows through two primary buyer channels: direct carriers purchasing leads for their in-house sales operations, and independent agencies purchasing leads to grow their books of business.

Understanding how these channels differ begins with recognizing what they have in common. Both buyer types want leads that convert to customers at acceptable cost-per-acquisition ratios. Both require compliant consent documentation that protects them from TCPA liability. Both evaluate lead quality through measurable metrics: contact rates, conversion rates, and return rates.

The differences emerge in how they pursue these common goals – and in the scale, sophistication, and relationship dynamics that govern their purchasing behavior.

The Carrier Direct Channel

Direct carriers – Progressive, GEICO, Allstate Direct, State Farm Direct, and similar operations – purchase leads to feed their own sales organizations. These are the insurance companies themselves, not intermediaries or distribution partners.

Carrier direct buyers share defining characteristics that shape every aspect of the relationship. The scale of these operations is staggering – major carriers process thousands to tens of thousands of leads daily, with Progressive’s record advertising spend in 2024 fueling lead acquisition at volumes that dwarf most lead generators’ total production. A carrier might purchase more leads in a single day than a mid-sized agency purchases in a year.

Behind this volume sits sophisticated technology infrastructure: predictive dialers, AI-powered lead scoring, CRM systems integrated with policy administration platforms, and real-time analytics dashboards. Carriers expect lead providers to integrate seamlessly with this infrastructure through well-documented APIs. Their purchasing flows through formalized vendor management processes where contracts specify performance requirements, service level agreements, and penalty structures. Relationship decisions involve multiple stakeholders – marketing, operations, compliance, procurement – each with different priorities.

These buyers measure everything. They track conversion by source, geography, time of day, lead score, and dozens of other dimensions, knowing within weeks whether a lead source performs. They will adjust volume or terminate relationships based on data alone. And while individual lead prices may be lower than what agencies pay, the aggregate spend is massive – a penny per lead difference at carrier volume translates to millions annually. Procurement teams negotiate aggressively on price.

The Independent Agency Channel

Independent insurance agents and agency networks represent the other end of the buyer spectrum. These are licensed professionals who sell products from multiple carriers, building local or regional books of business.

Agency buyers share their own defining characteristics that create a fundamentally different relationship dynamic. The scale is human – most independent agents purchase 20 – 200 leads monthly, with larger agencies buying 500 – 1,000 leads monthly across their agent roster. Even substantial agency networks operate at fractions of carrier volume.

Technology adoption varies wildly across this segment. Some agencies run sophisticated operations with integrated CRMs, automated follow-up sequences, and performance tracking. Others work from spreadsheets and sticky notes. Lead providers cannot assume any particular technology capability. Purchasing decisions follow relationship patterns rather than procurement processes – agents often choose lead providers based on personal relationships, referrals from colleagues, or past experiences. The decision-maker is typically the agency owner or sales manager, not a committee.

These buyers generally prefer exclusive leads at higher prices over shared leads at lower prices, since they lack the call center infrastructure to compete on speed with major carriers. Instead, they compete on service quality and relationship building. Agency buyers accept higher per-lead pricing than carriers because they are not negotiating at carrier volume; they evaluate lead costs against their own close rates and commission structures.

Economic Differences: What Each Buyer Will Pay

Lead pricing strategies must account for fundamentally different economics between carrier and agency buyers. Understanding these economics helps you position appropriately and avoid the margin destruction that comes from misaligned pricing.

Carrier Pricing Economics

Direct carriers evaluate leads on fully loaded cost-per-acquisition (CPA) metrics that account for contact rates, conversion rates, and customer lifetime value. Their pricing tolerance reflects their operational efficiency and LTV calculations.

Typical carrier pricing ranges for auto insurance leads:

- Shared leads: $15-30 per lead

- Exclusive leads: $35-60 per lead (when purchased at volume)

- Live transfers: $80-150 per transfer

These prices reflect several carrier advantages that compound to justify their pricing discipline. Speed-to-contact capability stands paramount – carriers can respond to leads within 30 – 60 seconds using predictive dialers and dedicated response teams. Research shows leads contacted within one minute convert 391% higher, and this speed advantage means carriers extract more value from each lead.

Conversion efficiency amplifies this advantage. With optimized sales scripts, extensive product training, and sophisticated call routing, carriers convert at higher rates than typical agencies. A carrier achieving 12% conversion can pay less per lead than an agency converting at 8% while maintaining similar CPA. Volume leverage further strengthens their position – carriers purchasing 5,000 leads daily command pricing power that smaller buyers cannot match. Their volume represents must-have demand for lead generators, and losing a carrier relationship can mean losing a significant percentage of revenue overnight. Finally, carriers provide detailed conversion data that helps lead generators optimize quality, creating value for generators that partially offsets lower pricing.

Agency Pricing Economics

Independent agents operate with different constraints and opportunities that support different pricing:

Typical agency pricing ranges for auto insurance leads:

- Shared leads: $25-40 per lead

- Exclusive leads: $50-100 per lead

- Live transfers: $120-200 per transfer

Agencies pay more per lead for several interconnected reasons. The value of exclusive distribution dominates – agents strongly prefer exclusive leads because they cannot compete with carrier call centers on speed. The premium for exclusivity, often 2 – 3x shared lead pricing, reflects the genuine competitive advantage of being the only agent contacting a prospect.

Relationship-based sales create additional value that carriers cannot replicate. A local agent who writes auto insurance today may capture home, umbrella, and life policies over time, and this cross-selling opportunity increases customer lifetime value beyond what carriers achieve with single-product direct sales. Higher commission structures support the economics – independent agents typically earn 10 – 15% first-year commission on auto policies, with renewal commissions continuing for the customer lifetime. Captive carrier agents often earn lower per-policy compensation, and the margin difference supports higher lead investment. Meanwhile, agents purchasing 50 leads monthly have no negotiating leverage based on volume; they accept market pricing for their purchase tier.

The Pricing Strategy Implications

Smart lead generators serve both channels with differentiated pricing through a tiered approach. Premium exclusive inventory routes to agents at $60 – 100 per lead, featuring verified contact information, documented TCPA consent, and no competition for the prospect’s attention. Volume shared inventory routes to carrier call centers at $18 – 30 per lead, with these leads selling to 3 – 5 buyers simultaneously as carriers compete on speed-to-contact. Aged and recycled inventory serves specialized remarketers and training operations at $3 – 12 per lead, extracting residual value from leads that did not convert initially. This tiered approach maximizes yield across your lead inventory while serving buyers at their preferred price points.

Technical Integration Requirements

The technology requirements for carrier versus agency relationships differ substantially. Carrier integrations require significant development investment but enable high-volume, high-efficiency operations. Agency integrations are simpler but require flexibility across diverse buyer systems.

Carrier Integration Requirements

Major carriers expect lead generators to meet demanding technical specifications across multiple dimensions. Real-time API delivery is non-negotiable – carriers require leads delivered via API within seconds of capture, since batch file delivery is generally unacceptable for fresh leads. They need real-time transmission to capitalize on their speed-to-contact advantage.

Most carrier relationships operate through ping/post protocols, where you ping the carrier with partial lead data (ZIP code, driver age, current coverage status), receive a bid based on their current demand and capacity, then post the full lead data to the winning bidder. This real-time auction model requires sophisticated technical infrastructure alongside precise field mapping – carrier APIs expect specific data formats for date fields, phone numbers, and state codes. Field mapping errors cause integration failures and rejected leads.

Robust error handling rounds out the technical requirements. Carrier systems experience occasional downtime, so your integration must implement intelligent retry logic with exponential backoff, circuit breaker patterns, and failover to secondary buyers when primary endpoints are unavailable. Carriers also require secure API authentication, typically OAuth 2.0 or API key-based, with IP whitelisting, encryption in transit, and data security compliance often contractually required. Some carriers provide conversion feedback through APIs, enabling closed-loop optimization – supporting these feedback mechanisms requires additional development but enables quality improvement.

The timeline to establish carrier integration typically spans 3 – 6 months from initial conversation to live traffic. Technical due diligence, legal review, compliance certification, integration development, and testing all require time. Plan accordingly.

Agency Integration Requirements

Agency integrations are technically simpler but operationally more varied. Many agencies prefer web portal delivery where leads appear in a dashboard they access via browser, with portal systems supporting mobile access, lead assignment across agent rosters, and activity tracking. Agencies using platforms like AgencyZoom, EZLynx, or Hawksoft may request direct CRM integration – these integrations are typically simpler than carrier APIs but require supporting multiple destination platforms.

Some agencies accept leads via email or daily batch files, and while less sophisticated, this delivery method serves agencies without technical resources for API integration. Portal features that enable immediate calling prove valuable – one-click dial from the lead record, call logging, and integration with telephony systems where available. Unlike carriers, agencies care less about rigid field formatting than about seeing all relevant lead information clearly; display fields in human-readable formats rather than system-optimized codes.

The timeline to onboard agency buyers is typically 1 – 2 weeks, much faster than carrier relationships. The lower technical bar enables rapid relationship development.

Platform Selection Considerations

Supporting both buyer types requires distribution platform capabilities across several dimensions. Multi-buyer routing allows you to route high-value leads to exclusive agency buyers while routing remaining inventory to shared carrier distribution, with dynamic routing based on lead characteristics, buyer capacity, and bid prices optimizing yield. Delivery method flexibility means supporting real-time API delivery for carriers, portal access for agencies, and batch delivery for specialized buyers – all from a single lead management platform.

Return handling demands particular attention since both buyer types return leads but for different reasons and at different rates. Carriers return leads that fail technical validation; agencies return leads they cannot contact. Your platform must handle return processing for both patterns. Performance reporting by buyer segment rounds out the requirements, tracking metrics separately for carrier versus agency relationships since different benchmarks apply to each segment. Leading platforms like boberdoo, LeadsPedia, and Phonexa support these requirements, though configuration complexity varies.

Relationship Dynamics and Sales Cycles

Building relationships with carriers versus agencies follows different patterns. Understanding these dynamics helps you allocate sales resources appropriately and set realistic expectations for new business development.

Carrier Relationship Development

Establishing carrier relationships is a lengthy process with significant upfront investment:

Long sales cycles. Expect 6-12 months from initial outreach to first lead delivery. Carriers evaluate vendors thoroughly before committing purchasing authority. Multiple stakeholders – marketing, operations, compliance, procurement, legal – must approve new vendor relationships.

Formal vendor qualification. Carriers require documentation of your compliance practices, technology infrastructure, data security measures, and business stability. Questionnaires running dozens of pages are common. Site visits may be required for significant relationships.

Contract negotiation. Carrier contracts specify service level agreements (SLAs), performance benchmarks, pricing structures, return policies, indemnification requirements, and termination conditions. Legal review on both sides extends timelines.

Pilot program structure. Most carriers begin with limited pilot programs – perhaps 500-1,000 leads over 30-60 days – before committing to volume. Pilot performance determines whether the relationship expands, continues at pilot scale, or terminates.

Ongoing performance review. Carriers conduct regular business reviews – monthly or quarterly – examining performance metrics, addressing quality issues, and negotiating terms. Prepare data showing your performance, competitive positioning, and optimization initiatives.

Single point of failure risk. A single carrier relationship may represent 20-40% of your revenue. Losing that relationship – due to carrier budget cuts, underwriting cycle changes, or internal reorganization – creates immediate financial stress. Diversification across multiple carrier relationships provides stability.

Agency Relationship Development

Agency relationships develop faster but require different approaches:

Short sales cycles. Agency decision-makers often approve new lead sources within days or weeks. The decision authority sits with the agency owner or sales manager – one person, not a committee.

Relationship-based selling. Agencies choose lead providers based on trust, referrals, and personal connection. Conference networking, industry events, and referral programs drive agency customer acquisition more effectively than formal RFP processes.

Low barrier trial programs. Agencies typically start with small volume – 25-50 leads – to evaluate quality before scaling. Low minimum commitments reduce the risk of testing new sources.

Hands-on support expectations. Agency buyers expect accessible customer service. When leads have issues, they want to reach a human who can resolve problems quickly. Automated ticketing systems frustrate agency customers accustomed to personal service.

Loyalty and switching costs. Agencies satisfied with lead quality and service develop loyalty that transcends pure price competition. Building trust over months of consistent delivery creates stickiness that protects against competitor poaching.

Volume fragmentation. Serving agencies means managing many small relationships rather than few large ones. An agency portfolio of 100 buyers purchasing 50 leads monthly each creates different operational challenges than 5 carriers purchasing 30,000 leads monthly each.

Resource Allocation Implications

These relationship dynamics suggest different organizational approaches:

Carrier-focused operations require dedicated enterprise sales resources with long-term relationship perspectives, technical implementation teams capable of complex integrations, and account management capacity for formal business reviews.

Agency-focused operations require scalable customer acquisition (marketing, inside sales, referral programs), efficient onboarding processes that handle volume, and responsive customer service that maintains relationship quality across many accounts.

Most sustainable lead businesses serve both segments, balancing carrier volume with agency margin while managing the distinct operational requirements of each.

Quality Requirements and Return Policies

Carriers and agencies evaluate lead quality differently and have different return patterns. Understanding these differences helps you manage quality, set appropriate return policies, and avoid disputes.

Carrier Quality Standards

Carriers impose rigorous quality requirements backed by contractual enforcement:

Validation requirements. Carriers require phone validation (carrier lookup, line type verification), email validation, and address verification before accepting leads. Leads failing validation are rejected at delivery or returned immediately.

Consent documentation. TrustedForm or Jornaya certificates are typically required. Carriers may specify exact consent language that must appear on lead capture forms. Non-compliant consent creates TCPA liability that carriers will not accept.

Fraud detection. Carriers monitor for fraud indicators: bot traffic patterns, duplicate submissions, velocity attacks, and synthetic identities. Sources generating fraudulent leads face immediate termination and potential clawback of previously paid leads.

Return rate thresholds. Carrier contracts typically specify maximum acceptable return rates – often 8-12%. Sustained return rates above threshold trigger relationship review or termination. Some contracts include financial penalties for excess returns.

Quality scoring. Carriers may implement quality scores based on their conversion data, adjusting bid prices or volume allocation based on source-level performance. Sources with declining quality scores see demand reduction before formal relationship termination.

Compliance audits. Carriers periodically audit lead generation practices, reviewing landing pages, consent flows, and traffic sources. Audit failures – even for issues that never caused lead problems – can terminate relationships.

Agency Quality Standards

Agency quality expectations are less formalized but equally important:

Contact quality. Agencies care intensely about reaching consumers. Leads with working phone numbers that answer calls represent quality. Leads with disconnected numbers, wrong numbers, or persistent non-answers represent failure – regardless of validation status at time of sale.

Information accuracy. Agents quote based on lead form data. When consumers’ actual situations differ from form submissions – different vehicle, different address, different driving history – quoting becomes difficult and conversion probability drops.

Timeliness. Agencies purchasing exclusive leads expect freshness. A lead marked as real-time that actually originated hours earlier frustrates agents who invest in rapid response infrastructure.

Return flexibility. Agencies expect reasonable return policies for leads with clear quality issues: disconnected phones, wrong numbers, consumers who deny requesting information. Rigid return policies damage agency relationships.

Managing Return Rate Differences

Return patterns differ between buyer types:

Carrier returns tend to be systematic: validation failures, duplicate detection, technical integration issues. Return rates are relatively consistent and predictable once integration is stable.

Agency returns tend to be circumstantial: specific leads with contact problems, disputed lead quality, agent capacity issues. Return rates vary more widely based on individual agent performance and market conditions.

Successful return management requires:

Clear return policies documented in buyer agreements, specifying valid return reasons, return windows (typically 24-72 hours for agencies, 5-7 days for carriers), and return processing procedures.

Rapid return processing that credits buyer accounts promptly and routes returned leads to secondary buyers or aged inventory pools.

Return rate monitoring by source identifying lead sources generating excessive returns and addressing quality issues before they damage buyer relationships.

Return reason analysis distinguishing valid quality issues (contact problems, fraud) from buyer cherry-picking (returning leads they simply could not close). Push back on illegitimate returns while quickly resolving genuine quality issues.

Compliance Considerations by Buyer Type

TCPA compliance requirements apply to all insurance lead generation, but carrier and agency buyers have different risk tolerances and different compliance infrastructure.

Carrier Compliance Requirements

Carriers face substantial TCPA exposure given their call volume and visibility. They impose strict compliance requirements on lead sources:

One-to-one consent. Though the FCC’s one-to-one consent rule was vacated and repealed, CMS requirements for Medicare remain in effect, and carriers increasingly require one-to-one consent identifying the specific entity authorized to contact the consumer. Blanket consent to “partners” may not satisfy carrier requirements.

Consent language approval. Carriers may require approval of exact consent language appearing on your lead capture forms. Changes to consent language may require re-approval before continuing lead delivery.

TrustedForm or Jornaya certification. Independent consent verification is typically mandatory. Carriers require certificates validating that consumers actually completed forms and saw required disclosures.

Consent documentation retention. Carriers require lead generators to retain consent documentation for extended periods – typically 5 years or longer – and to produce documentation promptly if TCPA claims arise.

Indemnification provisions. Carrier contracts typically require lead generators to indemnify carriers for TCPA claims arising from lead generation practices. This transfers litigation risk from carrier to generator, making robust compliance essential for protecting your own business.

Compliance audits. Carriers audit compliance practices, reviewing consent flows, landing pages, and documentation procedures. Audit failures create relationship risk beyond specific lead quality issues.

Agency Compliance Expectations

Agencies have similar compliance concerns but less formal enforcement mechanisms:

TCPA awareness. Sophisticated agencies understand TCPA requirements and expect compliant leads. Less sophisticated agencies may not fully understand compliance requirements, creating education opportunities.

Documentation requests. Agencies may request consent certificates for specific leads when consumers dispute receiving calls. Your ability to produce documentation quickly affects agency perception of your compliance infrastructure.

Return rights for compliance issues. Agencies expect return rights for leads with compliance deficiencies – missing consent documentation, problematic consent language, or consumers who deny requesting contact.

Liability concerns. Independent agents face personal liability for TCPA violations. Agents who experience TCPA claims (or near-misses) become highly sensitive to lead source compliance.

Compliance Infrastructure Investment

The compliance requirements of carrier relationships often set the standard for your entire operation:

TrustedForm or Jornaya implementation becomes mandatory when carriers require it – and once implemented, extends to all leads regardless of destination.

Consent language standardization across all lead capture forms simplifies compliance management and reduces the risk of non-compliant leads entering distribution.

Documentation retention systems capable of producing consent certificates for any lead within 24-48 hours protect against both carrier audits and agency disputes.

Compliance monitoring processes that regularly review landing pages, consent flows, and traffic sources catch issues before they create liability.

The investment in compliance infrastructure required for carrier relationships benefits agency relationships as well, providing competitive advantage against less sophisticated lead generators.

Building a Diversified Buyer Portfolio

Sustainable lead businesses serve both carrier and agency buyers, balancing the advantages of each channel while managing the distinct risks.

The Case for Carrier Relationships

Carrier relationships provide several strategic advantages:

Volume capacity. Carriers can absorb lead volume that would overwhelm agency distribution. Scaling production requires buyers capable of scaling purchases.

Predictable demand. Carrier purchasing is contractual and systematic. Committed volume provides revenue predictability that supports business planning.

Performance feedback. Carrier conversion data enables quality optimization that improves performance across all buyer channels.

Market validation. Major carrier relationships validate lead quality to the broader market. If Progressive buys your leads, agencies assume quality meets acceptable standards.

The Case for Agency Relationships

Agency relationships provide complementary advantages:

Margin quality. Agency pricing supports higher margins per lead. A portfolio generating $0.50 margin per carrier lead and $15 margin per agency lead needs both channels for overall margin health.

Relationship stability. Agency relationships based on trust and service quality are less vulnerable to procurement-driven vendor switching than carrier relationships.

Inventory optimization. Premium leads command premium pricing from agencies. Tiered distribution – best leads to agencies, remaining inventory to carriers – maximizes yield.

Revenue diversification. A portfolio of 50 agency relationships diversifies revenue more effectively than 3 carrier relationships representing equivalent volume.

Portfolio Balance Considerations

The optimal mix depends on your operational capabilities and strategic priorities:

Volume-oriented operations may target 70-80% carrier, 20-30% agency. The scale efficiency of carrier operations aligns with high-volume business models.

Margin-oriented operations may target 40-60% carrier, 40-60% agency. Higher agency concentration increases per-lead margin at the cost of reduced volume capacity.

Diversification-focused operations intentionally limit any single buyer to 15-20% of revenue, accepting some margin dilution for reduced concentration risk.

Market conditions affect optimal mix. When carrier advertising budgets expand (as in 2024’s surge), carrier channels offer growth opportunity. When carriers contract, agency channels provide revenue stability.

Managing Channel Conflict

Serving both channels creates potential conflicts:

Exclusivity expectations. Agents paying premium prices for exclusive leads expect genuine exclusivity. Routing the same lead to an agency and a carrier – even with time delay – violates that expectation.

Quality perception. Carriers receiving leads that agents rejected (or vice versa) may perceive quality issues that do not actually exist. Separate lead routing by quality tier, not by buyer availability.

Pricing transparency. Agents learning that carriers pay $20 for leads they pay $70 for may demand price adjustments. Position pricing based on value delivered (exclusivity, service, relationship) rather than pure lead cost.

Clear lead routing logic, honest buyer communication, and consistent quality standards across channels minimize conflict risk.

Strategic Considerations for Lead Generators

Understanding carrier versus agency buyers informs strategic decisions across your lead generation operation.

Traffic Acquisition Strategy

Buyer type affects traffic strategy:

High-volume channels (Google Ads at scale, programmatic networks, large publisher relationships) align with carrier demand. Carriers need predictable volume; these channels deliver it.

Quality-focused channels (SEO content, targeted social campaigns, selective affiliate relationships) align with agency demand. Agencies pay for quality; these channels can deliver premium leads at premium prices.

Mixed strategies combining volume and quality channels serve diversified buyer portfolios. Optimize channel mix based on current buyer demand and pricing.

Form and Landing Page Design

Buyer requirements affect lead capture:

Carrier-optimized forms prioritize completion rate and data standardization. Carriers process leads algorithmically; consistent data formatting matters more than conversational framing.

Agency-optimized forms may prioritize lead quality signals over completion rate. Agents value qualified leads over raw volume; forms that filter out low-intent consumers may improve agency conversion rates.

Consent language must satisfy the most stringent buyer requirements. If carriers require one-to-one consent, implement it universally rather than maintaining multiple consent flows.

Technology Investment Priorities

Buyer mix affects technology priorities:

Carrier-focused operations invest heavily in API infrastructure, real-time delivery systems, and ping/post auction platforms.

Agency-focused operations invest in portal systems, agent assignment logic, and customer service infrastructure.

Diversified operations require both capabilities, with the carrier-focused infrastructure typically requiring greater investment.

Sales and Account Management Structure

Buyer types require different sales approaches:

Carrier sales requires enterprise sales skills: long relationship cycles, multiple stakeholder management, formal proposal processes, and patience measured in quarters.

Agency sales requires volume sales skills: efficient prospecting, quick qualification, simple onboarding, and relationship maintenance across many accounts.

Organizations serving both channels often separate these functions, with dedicated enterprise teams for carrier development and inside sales or marketing-driven approaches for agency customer acquisition.

Frequently Asked Questions

What is the difference between selling leads to insurance carriers versus independent agencies?

Direct carriers purchase leads at high volume (thousands daily) through sophisticated technology integrations, with lower per-lead pricing offset by massive scale. Independent agencies purchase leads at lower volume (20-500 monthly) through simpler delivery methods, paying premium prices for exclusive distribution and personal service. Carriers require real-time API delivery and formal vendor contracts; agencies accept portal access and relationship-based purchasing. Understanding these differences enables appropriate positioning for each buyer type.

How much do insurance carriers pay for leads compared to agencies?

Carriers typically pay $15-30 for shared auto insurance leads and $35-60 for exclusive leads at volume. Agencies typically pay $25-40 for shared leads and $50-100 for exclusive leads. Live transfers command $80-150 from carriers and $120-200 from agencies. The pricing difference reflects carrier advantages in volume negotiation and operational efficiency, while agencies pay premiums for exclusivity and service quality.

How long does it take to establish a carrier lead buying relationship?

Carrier relationships typically require 6-12 months from initial outreach to first lead delivery. This timeline includes vendor qualification (1-2 months), contract negotiation (2-3 months), technical integration (2-4 months), and pilot testing (1-2 months). Multiple stakeholders – marketing, operations, compliance, procurement – must approve new vendor relationships. Plan resource allocation accordingly.

What technical requirements do carriers have for lead delivery?

Carriers require real-time API delivery, ping/post auction capability, precise field mapping to their data formats, OAuth 2.0 or API key authentication, and intelligent error handling with retry logic. Integration development typically requires 2-4 months of engineering work. Carriers may also require IP whitelisting, encryption in transit, and security compliance documentation.

Do agencies require the same lead quality as carriers?

Both buyer types want leads that convert, but they measure quality differently. Carriers emphasize validation compliance, fraud detection, and systematic quality scoring based on conversion data. Agencies emphasize contact quality (can they reach the consumer?), information accuracy (does the lead match reality?), and timeliness (is the lead fresh?). Both require TCPA-compliant consent documentation, though carrier requirements tend to be more formally specified.

What return rates should I expect from carriers versus agencies?

Carrier return rates typically stabilize at 8-12% once integration is established, with returns driven by validation failures and duplicate detection. Agency return rates vary more widely (5-20%) based on individual agent performance and market conditions, with returns driven by contact problems and perceived quality issues. Clear return policies, rapid return processing, and source-level quality monitoring help manage returns from both buyer types.

How do I price leads for carrier versus agency buyers?

Price carriers based on volume, competitive positioning, and your cost structure – recognizing that carrier volume represents must-have demand worth pricing competitively. Price agencies based on value delivered: exclusivity commands 2-3x shared pricing, verified contact information supports premium positioning, and responsive service justifies margin that covers higher support costs. Tier your inventory with premium leads to agencies at higher prices and remaining inventory to carriers at volume pricing.

Should I focus on carriers or agencies when building a lead business?

Most sustainable lead businesses serve both channels. Carriers provide volume capacity, predictable demand, and performance feedback. Agencies provide margin quality, relationship stability, and revenue diversification. The optimal mix depends on your operational capabilities and strategic priorities. Consider targeting 40-60% carrier and 40-60% agency for balanced diversification, adjusting based on your specific advantages and market conditions.

What compliance requirements differ between carrier and agency relationships?

Carriers impose stricter formal compliance requirements: one-to-one consent language, TrustedForm/Jornaya certification, consent documentation retention, compliance audits, and indemnification provisions in contracts. Agencies have similar concerns but less formal enforcement. The compliance infrastructure required for carrier relationships typically exceeds agency requirements – but once built, benefits all buyer relationships through reduced TCPA risk and competitive differentiation.

How do carrier advertising cycles affect lead buying behavior?

Carrier lead purchasing directly correlates with advertising budgets, which respond to underwriting results. When carriers are profitable (combined ratios below 100%), they expand advertising and lead purchasing aggressively – as Progressive demonstrated with their 187% spending increase in 2024. When carriers face underwriting losses, they cut advertising and lead demand contracts. Lead generators dependent on single carriers face substantial risk when that carrier’s strategy shifts. Agency relationships provide relative stability during carrier contraction cycles.

Key Takeaways

-

Carrier and agency buyers operate by fundamentally different rules. Carriers purchase at massive scale with sophisticated technology, lower per-lead pricing, and formal procurement processes. Agencies purchase at human scale with simpler delivery, premium pricing for exclusivity, and relationship-based purchasing. Serving both requires understanding their distinct requirements.

-

Pricing strategies must reflect buyer economics. Carriers paying $20 for shared leads command pricing through volume leverage. Agencies paying $75 for exclusive leads pay for genuine competitive advantage. Tier your inventory with premium leads to agencies and volume inventory to carriers to maximize yield.

-

Technical integration requirements differ substantially. Carriers require real-time API delivery, ping/post capability, and months of integration development. Agencies accept portal access, email delivery, and can be onboarded in weeks. Support both delivery methods from a unified platform.

-

Relationship development follows different timelines. Carrier relationships require 6-12 months from first contact to first lead. Agency relationships develop in days or weeks. Allocate sales resources accordingly, with enterprise skills for carriers and volume skills for agencies.

-

Quality expectations vary but compliance requirements are universal. Carriers impose formal quality standards with contractual enforcement. Agencies emphasize practical contact quality. Both require TCPA-compliant consent – implement the highest standard universally.

-

Diversification across both channels provides strategic stability. Carrier relationships provide volume and predictability. Agency relationships provide margin and diversification. Balance the portfolio based on your capabilities and risk tolerance.

-

Market conditions shift buyer behavior. Carrier advertising cycles driven by underwriting results create feast-or-famine dynamics. Agency purchasing is more stable but represents smaller individual relationships. Monitor carrier behavior through public filings and earnings commentary to anticipate market shifts.

Sources

- MediaAlpha Investor Relations - Publicly traded insurance lead exchange reporting $864.7M revenue and $1.5B transaction value for 2024

- Allstate Investors - Major carrier financial disclosures and advertising spend data

- Harvard Business Review: The Short Life of Online Sales Leads - Research on lead response timing and the 391% conversion improvement for speed-to-contact

- Investopedia: Combined Ratio - Definition of combined ratio metric used for carrier underwriting profitability analysis

- TrustedForm by ActiveProspect - Consent documentation platform required by carriers for TCPA compliance

- Verisk (Jornaya) - LeadiD platform for consent verification and lead journey tracking

- boberdoo - Lead distribution platform supporting carrier and agency integrations

- LeadExec - Scalable, automated lead capture, validation, routing, and distribution platform

Statistics and market information current as of 2025. Carrier advertising spend, pricing benchmarks, and regulatory requirements change – verify current conditions before making significant business decisions.