# Martech Peak Plateau – 15,505 Products, 1,367 Removed, and What the AI-Driven Shakeout Means for Lead Generation

> **Canonical:** https://www.leadgen-economy.com/blog/martech-peak-plateau-15505-products-ai-shakeout-2026/

> **Published:** 2026-06-15

> **Author:** Alex Paddington

> **Source:** LeadGen Economy – https://www.leadgen-economy.com

---

*The supergraphic that grew a hundredfold in 15 years grew under 1 percent in 2026 – and the category-level churn underneath the flat headline tells the operator story the headline misses.*

---

## What the May 2026 Supergraphic Actually Shows

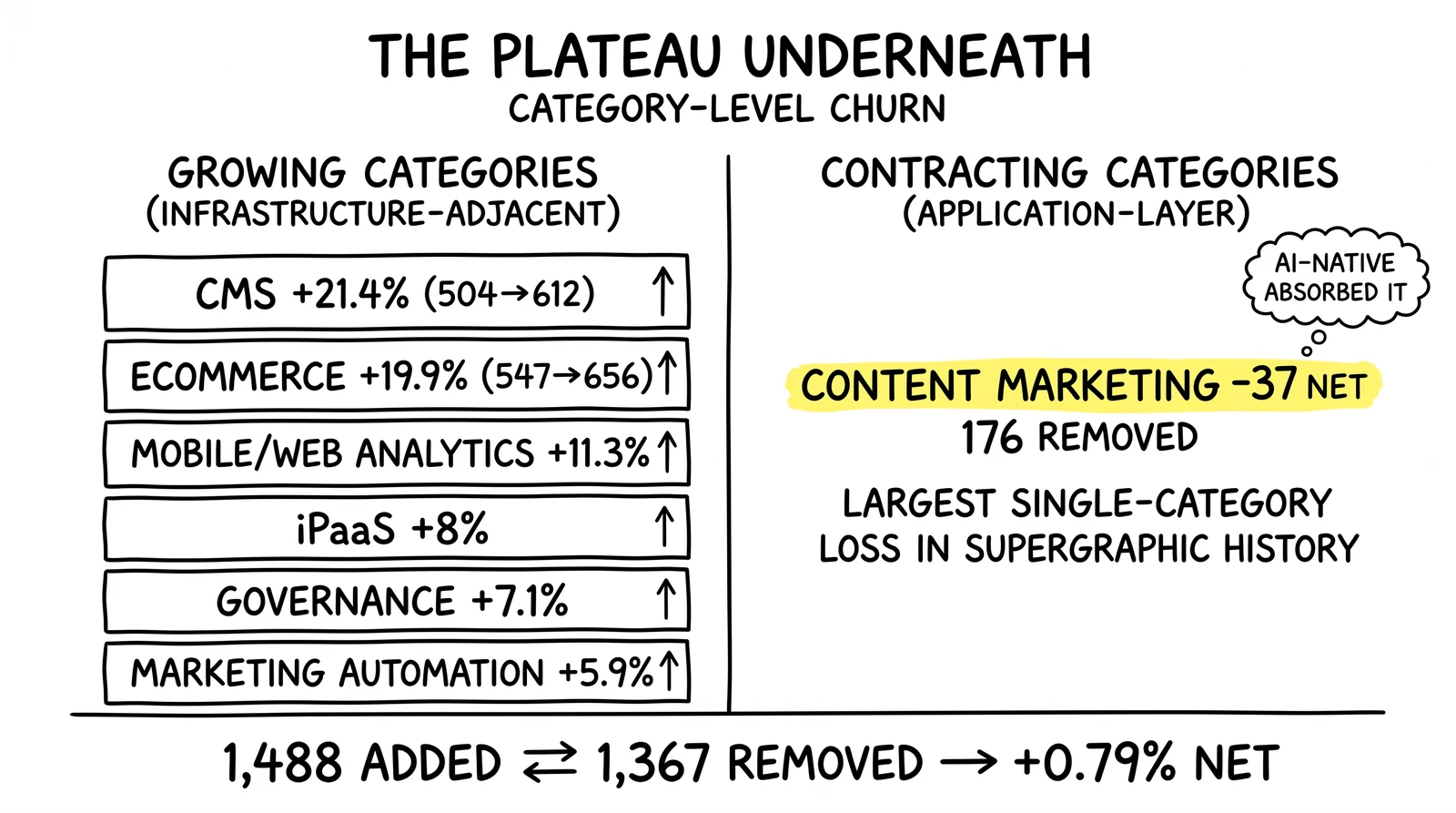

Scott Brinker published the 2026 chiefmartec Marketing Technology Landscape Supergraphic in May 2026 as the 15th annual edition of the canonical industry map. The headline number – 15,505 products – landed only 0.79 percent above the prior year's 15,384. The category that began with 150 solutions in 2011 grew under 1 percent year-over-year for the first time in the supergraphic's measurement history.

The flat headline conceals the activity underneath. The 2026 edition documented 1,488 additions against 1,367 removals. Additions fell 40 percent from the 2,489 added in the 2025 edition. Removals rose 13 percent from the 1,211 removed the prior year. The category did not stall; it churned. New vendors continued to launch into 2026 at substantial volume, and existing vendors continued to fail or exit at rising volume. The two flows nearly cancel, producing the appearance of stability while the underlying composition reshapes.

Brinker's framing was direct: "AI doesn't make martech complexity go away. It exposes it." The line, quoted in CMSWire's May 5 coverage, names the structural mechanism. AI's arrival did not consolidate the category – it accelerated both vendor formation in agent-native categories and vendor failure in categories where AI absorbed the workflow surface. Brinker's secondary framing of the landscape as a river rather than a lake reinforces the point. The total volume held steady; the composition flowed.

For lead-generation operators, the operational question is which categories grew, which contracted, and what the churn means for the infrastructure decisions sitting in front of 2027 planning conversations. The MarTech.org June 10 follow-up by Pamela Parker provided the first published agent-readiness scoring of specific vendors, completing the analytical frame the supergraphic raw counts cannot.

The 0.79 percent plateau hides bifurcation. Infrastructure categories grew double-digits; Content Marketing lost 176 – the largest single-category contraction the supergraphic has measured.

---

## Which Categories Grew, Which Contracted

The category-level cuts from the 2026 supergraphic produce a clear infrastructure-versus-application pattern. Content Management Systems grew 21.4 percent from 504 to 612 products. Ecommerce grew 19.9 percent from 547 to 656. Mobile and Web Analytics grew 11.3 percent. iPaaS grew 8 percent. Governance grew 7.1 percent. Marketing Automation grew 5.9 percent.

The growth categories share an infrastructure-adjacent quality. CMS, Ecommerce, Mobile and Web Analytics, and iPaaS sit at the data-layer-and-protocol-layer side of the stack. They support agent-mediated activation rather than performing it directly. The category growth signals that vendors are positioning to be the surface AI agents read and write against, rather than the surface that contains the agent decisioning.

The contraction was concentrated. Content Marketing lost 176 products against 139 additions, for a net category loss of 37. The 176-removal figure is the largest single-category loss the supergraphic has recorded. The category that had been doubling through 2023, 2024, and 2025 reversed direction in 2026. The structural reading is that AI-native content generation tools absorbed the use cases previously served by point solutions for blog drafting, social copy generation, email subject line testing, and SEO content optimization. The point solutions did not migrate to AI; they were absorbed by AI-native incumbents and challengers.

The State of Martech 2026 report data adds the departure-profile breakdown. Of the vendors that exited, 51.7 percent had launched during the 2010-to-2019 SaaS wave. Forty-five and a half percent sat in the $1 million to $10 million revenue band. Seventy-nine percent had 50 or fewer employees. The departure cohort is concentrated in mid-stage SaaS that lacked the scale to absorb AI-driven margin compression and the AI-native architecture to compete on output quality. The combination is fatal in compressed conditions.

For lead-generation tool categories specifically, the implications track. Form-fill SaaS without TCPA-grade consent capture, generic CRM-bolted-on landing page builders, and basic A/B testing platforms map onto the contracting profile. Categories with disciplined APIs, structured consent metadata, and sub-second service-level agreements – exemplified by ActiveProspect after the InfutorData consolidation, ping-tree routers like Boberdoo, Phonexa, and LeadsPedia, and emerging voice AI qualification tools – map onto the defended profile. The shakeout is not random; it follows the agent-readiness logic Parker's June 10 framework articulated.

---

## Parker's June 10 Agent-Readiness Scoring

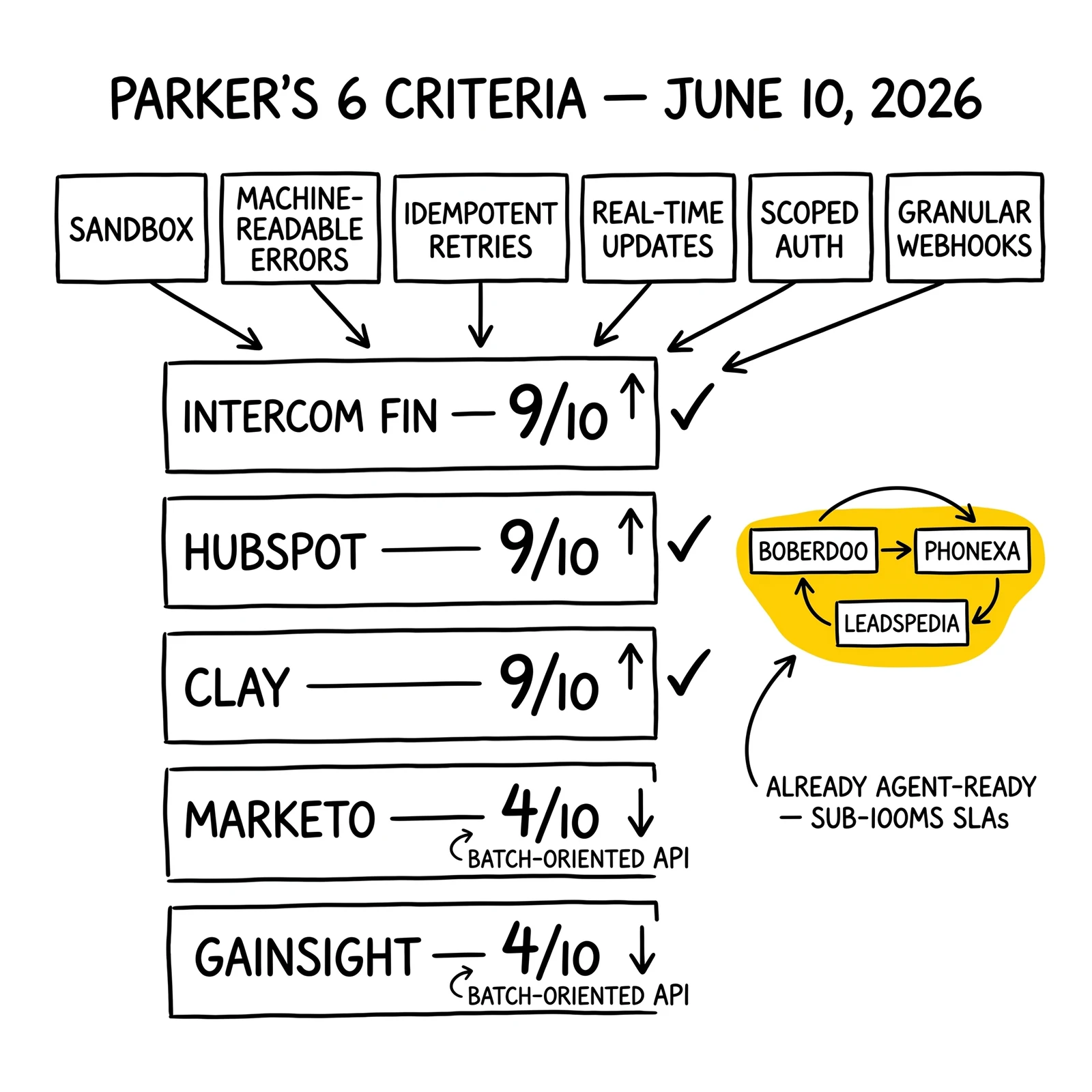

MarTech.org senior writer Pamela Parker published a category-by-category agent-readiness analysis on June 10, 2026. The framework introduced six evaluation criteria: sandbox availability for testing, machine-readable error responses for agent debugging, idempotent retry support for fault tolerance, real-time update mechanisms for agentic decisioning latency, scoped authorization for safe agent deployment, and granular webhook structure for event-driven workflows. Parker scored selected vendors on the 10-point combined scale.

The scoring distribution was uneven. Marketo received 4 out of 10, the lowest among major incumbents Parker reviewed. The framework flagged Marketo's API design as oriented toward batch operations rather than the real-time updates AI agents require. Intercom Fin received 9 out of 10 for its agent-native architecture. HubSpot received 9 for the same reason. Clay received 9 for its data-orchestration capabilities. Gainsight received 4, flagged for the same batch-orientation issues that affected Marketo.

The scoring matters more than the specific vendor placements. The framework treats agent-readiness as a measurable architectural property rather than an aspirational vendor claim. Lead-generation operators selecting infrastructure for 2027 procurement should require agent-readiness disclosure against Parker's six criteria during vendor evaluation, not after. The criteria translate directly into operational performance – a sandbox accelerates integration, machine-readable errors accelerate debugging, idempotent retries reduce duplicate-event risk, real-time updates determine activation latency, scoped authorization governs blast-radius for agent misbehavior, and granular webhooks support event-driven routing decisions.

For lead-distribution platforms specifically, the Parker scoring framework maps cleanly onto the existing ping-post architecture discipline. Boberdoo, Phonexa, and LeadsPedia have run sub-second SLAs, structured payloads, idempotent retry logic, and scoped buyer authorization since the platforms launched. The lead-gen industry's TCPA-compliance discipline produced the exact context plumbing that Brinker described as the new bottleneck. The ping-post architecture was effectively agent-ready before the term existed. The narrowed selection criteria simply formalize what the lead-distribution category already implemented.

The MarTech.org agent-readiness pattern applies most aggressively to lead-gen tool categories where the architectural debt accumulated under SaaS-era assumptions. Lead-form builders that paginated through REST APIs at hourly rate limits, CRM integrations without machine-readable error responses, and A/B testing platforms without real-time-event webhooks each fail the Parker criteria. The categories' decline in the 2026 supergraphic reflects the underlying architecture mismatch.

Parker's framework formalizes what lead distribution already built. Ping-post platforms hit sub-100ms SLAs and structured payloads years before agent-readiness became the procurement criterion.

---

## The Sponsor-Side Reality – What GrowthLoop, MoEngage, Hightouch Are Doing

The State of Martech 2026 report was sponsored by GrowthLoop, Hightouch, Knak, MoEngage, Pega, Progress, and SAS. The sponsor cohort's activity in the six weeks after the May 5 report publication signals that the chrysalis framework is being operationalized rather than received as analysis.

GrowthLoop published the 2026 AI and Marketing Performance Index on May 13, 2026, drawn from a survey of more than 300 marketers conducted with Ascend2. The headline finding pointed at the data infrastructure underneath agentic marketing. Companies operating from a single source of truth reported 44 percent revenue growth against 8 percent for companies without one. Eighty-seven percent of organizations reported implementing AI; only 12 percent reported using mostly real-time signals. The structural insight is that AI adoption is mainstream and the data-infrastructure capability that determines AI's actual contribution is not.

Hightouch closed a $150 million Series D on April 29, 2026 at a $2.75 billion valuation, led by Goldman Sachs and Bain Capital Ventures. The June 15 "Agentic CDP" blog post crystallized Hightouch's positioning the day before Databricks launched CustomerLake and two days before BlueConic acquired Blueshift. The three vendor moves – Hightouch, Databricks, BlueConic-Blueshift – staked three distinct architectural positions for the agentic CDP category within a single week. The [agentic CDP wars analysis](https://www.leadgen-economy.com/blog/agentic-cdp-wars-databricks-customerlake-blueconic-blueshift-2026/) covers the architecture comparison.

MoEngage launched Merlin AI Custom Agents and a Model Context Protocol server on June 3, 2026, then acquired Aampe in an all-cash deal on June 23. The Aampe acquisition added per-customer AI agent technology to the MoEngage platform, signaling a bet on individualized customer-AI rather than the segment-level personalization that previous-generation customer engagement platforms ran. The acquisition pace inside the sponsor cohort – at least three sponsors making meaningful product or M&A moves in seven weeks – reinforces the supergraphic's churn pattern at the major-vendor level.

The sponsor activity makes the Brinker framework operational. Marketers reading the State of Martech 2026 report alongside the GrowthLoop Index, the Hightouch agentic CDP positioning, and the MoEngage acquisition can map specific vendor moves to specific chrysalis dimensions. The supergraphic data set the scale; the sponsor-side activity sets the cadence. The chrysalis is happening on observable vendor-product timelines.

---

## What This Means for Lead-Gen Vertical Tool Selection

The lead-generation vertical's tool selection criteria for 2027 planning should weight the agent-readiness logic Parker articulated more heavily than the category-presence reasoning that vendor RFPs traditionally rewarded. Five specific implications track.

First, lead-form SaaS that does not capture TCPA-grade consent metadata or expose the consent record through machine-readable APIs is exposed to the same shakeout pattern that hit Content Marketing. AI agents now submit forms, including legitimate agent-mediated submissions under delegated mandates that the [Know Your Agent compliance analysis](https://www.leadgen-economy.com/blog/know-your-agent-kya-tcpa-replacement-compliance/) addressed. Form-fill platforms without explicit handling for agent-mediated submissions cede the operator's most defensible top-of-funnel surface.

Second, the lead-distribution category – Boberdoo, Phonexa, LeadsPedia, and the bespoke ping-post stacks at MediaAlpha, EverQuote, LendingTree, QuinStreet – is structurally defended. The architectural disciplines the category built under TCPA pressure during the prior decade are the exact architectural disciplines Parker's six criteria measure. The category should grow share in 2026 and 2027 as adjacent vendors fail the agent-readiness threshold.

Third, generic CRM-attached landing page builders without disciplined APIs face direct exposure. The category had operated under HubSpot's and Salesforce's protection, with the implicit promise that the CRM-platform incumbents would maintain the integration surface. Parker's June 10 scoring puts HubSpot at 9 out of 10 and implicitly raises the question of which CRM-attached builders the major platforms will continue to integrate with as the agent-readiness threshold rises.

Fourth, voice AI qualification tools that displace inside-sales SDR layers represent the canonical new-category growth driver. The category aligns with the rep-free buying preference Gartner measured at 67 percent. The lead-gen operator's economic question is whether to license third-party voice AI or to acquire and integrate the capability. The decision depends on volume thresholds and customization requirements, but the strategic verdict is that the SDR layer is being unbundled by definition.

Fifth, consent vault and identity-resolution infrastructure – the [ActiveProspect-InfutorData consolidation category](https://www.leadgen-economy.com/blog/infutordata-trustedform-jornaya-consolidation-risk/) – is structurally defended on the same logic as ping-post. The TCPA-driven discipline produced agent-ready infrastructure as a side effect. The [Publicis-LiveRamp identity-resolution captivity question](https://www.leadgen-economy.com/blog/publicis-liveramp-2-2-billion-identity-resolution-lead-aggregators/) adds the holding-company captivity layer to the selection criteria, but the underlying agent-readiness of the consent-and-identity layer holds.

---

## What Lead Operators Should Do in the Next 90 Days

The operator action follows directly from the data. Six steps map the implementation arc against the 90-day horizon.

First, audit the current stack against Parker's six criteria. Sandbox, machine-readable errors, idempotent retries, real-time updates, scoped auth, granular webhooks. Score each vendor on the 10-point combined scale. Vendors scoring below 6 should be flagged for replacement evaluation; vendors scoring 4 or lower should be on a replacement timeline.

Second, identify the categories in the current stack that match the contracting profile. Form-fill SaaS without consent discipline, generic CRM-attached page builders, basic A/B testing platforms, content marketing point solutions. The categories' decline in the 2026 supergraphic predicts continued attrition through 2027. Replacement timing depends on contract renewal cycles and internal change-management capacity, but the replacement decision should be staged rather than reactive.

Third, evaluate exposure to the agentic CDP architecture choice. Operators running on traditional SaaS CDPs (Segment, mParticle, Treasure Data) should model whether the migration path runs through warehouse-native (Hightouch), embedded-in-lakehouse (Databricks CustomerLake), or execution-coupled (combined BlueConic-Blueshift). The three architectures produce different cost-and-latency profiles for ping-post lead distribution. The [agentic CDP wars analysis](https://www.leadgen-economy.com/blog/agentic-cdp-wars-databricks-customerlake-blueconic-blueshift-2026/) walks the trade-offs.

Fourth, instrument context-engineer accountability. The chrysalis framework's context-engineer role assumes someone curates the context that AI agents read. Lead-generation operations should define the role explicitly – who owns the JSON-LD schema, the MCP server definitions, the consent metadata structure, the agent-readable documentation. Operations without defined context-engineer accountability will see vendor selection underperform.

Fifth, watch the Q3 and Q4 2026 vendor cohort for further acquisitions. The June 16 Databricks launch, the June 17 BlueConic-Blueshift acquisition, and the June 23 MoEngage-Aampe acquisition cluster suggests acceleration rather than completion. Adobe, Salesforce, Microsoft, Snowflake, Twilio Segment, Oracle Marketing Cloud, and the broader sponsor cohort have positioning decisions to make. Vendor consolidation through the second half of 2026 will determine which architecture choices become standard and which become legacy.

Sixth, build optionality into multi-year contracts. The vendor risk in 2026 and 2027 is no longer the vendor going out of business – it is the vendor making an architectural choice that becomes the wrong side of the agent-readiness divide. Multi-year contracts signed in 2025 against agent-readiness criteria that did not exist will be the contracts operators want exit clauses on by 2027. New procurement should include explicit agent-readiness disclosure requirements and pricing-protection clauses against major architectural pivots.

---

## Key Takeaways

- The 2026 chiefmartec Marketing Technology Landscape Supergraphic published in May 2026 documented 15,505 products, up 0.79 percent from 15,384. The first true plateau in the category's 15-year measurement history.

- The plateau headline conceals churn: 1,488 additions against 1,367 removals. Additions down 40 percent from 2025; removals up 13 percent.

- Content Marketing lost a net 37 products in 176 removals – the largest category-level loss in the supergraphic's history. The category that doubled through 2023-2025 reversed direction in 2026.

- Growth categories concentrate on infrastructure: CMS 21.4 percent, Ecommerce 19.9 percent, Mobile/Web Analytics 11.3 percent, iPaaS 8 percent, Governance 7.1 percent, Marketing Automation 5.9 percent.

- MarTech.org's Pamela Parker published category-by-category agent-readiness scoring on June 10, 2026. Marketo and Gainsight scored 4 out of 10; HubSpot, Clay, and Intercom Fin scored 9 out of 10.

- Departure profile per State of Martech 2026 report: 51.7 percent of exiting vendors launched in the 2010-2019 SaaS wave; 45.5 percent in $1M-$10M revenue band; 79 percent with 50 or fewer employees.

- Sponsor activity reinforces the chrysalis operationalization: Hightouch $150M Series D (April 29), GrowthLoop AI Performance Index (May 13), Hightouch Agentic CDP positioning (June 15), MoEngage Merlin AI + MCP server (June 3) and Aampe acquisition (June 23).

- For lead-gen vertical tool selection, ping-post platforms and consent-vault infrastructure are structurally defended; generic CRM-attached page builders and form-fill SaaS without TCPA-grade consent capture are exposed.

- 90-day operator actions: audit Parker's six criteria, replace failing categories, evaluate agentic CDP architecture choice, instrument context-engineer accountability, watch Q3/Q4 acquisitions, build optionality into multi-year contracts.

---

## Sources

- [chiefmartec – 2026 Marketing Technology Landscape Supergraphic (May 2026)](https://chiefmartec.com/2026/05/2026-marketing-technology-landscape-supergraphic-peak-martech-achieved-maybe/)

- [MarTech.org – The Martech Categories Hit Hardest by AI Agents (Pamela Parker, June 10, 2026)](https://martech.org/the-martech-categories-hit-hardest-by-ai-agents/)

- [CMSWire – The Martech Landscape Has Plateaued (Dom Nicastro, May 5, 2026)](https://www.cmswire.com/digital-marketing/the-martech-landscape-has-plateaued-the-real-crisis-is-what-ai-is-exposing-underneath-it/)

- [Hightouch – Series D Funding Announcement (April 29, 2026)](https://www.businesswire.com/news/home/20260427054567/en/Hightouch-Raises-$150-Million-to-Reinvent-How-Marketing-Works-Using-AI)

- [Hightouch – The Agentic CDP (June 15, 2026)](https://hightouch.com/blog/the-agentic-cdp)

- [GrowthLoop – 2026 AI and Marketing Performance Index (May 13, 2026)](https://www.growthloop.com/press/growthloop-unveils-2026-ai-and-marketing-performance-index)

- [Novistra Capital – MarTech M&A Market Landscape (April 15, 2026)](https://novistra.com/wp-content/uploads/2026/04/Novistra-Capital_MarTech-Report_20260415.pdf)

- [MartechView – Martech 2026 AI Rewires a Stalling Landscape](https://martechview.com/martech-2026-ai-rewires-a-stalling-landscape/)