March 4, 2026 is the date the mortgage industry rebuilds its top of funnel. The Homebuyers Privacy Protection Act flips a switch on a $200 million prescreen revenue line, and the lenders without a servicing book or a soft-pull stack will feel it first.

A Federal Off-Switch for Mortgage Trigger Leads

On September 5, 2025, the Homebuyers Privacy Protection Act became Public Law 119-XX after President Trump signed H.R. 2808. The bill cleared the House on a voice vote and passed the Senate by unanimous consent, an outcome the National Association of Mortgage Brokers’ president called the rarest kind of bipartisanship. The statute amends section 604(c) of the Fair Credit Reporting Act, codified at 15 U.S.C. §1681b(c), and takes effect March 4, 2026, exactly 180 days after enactment. Equifax, Experian, and TransUnion negotiated the longer-than-typical implementation window because filtering trigger leads at the prescreen layer requires meaningful changes to inventory and delivery systems.

The mortgage trigger lead has been a fixture of the lead-generation supply chain since the late 1990s. The mechanism is simple: a consumer applies for a mortgage, the originating lender pulls a hard credit inquiry, and within 24 hours the credit bureaus sell prescreened reports on that consumer to competing lenders who have filed a standing prescreen criteria file. Industry estimates place trigger-lead revenue across the three bureaus at roughly $200 to $300 million per year. From the consumer’s perspective, the experience has been roughly 15 unsolicited calls and texts within 48 hours of starting a mortgage application, a pattern the Mortgage Bankers Association and the National Association of Realtors documented in support of the legislation. From the lead-buyer’s perspective, the trigger feed was the cheapest high-intent mortgage signal available, and most independent brokers’ acquisition models depended on it.

The HPPA does not abolish prescreening on residential mortgage inquiries outright. It carves four exceptions that determine which lenders survive on trigger data and which lose access entirely. The carve-outs reshape the competitive map more than the headline ban does, and they are the reason the mortgage market is consolidating around originator-servicer combinations rather than independent broker volume.

What HPPA Actually Says

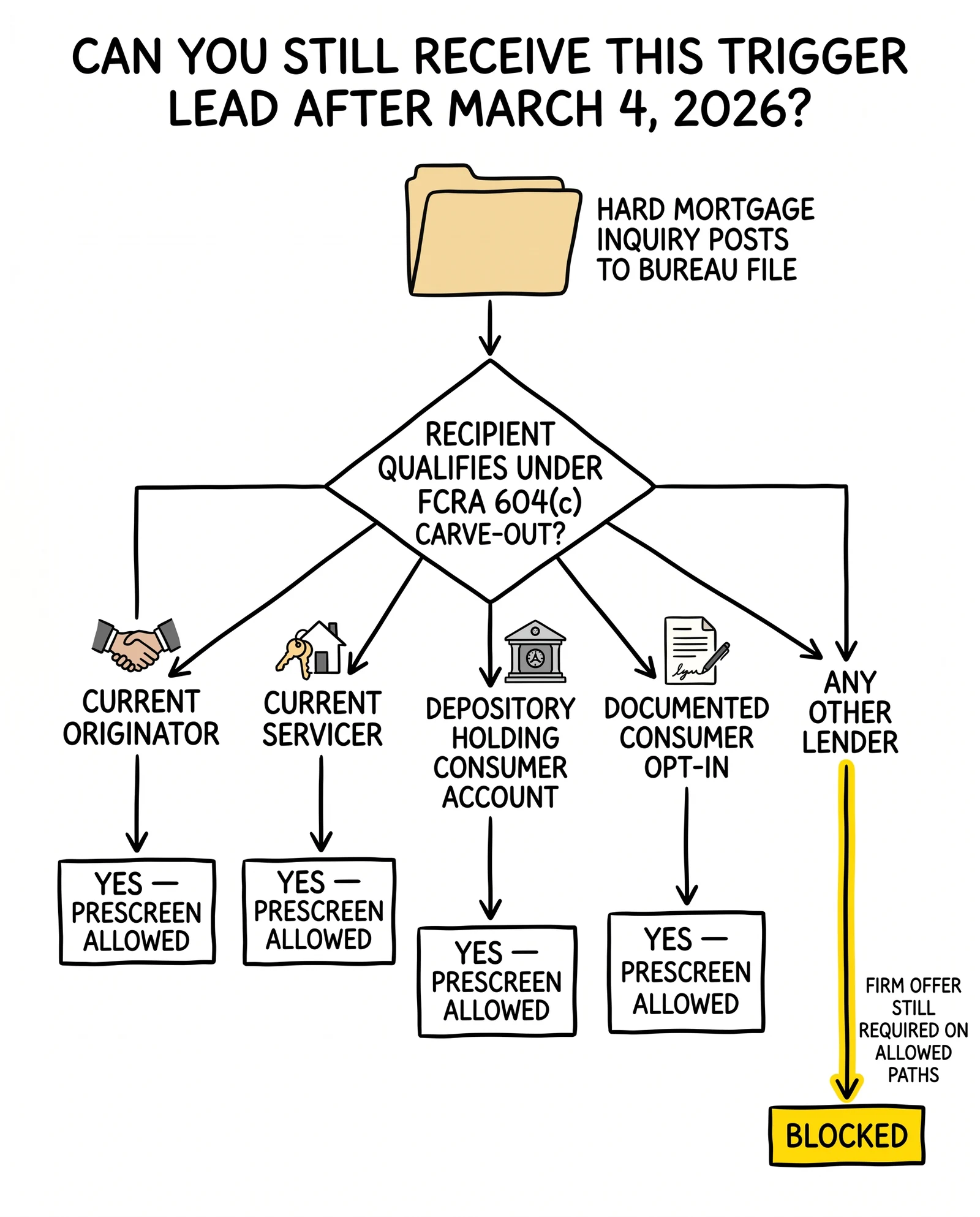

The new paragraph inserted into FCRA §604(c) prohibits a consumer reporting agency from furnishing a consumer report in connection with any credit transaction not initiated by the consumer when that transaction involves a residential mortgage loan, unless one of four conditions applies. The conditions, in plain English: the recipient is the originator of the consumer’s current residential mortgage; the recipient is the current servicer of the consumer’s residential mortgage; the recipient is an insured depository institution or insured credit union that holds a current account for the consumer, with “current account” defined to include deposit accounts, share accounts, and existing loans; or the consumer has provided documented authorization to receive the report. A firm offer of credit must still accompany any permitted prescreen, the existing FCRA requirement.

The statutory definition of “residential mortgage loan” tracks the Truth in Lending Act, capturing closed-end credit secured by a one-to-four-unit principal dwelling, including refinances and home-equity lines. The carve-outs cover the relationship the consumer already has, not future relationships the lender hopes to form. A bank can prescreen its own depositors. A servicer can prescreen its own borrowers. An originator can prescreen its own existing customers when those customers shop a competitor. A bank cannot prescreen a non-customer who happens to live in its branch footprint.

The opt-in carve-out is narrow in practice. Documented consumer authorization to be the subject of a prescreened mortgage solicitation is uncommon outside of co-marketing arrangements with real-estate agents, and the FCRA’s documentation standards plus the FCC’s reinstated prior-express-written-consent regime make any blanket consent capture difficult to sustain. Most lenders will treat the opt-in path as a marginal supplement to the relationship-based carve-outs, not a replacement.

The Industry Coalition Behind the Bill

The legislative coalition that pushed HPPA through Congress was wider than typical mortgage-policy fights. The Mortgage Bankers Association led a 23-organization letter campaign that included the National Association of Mortgage Brokers, the National Association of Realtors, the Community Home Lenders of America, the American Bankers Association, the Independent Community Bankers of America, the National Association of Federally-Insured Credit Unions, and consumer-side organizations including the National Consumer Law Center. The Broker Action Coalition, representing independent originators, ran a parallel campaign focused on member education. Trade press described the seven-year arc from the first congressional draft in 2018 to the September 2025 signing as the longest negotiation since the Dodd-Frank rule writing.

The political calculus was unusual. Trade groups historically split on lead-supply rules along the same lines as they split on QM, broker compensation, and net-tangible-benefit standards: depositories favor restrictions, independents oppose them. HPPA broke that pattern because the carve-out structure favors depositories and integrated originator-servicers without forcing brokers off prescreen entirely. Brokers retained access to their own prior originations and to anyone who explicitly opted in, while large nonbank originators with growing servicing books gained the most. The final vote was a textbook case of an industry’s largest players supporting a rule that disadvantages their smaller competitors more than it disadvantages them.

The Prescreen Rules, Pre- and Post-HPPA

The clearest way to read HPPA is against the rules it replaces. The table below maps the old prescreen environment under FCRA §604(c) to the new one taking effect March 4, 2026.

| Dimension | Pre-HPPA (through March 3, 2026) | Post-HPPA (from March 4, 2026) |

|---|---|---|

| Statutory basis | FCRA §604(c)(1)(B), firm offer of credit | FCRA §604(c) as amended by H.R. 2808 |

| Trigger event | Hard mortgage inquiry on consumer file | Hard mortgage inquiry on consumer file |

| Prescreen recipient | Any lender with prescreen criteria file | Current originator, current servicer, depository with consumer account, or opt-in only |

| Firm offer required | Yes | Yes |

| Consumer notice | Generic FCRA prescreen disclosure | Same disclosure plus statutory restriction |

| Bureau revenue line | Estimated $200-300M annually | Estimated 60-80% reduction |

| Independent broker access | Open via list purchase | Closed unless prior origination relationship or opt-in |

| Servicer access to own book | Permitted | Permitted, now competitively material |

| State law overlay | Several state mini-trigger laws active | State laws survive where they go further |

The carve-out structure is the consequential part. Under the prior regime, a regional independent broker could buy the same trigger feed as the largest depository in the country. Under HPPA, the regional independent loses prescreen access entirely except for consumers it previously originated for, while the depository retains access to its full deposit base and the servicer-of-record retains access to anything in its servicing book. The competitive asymmetry is structural and intended.

The Supply Shock in Cost Per Lead

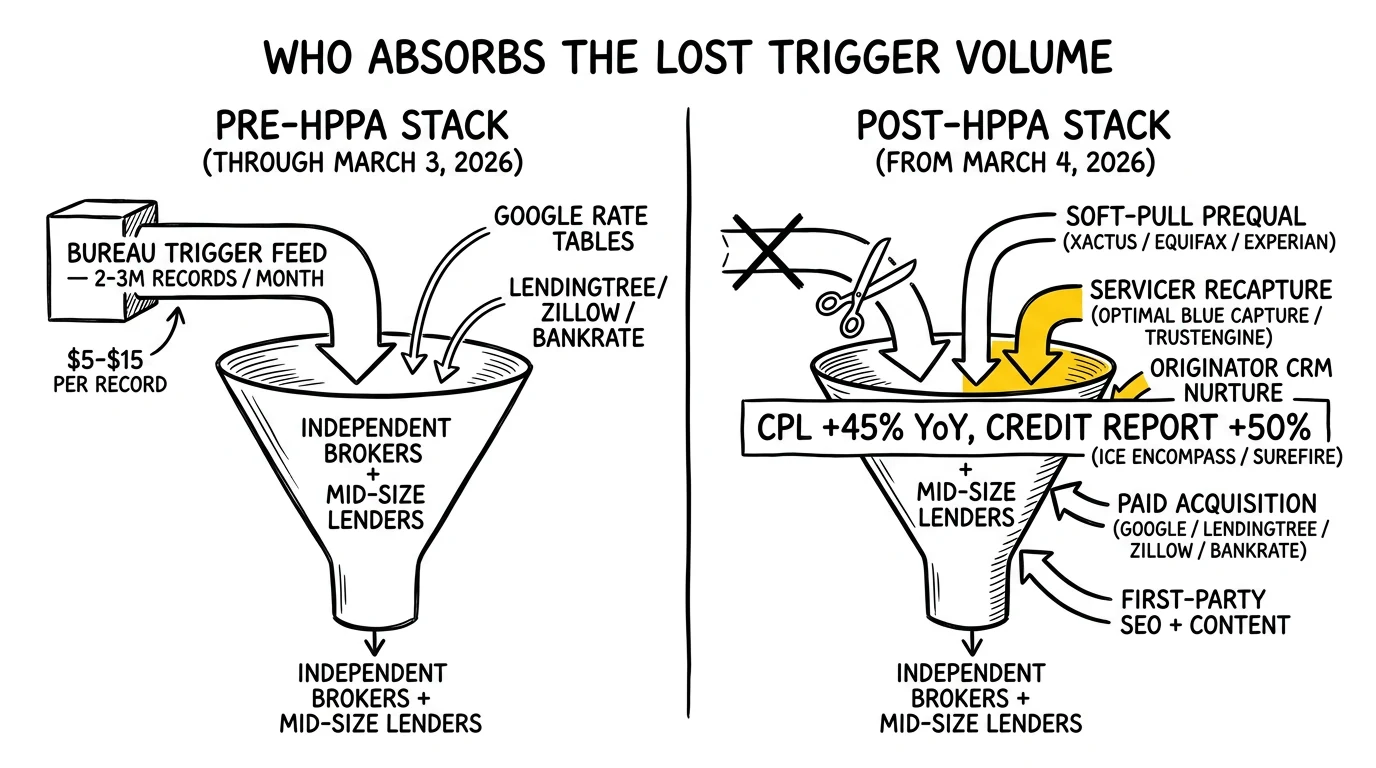

HPPA collapsed the cheapest segment of the mortgage lead supply curve. The independent purchase-lead aggregators, telemarketing rooms, and direct-mail vendors that built businesses around buying bureau trigger feeds at $5 to $15 per record and reselling worked leads at $80 to $250 lost their input on March 4, 2026. Demand from lenders did not contract proportionally. The result is the price chart that 2026 mortgage operators are now staring at.

HousingWire reported in early 2026 that internet purchase-lead pricing on the major aggregator platforms is up roughly 45% year over year. The pricing bands inside that average vary materially by exclusivity and intent quality. Exclusive purchase leads from rate-table placements run $150 to $250. Shared non-exclusive purchase leads run $80 to $130. Refinance leads, traditionally cheaper, have compressed less because refinance demand collapsed independently when 30-year rates stayed above 6.5% through most of 2024 and 2025. The pattern from prior credit-cycle disruptions, covered in mortgage lead pricing rate-cycle dynamics and mortgage lead CPL trends, suggests CPLs will plateau roughly 20 to 30% above the post-HPPA spike once supply substitutes are fully operational, but not return to pre-2026 levels.

The credit-report cost stack moved in parallel. Experian announced a separate mortgage-grade pricing increase in early 2026 layered on top of bureau base increases that had already taken effect in 2024 and 2025. Combined with FICO’s own re-pricing, total per-loan credit-report costs for mortgage lenders are rising as much as 50% in 2026, reaching $80 to $100 per fully-pulled tri-merge file in some bands. The cost structure of any lender that runs hard inquiries early in the funnel just got materially worse, which is one of the larger forcing functions behind the soft-pull migration covered below.

The volume effect is material. Industry estimates place 2024 trigger-lead inventory across the three bureaus at roughly 2 to 3 million prescreened reports per month during peak homebuying season. Even allowing 50% of that volume to flow under the carve-outs to existing originators and servicers, the post-HPPA inventory available to outside competitors falls by something like 1 to 1.5 million records monthly. That volume must either be replaced by other intent signals or pulled out of the funnel entirely. Most operators are choosing some combination of replacement and contraction.

The Replacement Vendor Map

Lenders rebuilding their pipelines after HPPA are settling around five categories of substitute. The table below maps the dominant vendors and what each substitute actually replaces.

| Substitute Category | What It Replaces | Representative Vendors | Practical Notes |

|---|---|---|---|

| Soft-pull prequalification | Initial credit screen without firing prescreen triggers | Xactus Pre-App X, Equifax Mortgage Prequalification, Experian Prequalification | Soft inquiry, no consumer score impact, no trigger generated |

| Servicer recapture | Refinance and home-equity outreach to existing book | Optimal Blue Capture, TrustEngine, Total Expert | Operates only on owned servicing data; ineffective for new acquisition |

| Originator CRM nurture | Long-cycle conversion from prior applicants | ICE Encompass, Surefire CRM, Velocify | Existing relationship satisfies HPPA carve-out for re-originations |

| Paid acquisition | Volume replacement at higher CPL | Google rate tables, LendingTree, Zillow, Bankrate | Roughly 45% YoY price increase; bidding-based, harder unit economics |

| First-party content and SEO | Owned demand at controlled CPL | Site SEO, mortgage calculators, rate alerts | 6-12 month build cycle; durable but slow |

The soft-pull layer is the most important operational shift. Xactus’s Pre-App X and Pre-Qualification X products, Equifax’s Mortgage Prequalification report, and Experian’s prequalification feed all generate a credit assessment without triggering the FCRA hard-inquiry event that previously fed the bureaus’ prescreen pipeline. Lenders integrating soft-pull early in the funnel get the credit-quality signal they need to price and triage without exposing the consumer to the trigger-lead solicitation cycle, even though that cycle is now legally constrained. The technique has been available for years; HPPA economics finally make it the default for serious operators.

The servicer-recapture stack is the most consequential strategically. Optimal Blue launched Capture for Originators on June 9, 2025, three months before HPPA was signed, with timing that suggests the company read the regulatory wind. The product runs portfolio-wide eligibility analysis monthly and surfaces recapture candidates with break-even calculations, closing-cost estimates, and prefilled outreach. TrustEngine, the merged entity formed when Sales Boomerang combined with Mortgage Coach, sits in adjacent territory with borrower-intelligence triggers around rate movement, equity gain, and life events. Total Expert handles the marketing-automation layer for many of the same use cases. None of these tools acquire new customers; they monetize relationships the lender already has. That is exactly what HPPA’s carve-out structure rewards.

The paid-acquisition layer fills the residual demand. Google’s rate-table placements, LendingTree’s auction-based marketplace, Zillow’s mortgage marketplace, and Bankrate’s rate aggregation absorb the budget that was flowing into trigger leads, at substantially higher CPLs. The economics for marketplaces shift in ways the LendingTree-Zillow mortgage marketplaces analysis has tracked through prior cycles: when third-party intent signals contract, marketplace pricing rises faster than fundamental demand because lenders perceive marketplaces as the path of least resistance.

Servicer Recapture Becomes the New Battlefield

The largest mortgage transaction in the period framing HPPA was Rocket Companies’ $14.2 billion acquisition of Mr. Cooper Group, which closed October 1, 2025, four weeks after HPPA’s signing. The combined entity services approximately 10 million homeowners, roughly one in six U.S. mortgages, with a combined servicing book near $2.1 trillion. Rocket Mortgage’s standalone recapture rate is 83%, approximately three times the industry average of 27 to 28%. Applying that recapture engine to Mr. Cooper’s serviced book is the strategic premise of the deal.

The HPPA timing is not coincidental. Rocket announced the acquisition in March 2025 at a $9.4 billion valuation and closed it at $14.2 billion in October, a 51% increase that reflects market reassessment after HPPA’s September signing. The carve-out structure of the bill hands Rocket a decisive structural advantage: every Rocket-originated and Rocket-serviced consumer is, by statute, a permitted trigger-lead recipient class for Rocket itself, while outside competitors are blocked from prescreening that population. The combined company can run inbound marketing, outbound recapture, and rate-shop interception against its own book without competing for the same lead in an open market.

The implications for everyone else are sharp. United Wholesale Mortgage’s recapture rate is roughly 29%, close to the industry average. Most independent brokers and small banks operate below 25%. The competitive gap between Rocket and the next tier was already large before HPPA. Post-HPPA, the gap widens because the most efficient new-acquisition channel for the average lender has been removed, while the most efficient retention channel for Rocket has been protected. Industry analysts at Mortgage Professional America described the post-HPPA structure as the largest single-event consolidation pressure since the 2008 cycle.

The servicer-recapture playbook is unevenly distributed. Lenders with substantial servicing books, even small ones, can deploy Optimal Blue Capture or TrustEngine and run the same retention motion at a fraction of Rocket’s scale. Lenders that sold servicing rights aggressively to free up capital for origination volume, a common strategy in the 2020-2022 boom, now sit on the wrong side of HPPA without an obvious replacement. Several mid-size independents have reportedly begun buying back servicing rights at premium prices, an inversion of the prior decade’s strategy.

How HPPA Stacks With TCPA

HPPA controls who may receive a prescreened mortgage report. TCPA controls how anyone may contact the consumer once contact data is in hand. The two statutes are serial gates, not redundant ones, and the post-HPPA workflow has to satisfy both.

The TCPA stack moved separately in 2025 in ways that complicate the post-HPPA outreach environment. The Eleventh Circuit’s January 2025 decision in IMC v. FCC vacated the FCC’s 2023 one-to-one consent rule, which had been set to take effect that month. The FCC formally reinstated the prior prior-express-written-consent regime on August 29, 2025. The same agency had also adopted a “revoke-all” rule in 2024 that would treat any TCPA revocation as applying across all subjects from a given caller; that rule’s effective date has been pushed twice and now sits at January 31, 2027. The net effect is that 2026 outbound mortgage marketing operates under the older, less stringent PEWC standard, with the heavier revocation regime delayed.

A lender exercising one of HPPA’s carve-outs to receive a trigger lead still needs PEWC to autodial or text that consumer, must scrub against state and federal Do Not Call lists, must observe state mini-TCPA statutes including Florida’s FTSA and Oklahoma’s OTSA, and must honor any prior recorded revocation. Compliance teams that integrate HPPA filtering at the data-acquisition layer and TCPA filtering at the outbound layer will land in roughly the right place. The deeper structural treatment of PEWC after the FCC’s 2025 reinstatement is in the consent and PEWC guide, and the revocation-rule trajectory through 2026 is the focus of the FCC enforcement and TCPA penalties coverage. Teams that skip either gate will trip enforcement risk that is materially higher than pre-HPPA, because every trigger lead now flows through narrower channels and is easier to trace to source.

State-level overlay matters. Several states had passed restrictions on mortgage trigger leads before HPPA, and the federal statute preempts only where a direct conflict exists. State requirements that go further than HPPA, including enhanced disclosure or stricter timing rules, continue to apply. The Conference of State Bank Supervisors and individual state AGs retain authority over deceptive practices that survive HPPA, and the state mini-TCPA laws including FTSA and OTSA overlay an outbound-contact regime independent of how the lead was sourced. Multi-state lenders need a state matrix; single-state lenders need to read their own state law against HPPA’s federal floor.

What Brokers and Mid-Size Lenders Should Do

The independent broker channel and the mid-size non-depository lender channel face the steepest adjustment. Both segments overweight third-party trigger leads in their acquisition mix, neither has a deposit base to anchor the depository carve-out, and most do not own large enough servicing books to run the recapture motion at Rocket-comparable economics. The practical sequence for these operators, ordered by what should happen first:

Cut trigger spend ahead of the March 4, 2026 effective date and redirect the budget into Google rate tables, LendingTree, Zillow, Bankrate, and local SEO. The cost-per-acquisition shock is going to land regardless; running the substitute channels for 60 to 90 days before the effective date lets operators calibrate creative, bid strategy, and conversion paths before the supply curve breaks. Operators that wait until March 4 to learn how Google rate tables behave will be paying both the price spike and a learning-curve premium.

Stand up a soft-pull prequalification flow with Xactus Pre-App X, Equifax Mortgage Prequalification, or Experian Prequalification. The soft-pull layer becomes the primary credit-quality screen at the top of funnel, and integrating it before HPPA’s effective date avoids the experience of running unscreened leads through expensive hard-pull credit reports during the post-HPPA price spike. The mortgage lead generation credit-score strategies framework remains relevant for tier definitions, but the inquiry mechanics shift from hard-pull to soft-pull at the top of the funnel.

Deploy a servicer-style retention motion against any existing book, including small ones. Optimal Blue Capture and TrustEngine work on portfolios as small as a few thousand loans. Even brokers that do not own servicing rights typically have prior-applicant CRM data that satisfies the originator-relationship logic of HPPA’s first carve-out. The tooling investment is six to ten thousand dollars annually for a small operator, and the return on a single recaptured loan covers it.

Document PEWC for every contact lane in line with the reinstated FCC standard, with state mini-TCPA overlays where applicable. The August 2025 reinstatement gives operators a slightly looser standard than the vacated 2024 one-to-one rule, but documentation discipline still matters for both enforcement risk and litigation defense. The serial TCPA litigators framework covers the plaintiff economics that drive the documentation expectation.

Re-price the loan. Brokers without a servicing book or depository relationship should expect their effective customer-acquisition cost to roughly double from late-2025 levels. Loan-level pricing must absorb that increase, either through points on rate sheets, originator compensation adjustments, or volume contraction. The math does not produce a free lunch; the only choice is where the cost lands.

Where 2026 and 2027 Land

The HPPA effect on the mortgage market is structural, not cyclical. Trigger leads as a credit-bureau product are not coming back, even if a future Congress revisits the statute, because the political coalition that produced it included consumer groups, broker associations, and depositories simultaneously. The substitution patterns that emerge in the next 18 months will define mortgage lead generation through the end of the decade.

Three patterns are visible already. The first is that paid-acquisition pricing on Google, LendingTree, Zillow, and Bankrate will plateau above pre-HPPA levels rather than returning to baseline once volume substitutes settle. The roughly 45% YoY CPL increase that HousingWire reports in early 2026 is the spike phase; the equilibrium is likely to land 20 to 30% above 2024 levels. Lenders modeling 2027 budgets against 2024 CPLs will run short.

The second is that servicer recapture becomes a competitive moat rather than a back-office function. Rocket’s $14.2 billion bet on Mr. Cooper is the largest expression of that thesis, but the same logic applies to every lender with a servicing book of any size. The operators that retain servicing rights and deploy recapture tooling will compound; the operators that sold servicing for working capital during the boom will face structural cost-of-acquisition disadvantage that compounds in the other direction.

The third is that soft-pull prequalification migrates from a niche product to a default top-of-funnel mechanic. Xactus, Equifax, and Experian have priced these products as premium services for years; HPPA economics make them the cheapest path to a credit-quality signal that does not feed the (now narrower) prescreen pipeline. Vendors that price aggressively and integrate into the mortgage pre-approval lead programs workflow will displace harder-pull legacy patterns.

The longer horizon question is whether the political logic that produced HPPA extends to other verticals. Auto finance, personal loans, and credit cards all run their own versions of trigger-lead-style prescreen products under FCRA §604(c), and the consumer-protection coalition that backed HPPA has signaled interest in extending the framework. Lead-generation operators outside mortgage should treat HPPA as a template, not an exception.

Key Takeaways

- HPPA takes effect March 4, 2026 and amends FCRA §604(c) to restrict prescreened mortgage reports to the consumer’s current originator, current servicer, an insured depository holding the consumer’s account, or a documented opt-in. Independent brokers and non-depository lenders without prior-origination relationships lose access to the channel entirely, and acquisition-cost models must reset accordingly.

- Internet purchase-lead CPLs are up roughly 45% year over year per HousingWire, with credit-report costs rising as much as 50% on top of base bureau increases. The combined cost shock is structural, not transitory; operators modeling 2027 against 2024 baselines will materially under-budget.

- The $14.2 billion Rocket-Mr. Cooper close on October 1, 2025 captures roughly one in six U.S. mortgages and applies an 83% recapture rate, approximately three times the industry average. HPPA’s carve-out structure protects that recapture engine from outside competition by statute, which is why the deal repriced 51% upward between announcement and close.

- The replacement stack is built around five substitutes: soft-pull prequalification (Xactus, Equifax, Experian), servicer recapture (Optimal Blue Capture, TrustEngine, Total Expert), originator CRM nurture (ICE Encompass, Surefire), paid acquisition (Google, LendingTree, Zillow, Bankrate), and first-party SEO. None individually replaces trigger-lead economics; the working answer is a portfolio.

- HPPA and TCPA stack as serial gates. The FCC reinstated PEWC on August 29, 2025 and pushed the revoke-all rule to January 31, 2027, leaving 2026 outbound under the older PEWC standard. Lenders satisfying an HPPA carve-out still need PEWC for autodialed or texted contact, federal and state DNC scrub, and state mini-TCPA compliance.

- Servicer recapture becomes the central competitive battleground. Lenders that retained servicing rights compound through the carve-out; lenders that sold servicing rights for working capital during the 2020-2022 boom face structural cost-of-acquisition disadvantage that does not reverse without buying servicing back at premium prices.

- Soft-pull prequalification migrates from niche to default. Hard-pull credit reports at the top of funnel become economically untenable when the prescreen pipeline they feed is closed and the per-pull cost is up 50%. Operators integrating Xactus Pre-App X or equivalent ahead of March 4, 2026 avoid the worst of the post-effective price spike.

- State law overlays survive. HPPA preempts only direct conflicts, leaving state mini-trigger statutes, state mini-TCPAs, and state UDAP authority in place. Multi-state operators need a state-by-state matrix; single-state operators need to read their state law against the new federal floor.

- The political coalition behind HPPA spans consumer groups, broker associations, and depositories simultaneously. The consumer-protection logic likely extends to auto finance, personal loans, and credit-card prescreening over the next several years. Lead-generation operators outside mortgage should treat HPPA as a template.

- Independent brokers and mid-size non-depository lenders face the steepest adjustment. The practical playbook: cut trigger spend before the effective date, stand up soft-pull prequal, deploy recapture tooling against any existing book, document PEWC end-to-end, and re-price the loan to absorb the cost-of-acquisition increase that the math will not absorb itself.

Frequently Asked Questions

What is the Homebuyers Privacy Protection Act?

The Homebuyers Privacy Protection Act (HPPA), H.R. 2808 in the 119th Congress, is a federal statute signed September 5, 2025 that amends section 604(c) of the Fair Credit Reporting Act to restrict prescreened consumer reports tied to a residential mortgage credit inquiry. It takes effect March 4, 2026, 180 days after enactment. The law preserves prescreening for four narrow recipients: the consumer’s current mortgage originator, the current servicer, an insured depository institution or credit union holding a current account for the consumer, and any party with documented consumer opt-in. Outside those carve-outs, the standard mortgage trigger lead disappears as a credit-bureau product.

When does the HPPA take effect and is it retroactive?

HPPA takes effect March 4, 2026, exactly 180 days after the September 5, 2025 signing. It is not retroactive. Trigger leads sold before that date remain lawful and can still be worked under existing TCPA, DNC, and state-level rules. Lists generated on or after March 4, 2026 must satisfy one of the four statutory carve-outs to leave the credit bureaus. Pipeline records purchased earlier do not become unlawful overnight, but lenders relying on continuous trigger feeds will see those feeds stop or shrink at the effective date. The implementation window was extended from the more typical 90 days because Equifax, Experian, and TransUnion need to rewrite filtering logic for their prescreen feeds.

Which lenders can still receive a trigger lead under HPPA?

Four classes of recipients keep prescreen access. The originator of the consumer’s current mortgage may receive a trigger lead when that consumer applies elsewhere. The current servicer may also receive it, even when servicing rights and origination sit at different companies. An insured depository institution or credit union holding a deposit, loan, or asset account for the consumer qualifies under the existing-relationship carve-out. Anyone else needs documented consumer authorization that meets FCRA standards for express consent. The combined effect favors integrated origination-plus-servicing platforms and depositories, and removes most independent third-party telemarketers from the supply chain.

How much will mortgage cost per lead actually rise?

Internet purchase-lead CPLs are already trending roughly 45% higher year over year on the major aggregator platforms, per HousingWire reporting in early 2026. Range pricing on rate-table and exclusive purchase leads sits between $150 and $250 each, with non-exclusive shared leads in the $80 to $130 band. Credit-report bundle pricing is rising as much as 50% in 2026 because Experian and FICO have re-priced mortgage-grade reports on top of base bureau increases. The supply curve shifted as Equifax, Experian, and TransUnion lose roughly $200 to $300 million in combined trigger-lead revenue, while demand stays constant or rises, forcing lenders into Google, aggregators, and direct-mail substitutes.

What replaces trigger leads operationally?

Four substitutes carry most of the load. Soft-pull prequalification through Xactus Pre-App X, Equifax Mortgage Prequalification, or Experian Prequalification surfaces credit-eligible prospects without firing a hard mortgage inquiry. Servicer recapture, anchored by tools like Optimal Blue Capture and TrustEngine, mines the existing book for refinance and home-equity opportunities the lender already has a relationship with. ICE Encompass and Surefire CRM automate the prequal-to-application path inside the loan-origination system. Paid acquisition through Google rate tables, LendingTree, Zillow, and Bankrate absorbs the rest, at materially higher CPLs than the displaced trigger feed.

How does HPPA interact with TCPA after the August 2025 PEWC reinstatement?

HPPA controls who may receive a prescreened mortgage report. TCPA controls how anyone may call or text the consumer once contact data is in hand. The two stack rather than overlap. After the Eleventh Circuit’s IMC v. FCC vacatur in early 2025, the FCC reinstated the prior prior-express-written-consent standard on August 29, 2025, and the agency has since extended the revoke-all rule to January 31, 2027. A lender pulling a permitted trigger lead under one of HPPA’s carve-outs still needs PEWC to autodial or text that consumer, scrubs against state and federal DNC, and must honor any previously recorded revocation. Compliance teams should treat HPPA and TCPA as serial gates, not redundant ones.

Why did Rocket buy Mr. Cooper, and what does it have to do with trigger leads?

Rocket Companies closed its $14.2 billion acquisition of Mr. Cooper Group on October 1, 2025, four weeks after President Trump signed HPPA. The combined company services roughly 10 million homeowners, about one in six U.S. mortgages, and carries a roughly $2.1 trillion servicing book. Rocket’s standalone recapture rate is 83%, approximately three times the industry average, and applying that recapture engine to Mr. Cooper’s portfolio is the strategic point of the deal. With trigger leads disappearing for outside competitors, the originator-servicer carve-out hands the existing relationship advantage directly to Rocket. The transaction is, in effect, a structural bet that HPPA passes.

What should independent brokers do before March 4, 2026?

Independents that ran on trigger leads need a substitute pipeline operational before the effective date, not on it. The practical sequence is: cut trigger spend ahead of schedule to redirect budget into Google rate tables, LendingTree, Zillow, or local SEO; stand up a soft-pull prequalification flow with Xactus, Equifax, or Experian so leads enter the funnel without firing a hard inquiry; deploy a servicer-style retention motion against any existing book, even small ones, using Optimal Blue Capture or TrustEngine; document PEWC for every contact lane in line with the reinstated FCC standard. Brokers without a servicing book or depository relationship should expect their effective CPL to roughly double and price loans accordingly.

Are state mini-trigger laws still active after HPPA?

Yes. Several states had passed or proposed restrictions on mortgage trigger leads before federal action, and HPPA preempts only where it directly conflicts. State requirements that go further, such as enhanced disclosure or stricter timing rules, can continue to apply. Compliance officers should treat HPPA as the federal floor and run a state-by-state matrix for any multi-state lending footprint. The Conference of State Bank Supervisors and individual state attorneys general retain enforcement authority over deceptive practices that survive HPPA, and state mini-TCPA statutes such as Florida’s FTSA and Oklahoma’s OTSA still apply to outbound contact regardless of how the lead was sourced.

Will trigger leads come back in another form?

Probably not as a credit-bureau product, but partial substitutes are already visible. Soft-pull prequalification flows can identify mortgage-curious consumers without triggering a hard inquiry, and several vendors are productizing portfolio monitoring that surfaces refinance candidates from a lender’s own book. Marketing-list providers are repositioning around modeled propensity scores, public-records data, and listing alerts rather than credit-inquiry triggers. None of these will replicate the timing precision of a same-day mortgage trigger because the FCRA prescreen pipeline was unique. Expect 2026 and 2027 to settle into a market where lenders pay more for slower, lower-precision intent signals and compete harder for the existing relationships HPPA’s carve-outs protect.

The mortgage lead-generation business that worked through the end of 2025 is gone. What replaces it rewards depositories, integrated originator-servicers, and any operator with the discipline to rebuild around owned relationships and soft-pull credit signals before the effective date forces the rebuild under price-spike conditions. The window between now and March 4, 2026 is the cheapest time to make the transition; every month after the effective date is more expensive than the one before it.

Sources

- U.S. Congress, “H.R. 2808 - 119th Congress (2025-2026): Homebuyers Privacy Protection Act”, Congress.gov, signed September 5, 2025.

- Hunton Andrews Kurth LLP, “Homebuyers Privacy Protection Act Amends FCRA”, Privacy and Cybersecurity Law Blog, September 2025.

- Troutman Pepper Locke, “The Homebuyers Privacy Protection Act Becomes Law”, Consumer Financial Services Law Monitor, September 2025.

- Rocket Companies, “Rocket Companies Closes $14.2 Billion Acquisition of Mr. Cooper”, Press Release, October 1, 2025.

- HousingWire, “Mortgage lead prices to rise as trigger lead ban disrupts lenders”, 2026.

- HousingWire, “Credit report costs for mortgage lenders to rise up to 50% in 2026”, 2026.

- Optimal Blue, “Optimal Blue Launches New Lead Generation Tool for Originators”, Press Release, June 9, 2025.

- Burr & Forman LLP, “FCC Delays Effective Date of TCPA Revoke-All Rule Until January 31, 2027”, 2026.

- ActiveProspect, “Understanding the FCC One-to-One Consent Rule Update”, 2025.

- Scotsman Guide, “Trigger Leads Legislation Passes Through Full Senate by Unanimous Consent”, August 2025.