FHFA’s April 22, 2026 decision to clear VantageScore 4.0 for Fannie Mae, Freddie Mac, and FHA underwriting – paired with VantageScore-component bureau prices that landed between free and $4.50 within seventy-two hours – quietly shifted the cost assumptions sitting under mortgage prequalification funnels. The shift is real, and it is narrower than a full lead-price reset. It changes which score model lenders can accept (a score-model eligibility shift), it changes the marginal cost of running a soft-pull prequalification on the VantageScore-component layer (a prequal cost-assumption shift), and it leaves the all-in tri-merge bundle and per-lead pricing to adjust on a slower, buyer-driven cycle.

Three Distinct Layers, Not One Re-Pricing Event

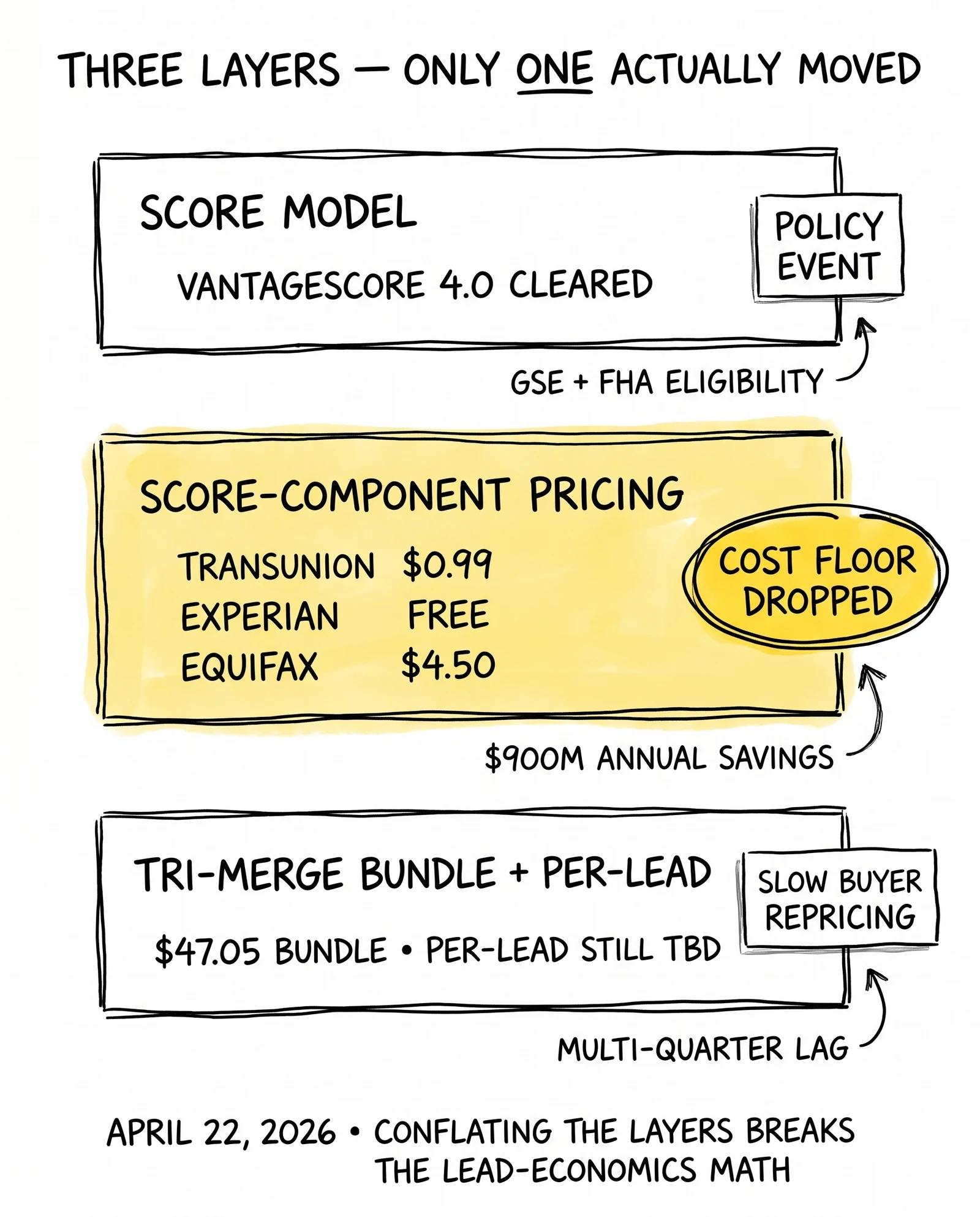

On April 22, 2026, Federal Housing Finance Agency Director William J. Pulte and Department of Housing and Urban Development Secretary Scott Turner stood together to announce something that mortgage operators had been waiting more than seven years to hear. Fannie Mae and Freddie Mac would, effective immediately, begin accepting VantageScore 4.0 for mortgage underwriting. The Federal Housing Administration would follow with both VantageScore 4.0 and FICO Score 10T “in coming months.” Twenty-one of the country’s largest lenders had already applied to deliver loans scored under the new model. Within seventy-two hours, the three credit bureaus published VantageScore 4.0 component pricing: TransUnion at $0.99 per score, Experian free indefinitely, Equifax at $4.50 with a free bundle through 2026.

The right way to read this for lead-gen unit economics is to separate three layers that the trade-press headline tends to conflate. Layer one – score model. FHFA accepted VantageScore 4.0 (and signaled FICO 10T acceptance to follow at FHA). This is a score-model eligibility decision; lenders can now choose. Layer two – credit-report/tri-merge product. The tri-merge product bundles each bureau’s full credit report with a score from each. The April 22 pricing applies to the VantageScore 4.0 score component only, not to the tri-merge bundle that wraps around it. The tri-merge price climbed from $33.50 in 2025 to $47.05 in 2026 by industry-tracked figures, and the score-component pricing changes do not directly reduce that bundle. Layer three – lead-price economics. Per-lead pricing depends on what lenders pay lead generators, which depends on buyer-side underwriting cost, conversion rate, and competition for inventory. None of the layer-one or layer-two changes automatically reprice every mortgage prequalification lead overnight; per-lead repricing is a buyer-driven process that follows cost-assumption changes on a multi-quarter lag.

For mortgage lead generators, the practical implication is bounded. The marginal cost of running a soft-pull prequalification on the VantageScore 4.0 component drops materially. The all-in tri-merge bundle does not drop in lockstep. Per-lead pricing adjusts as lenders work through their own underwriting-cost models, LLPA grids, and bid logic. This analysis covers what changed on April 22 at each of the three layers, why the score-component price war matters less than headlines suggest for the all-in lead-economic question, how the prequalification funnel adjusts in this environment, and what mortgage lead operators should be doing in the next ninety days to position for the slower per-lead repricing that follows.

What Changed on April 22, 2026 – and Why the Score-Component Price War Is Narrower Than the Headlines Imply

The headline event was the scoring-model eligibility decision. The downstream effect at the score-component layer is real but narrower than “every mortgage lead just got cheaper.”

Pulte and Turner’s joint announcement was the formal end of a process that began with the FHFA’s 2022 validation of VantageScore 4.0 and FICO Score 10T as eligible models for GSE use. What the April 22 decision added was operational immediacy. Fannie Mae’s and Freddie Mac’s selling guides were updated the same day. Loans scored on VantageScore 4.0 were eligible for delivery from approved lenders effective immediately. By the end of April, Freddie Mac had already securitized the first wave of VantageScore 4.0-scored mortgages from Newrez – approximately $10 million in initial volume. The Mortgage Bankers Association, which had been lobbying for this outcome since at least 2018, issued a “Breaking Advocacy Update” the following morning.

The lender pilot list – Pennymac, Rocket Mortgage, Newrez, and eighteen other large originators – signals a market structure decision rather than a technology swap. These twenty-one institutions account for a substantial share of GSE-eligible originations. Their willingness to deliver Vantage-scored loans creates the secondary-market liquidity that makes the new score commercially viable. Without that liquidity signal, the score would remain technically accepted but operationally orphaned, the way many “approved alternative” frameworks ended up over the past decade.

The score-component price war that ran in parallel

Within seventy-two hours of the FHFA announcement, all three bureaus published VantageScore 4.0 score-component pricing. TransUnion at $0.99 per score. Experian free indefinitely. Equifax at $4.50 per score with a free bundle through the end of 2026. The pricing applies to the VantageScore 4.0 score component, not to the tri-merge bundle that wraps full credit-report data from each bureau around the score. Industry analysis projects more than $900 million in annual lender and consumer savings from the score-component repricing alone. For comparison, FICO has been operating under a 2025 wholesale price of $4.95 per score, with its newer “performance pricing” model adding a $33 fee per borrower on funded loans.

The numbers matter less than the slope they describe at the score-component layer. Until April 22, that layer of mortgage origination was a single-vendor monopoly with annual price increases that had compounded into a fourth consecutive year of double-digit cost growth. The tri-merge credit-report bundle – which packages each bureau’s full credit report with a score – rose from $33.50 in 2025 to $47.05 in 2026, a 40.4 percent year-over-year increase, according to MBA documentation, and the April 22 score-component repricing does not directly cut that bundle price. Some credit vendors were charging brokers and consumers $200, $212, or $220 per tri-merge. After April 22, the score component of the bundle is competitively priced for the first time in over a decade; the bundle as a whole adjusts on a slower cycle as the bureaus protect bundled-product margins.

This is the news that matters for mortgage lead generation economics at the score-component layer. The score-model eligibility decision is the policy event. The score-component price war is a prequal cost-assumption event, not an automatic per-lead repricing event.

Why the timing aligned with the bureau cycle

The April 22 announcement landed at a particular moment in the credit-bureau pricing cycle. FICO had spent the prior eighteen months reformulating its commercial relationship with the bureaus – moving in late 2024 to a fixed $3.50 royalty per score for both soft and hard pulls, then in October 2025 launching a Mortgage Direct License Program that bypassed reseller markups. The bureaus, in turn, had been signaling capacity to compete on a non-FICO product as soon as a regulatory pathway opened.

What FHFA did was open the pathway. The bureaus did the rest in seventy-two hours, at the score-component layer. The result is that mortgage lead operators now have access to a VantageScore 4.0 score component priced between free and $4.50 per pull depending on bureau choice – versus the $4.95 per FICO score wholesale that has anchored prequalification cost assumptions since the post-2008 reform era. The all-in tri-merge bundle remains separate; the bundle still wraps the score with full credit-report data and prices accordingly.

For operators who built their funnel on the assumption that a soft-pull score component costs $2 to $3 and gates the prequalification event, that assumption is shifting. The hard-pull tri-merge bundle remains the gating cost at the application step, and that bundle has not collapsed alongside the score component.

The Three Dimensions of the Pre-Qualification Funnel Reset

Beneath the surface of the announcement sit three distinct shifts, each of which independently affects mortgage lead unit economics. Operators who treat this as a single change miss the compound effect.

Dimension one: the soft-pull cost floor collapses

The first shift is the most direct. A soft-pull credit inquiry – one that does not affect the consumer’s credit score – historically cost lead generators between $2 and $3 per pull when sourced through prequalification platforms or bureau-direct APIs. That floor was set primarily by the bureaus’ wholesale margin on the underlying score plus integration overhead. With VantageScore 4.0 at $0.99 from TransUnion and free from Experian, the underlying scoring component is no longer the binding cost driver. Integration and identity-verification costs become the new floor.

For a mortgage funnel that runs at, say, ten thousand prospect prequalifications per month, the difference between a $2.50 average soft-pull cost and a $1.25 average soft-pull cost is $15,000 monthly – $180,000 annualized. That is not strategic-level money, but it is operationally meaningful at the volume tier most performance-marketing-driven mortgage lead aggregators operate at. More importantly, it changes what is feasible. A pre-qualification gate that was uneconomic at $2.50 may be economic at $1.25 for prospects whose conversion probability sits in the marginal zone – the borrowers a publisher would have routed to a shared-lead bucket before but can now route through a soft-pull qualification step first.

Dimension two: the soft-pull / hard-pull spread becomes the funnel’s load-bearing variable

The second shift is structural. With soft-pull prices collapsing and tri-merge prices climbing, the spread between the two has widened from roughly 20-to-1 in 2024 to something closer to 40-to-1 in 2026. That spread is now the variable that determines whether a lead operator’s pre-qualification funnel is economically viable.

A simplified version of the math: a mortgage lead funnel that captures a prospect at $40 in paid-media cost, qualifies that prospect through a soft-pull at $1.25, and routes the qualified subset to a buyer at $80 generates a positive contribution margin even if only fifty percent of soft-pull-qualified prospects convert to billable leads. The same funnel run with a $2.50 soft-pull and a sixty percent qualification yield generates roughly the same margin. Now consider the alternative: skipping the soft-pull and running every prospect through a hard-pull tri-merge at $47. That funnel requires either dramatically higher per-prospect billable-lead pricing or a dramatically higher conversion rate to break even.

What changes after April 22 is that the soft-pull pre-qualification path becomes economically dominant for a much wider range of prospect cohorts. Funnels that were marginal under the old pricing become viable. Funnels that were viable become more profitable. And operators who previously skipped pre-qualification altogether – running every prospect to a buyer who would themselves pay for the credit pull – find their lead pricing under pressure as buyers begin demanding pre-qualified inventory at the same per-lead price points.

Dimension three: the LLPA risk-weighting layer changes the buyer-side bid

The third shift is the most subtle and the most important. Fannie Mae and Freddie Mac, per their April 23 selling-guide updates, will operate separate loan-level pricing adjustment grids for VantageScore 4.0 and FICO 10T. The grids will reflect the different risk-weighting characteristics of each model – VantageScore 4.0’s incorporation of rent and utility payment history, FICO 10T’s twenty-four-month trended credit behavior – and will result in different pricing outcomes for borrowers with the same nominal score from each model.

For lead buyers – the lenders and brokers ingesting mortgage leads from publishers and aggregators – this introduces a new variable into the bid logic. The same lead, scored under different models, may carry different acquisition value to different lenders depending on which model their pricing infrastructure favors. Some lenders will optimize for VantageScore 4.0 borrowers because the LLPA grid is more favorable for thin-file applicants who score well on alternative-data metrics. Others will optimize for FICO 10T because their book is concentrated in trended-credit-favorable cohorts. The result is that the buyer waterfall – the routing logic that sends a given lead to the highest bidder – now has a model-dependent dimension.

Lead operators who continue to deliver leads as score-agnostic units will find their pricing compressed against operators who deliver leads tagged with the model that best fits each buyer’s pricing grid. This is not a 2027 problem. It is a Q3 2026 problem, because the LLPA grids go live with the loan-delivery flows that began in late April.

The Approaches That Will Underperform This Cycle

Three responses to the April 22 announcement are visible in the early industry chatter. Each will produce worse outcomes than its proponents expect, and the reasons are worth being explicit about.

The first is the wait-and-see posture. The argument runs that the FHA implementation is still “in coming months,” that the LLPA grids are not fully published, and that the secondary-market liquidity for VantageScore 4.0 loans is still small (Freddie Mac’s first securitization wave was about $10 million). Until the dust settles, the wait-and-see operator continues running funnels on existing tri-merge economics. The problem is that the bureau price war is not waiting for the FHA timeline. The pricing change is real now. Operators who delay will run funnels at marginal-cost disadvantages relative to operators who do not, and the lost margin compounds monthly. By the time the FHA implementation completes and the secondary-market liquidity scales, the operators who moved first will have established cost positions that the wait-and-see cohort cannot easily match.

The second is the hard-pull-only posture. Some operators read the announcement as a low-quality alternative scoring path and conclude that the right defensive response is to continue gating every prospect through a full tri-merge at the front of the funnel. The argument is that lead-buyer preferences favor hard-pull-verified prospects and that the additional friction is a quality moat. The argument was sound in 2022, and it is wrong in 2026. Hard-pull-only funnels cannot compete on per-prospect acquisition cost with funnels that use a soft-pull pre-qualification step before the hard-pull. The economics are stark: a hard-pull-only funnel that captures and qualifies one in five prospects at $47 per qualified hard pull carries a $235 per-billable-lead floor on credit-bureau cost alone. A two-stage funnel that captures, soft-pull-qualifies, and then hard-pulls the qualified subset carries a per-billable-lead bureau cost closer to $80. Buyer demand for hard-pull-verified inventory does not justify a 3x cost differential.

The third is the score-agnostic posture. This is the response of operators who continue treating mortgage leads as a single inventory pool, with credit scores reported as data points rather than as model-tagged attributes. The argument is that the LLPA grid differences are minor and that buyers will accept any score model. They will not. By Q3 2026, lender bids will diverge by model – and operators who do not capture and report the model used in qualification will be selling, in effect, a generic average against operators who can deliver model-matched inventory. The score-agnostic operator is bidding against a tagged inventory operator who can extract a fifteen percent premium on each side of the spread.

The common pattern across these three approaches is the same: each underestimates the speed at which the buyer side of the market will reprice, and each fails to recognize that the policy change is already live in the unit-economic layer regardless of how slowly it appears to roll out at the regulatory layer.

The Strategic Reframe: Three Principles for the Re-Priced Funnel

The right response to April 22 starts from a different premise. The credit-bureau pricing layer of the mortgage funnel is no longer a fixed cost block to be optimized around. It is a variable cost block to be designed against. Three principles flow from that premise.

Principle one: bundle scoring with prospect routing, not with qualification

In the old funnel, the credit pull happened once – at the qualification step – and the resulting score was used to gate the prospect into either a billable-lead bucket or a discard bucket. In the re-priced funnel, the score happens early and cheaply, and it carries forward as a routing input through multiple buyer matches. A prospect who scores 720 on VantageScore 4.0 with strong alternative-data signals (rent, utilities) routes to lenders whose VantageScore 4.0 LLPA grid favors thin-file 720s. The same prospect, scored 705 on FICO 10T because of weaker trended-credit behavior, routes to a different lender whose FICO 10T grid is more forgiving on borderline scores. The operator captures the higher of the two bids.

What this requires operationally is a scoring layer that is cheap enough to run twice – once on each model – and a routing layer that can ingest model-tagged scores as bid inputs. The first is now affordable. The second is a build that most lead-distribution platforms have not started. Operators who complete the build before competitors do will run a routing engine that competitors cannot match on per-lead margin.

Principle two: stage qualification by cost, not by step

The legacy funnel architecture treats qualification as a single event: capture the prospect, pull the credit, decide. The re-priced funnel architecture treats qualification as a staged sequence in which each stage is sized to its marginal cost. A free Experian VantageScore 4.0 inquiry is run at the top of the funnel for every prospect. A paid TransUnion or Equifax pull is run only on prospects who pass the free-inquiry threshold. A full tri-merge is run only on prospects who have already converted to a billable lead and are approaching application. Each stage carries its own gate and its own pricing, and the prospect’s accumulated cost rises only as conversion probability rises.

This is the principle that turns the bureau price war from a cost reduction into a margin restructure. The same total credit-bureau spend, deployed in a staged sequence, qualifies more prospects per dollar than the same spend deployed in a single up-front pull. For a funnel running tens of thousands of prospects per month, the compounded effect is a thirty to fifty percent improvement in per-billable-lead bureau efficiency.

Principle three: re-price the buyer waterfall against the new bureau-cost floor

The legacy buyer waterfall was tiered on a relatively flat cost base: every lead carried a similar bureau-cost burden, so the tiering logic was driven mostly by buyer pricing tiers and exclusivity terms. The re-priced waterfall has a more complicated cost base. A prospect run through the staged qualification described above carries different accumulated bureau costs depending on which stages they passed through. A prospect who passed only the free Experian inquiry carries about $0.10 in attributable identity-verification cost. A prospect who passed both the free and the $0.99 TransUnion stages carries roughly $1.10. A prospect who passed all three stages and a full tri-merge carries about $48.

The buyer waterfall should reflect this: highest-tier buyers (exclusive, with the strongest pricing grids) get prospects who passed all stages and carry the highest accumulated cost. Mid-tier buyers (shared, with broader pricing tolerance) get prospects who passed two stages. Lowest-tier buyers (open marketplace) get prospects who passed only the free inquiry. Each tier is priced to recover its accumulated cost plus a margin layer, and the waterfall is dynamic rather than static – prospects route based on real-time bid response, not a fixed cascade.

The result is a waterfall that maximizes per-buyer margin at every tier while preserving the operator’s option value across the buyer set. It is a structurally more complex waterfall than what most operators run today, and the design work is non-trivial. It is also the only waterfall that captures the full margin opportunity that April 22 created.

Evidence and Early Movers: Pennymac, Rocket Mortgage, and the Newrez Securitization Signal

The decision did not arrive in a vacuum. Three named lender activities in April 2026 give early evidence about how the market will reprice.

Pennymac, named publicly as one of the twenty-one large lenders in the FHFA pilot, has run its own internal validation of VantageScore 4.0 against FICO since 2023. The lender’s reported strategic interest in Vantage has been driven by its book concentration in markets with high renter-to-buyer transition volumes – exactly the cohort that VantageScore 4.0’s rent-and-utility incorporation is designed to score better. For lead operators routing prospects to Pennymac, the practical implication is that the bid for Vantage-scored thin-file prospects (first-time buyers, recent renters) will be higher under the new model than under the legacy FICO-only architecture. A lead operator capturing prospects with strong rent payment history but limited revolving credit who fails to score them under VantageScore 4.0 is leaving bid uplift on the table.

Rocket Mortgage’s role in the pilot reflects a different strategic calculus. Rocket has invested heavily in its own underwriting infrastructure and has the technical capacity to run dual-model scoring at scale. The lender’s participation signals that it views VantageScore 4.0 as additive – a way to compete for borrower segments that FICO scores less favorably – rather than as a replacement. For lead operators, the implication is that Rocket’s bid logic will be model-aware. A Rocket bid on a Vantage-scored prospect will reflect the LLPA grid for that prospect’s specific Vantage 4.0 score, and a Rocket bid on the same prospect’s FICO 10T score will reflect a different grid. Operators who report both scores capture both bids; operators who report neither capture an average that is structurally below the model-matched price.

The Newrez securitization signal is the most operationally instructive. Newrez originated and delivered the first wave of VantageScore 4.0-scored loans to Freddie Mac in late April 2026, totaling approximately $10 million in initial securitized volume. The number is small relative to Freddie Mac’s monthly origination flow, but the speed is the signal – Newrez was able to take a prospect from application to securitization under the new model within days of the FHFA announcement. The infrastructure required to do that – a loan origination system with VantageScore 4.0 integration, an LLPA grid configuration that handled the new model, and a securitization pathway that Freddie Mac would accept – was clearly built before April 22. Lenders without that prepared infrastructure will spend Q2 and Q3 2026 building it. Operators routing leads to those late-mover lenders will see slower conversion velocity and lower per-lead pricing during the build period.

The data-quality consideration most operators are missing

VantageScore 4.0’s incorporation of alternative payment data – rent and utilities – is structurally favorable to a specific demographic that overlaps with several mortgage lead-gen vertical strategies. According to U.S. News reporting that summarized the Federal Reserve and HUD-cited research, on-time rent payment history can materially improve the credit profile of borrowers who would otherwise be classified as thin-file or invisible under the legacy FICO architecture. For lead operators in markets where rent burden is high and home-ownership transition rates are rising – Sunbelt metros, post-pandemic migration corridors – the prospect pool that becomes scoreable under VantageScore 4.0 is materially larger than the pool scoreable under FICO 8.

What this means in practice is that an operator capturing prospects from a first-time-buyer-focused funnel gets two compounding benefits from VantageScore 4.0 adoption: a larger qualifiable prospect pool (because thin-file prospects now score) and a higher bid per qualified prospect (because the LLPA grid favors strong-rent-history applicants). The combined effect on funnel margin is significantly larger than the bureau-cost reduction alone.

The broader pattern: the April 22 decision is not a single change but a layered change. Each layer compounds with the others. Operators who model only one layer will systematically understate the opportunity.

Implementation Reality: What It Actually Takes to Capture the Re-Priced Funnel

The strategic reframe is straightforward. The implementation is not.

Resource requirements

Building a staged qualification funnel against the new bureau pricing requires three types of investment that most lead-distribution platforms have not budgeted for. The first is API integration with multiple bureaus’ VantageScore 4.0 endpoints – Experian’s free pathway, TransUnion’s $0.99 pathway, Equifax’s $4.50 with bundle pathway. Each bureau exposes a different integration surface, and the integration cost is non-trivial. Operators running on legacy single-bureau integrations should plan for sixty to one hundred and twenty engineering days to complete the multi-bureau integration with the staging logic that makes the pricing tiers work.

The second is the model-tagged routing infrastructure. Most lead-distribution platforms route on a flat-prospect-record schema that does not distinguish between Vantage and FICO scores. Adding model-tagged routing requires schema changes in the prospect-record store, in the buyer-bidding interface, and in the analytics and reporting layer. For a platform handling tens of thousands of prospects per month, this is a forty-to-eighty engineering-day project plus operational changes to buyer onboarding documentation. Most platforms will need to push the project to Q3 2026 at the earliest, which is exactly when the LLPA grids will be live and the pricing premium for tagged inventory will be peaking.

The third is compliance review. The new pricing-tier funnel involves more pull events per prospect, with different bureau footprints depending on the staging path. Each pull, even a soft pull, creates a regulatory artifact. Operators need to validate that their consent disclosures, retention policies, and adverse-action protocols cover the new staging logic. A compliance review of the multi-stage funnel is typically a two-week external counsel engagement. It is not optional.

Timeline expectations

A realistic implementation timeline for a mid-sized mortgage lead operator:

| Phase | Duration | Key Activities |

|---|---|---|

| Bureau API integration | 60–120 days | Connect Experian VantageScore 4.0 free endpoint; TransUnion $0.99 endpoint; Equifax $4.50 endpoint |

| Staging logic build | 30–60 days | Implement free → paid → tri-merge staging gates with prospect-record propagation |

| Routing schema update | 40–80 days | Tag prospects by model; update buyer bid interface; update analytics layer |

| Compliance review | 14–21 days | External counsel review of consent flow, retention, adverse action |

| Buyer onboarding | 30–45 days | Communicate model tagging to existing buyers; renegotiate pricing tiers where appropriate |

| Total elapsed time | 4–6 months | Conservative estimate for a platform without prior multi-bureau integration |

Source: Composite of MBA implementation guidance and analysis of FHFA implementation timeline

Common obstacles

Three obstacles consistently slow these implementations beyond the nominal timeline. The first is buyer fragmentation. Mortgage lead operators typically work with twenty to one hundred buyers, each with its own bid logic and onboarding process. Communicating the new model-tagged inventory and renegotiating pricing tiers takes longer than engineering work because it depends on each buyer’s internal cycle. Operators who start the buyer conversations before the engineering work is complete tend to compress the overall timeline.

The second is the analytics gap. Most lead-distribution platforms run analytics on a prospect-funnel basis without model attribution. Adding model-tagged analytics requires either a re-platform or an extension of the existing analytics layer. The re-platform is rarely justifiable on this single change; the extension typically takes longer than expected because it surfaces edge cases in the existing analytics design.

The third is the pricing-tier negotiation. The shift from a flat prospect-cost base to a staged-cost base requires re-pricing the buyer waterfall. Buyers who have been paying a flat per-lead price will not accept a staged-cost-pass-through model without a negotiation. Operators who try to absorb the re-pricing without buyer negotiation end up with margin compression. Operators who negotiate well end up with margin expansion.

The implementation is hard. The operators who complete it before the rest of the market reprices will run a six-to-twelve-month structural margin advantage.

Future Implications: The Five-Year Trajectory of Mortgage Lead Pricing

The April 22 decision is the first event in a multi-year sequence. The shape of the sequence is reasonably predictable from the structure of the market.

In the next twelve months, the bureau price war will widen. Equifax’s $4.50 with bundle pricing will face pressure from TransUnion’s $0.99 and Experian’s free positions; expect Equifax to match or undercut by Q4 2026. FICO will respond with further pricing moves – likely a permanent reduction in its mortgage royalty rate to defend share against Vantage 4.0. The sub-$1 per-score tier will become the new baseline, and the marginal scoring cost will approach zero.

In the next twenty-four months, the pre-qualification funnel architecture will standardize around staged qualification. The handful of operators who build the staged funnel in 2026 will be the proof points. By mid-2027, the staged funnel will be table stakes for mortgage lead operators above a minimum scale threshold. Operators who do not adopt will be pushed to the lowest-margin tiers of the buyer waterfall.

In the next thirty-six months, the LLPA grid divergence will compress. The GSEs’ separate pricing grids for VantageScore 4.0 and FICO 10T are an interim design while both models accumulate sufficient secondary-market performance data. By 2029, expect a single integrated grid that incorporates both models with cohort-specific weights – at which point the model-tagged routing premium that operators capture in 2026-2028 will narrow significantly.

The longer-term shift is more interesting. The April 22 decision is a precedent for what happens when the FHFA opens a competitive pathway in a previously single-vendor regulated market. Other layers of the mortgage stack – appraisal, title, loan origination software – operate under similar single-vendor or oligopoly conditions. The political case for opening those layers will be made by reference to the success of credit-score competition. Operators who build infrastructure flexibility now will be positioned to capture the next round of competitive openings as they arrive.

For lead generators, the strategic implication is to design the funnel for the world after the next FHFA competition, not just the world after this one. A funnel architecture that abstracts the credit-scoring layer so that any model from any vendor can be plugged in is a more durable architecture than one optimized specifically for the April 22 scoring options.

Key Takeaways

The April 22, 2026 FHFA decision and the bureau price war that followed reset the unit economics of mortgage pre-qualification funnels in ways that compound across multiple cost layers. Treating the change as a single-vendor swap underestimates what happened.

The score-component layer of the funnel – the VantageScore 4.0 score itself, not the all-in tri-merge bundle – repriced to between free and $4.50 per pull within seventy-two hours. The tri-merge bundle remained near $47 because it includes full credit-report data alongside the score. The widened spread between the score-component cost and the all-in bundle cost is a load-bearing variable in funnel design; the bundle-level cost has not collapsed.

VantageScore 4.0’s incorporation of rent and utility payment history is structurally favorable to thin-file and first-time-buyer cohorts, expanding the qualifiable prospect pool and creating bid uplift on Vantage-tagged inventory for lenders whose pricing grids favor those cohorts.

Fannie Mae and Freddie Mac will operate separate LLPA pricing grids for VantageScore 4.0 and FICO 10T at least through 2028, which means the same prospect can carry different bid value to different lenders depending on which model the lender’s grid favors – making model-tagged routing a margin-extraction lever for the next twenty-four months.

Pennymac, Rocket Mortgage, and Newrez represent the early-mover cohort of the twenty-one-lender pilot; their pricing logic and infrastructure readiness set the pace for the rest of the market, and operators routing leads to late-mover lenders will see slower conversion velocity through Q3 2026.

Three approaches will underperform: the wait-and-see posture (loses margin every month it persists), the hard-pull-only posture (carries a 3x bureau-cost disadvantage versus staged funnels), and the score-agnostic posture (cedes the model-tagged routing premium to competitors).

The implementation is non-trivial. A mid-sized mortgage lead operator should plan four to six months of engineering, compliance, and buyer-negotiation work to capture the re-priced funnel, with bureau API integration, model-tagged routing schema, and pricing-tier renegotiation as the three critical-path items.

The five-year trajectory points toward sub-$1 per-score baseline pricing, standardized staged-qualification architecture by mid-2027, LLPA grid convergence by 2029, and broader competitive openings in adjacent layers of the mortgage stack – appraisal, title, loan origination – that will reward operators with flexible funnel architectures.

For lead operators currently running tri-merge-only or score-agnostic funnels, the next ninety days are the planning window. The next one hundred and eighty days are the build window. The first lenders to reprice their bids on the new architecture are doing it in Q3 2026; the operators who arrive at that conversation with model-tagged inventory and staged funnels capture the margin opportunity. The operators who arrive later compete for what is left.

Frequently Asked Questions

What did the FHFA actually decide on April 22, 2026?

The FHFA, jointly with HUD, announced that Fannie Mae and Freddie Mac would accept VantageScore 4.0 for mortgage underwriting effective immediately, with twenty-one large lenders selected for an initial implementation pilot. FHA announced it would accept both VantageScore 4.0 and FICO Score 10T “in coming months.” The decision formally ended a process that began with FHFA’s 2022 validation of both models and represented the first time a non-FICO scoring model has been operationally accepted across the GSE-funded mortgage stack. Within seventy-two hours of the announcement, the three credit bureaus repriced VantageScore 4.0 sharply downward – TransUnion to $0.99 per score, Experian to free, Equifax to $4.50 with a free bundle through 2026 – turning the decision into both a policy event and a unit-economic event.

Why does the bureau price war matter more than the scoring-model swap for lead generators?

The scoring-model swap affects which credit model lenders use to assess underwriting risk. The bureau price war affects the marginal cost of every credit inquiry that flows through a mortgage lead funnel. For a lead operator running pre-qualification at scale, marginal cost is the variable that determines funnel viability – not the underlying risk model. With VantageScore 4.0 priced between $0.99 and $4.50 per pull (versus FICO at $4.95 wholesale plus $33 per funded loan), the soft-pull pre-qualification step that gates most mortgage lead funnels just became dramatically cheaper. Funnels that were marginal at $2.50 per soft-pull are profitable at $1.25. Funnels that were profitable become more profitable. The scoring-model swap is the headline; the bureau price war is the unit-economic event.

How does VantageScore 4.0 differ from the FICO scores mortgage lenders have used historically?

VantageScore 4.0 incorporates trended credit data and alternative payment histories – rent and utility payments specifically – that FICO 8 and earlier FICO versions do not use. FICO Score 10T, which is being adopted alongside VantageScore 4.0 in the April 2026 decision, also uses trended data but draws primarily from twenty-four months of credit-account behavior rather than alternative-data sources. The practical effect: VantageScore 4.0 produces materially different scores for thin-file applicants, recent renters with limited revolving credit, and borrowers whose credit history shows strong payment patterns on non-traditional accounts. For mortgage lead generators serving first-time-buyer or post-pandemic-renter cohorts, the prospect pool that becomes scoreable under VantageScore 4.0 is larger than the pool scoreable under legacy FICO models.

What is a soft-pull pre-qualification funnel and why does the bureau price war matter for it?

A soft-pull pre-qualification funnel is a lead generation workflow that uses a credit inquiry which does not affect the consumer’s credit score to qualify mortgage prospects before triggering a full hard-pull tri-merge. Soft pulls historically cost lead operators between $2 and $3 per inquiry; hard-pull tri-merges cost $33.50 in 2025 and $47.05 in 2026. The economic rationale of the soft-pull funnel is that it filters out prospects who will not qualify for a mortgage before the operator incurs the much higher hard-pull cost. With VantageScore 4.0 now priced between $0.99 and $4.50 per soft pull, the cost basis of the entire pre-qualification funnel collapses, expanding the range of prospect cohorts where soft-pull qualification is economically dominant over either hard-pull-first or no-qualification approaches.

Which lenders are in the FHFA’s twenty-one-lender pilot and what does that mean for lead routing?

Pennymac, Rocket Mortgage, and Newrez have been publicly named as participants. Newrez originated the first wave of VantageScore 4.0-scored loans, totaling approximately $10 million securitized by Freddie Mac in late April 2026. The full list of twenty-one has not been published in trade press, but the cohort is described as the country’s largest GSE-eligible originators. For lead operators, the practical implication is that these twenty-one lenders have prepared infrastructure to ingest, score, and price Vantage-scored inventory immediately. Lenders outside the pilot will spend Q2 and Q3 2026 building that infrastructure, during which time leads routed to non-pilot lenders will see slower conversion velocity and lower per-lead bid pricing than leads routed to pilot participants.

How should lead operators think about LLPA grid divergence between VantageScore 4.0 and FICO 10T?

Loan-level pricing adjustments are the rate-and-fee modifications Fannie Mae and Freddie Mac apply to mortgage pricing based on borrower risk characteristics. Per the April 23, 2026 selling-guide updates, the GSEs will operate separate LLPA grids for VantageScore 4.0 and FICO 10T, reflecting the different risk-weighting characteristics of each model. The practical implication: the same prospect, scored under both models, may carry different bid value to different lenders depending on which grid is more favorable to that prospect’s profile. A thin-file applicant with strong rent history may produce a higher bid from a lender whose VantageScore 4.0 grid favors that profile, while a borderline trended-credit applicant may produce a higher bid from a lender whose FICO 10T grid favors that profile. Lead operators who report both scores capture both bids; operators who report neither capture an average price that is structurally below the model-matched price.

What does this mean for tri-merge credit report costs over the next twelve months?

Tri-merge credit report pricing rose from $33.50 in 2025 to $47.05 in 2026, with some vendor and broker pricing reaching $200 to $220 per report. The April 22 bureau-pricing reset does not directly reduce tri-merge prices, because tri-merge bundles include both score and full credit report data from each of the three bureaus. However, the pricing pressure on the score component will likely cascade into modest tri-merge price moderation as the bureaus seek to defend their bundled-product margins against unbundled-score competition. Over the twelve months following April 22, expect tri-merge price growth to slow significantly versus the 40-percent annual increases of 2024-2026, with the possibility of flat or modestly declining tri-merge pricing in 2027 if competitive pressure intensifies. The bigger structural change is that the tri-merge will become a less central component of the funnel, run only at the late-stage application step rather than at the qualification gate.

What are the compliance considerations for running a multi-stage qualification funnel?

A multi-stage qualification funnel involves more credit-bureau pull events per prospect, with different inquiry types (free, paid soft, paid hard) and different bureau combinations at each stage. Each pull, including soft pulls, creates a regulatory artifact under the Fair Credit Reporting Act, the Equal Credit Opportunity Act, and TCPA-adjacent state-level rules. Operators need to validate that their consent disclosures explicitly cover the staging logic, that retention policies handle multi-stage pull records appropriately, and that adverse-action protocols address scenarios in which a prospect is gated out at an intermediate stage rather than at the final hard-pull. A typical compliance review of a multi-stage funnel is a two-week external counsel engagement and is not optional; the regulatory framework around multi-stage pulls is well established but requires explicit configuration to avoid disclosure or retention gaps.

How does this affect mortgage lead pricing and the buyer waterfall?

The buyer waterfall – the routing logic that sends each lead to the highest-bidding buyer – historically operated on a relatively flat cost base, with most leads carrying a similar bureau-cost burden. The re-priced funnel produces a more complex cost base: prospects who passed only the free Experian inquiry carry roughly $0.10 in attributable identity-verification cost; prospects who passed both free and $0.99 paid stages carry roughly $1.10; prospects who passed all three stages and a tri-merge carry about $48. The waterfall design that captures the most margin tiers buyers against the accumulated cost of each prospect – exclusive top-tier buyers receive prospects who passed all stages, mid-tier shared buyers receive prospects who passed two stages, and lowest-tier marketplace buyers receive prospects who passed only the free inquiry. Operators who run a static waterfall designed for the old cost base will systematically misprice inventory under the new architecture.

What is the realistic timeline for a mid-sized mortgage lead operator to capture the re-priced funnel opportunity?

A typical implementation timeline runs four to six months end-to-end, broken into three parallel work streams. Bureau API integration takes sixty to one hundred and twenty days for operators on legacy single-bureau infrastructure, covering the multi-bureau VantageScore 4.0 endpoints. Staging-logic build takes thirty to sixty days for the free-to-paid-to-tri-merge gating sequence. Routing schema updates take forty to eighty days for model-tagged prospect records, buyer bid interface changes, and analytics extension. Compliance review runs in parallel for two to three weeks. Buyer onboarding – communicating the model-tagged inventory and renegotiating pricing tiers across the operator’s buyer set – runs thirty to forty-five days but typically extends because it depends on each buyer’s internal cycle. The operators who finish ahead of the four-to-six-month timeline are those who started buyer conversations in parallel with engineering work rather than sequentially.

How will this decision evolve through 2029?

The five-year trajectory points to four sequential shifts. In the next twelve months, expect Equifax to match TransUnion’s $0.99 or undercut, and FICO to permanently reduce its mortgage royalty rate. In the next twenty-four months, the staged-qualification funnel will standardize as table stakes for mortgage lead operators above a minimum scale threshold. In the next thirty-six months, the GSEs’ separate VantageScore 4.0 and FICO 10T LLPA grids will converge into a single integrated grid as both models accumulate secondary-market performance data, narrowing the model-tagged routing premium that operators can capture in 2026-2028. By 2029, the precedent set by credit-score competition will likely have been extended to other layers of the mortgage stack – appraisal, title, loan origination software – creating additional rounds of competitive opening that operators with flexible funnel architectures will be best positioned to capture.

What about operators who buy leads from third parties rather than generating them?

Lead buyers – lenders and brokers who purchase pre-qualified mortgage leads from publishers and aggregators – face a parallel set of decisions. The most important is to ensure their bid logic accommodates model-tagged inventory rather than treating all credit scores as a single attribute. Buyers whose bid interfaces still operate on a flat-score schema will systematically overpay for leads that scored well only on the model that disfavors their LLPA grid, and underpay for leads that scored well on the favorable model. Updating bid logic to incorporate model attribution is a smaller engineering change than the operator-side staged-funnel build, but it is essential for capturing the LLPA divergence premium. The buyer-side renegotiation that operators are initiating in Q3 2026 is the moment when sophisticated buyers will reprice their bids upward for tagged inventory; buyers who delay the bid-logic update will pay generic-average prices for inventory their LLPA grid would have valued more highly under model-aware bidding.

Sources

Tier 1: Primary Government and Regulatory Sources

-

Federal Housing Finance Agency, “Homebuying Advances into New Era of Credit Score Competition,” FHFA News Release, April 22, 2026 – https://www.fhfa.gov/news/news-release/homebuying-advances-into-new-era-of-credit-score-competition

-

U.S. Department of Housing and Urban Development, “Homebuying Advances into New Era of Credit Score Competition,” HUD Release HUD-26-026, April 22, 2026 – https://www.hud.gov/news/hud-no-26-026

-

Federal Housing Finance Agency, “Credit Scores,” FHFA Policy Page, accessed April 28, 2026 – https://www.fhfa.gov/policy/credit-scores

-

Freddie Mac, “Freddie Mac Begins Accepting VantageScore 4.0,” Freddie Mac News Release, April 22, 2026 – https://freddiemac.gcs-web.com/news-releases/news-release-details/freddie-mac-begins-accepting-vantagescore-40

-

Freddie Mac Single-Family, “Credit Score Models and Reports Initiative,” accessed April 28, 2026 – https://sf.freddiemac.com/general/credit-score-models

Tier 2: Established Industry Research and Trade Press

-

Mortgage Bankers Association, “Breaking Advocacy Update: FHFA, HUD Announce Next Steps for VantageScore 4.0, FICO 10T Adoption,” MBA Newslink, April 23, 2026 – https://newslink.mba.org/mba-newslinks/2026/april/mba-newslink-thursday-april-23-2026/breaking-advocacy-update-fhfa-hud-announce-next-steps-for-vantagescore-4-0-fico-10t-adoption/

-

HousingWire, “FHFA launches VantageScore 4.0 pilot; HUD signals FICO 10T for FHA,” April 22, 2026 – https://www.housingwire.com/articles/fhfa-vantagescore-pilot-gses-hud/

-

HousingWire, “Credit report costs for mortgage lenders to rise up to 50% in 2026,” 2026 – https://www.housingwire.com/articles/mortgage-credit-report-costs-2026/

-

HousingWire, “Freddie Mac securitizes first wave of Newrez mortgages with VantageScore 4.0,” April 2026 – https://www.housingwire.com/articles/freddie-newrez-vantagescore/

-

HousingWire, “New credit scores models raise questions on LLPAs and liquidity,” April 2026 – https://www.housingwire.com/articles/fha-hud-credit-scores-llpa/

-

ABA Banking Journal, “HUD, FHFA roll out plans for new credit scoring in mortgages,” April 2026 – https://bankingjournal.aba.com/2026/04/hud-fhfa-roll-out-plans-for-new-credit-scoring-in-mortgages/

-

National Mortgage News, “Fannie, Freddie, FHA to accept VantageScore immediately,” April 2026 – https://www.nationalmortgagenews.com/news/fannie-freddie-fha-to-accept-vantagescore-immediately

-

The Mortgage Point, “FHA, Fannie & Freddie to Begin Accepting New Credit Score Models,” April 22, 2026 – https://themortgagepoint.com/2026/04/22/fha-fannie-freddie-to-begin-accepting-new-credit-score-models/

-

National Mortgage Professional, “FHFA Opens Door To Credit Score Competition As Fannie, Freddie Move Forward With VantageScore 4.0,” April 2026 – https://nationalmortgageprofessional.com/news/fhfa-opens-door-credit-score-competition-fannie-freddie-move-forward-vantagescore-40

-

Inman Real Estate News, “HUD, FHFA greenlight VantageScore 4.0 for home loans,” April 22, 2026 – https://www.inman.com/2026/04/22/vantagescore-4-fhfa-hud-pulte-mortgage-home-loan/

-

Mortgage Professional America, “FHFA to accept VantageScore loans immediately; HUD to accept new scores ‘soon’,” April 2026 – https://www.mpamag.com/us/mortgage-industry/market-updates/fhfa-to-accept-vantagescore-loans-immediately-hud-to-accept-new-scores-soon/572744

-

CNBC, “Cost of credit reports for mortgages center of debate. What to know,” February 22, 2026 – https://www.cnbc.com/2026/02/22/cost-of-credit-reports-for-mortgages-center-of-debate-what-to-know-.html

-

Mortgage Professional, “Mortgage industry has ‘reached the breaking point’ over soaring credit reporting costs,” 2026 – https://www.mpamag.com/us/specialty/wholesale/mortgage-industry-has-reached-the-breaking-point-over-soaring-credit-reporting-costs/561695

Tier 3: Industry and Vendor Statements

-

VantageScore, “FHFA Director and HUD Secretary Jointly Announce VantageScore 4.0 Implementation for Fannie Mae, Freddie Mac and FHA,” VantageScore Knowledge Center, April 22, 2026 – https://vantagescore.com/resources/knowledge-center/fhfa-director-and-hud-secretary-jointly-announce-vantagescore-4-0-implementation-for-fannie-mae-freddie-mac-and-fha

-

FICO, “FICO Mortgage Direct License Program,” accessed April 28, 2026 – https://www.ficoscore.com/mortgagedirectlicense

-

Equifax, “Equifax Statement on the Costs of Credit Scores and Credit Reports,” 2026 – https://www.equifax.com/newsroom/all-news/-/story/equifax-statement-on-the-costs-of-credit-scores-and-credit-reports/

-

AmeriSave, “Understanding Tri-Merge Credit Reports in 2026: What Mortgage Borrowers Need to Know,” 2026 – https://www.amerisave.com/learn/understanding-trimerge-credit-reports-in-what-mortgage-borrowers-need-to-know

-

Factual Data, “Tri-Merge Credit Reports for Mortgage Lenders,” accessed April 28, 2026 – https://www.factualdata.com/products/tri-merge-credit-reports

Tier 4: Supporting Industry Commentary

-

U.S. News, “It’s Official: Paying Your Rent On Time Can Help You Buy a House,” 2026 – https://money.usnews.com/loans/mortgages/articles/its-official-paying-your-rent-on-time-can-help-you-buy-a-house

-

Scotsman Guide, “Shift away from tri-merge credit reports could send mortgage rates higher, study finds,” 2026 – https://www.scotsmanguide.com/news/shift-away-from-tri-merge-credit-reports-could-send-mortgage-rates-higher/

-

Lykken on Lending, “Tri-Merge Credit Costs Spike Again: MBA Pushes for Reform in 2026,” December 2, 2025 – https://lykkenonlending.com/podcasts/tri-merge-credit-costs-spike-again-mba-pushes-for-reform-in-2026/

Closing

The April 22, 2026 announcement is being read for the wrong reason in many trade headlines. The framing in those headlines treated it as the end of FICO’s monopoly on GSE underwriting – a regulatory milestone seven years in the making – and then jumped to “every mortgage lead is being repriced.” That framing conflates three separable layers. The score-model layer changed (eligibility opened). The score-component pricing layer changed within seventy-two hours, materially. The tri-merge bundle and per-lead pricing layers will adjust on slower, buyer-driven cycles, not overnight. The operational event most relevant for lead operators is the launch of separate LLPA grids that will reward operators who can route leads with model awareness for at least the next thirty-six months, alongside the prequal cost-assumption shift on the VantageScore 4.0 component. Operators who treat April 22 as a vendor swap will spend the next two years competing on yesterday’s cost base. Operators who treat it as a layered shift – score-component cost, eventual bundle adjustment, multi-quarter per-lead repricing – will run staged qualification, model-tagged routing, and adjusted buyer waterfalls into a margin window that closes when the rest of the market catches up. The decision is whether to instrument the new score-model-aware funnel before lenders price it back into the market.

Market data, regulatory developments, and bureau pricing reflect publicly reported conditions through April 28, 2026. Credit-bureau pricing, GSE selling-guide terms, and LLPA grid configurations change continuously; verify current terms through primary sources before making operational decisions. This article provides general industry analysis and does not constitute legal, financial, or compliance advice. Consult qualified counsel for specific compliance questions related to multi-stage qualification funnels, consent disclosures, and adverse-action protocols.