# MediaAlpha's Q1 2026 Print – $310M Revenue, P&C +31%, and the Autoinsurance.net ChatGPT App That Resets the Marketplace Thesis

> **Canonical:** https://www.leadgen-economy.com/blog/mediaalpha-q1-2026-autoinsurance-chatgpt-integration/

> **Published:** 2026-06-25

> **Author:** Alex Paddington

> **Source:** LeadGen Economy – https://www.leadgen-economy.com

---

*One quarter resolves the marketplace thesis MediaAlpha has been arguing for two years – and one product launch resolves the question of what comes after the click.*

---

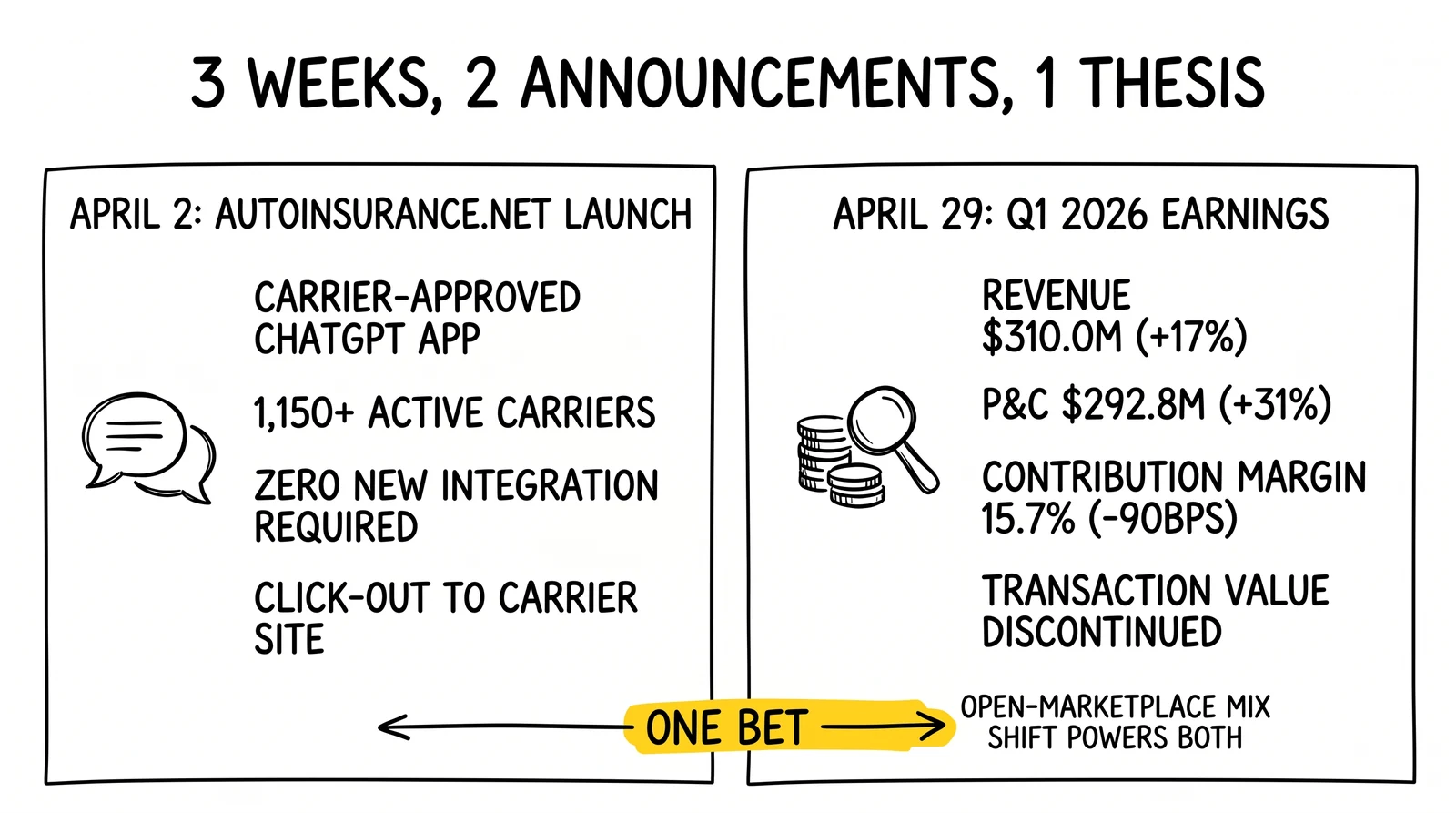

## A $310 million print and a ChatGPT app, three weeks apart

MediaAlpha (NYSE: MAX) reported first-quarter 2026 revenue of $310.0 million on April 29, up 17 percent year over year and $13.4 million above the $296.6 million sell-side consensus. Adjusted EBITDA of $31.4 million topped the prior-year quarter's $29.4 million. Net income swung to a $14.0 million profit from a $2.3 million loss in Q1 2025. Property and casualty insurance – the vertical that has carried the company since the 2024 hard-market reset began to ease – generated $292.8 million, 94.4 percent of total revenue, growing 31 percent year over year against a $223 million Q1 2025 comparable.

Three weeks earlier, on April 2, MediaAlpha launched Autoinsurance.net inside ChatGPT. The company called it the insurance industry's first carrier-approved conversational AI application. The consumer types "autoinsurance.net app" into ChatGPT's search interface, answers a structured conversation covering zip code, vehicle, homeownership, age, and credit profile, and receives a live shortlist of carrier-approved listings sourced from the same open marketplace MediaAlpha's 1,150-plus active carrier partners already participate in. The click-out lands on the carrier's own website. The carrier completes the quote. The certificate of consent is captured at the carrier form, not inside ChatGPT.

The two events describe one bet. MediaAlpha's earnings tell the market that the open-marketplace mix shift – non-leading top-15 and top-20 carriers allocating real budget into a programmatic auction – is the structural story for 2026. The Autoinsurance.net launch tells the market that the same marketplace is now extensible to whatever discovery surface consumers walk through next. Get one right and the other follows.

MediaAlpha's three-week window pairs an open-marketplace earnings beat with a ChatGPT shopping app – the same carrier-approved listing inventory rendered through two surfaces.

---

## The Q1 print – what the numbers actually say

MediaAlpha's Q1 2026 release stacks a clean set of beats against a stock-price reaction that registered the print as good rather than great. The decomposition matters because the same numbers carry different implications depending on which line of the income statement an operator cares about.

| Metric | Q1 2026 | Q1 2025 | Change |

|---|---|---|---|

| Total revenue | $310.0M | $264.7M | +17.1% |

| P&C insurance | $292.8M | $223.4M | +31.1% |

| Health insurance | $11.2M | $34.0M | -67.1% |

| Life insurance | $5.8M | n/d | n/d |

| Contribution | $48.7M | $43.9M | +10.8% |

| Contribution margin | 15.7% | 16.6% | -90 bps |

| Adjusted EBITDA | $31.4M | $29.4M | +6.8% |

| Net income (loss) | $14.0M | $(2.3)M | swing |

| Diluted EPS | $0.21 | n/d | beat by $(0.01) vs $0.22 cons |

The P&C revenue line is the headline. A 31 percent year-over-year P&C growth print in a vertical that grew at single digits for most of 2023 says the auto-insurance acquisition cycle is in a mid-up part of its curve. Carriers that had been raising rates and shrinking marketing budgets through the 2022-2024 hard market are now competing again for net-add policies. MediaAlpha is a direct beneficiary of every dollar of that re-acceleration that lands in an open-bid auction rather than in a captive-agent or direct-response funnel.

The health-insurance line is the obvious offset and the explanation for the contribution-margin compression from 16.6 to 15.7 percent. MediaAlpha is winding down its under-65 ACA-adjacent health business under an FTC settlement that produced an $11.5 million cash payment in Q1. Revenue in the segment fell 67 percent year over year. Health used to carry contribution margin above the company average; pulling it out of the mix shifts the consolidated margin down by structural composition, even though the remaining business is healthier. Management characterized the 15 to 16 percent range as sustainable given the new business composition.

The EBITDA line is what the market saw. $31.4 million is a 7 percent year-over-year increase against a 17 percent revenue increase – operating leverage at the EBITDA line is positive but not dramatic. The stock dipped roughly 5.6 percent in after-hours trading the same day on a combination of an EPS print one cent shy of consensus, Q2 guidance that landed close to the Street rather than above it, and a contribution-margin number that read as compression even though management explained it as mix.

### Q2 2026 guidance – high-teens growth at thinner unit margin

| Metric | Q2 2026 guide | YoY growth (midpoint) |

|---|---|---|

| Revenue | $290M – $310M | +19% |

| Contribution | $45.5M – $48.5M | +18% |

| Adjusted EBITDA | $28.0M – $30.5M | +19% |

Excluding the under-65 health business, MediaAlpha guided core P&C contribution to grow 21 to 28 percent and core P&C EBITDA to grow 26 to 36 percent. The ex-health view is the cleaner read for operators and the one the company has been signaling will become the durable disclosure once the FTC-driven health wind-down completes.

### Capital allocation – refinanced wall, continued buyback

The Q1 print also recorded two balance-sheet decisions that matter for the marketplace thesis. MediaAlpha completed a credit-facility refinancing into a $150 million senior secured term loan plus a $60 million revolving credit facility, both maturing March 2031, pushing the previous 2028 maturity wall out by approximately three years. And the company repurchased approximately 2.6 million shares for $25 million year to date through the Q1 print, bringing the cumulative program total to roughly 3.7 million shares – about 10 percent of outstanding. The refinancing locks capital structure for the duration of the marketplace re-acceleration; the buyback signals management's read that the equity is undervalued at the current mix.

### Transaction Value is gone

The most consequential disclosure change is the discontinuation of Transaction Value reporting and guidance, effective Q1 2026. Transaction Value – the gross dollar volume of clicks, calls, and leads transacted across the marketplace – had been the canonical non-GAAP top-line proxy for marketplace liquidity since the 2020 IPO. MediaAlpha framed the change as a reporting simplification. Analysts now triangulate the marketplace through revenue, contribution, and adjusted EBITDA. The implication for operators benchmarking against MediaAlpha disclosures is that the public-market read on gross volume is no longer available; the next-cleanest proxy is the open-marketplace revenue line itself.

---

## The non-top-5 carrier surge – the actionable signal

The single most operator-relevant disclosure on the Q1 call was the carrier-mix commentary. CEO Steve Yi attributed the 31 percent P&C growth not to incremental spend from the leading four or five carriers – Progressive, GEICO, State Farm, Allstate, Liberty Mutual at the top of personal-lines direct-premium rankings – but to broader participation from non-leading top-15 and top-20 carriers stepping into the open marketplace. Management characterized growth as "accelerating from non-leading carriers rather than a pullback from leading ones." Leading carriers maintain spend; the new growth is coming from mid-tier carriers leaning into growth marketing.

The structural framing on the call was that non-top-5 carriers were historically under-allocated to MediaAlpha relative to their digital-marketing share, with single-digit percentages of digital budgets routed into the marketplace against a benchmark closer to 10 to 20 percent for the leading carriers. That gap is closing in 2026, and the path of the closure determines marginal-bid economics for every other auction participant.

### Why the non-top-5 surge sets the marginal bid

In an open-bid auction, the marginal bidder sets the clearing price. As long as the leading carriers are the only buyers at full bid, marginal economics are determined by the leading-carrier customer-lifetime-value model – Progressive's combined ratio, GEICO's churn, Allstate's marketing budget – and aggregators selling into the top of the panel see margin determined by carrier headroom on those models.

When non-top-5 carriers re-enter the bid stack at materially higher allocations, two things happen. First, the marginal clearing price floor rises because there are more bidders competing for the same lead pool at the second-price layer. Second, the buyer-mix dilution of any single carrier's bidding posture decreases – no individual carrier's pullback can move the clearing price by as much. Both effects are friendly to aggregator margin.

The operator-side translation is that mid-tier carrier panels still carry budget headroom through at least Q3 2026, that the marginal-bid floor is being raised by mid-tier participation rather than top-tier escalation, and that aggregators selling into the mid-tier of the carrier panel should reprice upward to capture the cycle. Aggregators concentrated on the leading-carrier panel face a more contested bid environment; aggregators that have spent the last two years building out non-top-5 carrier relationships now collect the dividend.

### What the call did not disclose

Management did not break out the open-marketplace revenue contribution from non-top-5 carriers in dollar terms or as a share of P&C revenue. The 98 percent open-marketplace share of Q1 2026 revenue – the highest in company history – implies the open channel is doing the work, but the carrier-tier composition inside the open channel is not disclosed at the segment level. The Investor Presentation flagged the non-top-5 surge qualitatively, the 10-Q quantified it only at the aggregate P&C line, and the operator math on what fraction of the $292.8 million is mid-tier carriers versus the top five remains a triangulation rather than a disclosure.

---

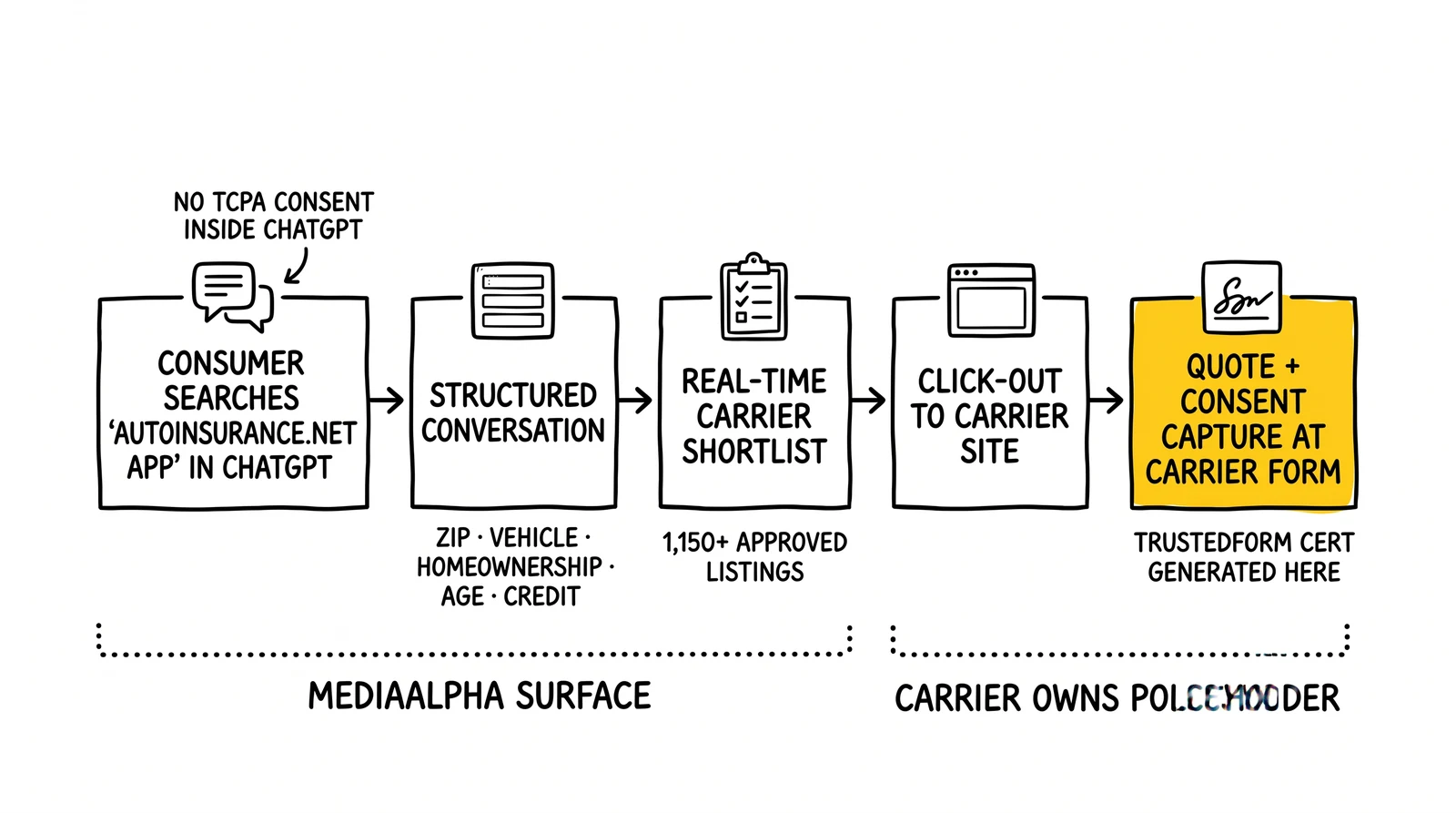

## Autoinsurance.net – the architecture of a carrier-approved ChatGPT app

The April 2, 2026 launch was framed inside the Q1 call as a strategic surface rather than a near-term revenue driver. The product mechanics deserve close reading because they describe a model of conversational shopping that is materially different from the horizontal ChatGPT advertising path running through Criteo's reseller integration that activated more than 2,000 brands as of June 22.

### The consumer flow

1. The consumer is inside ChatGPT for any reason – research, summary, drafting.

2. The consumer searches for the "autoinsurance.net app" inside ChatGPT, which surfaces and enables the application.

3. The app runs a structured conversation collecting zip code, vehicle make/model/year, homeownership status, age, and credit profile.

4. The app returns a shortlist of carrier-approved listings – carrier name, logo, headline benefit, indicative price – pulled in real time from MediaAlpha's marketplace.

5. The consumer clicks a listing and is routed directly to the carrier's own website to complete the quote and bind the policy.

The architectural commitment in step five is the part that determines downstream economics. The consumer does not complete the lead conversion inside ChatGPT, does not provide a phone number or email inside ChatGPT, and does not generate a TrustedForm or Jornaya certificate inside ChatGPT. The certificate, the phone number, the consent disclosure language, and the carrier's standard form interaction all happen at the carrier site. The Autoinsurance.net surface is a discovery and disambiguation layer; the lead acquisition itself is unchanged.

The consent certificate is generated at the carrier form, not inside ChatGPT – the design choice that lets 1,150 existing MediaAlpha carriers ship a conversational app with zero new compliance review.

### Carrier integration cost – zero

The launch press release emphasized that no new integration is required from carrier partners. The Autoinsurance.net app draws on the same listing inventory, the same approval workflows, and the same carrier-logo and headline-format constraints that MediaAlpha's open marketplace already runs against carrier compliance review. A carrier that already participates in the open marketplace does not need to negotiate a new integration to appear in Autoinsurance.net listings; their existing creative and compliance posture carries forward.

This is the most operationally consequential design choice. Conversational shopping inside an LLM context historically would require carriers to negotiate a new compliance review for every model surface – Was this listing accurately rendered? Did the conversation correctly disclose the carrier's required language? Did the AI-generated headline comply with state insurance regulation? MediaAlpha's design sidesteps this by treating the LLM surface as a thin renderer over a compliance-approved listing inventory, not as a generative endpoint that creates new copy for each interaction.

### What's not disclosed

Several economic mechanics were not disclosed at launch or in the Q1 print. MediaAlpha did not characterize the click-out economics – whether the click from ChatGPT into the carrier site is priced as a per-click MediaAlpha sale, whether the carrier pays a commission against the bound policy, or whether the channel runs on a hybrid model with a base click rate plus a quality-adjusted multiplier. The company did not disclose Autoinsurance.net's contribution to Q1 revenue, which is reasonable given the April 2 launch fell two-thirds of the way through the quarter. Management did not name the OpenAI partnership specifics – whether the app runs as a custom GPT, plugin, or framework-level integration with the ChatGPT app discovery surface.

The opacity on click economics is the most analytically frustrating gap. If Autoinsurance.net clicks are priced at MediaAlpha's standard carrier-direct click rate, the surface is incremental but margin-neutral. If they are priced at a premium because the conversational pre-qualification thinned the funnel before the click, the surface is a margin upgrade. If they are priced at a discount because OpenAI takes a revenue share, the surface is a margin drag. None of these are knowable from current disclosure.

---

## How this differs from the Criteo ChatGPT Ads path

Operators reading the LeadGen Economy [analysis of Criteo's June 22, 2026 disclosure that 2,000-plus brands were activated on its ChatGPT Ads reseller integration](https://www.leadgen-economy.com/blog/chatgpt-ads-cannes-2026-criteo-2000-brands-lead-gen/) should read the MediaAlpha-OpenAI partnership as a structurally different category. The two paths are not substitutes; they are complementary surfaces with different operator implications.

| Dimension | Criteo ChatGPT Ads | MediaAlpha Autoinsurance.net |

|---|---|---|

| Surface scope | Horizontal – 2,000+ brands across retail, fintech, local services | Vertical – auto insurance only |

| Consumer invocation | Ad served inside ChatGPT conversational flow | App invoked by consumer search |

| Buyer participation | Any brand running through Criteo's reseller integration | 1,150+ MediaAlpha carrier partners only |

| Compliance | Brand-side advertising compliance | Carrier-approved listings, MediaAlpha-mediated |

| Click destination | Advertiser landing page | Carrier's own website |

| Lead capture mechanic | Form on advertiser landing page | Form on carrier site, post-click |

| Consent certificate | Generated at advertiser form | Generated at carrier form |

| Insurance vertical posture | Gated by Fair Housing, MAP Rule, state insurance compliance through 2026-2027 | Live April 2, 2026 with carrier-approved listings |

The Criteo path optimizes for click reach across many advertisers and was explicitly described as gated for insurance and mortgage verticals through 2026 because of state-insurance-department disclosure complications. The MediaAlpha path runs a single auto-insurance flow with the compliance work already pre-done by the carriers in the marketplace. The two paths can coexist – and likely will – because they answer different operator questions.

For an aggregator deciding budget allocation, the Criteo path is a CPL-style ad-buy decision running through paid-media tooling and conversion attribution; the MediaAlpha path is a marketplace-participation decision running through carrier-direct relationships. For a carrier deciding consumer-channel posture, the Criteo path is a horizontal ad surface buy; the MediaAlpha path is an extension of the existing marketplace listing posture into a new discovery context. The activation cost of the MediaAlpha path is effectively zero for carriers already participating in the open marketplace, which is why launch participation breadth was not an issue. The Criteo path requires per-brand activation, which is why 2,000 brands in seven weeks is the meaningful metric.

---

## Why the marketplace transparency thesis matters for ChatGPT-as-lead-source

MediaAlpha's positioning across Q1 – both the earnings call and the Autoinsurance.net launch – centers on a transparency claim. CEO Steve Yi's launch quote framed the application as one where "every result is a real carrier partner, every click goes directly to the carrier's own site, and consumers get accurate information at every step." This is not throwaway language. It is the legal-and-product position MediaAlpha has built since its 2020 IPO, and it explains why an LLM surface is a natural extension rather than an awkward graft.

The transparency thesis has three operational pieces:

1. **Carrier-approved inventory.** Listings come from carriers who have pre-approved the headline, logo, and price-disclosure language. No generative substitution.

2. **Click-out destination integrity.** The consumer reaches the carrier site, not a MediaAlpha-owned form. The carrier owns the policyholder relationship from first click.

3. **Marketplace mechanic disclosure.** MediaAlpha discloses to carriers the auction logic, the placement determinants, and the data exchange – what is sometimes called the open-marketplace contract.

A consumer interacting with Autoinsurance.net inside ChatGPT is therefore not interacting with an "AI" in any model-generative sense; they are interacting with the same marketplace inventory rendered through a conversational interface. The integrity of the lead – and the legal posture of the carrier accepting it – is functionally identical to a click that originated from a Google Search comparison page or a publisher partner like NerdWallet.

This is the structural advantage that aggregators competing with MediaAlpha-style intent layers should pay attention to. The companies that already run carrier-approved listing inventories, that already have compliance-cleared creative formats, and that already operate transparent auction mechanics can extend into ChatGPT, Perplexity, Comet, Claude, and other agentic surfaces at near-zero marginal compliance cost. The companies that have been running optimize-for-CTR landing-page funnels with dynamically generated headlines will not have that extensibility. They will face per-surface compliance review, generative-content risk under state insurance regulation, and consent-capture architectural problems at every new surface.

The Autoinsurance.net launch is, in effect, MediaAlpha's argument that marketplace integrity is the prerequisite for LLM-distribution. Operators who agree with the thesis face an inventory-architecture decision; those who disagree are betting on a per-surface CPL ad-buy posture instead.

---

## Click economics, contribution margin, and what to monitor next

The remaining analytical question for operators is whether the Autoinsurance.net surface contributes positively, neutrally, or negatively to MediaAlpha's contribution margin once it scales. The 15.7 percent Q1 contribution margin gives the base. Three forward signals are worth monitoring.

**Click rate disclosure.** Will MediaAlpha break out Autoinsurance.net click volume, revenue contribution, or take rate at any future earnings disclosure? Management explicitly avoided discussion of new-product revenue at Q1, citing the post-launch ramp. The Q2 print scheduled for late July 2026 is the first opportunity for a meaningful disclosure. Watch for any segment-level or product-level commentary about conversational-channel click rates.

**Carrier mix inside Autoinsurance.net.** Does the conversational app over- or under-index on non-top-5 carriers relative to the broader open marketplace? If the non-top-5 surge that drove Q1 also concentrates inside Autoinsurance.net, the surface becomes a pricing wedge: it lets non-top-5 carriers reach LLM-mediated consumers without paying full top-5 bid rates. If the leading carriers dominate the surface, the channel is incremental but unsurprising.

**Conversion lift versus standard click.** The natural test is whether ChatGPT-originated clicks convert at carrier sites at a higher, equal, or lower rate than clicks from the same MediaAlpha marketplace served via traditional publisher partners. The conversational pre-qualification – zip, vehicle, homeownership, credit profile collected before the click – should produce a higher conversion rate per click. If it does, MediaAlpha can charge a premium against the standard click. If conversion lift is muted, the surface is a marginal channel addition.

These three signals will be visible inside two to three quarters. By the Q3 2026 print in late October 2026, operators should be able to read whether Autoinsurance.net is a margin-accretive new channel, a margin-neutral channel extension, or a strategic positioning play that runs at consolidated company economics.

---

## The dark-funnel attribution problem doesn't go away

Operators reading MediaAlpha's transparency thesis alongside the [dark-funnel self-reported attribution analysis](https://www.leadgen-economy.com/blog/dark-funnel-self-reported-attribution-incrementality-2026/) should hold both ideas at once. Autoinsurance.net solves the inventory-and-compliance side of LLM-distribution. It does not solve the attribution-side of LLM-mediated purchase journeys.

A consumer who interacts with Autoinsurance.net, clicks to a carrier site, abandons the quote, returns to ChatGPT three days later for further research, asks Claude about a different carrier, and then completes a bind on the carrier's app two weeks later is a real consumer journey. The Autoinsurance.net click is attributed to ChatGPT. The downstream behavior is not. The carrier's CRM may show "ChatGPT" or "Autoinsurance.net" as the lead source if the click-tracking is well wired; it will not show the full LLM-mediated research path that informed the eventual bind.

For operators running their own attribution stacks, the implication is that LLM-mediated channels – Criteo's ChatGPT Ads, MediaAlpha's Autoinsurance.net, Perplexity Comet, Anthropic surfaces – will require the same self-reported-attribution and incrementality-testing posture that 2024-2025 paid social already does. The carrier-direct click looks attributable. The journey that produced the click does not.

---

## What aggregators competing with MediaAlpha should do

Three positioning decisions follow from the Q1 print and the Autoinsurance.net launch for the rest of the publicly traded and private competitor set in the [insurance-lead-marketplace and lead-distribution-platform landscape](https://www.leadgen-economy.com/blog/lead-distribution-platforms-comparison-boberdoo-leadexec-leadspedia/).

**Mid-tier carrier panel build-out.** The 31 percent P&C growth and the non-top-5 carrier surge tell every competitor where the marginal bid is forming. Aggregators concentrated on the leading carriers face thinning carrier-bid headroom; aggregators that have invested in mid-tier carrier relationships through 2024 and 2025 are seeing those bets pay out now. Building or deepening mid-tier carrier panels should be a 2026 priority, not a 2027 priority.

**Conversational surface extensibility audit.** The Autoinsurance.net architecture works because MediaAlpha runs a carrier-approved listing inventory with clean creative compliance. Aggregators running dynamically generated landing-page creative or per-buyer headline optimization will have a harder time extending into LLM surfaces. The architectural audit question is whether the existing listing inventory is pre-cleared for LLM-rendering – and if not, what the cleanup path looks like.

**Click-out economics decision.** MediaAlpha's design routes the click to the carrier's own site, preserving the carrier's standard form and consent-capture flow. Aggregators that run their own forms and resell the lead downstream face a structural decision: route the click to the carrier (preserving the marketplace-integrity narrative but losing the lead-monetization layer) or run a competing form-on-aggregator-property flow (preserving lead monetization but introducing per-LLM-surface compliance review). The carrier-direct routing is the cleaner posture for LLM distribution; the form-on-property posture is the cleaner posture for ping-post downstream resale. Operators with hybrid models will need to pick per channel.

---

## Key Takeaways

- MediaAlpha Q1 2026 revenue of $310.0 million beat $296.6 million consensus by $13.4 million; the print is the strongest single-quarter top-line in company history.

- Property and casualty revenue of $292.8 million (+31 percent YoY) drove the print, with the under-65 health wind-down (-67 percent) explaining the contribution-margin compression from 16.6 to 15.7 percent.

- Adjusted EBITDA reached $31.4 million (+7 percent); net income swung to a $14.0 million profit from a $2.3 million loss; diluted EPS of $0.21 missed consensus by $0.01.

- MediaAlpha discontinued Transaction Value reporting effective Q1 2026, removing the canonical non-GAAP top-line proxy for marketplace liquidity.

- Non-leading top-15 and top-20 carriers drove the P&C growth – management said the leading carriers maintained spend while mid-tier carriers leaned in. The non-top-5 carrier surge is the actionable operator signal.

- Capital structure: refinanced into $150M term loan plus $60M revolver, both maturing March 2031; cumulative buyback program reached approximately 10 percent of outstanding shares.

- Autoinsurance.net launched April 2, 2026 inside ChatGPT as the industry's first carrier-approved conversational AI auto-insurance shopping app, with consumer click-out routed to the carrier's own website.

- The Autoinsurance.net architecture requires zero new integration from carrier partners – the LLM surface renders the existing open-marketplace inventory through a conversational interface.

- The MediaAlpha-OpenAI path is structurally different from the Criteo-OpenAI ChatGPT Ads path: vertical-specific shopping app versus horizontal advertising surface; carrier-approved listings versus open ad inventory; carrier-site lead capture versus advertiser-landing-page capture.

- Click economics, take rate, and conversion lift for Autoinsurance.net were not disclosed – Q2 and Q3 2026 prints will be the first read on whether the surface is margin-accretive, neutral, or strategic-positioning only.

- Aggregators competing with MediaAlpha should audit conversational-surface extensibility against their listing inventory architecture; companies running dynamically generated creative face structurally harder LLM-distribution paths.

---

## Sources

- [MediaAlpha Q1 2026 Earnings Release Form 8-K (SEC, April 29, 2026)](https://www.sec.gov/Archives/edgar/data/0001818383/000181838326000117/maxq12026-earningsreleasex.htm)

- [MediaAlpha Q1 2026 Form 10-Q (SEC, April 29, 2026)](https://www.sec.gov/Archives/edgar/data/0001818383/000181838326000118/max-20260331.htm)

- [MediaAlpha Launches the Insurance Industry's First Carrier-Approved Conversational AI Application (GlobeNewswire, April 2, 2026)](https://www.globenewswire.com/news-release/2026/04/02/3267401/0/en/mediaalpha-launches-the-insurance-industry-s-first-carrier-approved-conversational-ai-application-for-carriers-and-consumers.html)

- [MediaAlpha (MAX) Q1 2026 Earnings Transcript (The Motley Fool, April 29, 2026)](https://www.fool.com/earnings/call-transcripts/2026/04/29/mediaalpha-max-q1-2026-earnings-transcript/)

- [MediaAlpha Q1 2026 Slides – P&C Surge Drives 17% Revenue Growth (Investing.com, April 29, 2026)](https://www.investing.com/news/company-news/mediaalpha-q1-2026-slides-pc-surge-drives-17-revenue-growth-93CH-4647397)

- [MediaAlpha Q1 2026 Revenue Rises 17% to $310M (StockTitan, April 29, 2026)](https://www.stocktitan.net/news/MAX/media-alpha-announces-first-quarter-2026-financial-thqnv9y0udr5.html)

- [MediaAlpha (MAX) Q1 2026 Earnings Call Transcript (Seeking Alpha, April 29, 2026)](https://seekingalpha.com/article/4896215-mediaalpha-inc-max-q1-2026-earnings-call-transcript)

- [MediaAlpha Q1 Earnings Call Highlights (Yahoo Finance, April 29, 2026)](https://finance.yahoo.com/markets/stocks/articles/mediaalpha-q1-earnings-call-highlights-114918758.html)