Google’s October 2025 developer-blog announcement, formalized through Google Ads Help in early 2026, locked out new call-only ad creation in February 2026 and set February 2027 as the date existing call-only ads stop receiving impressions. The replacement format – responsive search ads with call assets – sits inside the same AI Max architecture that Dynamic Search Ads will auto-upgrade into in September 2026. For pay-per-call operators, this is not a creative refresh. It is the dismantling of the structural advantage that produced 10-to-30x premiums on call leads over form-fill leads, and the start of a multi-year compression in live-transfer pricing.

A Twelve-Month Forced Migration for Every Pay-Per-Call Operator

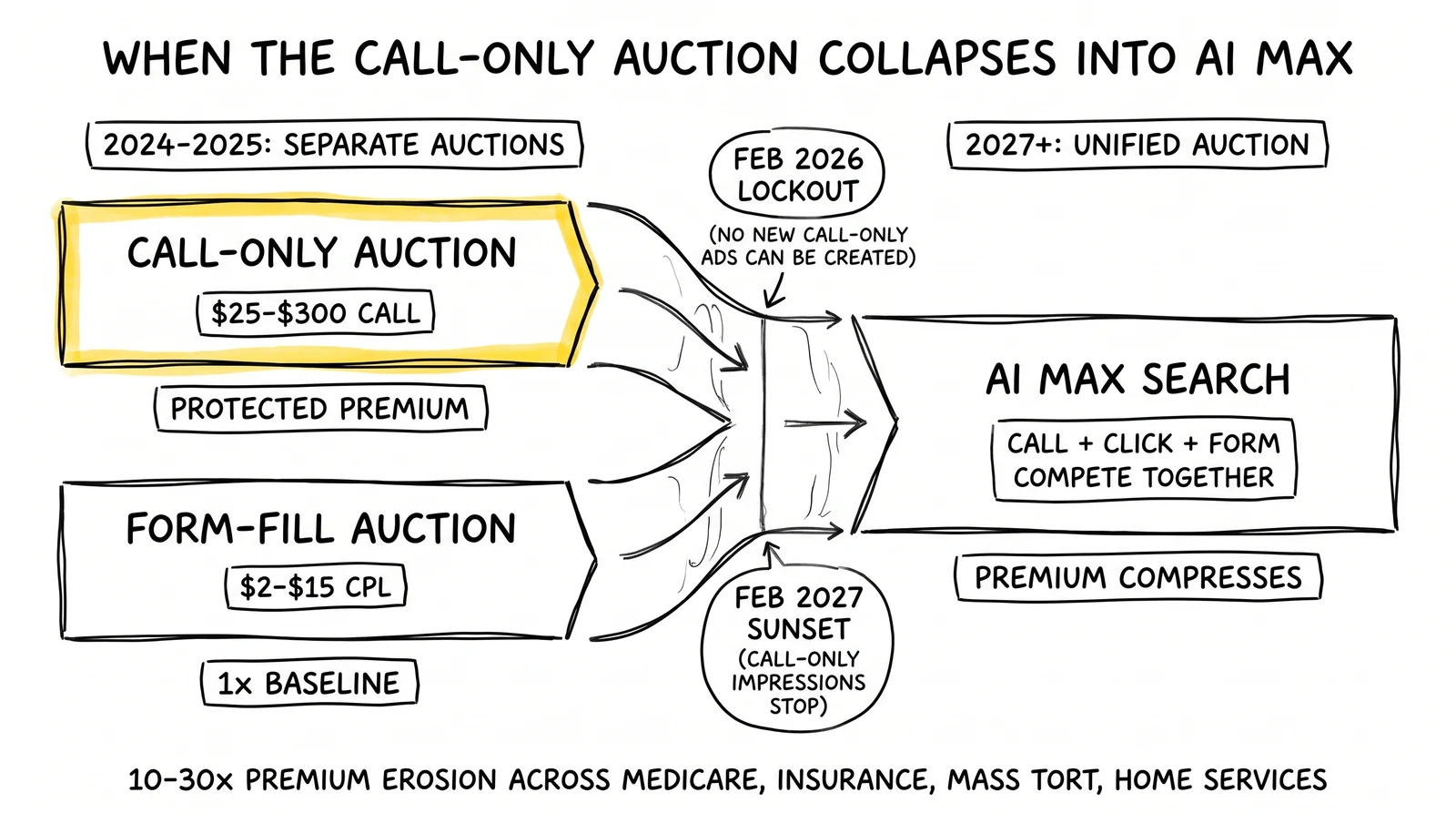

The pay-per-call industry was built on a narrow ad format. For more than a decade, Google’s call-only ad – a mobile-search creative whose primary call-to-action was a tap-to-dial button rather than a click-to-website link – sat in its own auction lane. It competed against other call-only ads. It bypassed the asset-combination and landing-page-quality logic that governed standard search auctions. Insurance agencies, Medicare brokers, mass tort intake firms, and home-services operators built entire publisher economies on top of that lane. Pay-per-call networks like RingPartner, Aragon Advertising, Astoria Company, and Marketcall priced calls at $25 to $300 per qualified billable call – a 10-to-30x premium over form-fill leads in the same verticals – because the call-only format produced caller intent that form clicks did not.

In October 2025, Google’s developer blog instructed advertisers to begin migrating call-only ads to responsive search ads with call assets through the Google Ads API. By January 2026, the trade press was describing the timeline in plain language: February 2026 would close new call-only ad creation, and February 2027 would sunset impressions on every existing call-only ad. In April 2026, Google followed with a separate announcement that Dynamic Search Ads – the other major automated search format – would auto-upgrade to AI Max for Search in September 2026, with new DSA creation disabled at the same point. The two announcements share a single architectural conclusion: by the end of 2026, virtually every Google Ads acquisition path for a pay-per-call operator will live inside the AI Max system, where automated bidding, asset combinations, and search-term matching are governed by the same machine-learning stack regardless of whether the ad’s primary action is a phone call or a form click.

That convergence is the news that matters. The call-only sunset is the policy event. The AI Max convergence is the unit-economic event. This analysis covers what Google actually changed, why responsive search ads with call assets sit on a different cost curve than the call-only ads they replace, how the 10-to-30x pay-per-call premium compresses when call campaigns share an auction with form-fill, what the migration playbook looks like for the next ninety to one hundred and eighty days, and where live-transfer pricing in Medicare, insurance, mass tort, and home services lands by 2030.

What Google Actually Changed – and Why the AI Max Convergence Is the Real Story

The headline is the call-only sunset. The structural change runs underneath it.

The call-only timeline, in operational terms

Google’s October 2025 developer-blog post laid out a phased plan. Beginning February 2026, advertisers can no longer create new call-only ads through any surface – the Google Ads UI, Google Ads Editor, or the Google Ads API. Existing call-only ads continue to serve through 2026. In February 2027, all remaining call-only ads stop receiving impressions. Between those two dates, advertisers can keep their legacy ads live but cannot scale them, cannot duplicate them into new ad groups, and cannot recover any that get accidentally archived. The Google Ads Help center’s transition documentation calls the migration path “Responsive Search Ads with Call Assets” and provides bulk-migration tooling that copies a call-only ad’s headline, description, and phone number into a new RSA-with-call-asset combination. Search Engine Land, PPC Land, and Search Engine Roundtable each independently published the dates and the migration framing. The Google Ads developer-blog post is the primary source of record.

The migration tool is not optional in the long run. Operators who do nothing simply have their call-only ads stop serving in February 2027. Operators who use the migration tool keep their phone-call conversions running, but inside a different ad format with different auction mechanics.

Responsive search ads with call assets – what changes mechanically

A responsive search ad with a call asset is not a call-only ad with a longer creative. It is a structurally different ad unit.

A call-only ad presents a phone number as its dominant visual element. The headline space carries supporting copy. There is no landing page in the conventional sense; the click action is a tap-to-dial event. The auction in which a call-only ad competed was a narrower one, populated overwhelmingly by other call-only ads from operators in the same vertical.

A responsive search ad with a call asset presents up to fifteen headlines and four descriptions, combined dynamically by Google’s machine-learning models. The call asset attaches a phone number as an extension, which renders alongside the ad as a callout that users can tap on mobile or see displayed on desktop. The user has multiple paths: tap to call, click through to a landing page, or in some surfaces interact with sitelinks and other extensions. The auction in which the RSA-plus-call-asset competes is the full search auction for its keywords – populated by every other RSA serving on those keywords, regardless of whether any individual competitor wants the call or the click.

The mechanical implications are three. First, conversion attribution gets noisier. A call from a call-only ad was unambiguous; a call from a call-asset RSA shares attribution with website clicks from the same impression. Second, the call-versus-click ratio falls. With a clickable headline and a landing page in the creative, some users who would have tapped to call on a call-only ad now click through to the website instead. Third, the cost per call rises in any vertical where the broader RSA auction has higher CPCs than the prior call-only auction. None of these effects is uniform across verticals, but each shifts the unit economics in ways operators built their P&Ls without anticipating.

Why AI Max for Search closes the loop

The April 2026 AI Max announcement is the second half of the architectural story. AI Max for Search is Google’s AI-driven campaign type that bundles search-term matching (a successor to broad match), text customization (asset rewriting), and final-URL expansion. In April 2026, Google announced that all Dynamic Search Ads campaigns, automatically created assets, and campaign-level broad match settings would auto-upgrade to AI Max in September 2026, and that DSA creation would be turned off at the same point. AI Max for Search is also the only campaign type – alongside Performance Max – eligible to serve in AI Mode placements, which Google reports appear in approximately 25.5 percent of AI Mode results. Google publishes a 7 percent average conversion-or-conversion-value lift when advertisers use the full AI Max feature suite versus search-term matching alone.

The convergence, from a pay-per-call operator’s vantage, is that responsive search ads with call assets sit inside the same auction architecture and bidding logic that AI Max governs. Once the call campaigns are RSAs, they compete asset-by-asset against form-fill RSAs in the same automated stack. The structural separation that gave call-only ads their own auction is gone. Pay-per-call’s premium was rooted in that separation; the auction that produced the premium does not exist after the migration completes.

This is why the call-only sunset is more than a creative deprecation. It is the dismantling of the structural condition that produced the 10-to-30x pay-per-call premium over form-fill cost-per-lead benchmarks.

The Three Compression Vectors That Hit Pay-Per-Call Premiums Simultaneously

Beneath the format change sit three distinct economic shifts. Each compresses the pay-per-call premium independently. Operators who model only one vector miss the compounding effect.

Vector one: auction-mix compression

Call-only auctions historically had a different competitive set than text-search auctions. Insurance agents bidding on call-only ads competed with other insurance agents who wanted the same caller. The auction floor was set by the marginal call-buying agent’s willingness to pay, which reflected agent commission economics on closed policies.

The RSA-with-call-asset auction is the full RSA auction. An auto-insurance call campaign is now bidding against carrier brand campaigns, comparison-shopping affiliates, lead-gen marketplaces running form-fill RSAs, and direct-to-consumer carriers running website-conversion RSAs – all on the same keywords. The marginal bidder is no longer a call-buying agent; it is whichever advertiser, across formats, has the highest expected value per impression. In verticals where form-fill economics support higher per-impression bids than per-call agent economics – auto insurance, broad health insurance – the auction floor rises and the call-buyer pays more for the same call. In verticals where call-buyer economics still dominate the keyword-level bid – Medicare AEP calls, mass tort intake – the floor moves less, but the variance widens.

For lead operators routing traffic to pay-per-call buyers, the practical implication is that the historical 10-to-30x call-vs-form premium was partially an auction-mix artifact. As call campaigns merge into the form-fill auction, that part of the premium narrows. Estimates of the size of the narrowing depend on vertical and on operator architecture; the direction is unambiguous.

Vector two: conversion-action ambiguity

The second compression vector is internal to the ad unit. A call-only ad produced one conversion type: a phone call. A responsive search ad with a call asset produces multiple conversion types from the same impression – a tap-to-call, a click-through-to-landing-page, sometimes a sitelink interaction. Google’s bidding system optimizes against the conversion goal the advertiser sets, but the mix of actions on any individual impression is no longer call-deterministic.

For pay-per-call operators whose business model depends on a high call-to-impression rate, this is a structural problem. The advertiser keeps paying for impressions that produce clicks-to-website, even when website conversion was not part of the publisher’s monetization plan. The publisher’s effective cost-per-billable-call rises because some share of the ad spend now produces a non-monetizable click rather than a monetizable call. Industry commentary in early 2026 – including coverage in Search Engine Land, PPC Land, and several PPC-agency blogs – has flagged this as the most-cited concern from advertisers running migration pilots: the call ratio falls, and the publisher’s per-call CAC rises, even when impression-level CPMs are unchanged.

The size of the call-ratio drop varies. For verticals where the user’s intent is unambiguously call-first – emergency plumbing, locksmith, urgent legal intake – the drop is small because the user still wants the phone. For verticals where call versus form is roughly indifferent – Medicare research, auto insurance shopping – the drop is larger because the user has a real choice, and Google’s machine learning routes the impression toward whichever conversion the advertiser’s bid signals reward.

Vector three: AI Max bidding-logic uniformity

The third vector is the most subtle and the most important over a multi-year horizon. Once call-asset RSAs operate inside AI Max – either directly as AI Max for Search campaigns or as DSA-upgraded campaigns running in the AI Max environment – the bidding optimization is the same as it is for form-fill campaigns. Smart Bidding’s tCPA, tROAS, and Maximize Conversion Value strategies treat a tap-to-call conversion the same way they treat a form-submit conversion: as a conversion event with an assigned value.

For operators who set the call-conversion value above the form-conversion value (because a call lead is monetized at a higher per-unit price), Smart Bidding will route impressions toward call-likely users – for now. Over time, as the AI Max model accumulates conversion data across both formats and across multiple advertisers, the system’s understanding of which users convert via call versus form gets sharper. The advertisers whose call-conversion values are correctly calibrated will continue to capture call-likely impressions; the advertisers whose values are not calibrated will lose impressions to advertisers with better-calibrated values.

What this means for pay-per-call operators: the era of running a call-only campaign and capturing call-intent users at a structurally subsidized auction price is ending. The new equilibrium is a calibrated-conversion-value auction in which call-buying advertisers compete with form-buying advertisers on a level basis. The premium that survives is the premium justified by the actual lifetime-value differential between call leads and form leads in the buyer’s portfolio – which, for most verticals, is positive but materially smaller than the 10-to-30x ratio that the call-only auction lane preserved.

The Pay-Per-Call Premium: How Big Was It, and How Much Compresses?

The premium is real, but it is not uniform. Quantifying it requires walking through the verticals where pay-per-call has dominant share.

Medicare Advantage AEP – the high-water mark

The 2025 Medicare Annual Election Period produced the most-publicly-cited pay-per-call benchmarks. Astoria Company’s published Medicare lead pricing, network reporting from RingPartner publisher disclosures, and trade-press summaries from publishers covering Medicare AEP and OEP strategy put the 2025 price band at $80 to $150 per qualified Medicare call during AEP, with premium T65 live transfers – pre-qualified, within ninety days of the prospect’s sixty-fifth birthday, with confirmed Part B enrollment timing – clearing $150 to $225. Form-fill Medicare leads in the same period priced at roughly $20 to $50 in shared inventory and $40 to $80 in exclusive inventory. The implied call-to-form premium ranged from roughly 2x at the cheapest call tier to 10x at the live-transfer tier.

For pay-per-call operators running Medicare AEP campaigns, the 2025 numbers were a high-water mark in two senses. They were the highest realized prices in the recent pay-per-call cycle, and they were set under the auction structure that the call-only sunset is dismantling. Operators forecasting 2026 AEP pricing on the assumption that 2025 numbers are a clean baseline are forecasting a number that the auction architecture no longer supports.

A reasonable operator-level forecast: 2026 AEP qualified-call prices compress by 10 to 25 percent against 2025 in the migrated-format world, with most of the compression hitting the low and middle of the band ($80 to $120 calls) rather than the premium tier ($150 to $225 live transfers). The premium tier is more durable because pre-qualification and live-transfer infrastructure adds value the call-format migration does not directly remove. By 2027 AEP, with call-asset RSAs fully integrated into AI Max, the compression deepens – operator-level forecasts in the 20-to-40 percent range against the 2025 high-water mark are defensible. Note that all of these are directional estimates rather than measured outcomes; the migration is in progress, not complete.

Auto and home insurance – the largest auction-mix shift

Auto insurance pay-per-call has historically priced at $25 to $80 per qualified call, with the premium tier covering insurance-specific sub-vertical CPL benchmarks. Form-fill auto insurance leads in the same vertical priced at $5 to $25 in shared inventory. The 2-to-10x call-to-form premium reflected the same auction-lane separation that defined Medicare, but auto insurance is more vulnerable to the auction-mix compression vector because the form-fill auction in auto has very high per-impression bids – driven by carrier brand campaigns and comparison-shopping marketplaces with multimillion-dollar budgets.

Once call-asset RSAs sit in the same auction as those form-fill RSAs, the marginal-bidder analysis turns. The carrier-funded form-fill auction has higher impression-level bids than the agent-funded call auction in many keyword segments. The call-buying agent’s bid no longer sets the auction floor; the carrier’s form-fill bid does. The agent who used to buy auto-insurance calls at $40 may now have to bid $55 to $65 to win the same impression – even though the call-conversion value to the agent has not changed.

The expected outcome is partial: not every keyword shifts, and operator-side bid management can mitigate part of the cost increase. But the auction-mix compression vector hits auto insurance more than it hits Medicare, because auto’s form-fill auction is structurally richer. Operator forecasts for 2027 auto-insurance pay-per-call call prices: a 15-to-30 percent rise in cost-per-billable-call against 2025 baseline, with most of the increase passed through to call-buying agents in the form of higher network rate cards.

Mass tort and personal injury – the most durable premium

Mass tort and personal injury intake calls priced at $200 to $500-plus in 2025, with some elective-surgery and complex-litigation verticals exceeding $1,000. The premium reflected case-value economics: a single qualified mass tort claimant can produce tens of thousands of dollars of attorney fee value, which justifies extreme willingness-to-pay on the call-buying side.

The compression vectors hit mass tort least hard. The auction-mix vector is muted because the mass tort form-fill auction is itself expensive – the law-firm form-fill bid is not far below the law-firm call-fill bid. The conversion-action ambiguity vector is real but partially mitigated by the urgency of the user’s intent: a mass tort prospect who clicks a call asset typically wants to call, because the user’s mental model is “talk to a lawyer.” The AI Max bidding-logic uniformity vector still applies, but the premium it compresses against is the smaller mass-tort form-fill premium rather than the much larger ratio that defined Medicare and auto insurance.

Operator forecasts for mass tort pay-per-call by 2030: pricing roughly flat to slightly down against 2025, with the structural durability concentrated in the live-transfer and pre-qualified tiers. The 10-to-30x call-vs-form premium narrows toward 5-to-15x as form-fill mass tort lead prices catch up to part of the call premium.

Home services – the most vulnerable to the call ratio drop

Home services pay-per-call – HVAC, roofing, plumbing, garage door, locksmith – priced at $20 to $120 in 2025 depending on urgency and metro. The form-fill alternative is a homeowner web form filled out for a quote. The premium reflected urgency: a homeowner with a flooded basement does not fill out a form. The marginal call buyer was the urgency-routed contractor with high closure rates on inbound calls.

Home services is the most vulnerable to the conversion-action ambiguity vector. With a call-asset RSA, a homeowner who would have tapped a call-only button now sees a creative with a “Get a Quote” headline, a website link, and a call button. Some share of the previously call-only homeowners click through to a website and either convert via form or abandon entirely. The publisher’s call-to-impression ratio falls, and per-call CAC rises proportionally.

Operator forecasts for home-services pay-per-call: 10-to-20 percent compression in cost-per-billable-call by 2027, concentrated in the lower tiers of the price band. The premium tier – true emergency-intent calls – is more durable, but the volume of premium-tier calls is smaller than the volume of mid-tier calls, so the network-level revenue-mix shift is meaningful.

The Approaches That Will Underperform This Cycle

Three responses to the call-only sunset are visible in the early operator chatter. Each will produce worse outcomes than its proponents expect.

The first is the “wait until 2027” posture. The argument is that existing call-only ads continue serving until February 2027, so why migrate now? The flaw is that the auction conditions for call-only ads are already changing. Google’s bid landscape adjusts to the migration as advertisers move; the operators who migrate first capture early bidding-data advantages inside the call-asset RSA format and AI Max, and the advertisers who hold legacy call-only campaigns through 2026 are bidding into a thinning auction without the AI Max conversion-data accumulation that the migrating cohort is building. By the time February 2027 forces the migration, the wait-until cohort has no learning data inside the new architecture and competes against advertisers who do.

The second is the “preserve call-only with workarounds” posture. Some operators have explored running pay-per-call traffic through Local Services Ads, Google Voice click-to-call sitelinks, or third-party landing pages with prominent call buttons. None of these is a full substitute for the call-only ad’s auction position. Local Services Ads operate in a different auction with different qualification mechanics. Click-to-call sitelinks attached to standard search ads do not produce the call-first conversion mix that call-only ads produced. Third-party landing pages with click-to-call CTAs face the same conversion-action-ambiguity problem as call-asset RSAs. Each workaround captures some of the call volume; none restores the structural premium.

The third is the “ride out the compression and reprice the rate card” posture. Networks that have spent five years marketing $80-$150 Medicare calls and $200-$500 mass tort calls do not want to publish lower rate cards in 2026. The temptation is to hold rate cards flat, absorb network margin compression, and hope publisher inventory holds up. The flaw is that publisher economics are independently compressing – call ratios drop, per-call CAC rises, publisher margin shrinks. A rate card that does not adjust to the new buyer-side bidding posture will produce buyer churn (because buyers will measure the call quality, conclude the value-per-call has not held, and shift budget) and publisher churn (because publishers will measure their CAC, conclude the network rates do not cover the new acquisition cost, and shift inventory to other networks or to direct buyer relationships).

The common pattern across these three approaches: each underestimates the speed at which the migrating cohort builds compounding bidding-data advantages inside the new architecture. The pay-per-call operators who treat the migration as a deferral problem will spend 2027 and 2028 catching up to operators who treated 2026 as the build year.

The Strategic Reframe: A Migration Playbook for the Next 180 Days

The right response starts from a different premise. The call-only sunset is not a creative deprecation; it is a structural shift in how call campaigns interact with Google’s AI auction. Three principles flow from that premise.

Principle one: migrate aggressively, not minimally

The bulk-migration tool that Google ships through Google Ads Help is the minimum migration. It copies a call-only ad’s headline, description, and phone number into a call-asset-equipped RSA. The minimum migration preserves nothing about how the original ad’s creative was tuned to a call-first user, because the new RSA format has fifteen headline slots, four description slots, and asset-combination logic that the original ad never used.

The aggressive migration treats the new format as a rebuild. Each ad group gets a full RSA built with multiple call-emphasizing headlines (“Call Now,” “Speak to an Agent,” “24/7 Phone Support”), descriptions that reinforce phone-first intent, a call asset, and supporting extensions (location, structured snippets) that lift the call-asset’s impression share within the rendered ad. Conversion goals are configured to weight the tap-to-call event significantly above the website-click event. Smart Bidding’s tCPA target is set against the call-conversion value, not the blended-conversion value.

The aggressive migration takes more engineering and creative work – typically thirty to ninety days for a mid-sized pay-per-call publisher across a multi-vertical ad account. The payoff is bidding-data accumulation in the call-conversion-weighted bidding model that runs throughout 2026 and into the AI Max environment in September. That data accumulation is the moat that the wait-until cohort will not have.

Principle two: reweight the call-tracking and attribution stack for ambiguous attribution

The call-asset RSA produces conversions of multiple types from a single impression. Operators running on legacy call-tracking systems built for call-only attribution will systematically misattribute conversion paths.

The reweight requires three changes. First, every call-asset RSA gets a unique tracking number per ad group (or ideally per ad), routed through a dynamic-number-insertion-aware call-tracking platform that pushes call events back to Google Ads as conversions with the correct conversion-action ID. Second, website-click conversions from the same impression get tagged separately, so the operator can see the true call-vs-click split per ad group. Third, the analytics layer reports on call-rate (calls per impression) as a primary KPI rather than as a derived metric – because the call-rate is now the variable that determines whether the publisher’s monetization model works.

Operators who skip this reweight will see their reported CPA stay flat while their real per-billable-call CAC rises, because the click conversions that look fine in the platform are not actually being monetized at the same rate as the call conversions.

Principle three: rebuild the network rate card and the publisher payout stack

Networks and publishers operating on 2025 rate cards into the second half of 2026 will produce mismatched economics. The buyer-side bid posture is changing because call-asset RSAs sit in a different auction; the publisher-side acquisition cost is changing because the conversion-action ambiguity hits per-call CAC; the network-side margin gets squeezed in the middle.

The rebuild has two parts. The buyer-facing rate card should incorporate explicit tiering by call format (legacy call-only versus call-asset RSA versus AI Max for Search), with the legacy tier sunsetting in line with Google’s February 2027 cutoff and the AI Max tier scaling up through 2027. The publisher-facing payout schedule should reflect the per-vertical CAC inflation from the conversion-action ambiguity, with vertical-specific adjustments – auto insurance and home services adjusted up, mass tort and emergency intake adjusted modestly, Medicare adjusted variably depending on AEP cycle. The network’s CPA benchmark management needs to publish updated benchmarks twice a year through the migration period, not annually.

The rebuilt rate card produces lower headline call prices in some segments and higher prices in others. The total network revenue trajectory depends on how well the rebuild matches the underlying auction shifts; networks that rebuild well roughly hold revenue with margin compression, while networks that hold rate cards flat produce churn on both sides.

Implementation Reality: What It Actually Takes to Migrate a Pay-Per-Call Operation

The strategic reframe is straightforward. The implementation is not.

Resource requirements

A mid-sized pay-per-call publisher running call-only campaigns across three to five verticals – say, Medicare, auto insurance, home services, mass tort, and final expense – typically operates three hundred to two thousand call-only ads, distributed across one hundred to four hundred ad groups, in five to twenty-five Google Ads accounts. The migration touches every one of those ads, every ad group’s tracking configuration, every conversion-goal setup, and every Smart Bidding strategy.

The engineering and operations work breaks into four streams. Ad-creative rebuilding requires creative resourcing – copywriters, designers, and a QA pass – proportional to the ad inventory. For three hundred to two thousand ads, plan forty-five to one hundred and twenty days of creative work, parallelized across multiple writers. Tracking-and-attribution rebuild requires call-tracking platform reconfiguration, conversion-action setup in Google Ads, and analytics layer changes; thirty to sixty days of dedicated technical work for a publisher with an established call-tracking stack, sixty to one hundred and twenty days for a publisher migrating tracking platforms in parallel. Bidding-strategy rebuild requires Smart Bidding migration to call-conversion-weighted targets, with two to four weeks of post-migration learning-period turbulence per ad group. Compliance review covers the call-recording laws by state and CMS-specific Medicare marketing rules that affect script and consent disclosures on the new ad units.

Timeline expectations

A realistic implementation timeline for a mid-sized pay-per-call operator:

| Phase | Duration | Key Activities |

|---|---|---|

| Audit and inventory | 14–21 days | Catalog every call-only ad, ad group, account; map current conversion goals; baseline call-rate KPIs |

| Tracking-and-attribution rebuild | 30–60 days | Migrate to call-asset-aware tracking; configure unique numbers per ad group; tag click and call conversions separately |

| Creative rebuild | 45–120 days | Write fifteen-headline and four-description RSAs for every ad group; design call-emphasizing creative variants; QA |

| Bidding-strategy migration | 30–60 days | Set call-conversion values; migrate to tCPA or Max Conv Value targeting; run learning-period validation |

| Compliance review | 14–21 days | Counsel review of new ad copy against state call-recording rules, CMS Medicare marketing rules, TCPA disclosure language |

| Buyer-side rate-card rebuild | 30–45 days | Communicate format-tiered rate card to buyer base; renegotiate where appropriate |

| Total elapsed time | 4–7 months | Conservative for a multi-vertical publisher operating two hundred-plus call-only ads |

Source: Composite based on Google Ads migration documentation and operator-side migration timelines reported in trade-press case studies through April 2026

Common obstacles

Three obstacles consistently slow these implementations beyond the nominal timeline. The first is the learning-period turbulence inside Smart Bidding. When a campaign migrates from a call-only ad to a call-asset RSA with reweighted conversion goals, Smart Bidding’s models reset. The two-to-four-week learning period produces volatile CPAs, volatile call rates, and volatile spend pacing. Operators who are not prepared for the volatility tend to abort the migration midway and revert to legacy ads – losing the bidding-data accumulation that the migration was supposed to capture. The discipline is to commit to the learning period and accept the short-term CPA noise.

The second is buyer renegotiation friction. Pay-per-call buyers – Medicare brokers, insurance agents, law-firm intake managers, home-services operators – typically have standard buyer-network contracts that do not contemplate format-tiered pricing. Renegotiating those contracts to reflect legacy-versus-RSA-versus-AI-Max tiers requires legal work on the network side and approval cycles on the buyer side. Networks that try to push the new rate card without explicit buyer renegotiation produce contract disputes and buyer churn.

The third is the call-quality-versus-call-volume tradeoff. The migration produces a smaller volume of higher-cost calls in many verticals during the transition. Publishers and networks accustomed to volume-based revenue reporting see top-line revenue drop during Q2 and Q3 2026 even when per-call quality and per-call buyer-side close rates are flat or improving. Distinguishing between the volume effect (transitory, recovers as the AI Max model’s bidding accumulates data) and the quality effect (permanent, requires creative or targeting adjustment) takes deliberate analytics work.

The implementation is hard. The operators who finish before February 2027 will run twelve-to-eighteen months of structural advantage against operators who push the work into the final quarter.

Future Implications: A Five-Year Forecast for Live-Transfer Pricing

The April 2026 announcement is the first event in a multi-year sequence. The shape of the sequence is reasonably predictable from the structure of the auction.

In the next twelve months – through April 2027 – call-only ads complete their phase-out. Publishers and networks that migrate aggressively in 2026 build conversion-data and bid-management advantages inside AI Max. Publishers that migrate minimally face elevated CAC and rate-card friction. Live-transfer prices in Medicare, auto insurance, and home services compress modestly against 2025 baselines, with the largest moves in middle-tier inventory and the smallest moves in premium pre-qualified tiers. The Medicare AEP 2025 high-water mark of $80-$150 calls becomes a reference point that 2026 AEP modestly undercuts and 2027 AEP undercuts more meaningfully.

In the next twenty-four months – through April 2028 – AI Max becomes the dominant search-campaign environment, with call-asset RSAs operating fully inside AI Mode placements (which Google reports cover roughly 25.5 percent of AI Mode results and which are growing meaningfully year-over-year as AI Mode usage scales). The cost-per-billable-call distribution widens – call campaigns with strong conversion-data accumulation and well-calibrated call-conversion values capture impression share at lower CPAs than campaigns without that infrastructure. Live-transfer pricing stabilizes at a lower steady-state level than 2025 in volume verticals (Medicare AEP qualified calls in the $65-$120 band, auto insurance in the $30-$70 band, home services in the $20-$95 band), with premium tiers (T65 live transfers, mass tort intake) holding closer to their 2025 levels.

In the next thirty-six to sixty months – through 2030 – the auction equilibrium settles. Pay-per-call’s premium over form-fill narrows from the historical 10-to-30x to a vertical-dependent range closer to 3-to-12x, justified entirely by the lifetime-value differential between call leads and form leads in the buyer’s portfolio rather than by the auction-lane separation that produced the higher historical ratio. The networks that survive are the ones that built call-asset-aware infrastructure and rebuilt rate cards in 2026; the networks that did not consolidate into the survivors. AI Mode placement share grows beyond 25.5 percent of AI Mode results – Google’s broader product trajectory points toward higher monetization rates inside AI surfaces – and call-asset RSAs that have accumulated AI Max conversion data through 2026-2027 capture a disproportionate share of the AI Mode call volume.

The longer-term shift is more interesting. The call-only sunset is a precedent for what happens when Google deprecates a structurally separated ad format and folds it into the AI auction. Other formats – Local Services Ads, Performance Max product feeds, App campaigns – operate today with their own auction lanes. The political and product case for folding more of those into AI Max will be made by reference to the call-only migration. Operators who built infrastructure flexibility in 2026-2027 will be positioned to handle additional format consolidations as they arrive.

For pay-per-call networks and publishers, the strategic implication is to design the operating stack for the world after the next consolidation, not just the world after this one. A monetization architecture that treats Google ad-format separation as a load-bearing assumption is fragile against future consolidations. A monetization architecture that treats AI Max conversion-data accumulation as the durable asset is more resilient.

Key Takeaways

The October 2025 announcement and the February 2026/February 2027 timeline reset the pay-per-call industry’s structural premium in ways that compound across multiple economic vectors. Treating the change as a creative refresh underestimates what is happening.

The call-only sunset removes the auction-lane separation that produced the historical 10-to-30x pay-per-call premium over form-fill, with new call-only ad creation locked out in February 2026 and existing call-only ad impressions ending in February 2027.

Responsive search ads with call assets, the replacement format, sit inside the same Google search auction as form-fill RSAs and inside the same AI Max architecture that Dynamic Search Ads will auto-upgrade into in September 2026.

Three compression vectors hit pay-per-call premiums simultaneously: auction-mix compression as call campaigns compete against form-fill bidders, conversion-action ambiguity as call-asset RSAs produce mixed call-and-click conversion paths, and AI Max bidding-logic uniformity as Smart Bidding optimizes against calibrated conversion values rather than format-specific auction lanes.

The 2025 Medicare AEP price band of $80-$150 per qualified call (with premium T65 live transfers at $150-$225) marks the high-water mark; operator-level forecasts point to 10-to-25 percent compression by 2026 AEP and 20-to-40 percent compression by 2027 AEP, concentrated in the middle tier rather than the live-transfer tier. These are directional estimates; actual outcomes will vary by operator and by AEP cycle.

Auto insurance is most exposed to auction-mix compression because the form-fill auction is structurally rich; home services is most exposed to conversion-action ambiguity because the call-vs-click choice is meaningful at the user level; mass tort and personal injury hold the most durable premium because the call-buyer’s willingness-to-pay tracks case-value economics that the format change does not displace.

Three approaches will underperform: the wait-until-2027 posture cedes AI Max conversion-data accumulation to the migrating cohort; the preserve-call-only-with-workarounds posture captures a fraction of call volume but none of the auction premium; the ride-out-and-hold-rate-card posture produces buyer-side and publisher-side churn that compounds through the migration period.

The migration playbook is a four-to-seven-month operation for a mid-sized pay-per-call publisher, with creative rebuild, tracking-and-attribution rebuild, bidding-strategy migration, compliance review, and buyer-side rate-card renegotiation as the critical-path items.

The five-year forecast points to live-transfer pricing stabilizing at a lower steady-state in volume verticals, premium tiers holding closer to 2025 levels, the call-vs-form premium narrowing from 10-to-30x to 3-to-12x, network consolidation around operators that built call-asset infrastructure in 2026, and AI Mode placement growth as a structural tailwind for operators who accumulated AI Max conversion data through the migration period.

For pay-per-call operators currently running call-only campaigns at scale, the next ninety days are the planning window. The next one hundred and eighty days are the migration window. The operators who arrive at AEP 2026 with rebuilt creative, retooled attribution, and renegotiated rate cards capture the share that the wait-until cohort gives up. The operators who arrive late compete for what is left.

Frequently Asked Questions

What did Google actually announce in October 2025 and April 2026 about call-only ads?

In October 2025, Google’s Ads Developer Blog instructed advertisers to begin migrating call-only ads to responsive search ads with call assets through the Google Ads API and laid out the phase-out timeline. The Google Ads Help center and the trade press confirmed the operational dates: in February 2026, all options to create new call-only ads through any surface (UI, Editor, API) were removed, and in February 2027, all existing call-only ads will stop receiving impressions. In April 2026, Google announced a separate-but-related change: Dynamic Search Ads campaigns, automatically created assets, and campaign-level broad match settings will auto-upgrade to AI Max for Search in September 2026, with new DSA creation disabled at the same point. Together, the two announcements close most of Google’s automated and call-format ad surfaces inside the AI Max architecture by the end of 2026.

Why does the convergence with AI Max matter more than the call-only sunset itself?

The call-only sunset is the format event. The AI Max convergence is the auction event. Call-only ads competed in their own narrower auction, populated overwhelmingly by other call-only ads from operators in the same vertical. That auction-lane separation is what produced the structural pay-per-call premium over form-fill leads. Once call campaigns migrate to responsive search ads with call assets, they compete in the full search auction against every other RSA serving the same keywords – including form-fill campaigns from carriers, comparison-shopping marketplaces, and direct-to-consumer brands with much higher impression-level bids. AI Max for Search, which DSA campaigns auto-upgrade into in September 2026, applies a uniform automated-bidding logic across both call-conversion and form-conversion campaigns. The combined effect is that the auction-mechanical separation that produced the pay-per-call premium does not survive the migration.

What is the migration path Google provides, and is it sufficient?

Google’s migration path moves call-only ads to responsive search ads with call assets through bulk-migration tooling exposed in Google Ads Help and the Google Ads API. The minimum migration copies a call-only ad’s headline, description, and phone number into a new RSA-with-call-asset combination. The minimum migration is sufficient to keep ads serving past February 2027, but it does not capture the full conversion-data accumulation that an aggressive rebuild produces. The aggressive migration treats the new format as a structural rebuild – fifteen headline slots written for call-first intent, four call-emphasizing descriptions, supporting extensions, conversion goals weighted toward tap-to-call events, and Smart Bidding strategies calibrated against call-conversion values. The minimum migration preserves serving; the aggressive migration captures the bidding-data advantage that operators who finish in 2026 will run against operators who delay.

How big was the historical pay-per-call premium over form-fill leads, and why did it exist?

The historical pay-per-call premium ranged from roughly 2x at the cheapest call tiers to 30x in the most expensive verticals. In Medicare Advantage AEP, qualified calls priced at $80 to $150 (with live transfers at $150 to $225) versus form leads at $20 to $80. In auto insurance, calls at $25 to $80 versus form leads at $5 to $25. In mass tort, calls at $200 to $500-plus versus form leads at $40 to $200. The premium reflected three structural conditions: a separated auction lane in which call-only ads competed primarily against other call-only ads (so the marginal bidder was a call-buyer rather than a form-buyer), unambiguous call-only conversion mechanics (so the publisher’s call-rate was deterministic rather than a function of user choice), and call-format-specific Smart Bidding optimization (so the bidding logic was calibrated against call-conversion goals without competing form-conversion data in the same auction). The call-only sunset and AI Max convergence remove all three conditions.

Which verticals are most exposed to compression, and which are most durable?

Auto insurance is most exposed to auction-mix compression because the form-fill auction is structurally rich – carrier brand campaigns and comparison-shopping marketplaces bid heavily on the same keywords as call-buying agents. Home services is most exposed to conversion-action ambiguity because homeowners researching HVAC or roofing make a real choice between calling and submitting a quote form when a call-asset RSA presents both paths. Medicare is exposed in the middle of the band – qualified-call pricing compresses meaningfully, but premium T65 live transfers hold up because the pre-qualification infrastructure is durable. Mass tort and personal injury are most durable because case-value economics drive law-firm willingness-to-pay independently of the ad format, and the call-buyer’s bid floor is set by attorney-fee economics rather than by the form-fill auction.

What is the realistic timeline for a pay-per-call publisher to complete the migration?

A mid-sized pay-per-call publisher running call-only campaigns across three to five verticals – typically three hundred to two thousand call-only ads across five to twenty-five Google Ads accounts – should plan four to seven months end-to-end. The phases run in parallel: a two-to-three-week audit and inventory, a thirty-to-sixty-day tracking-and-attribution rebuild, a forty-five-to-one-hundred-twenty-day creative rebuild, a thirty-to-sixty-day bidding-strategy migration with Smart Bidding learning periods, a two-to-three-week compliance review, and a thirty-to-forty-five-day buyer-side rate-card renegotiation. Publishers who start the migration in Q2 2026 finish before AEP 2026; publishers who start in Q3 finish before the February 2027 cutoff but miss the AEP 2026 conversion-data cycle; publishers who start in Q4 2026 or later are migrating under deadline pressure with elevated CAC and reduced bidding-data accumulation.

How do call-asset RSAs change the call-tracking and attribution stack?

Call-asset RSAs produce conversions of multiple types from a single impression – a tap-to-call, a click-through-to-landing-page, sometimes a sitelink interaction. Operators running on legacy call-tracking systems built for call-only attribution will misattribute conversion paths. The reweight requires unique tracking numbers per ad group (or ideally per ad), routed through a dynamic-number-insertion-aware call-tracking platform that pushes call events back to Google Ads with the correct conversion-action ID. Website-click conversions from the same impression should be tagged separately, so the operator can see the true call-vs-click split per ad group. The analytics layer should report on call-rate (calls per impression) as a primary KPI, because the call-rate is now the variable that determines whether the publisher’s monetization model holds.

Will network rate cards drop, and how should buyers think about budget planning for 2026-2027?

Network rate cards will diverge by format tier rather than dropping uniformly. Legacy call-only inventory continues to price at 2025 levels through its serving period (ending February 2027) but volume is shrinking. Call-asset RSA inventory will price at variable levels by vertical, with auto insurance and broader health insurance facing higher buyer-side acquisition costs (network rate cards rise to reflect publisher CAC) and Medicare AEP and home services facing modest compression (network rate cards drop in the middle of the band). AI Max for Search inventory – fully consolidated by late 2026 – operates on calibrated-conversion-value pricing that varies more by operator’s bidding sophistication than by static rate-card position. Buyers planning 2026-2027 budgets should expect volatility through the migration period, plan to renegotiate buyer-network contracts to incorporate format tiers, and weight their budgets toward operators that publish migration progress reports rather than operators that hold rate cards opaque.

What about Local Services Ads as an alternative for call-driven advertisers?

Local Services Ads operate in a separate auction with separate qualification mechanics and are not a direct substitute for call-only ads. LSAs require business verification (license, insurance, background checks for some categories) and price on a per-lead model with Google as the intermediary. For some local-business call advertisers – plumbers, electricians, locksmiths in eligible categories – LSAs remain a viable supplement to call-asset RSAs, but they are not a substitute for the broader pay-per-call publisher network model. Pay-per-call publishers cannot redirect call-only campaign volume to LSAs because LSAs require the buyer’s own verified business and do not accept third-party publisher traffic. The practical implication: LSAs are a tool for direct local advertisers, not a workaround for the call-only sunset’s impact on the publisher-network model.

How does AI Mode placement affect call-asset RSA economics specifically?

AI Mode placements – sponsored slots within Google’s AI Mode answer surface – currently appear in approximately 25.5 percent of AI Mode results and are eligible for two campaign types: Performance Max and AI Max for Search. Standard search campaigns, including most call-asset RSA campaigns running outside AI Max, do not currently qualify. As call campaigns migrate to AI Max for Search through 2026-2027, their AI Mode placement eligibility expands. Google has reported a 7 percent average conversion-or-conversion-value lift when advertisers use the full AI Max feature suite (search-term matching, text customization, final-URL expansion) versus search-term matching alone. For pay-per-call operators, the AI Mode placement and AI Max feature uplift represent the offsetting tailwind to the auction-mix compression – operators who execute the AI Max migration well capture both AI Mode placement share and the conversion-rate uplift, partly offsetting the premium compression hitting the legacy call-only auction lane.

What compliance considerations come with the migration?

The migration touches three compliance surfaces. First, call-recording disclosure rules vary by state, and the script disclosures attached to incoming calls from RSA-call-asset campaigns may need re-verification against the operator’s existing recording-disclosure language. Second, CMS Medicare marketing rules impose specific requirements on the call-flow and disclosure scripts used in Medicare Advantage and Medicare Part D marketing – the migration to a different ad format does not change the CMS rules but may require re-validation of the call-script integration with the new ad units. Third, TCPA consent and one-to-one consent rules continue to govern the publisher-network-buyer liability stack regardless of ad format; the migration is an opportunity to re-document consent-capture flows in the publisher’s stack, not a moment when those flows can be relaxed. A two-to-three-week external counsel review during the migration window is the standard ask.

How does the five-year forecast on live-transfer pricing translate into operator decisions today?

The forecast points to a structural narrowing of the pay-per-call premium from 10-to-30x to 3-to-12x by 2030, with most of the compression hitting middle-tier inventory in volume verticals and the smallest moves hitting premium tiers in case-value-driven verticals. For operators today, the implication is that capacity built around pre-qualification, live-transfer infrastructure, and call-quality differentiation retains value across the forecast horizon, while capacity built around volume-only call-format arbitrage compresses with the auction. Investments in call-tracking sophistication, AI Max bidding-data accumulation, and format-tiered rate cards pay back across the forecast period; investments in scaling more call-only ads in 2026 or in workaround formats (LSAs, click-to-call sitelinks, third-party landing-page CTAs) do not. The decision today is whether to allocate Q2-Q3 2026 engineering and creative budget toward the migration or to defer that allocation; the cohort that allocates captures the AI Max bidding-data moat the cohort that defers will not have.

Sources

Tier 1: Primary Google Sources

-

Google Ads Developer Blog, “Upgrade your Call-Only Ads to Responsive Search Ads with Call Assets in the Google Ads API,” October 2025 – https://ads-developers.googleblog.com/2025/10/upgrade-your-call-only-ads-to.html

-

Google Ads Help, “Action Required: Transition from call ads to call assets,” accessed April 2026 – https://support.google.com/google-ads/answer/16598240?hl=en

-

Google Ads Help, “How to transition from call ads to call assets,” accessed April 2026 – https://support.google.com/google-ads/answer/16619010?hl=en

-

Google Ads Help, “How AI Max for Search campaigns works,” accessed April 2026 – https://support.google.com/google-ads/answer/15910187?hl=en

-

Google Blog (Ads & Commerce), “Dynamic Search Ads are upgrading to AI Max,” April 2026 – https://blog.google/products/ads-commerce/dsa-upgrade-to-ai-max-2026/

-

Google for Business Announcements, “Dynamic Search Ads are upgrading to AI Max,” April 2026 – https://business.google.com/us/accelerate/announcements/dsa-upgrade-to-ai-max-2026/

-

Google Ads Help, “About call assets,” accessed April 2026 – https://support.google.com/google-ads/answer/2453991?hl=en

-

Google Ads Help, “Measure calls from ads,” accessed April 2026 – https://support.google.com/google-ads/answer/6095882?hl=en

-

Google Ads Help, “About phone call conversion tracking,” accessed April 2026 – https://support.google.com/google-ads/answer/6100664?hl=en

Tier 2: Established Trade Press

-

Search Engine Land, “Google to phase out Call-Only Ads by 2027,” 2026 – https://searchengineland.com/google-to-phase-out-call-only-ads-by-2027-462983

-

Search Engine Land, “Google to retire Dynamic Search Ads in favor of AI Max,” April 2026 – https://searchengineland.com/google-retire-dynamic-search-ads-ai-max-474262

-

Search Engine Roundtable, “Google Sunset Call Ads Dates Revealed,” 2026 – https://www.seroundtable.com/google-sunset-call-ads-dates-40221.html

-

Search Engine Roundtable, “Google Ads To Retire Dynamic Search Ads For AI Max,” April 2026 – https://www.seroundtable.com/google-ads-dsa-ai-max-41170.html

-

Search Engine Journal, “Google Is Replacing Dynamic Search Ads With AI Max,” April 2026 – https://www.searchenginejournal.com/google-is-replacing-dynamic-search-ads-with-ai-max/571949/

-

PPC Land, “Google ends call ads in February 2026, shifts advertisers to RSA format,” 2026 – https://ppc.land/google-ends-call-ads-in-february-2026-shifts-advertisers-to-rsa-format/

-

PPC Land, “Google phases out call-only ads by February 2027 in push toward automation,” 2026 – https://ppc.land/google-phases-out-call-only-ads-by-february-2027-in-push-toward-automation/

-

PPC Land, “Google ends Dynamic Search Ads: DSA upgrades to AI Max in September,” April 2026 – https://ppc.land/google-ends-dynamic-search-ads-dsa-upgrades-to-ai-max-in-september/

-

Adweek, “Google is Migrating Dynamic Search Ads to AI Max,” April 2026 – https://www.adweek.com/media/google-is-migrating-dynamic-search-ads-to-ai-max/

-

MediaPost, “Google Replacing Dynamic Search Ads With ‘AI Max,’” April 15, 2026 – https://www.mediapost.com/publications/article/414317/google-replacing-dynamic-search-ads-with-ai-max.html

Tier 3: Industry and Vendor Commentary

-

Searchen Networks, “Google Sets Deadline to Retire Call-Only Ads, Urges Shift to Responsive Search Ads With Call Assets,” January 11, 2026 – https://www.searchen.com/2026/01/11/google-sets-deadline-to-retire-call-only-ads-urges-shift-to-responsive-search-ads-with-call-assets/

-

Symphonic Digital, “Google Ads Updates in 2026: Call-Only Ads End & AI Expansion,” 2026 – https://www.symphonicdigital.com/blog/google-ads-playbook-for-2026

-

YPC Media, “Google Is Phasing Out Call-Only Ads: What’s Changing, When, and How to Prepare,” October 13, 2025 – https://www.ypcmedia.com/2025/10/13/google-is-phasing-out-call-only-ads-whats-changing-when-and-how-to-prepare/

-

Neil Patel Blog, “Google Is Sunsetting Call-Only Ads: How to Update Your Strategy,” 2026 – https://neilpatel.com/blog/call-only-ads/

-

Digital Applied, “Google AI Mode: 75M Users, Ads in 25% of AI Results,” 2026 – https://www.digitalapplied.com/blog/google-ai-mode-75m-users-ads-in-ai-results-2026

-

Digital Applied, “Google AI Mode Advertising: Placement and Bidding,” 2026 – https://www.digitalapplied.com/blog/google-ai-mode-advertising-placement-bidding-guide

-

Astoria Company, “The Real Cost of Medicare Insurance Leads and Calls,” 2026 – https://astoriacompany.com/the-real-cost-of-medicare-insurance-leads-and-calls/

-

Astoria Company, “Maximizing Medicare Insurance Leads and Live Calls During AEP,” 2025-2026 – https://astoriacompany.com/maximizing-medicare-insurance-leads-and-live-calls-during-aep/

Tier 4: Supporting Vertical and Pricing References

-

AllCalls, “Is Pay-Per-Call Insurance Lead Generation Worth It? 2026,” 2026 – https://allcalls.io/blog/is-pay-per-call-insurance-lead-generation-worth-it-2026-cost-benefits-and-verdic-2/

-

AllCalls, “Best Medicare Lead Platforms for Inbound Calls: 5 Top Picks 2026,” 2026 – https://allcalls.io/blog/best-lead-generation-platforms-for-medicare-advantage-5-top-picks-2026/

-

LeadingResponse, “The Hottest Legal Leads for 2026 | PI, WC, SSD & Mass Tort,” 2026 – https://leadingresponse.com/blog/legal/the-hottest-mass-tort-leads/

-

LanderLab, “Is Pay-Per-Call Lead Generation Still Worth It in 2026?,” 2026 – https://landerlab.io/blog/is-pay-per-call-worth-it

-

MagnifyLab, “Google Ads Is Sunsetting Call-Only Ads: What This Means for Advertisers,” 2026 – https://www.magnifylab.com/blog/google-ads-is-sunsetting-call-only-ads-what-this-means-for-advertisers/

Closing

The October 2025 announcement and the February 2026/February 2027 timeline will be remembered, in trade-press summaries, as a routine ad-format deprecation. That framing misses what is actually happening. The structural event is the consolidation of call campaigns into the same AI Max auction architecture as form-fill, and the dismantling of the auction-lane separation that produced the historical 10-to-30x pay-per-call premium. The operators who treat this as a creative refresh will run 2026 and 2027 on a P&L that the auction will not support, and will spend 2028 explaining to investors why their network revenue compressed against forecasts. The operators who treat it as a structural migration – aggressive creative rebuild, retooled call-tracking and attribution, calibrated Smart Bidding against true call-conversion values, format-tiered buyer rate cards, and engineered AI Max conversion-data accumulation – will run twelve-to-eighteen months of bidding-data advantage against everyone else and will set the rate card for the post-migration market. The decision about which group to be in is being made now, in the next ninety days of audit and planning and the next one hundred and eighty days of build and renegotiation. There is no comfortable third option. The auction does not wait.

Channel data, ad-format timelines, and AI Max product details reflect publicly reported conditions through April 28, 2026. Google Ads product behavior, Smart Bidding mechanics, and AI Mode placement coverage change continuously; verify current product behavior through Google’s developer blog and Google Ads Help before making operational decisions. Pay-per-call pricing benchmarks and live-transfer ranges reflect publicly reported network and operator disclosures; actual rate cards vary by buyer relationship and inventory tier. This article provides general industry analysis and does not constitute legal, financial, or compliance advice. Consult qualified counsel for specific compliance questions related to TCPA consent, CMS Medicare marketing rules, and state-by-state call-recording disclosure requirements.