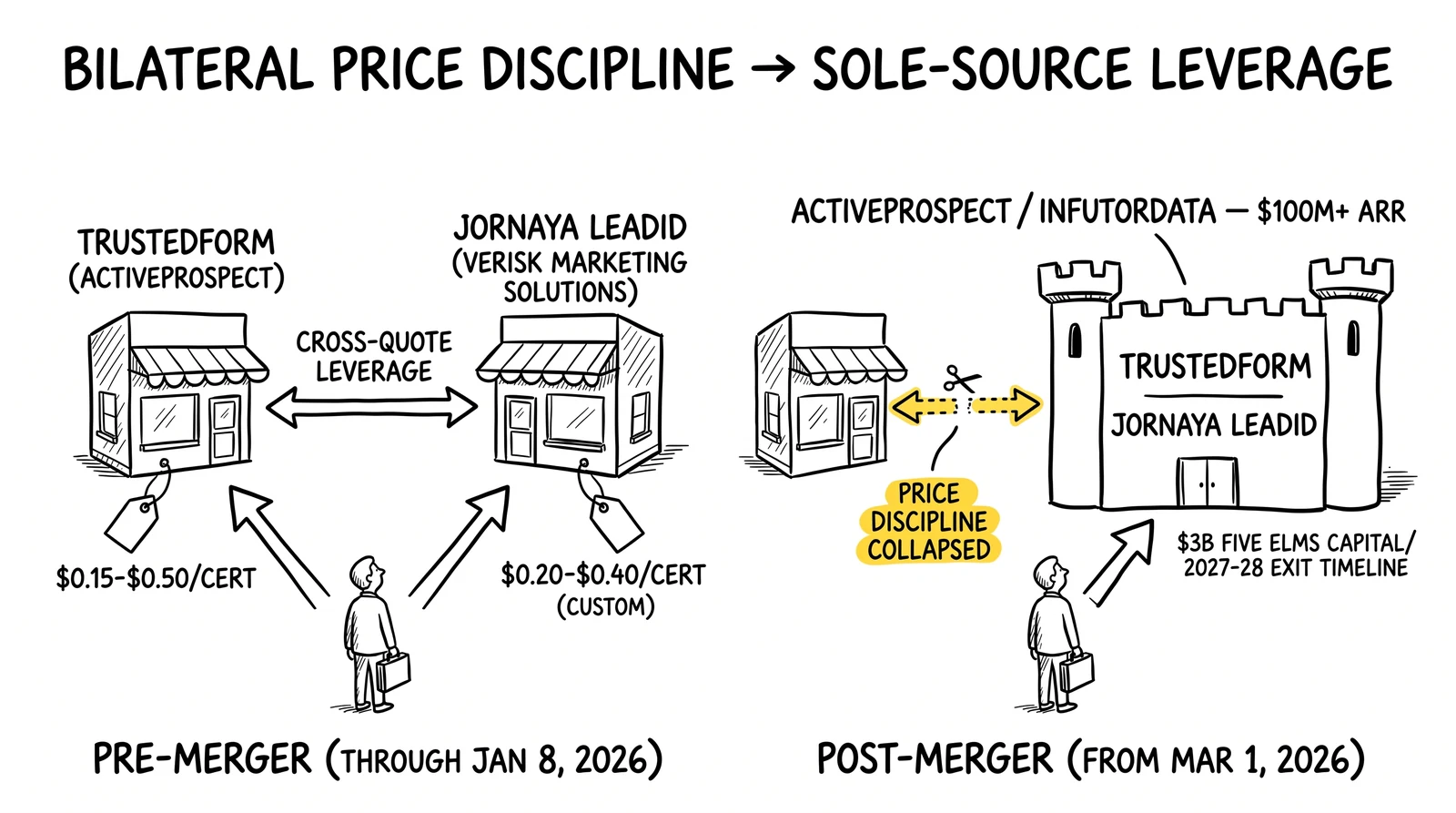

One private-equity-backed vendor now controls both commercially significant independent TCPA consent certificates in the U.S. lead generation market – and the buyer-side leverage that defined the prior decade just collapsed.

The March 1 Rebrand and What Actually Changed

ActiveProspect closed the acquisition of Verisk Marketing Solutions from Verisk Analytics on January 8, 2026, and rebranded the data unit as InfutorData effective March 1, 2026 (the rebrand was publicly recapped on the company’s blog roughly seven weeks later). The two announcements together complete a five-year consolidation arc that began with Verisk’s December 2020 purchase of Jornaya - terms of which were not publicly disclosed, with trade press reporting figures in the $125 to $145 million range that were never officially confirmed - and continued with Verisk’s $225 million purchase of Infutor in February 2022. By the time Verisk announced the unit’s sale on January 8, 2026, the combined Jornaya-plus-Infutor business was operating under the Verisk Marketing Solutions banner and had been earmarked for divestiture as Verisk refocused on its core insurance-analytics franchise. ActiveProspect – backed by Five Elms Capital since April 2020 – was the buyer that made strategic sense: the only company in the lead-generation stack with the customer base and certificate-handling infrastructure to absorb both the data assets and the LeadiD product line without creating channel conflict.

The deal terms were not publicly disclosed. The combined company exceeds $100 million in annual recurring revenue per the rebrand announcement, and the operating model splits into two product lines: ActiveProspect continues to run the consent-and-orchestration platform centered on TrustedForm, and InfutorData operates as a separate data-and-identity business covering identity resolution, enrichment, and the Jornaya LeadiD certificate. Steve Rafferty, ActiveProspect’s founder and CEO, framed the rebrand around “trust, transparency, and performance” but the operational reality is starker: a single executive team now sets pricing, roadmap, and packaging for the two products that defined independent third-party consent certification for the past decade.

Eric Troutman, who writes the TCPAWorld site under the byline “the Czar,” called the deal a “huge win for the good guys” in his January 8 commentary and described ActiveProspect as the natural winner among bidders. Troutman’s framing matters because his readership skews heavily toward the defense bar and enterprise compliance teams who specify which certificates buyers must accept. His endorsement signals that the enterprise side of the market views consolidation as a quality move rather than a competition concern. The buy-side reality is more complicated, and the next twelve months will reveal which framing the market actually accepts.

Why Both Certificates Existed in the First Place

For most of the 2015-to-2025 period, TrustedForm and Jornaya served different parts of the same compliance problem. TrustedForm Certify, the publisher-side product, captured a session-replay snapshot of the consumer’s interaction with a lead form: the page they saw, the boxes they checked, the consent language displayed at the moment of submission. TrustedForm Retain, the buyer-side product, let lead buyers claim and store the certificate against their own account so the document existed in their custody for the TCPA five-year statute-of-limitations window. The product’s defensibility advantage came from visual session replay: in litigation, defendants could show a court the actual page the plaintiff saw, not just a database row asserting consent existed.

Jornaya took a different route. The LeadiD product captured behavioral signals across the consumer’s full lead-gen journey – every form interaction, every cross-site session, every duplicate submission – and rolled those signals into a fraud-and-quality score that buyers used during ping-post evaluation. LeadiD certificates established that a consumer was on the publisher’s page at a specific moment, with timestamp and basic environmental data, but Jornaya’s pitch leaned more on consumer-journey intelligence than on visual reproduction of the consent moment. In verticals where seller networks standardized early – mortgage, auto insurance, and elder-care lead programs in particular – Jornaya became the contractual default because the seller-side platforms integrated it first.

By 2024 a meaningful portion of the enterprise lead-buyer base required both certificates by contract. The redundancy made sense for two reasons. First, the certificates captured complementary evidence: TrustedForm captured what the consumer saw, Jornaya captured how the consumer behaved across the journey. Second, the bilateral relationship between two independent vendors gave enterprise buyers leverage. A buyer who told ActiveProspect that Jornaya offered a better volume rate could extract a discount, and the same conversation worked in reverse with Verisk. The two-vendor structure functioned as price discipline even when the products themselves overlapped on the actual TCPA-defense use case. That structure ended on January 8, 2026.

The Five-Year Decline That Made the Merger Possible

Verisk’s strategic exit from marketing solutions did not happen in isolation. Lee Shavel became CEO of Verisk Analytics in May 2022 and immediately began a portfolio review that prioritized the insurance-data franchise – the company’s high-margin, regulated-buyer core – over its expansion into adjacent markets. The marketing-solutions group, built through the Jornaya and Infutor acquisitions during the prior CEO’s tenure, never reached the gross-margin profile that Verisk’s insurance-analytics business runs. Insurance-data customers buy on regulatory necessity and pay through the cycle; marketing-data customers buy on growth budget and cut spend in downturns. The 2022-to-2024 advertising slowdown exposed that margin difference at exactly the moment Verisk’s investor base was pushing for portfolio focus.

Public filings from Verisk during that period repeatedly described the marketing-solutions unit as a candidate for strategic alternatives, which is finance-speak for “actively shopping.” By the time the January 8, 2026 announcement landed, the deal had been telegraphed for at least eighteen months. The specific buyer – ActiveProspect rather than a traditional martech roll-up shop – was the surprise; the fact of the sale was not. Lee Shavel’s quoted statement in the January 8 release that the transaction “reaffirms our commitment to focusing on data, analytics and technology solutions for the global insurance industry” reads as a clean restatement of the strategic logic that had been driving Verisk’s portfolio decisions for the prior three years.

For ActiveProspect the calculation ran in the opposite direction. The company’s TrustedForm product had reached scale – the platform certifies more than 2.5 billion leads annually across more than 40,000 websites per the 2026 product page – but the natural growth ceiling for a single-product certificate business was visible. The next leg of growth required either international expansion, vertical adjacency, or platform consolidation. Buying VMS bought all three at once: the Infutor identity graph extended ActiveProspect’s reach into identity resolution, the Jornaya behavioral data extended it into journey analytics, and the LeadiD certificate eliminated the only product directly competitive with TrustedForm in the U.S. market.

Concentration Risk Math: Pricing Power on the Buyer Side

The pricing-power shift from the consolidation is structural, not cyclical. Before the deal, the two-vendor structure produced bilateral price discipline: every buyer renegotiation forced ActiveProspect and Verisk to reference each other’s pricing. After the deal, ActiveProspect controls both reference points.

The historical precedent for vendor concentration in adjacent data markets is unambiguous. When Equifax acquired major credit-attribute providers through the 2010s, enterprise contract pricing rose at compound annual rates of roughly 7 to 12 percent for two to three years post-merger. Experian’s identity-resolution roll-up produced similar dynamics. LexisNexis Risk Solutions, after consolidating public-records vendors, raised enterprise-tier prices in the high-single-digits annually for several years before hitting buyer pushback. None of those merged businesses was the only commercial substitute in its category – credit data and public records had at least two major competitors throughout. ActiveProspect, after closing InfutorData, has no comparable U.S. competitor in third-party independent consent certification. The concentration is closer to a true duopoly collapsing into a monopoly than to a typical mid-market merger.

The consolidation also changes how buyers should model their TCPA-defense cost line. The prior model treated certificates as a commodity with stable per-cert pricing and predictable annual increases tied to volume tiers. The new model needs to treat certificates as a sole-source vendor relationship with bundled-pricing risk: ActiveProspect can – and growth-equity-backed companies typically do – restructure packaging to push buyers toward higher-priced bundles that mix consent certification with identity resolution, lead orchestration, or analytics. A buyer who today pays $0.25 per TrustedForm cert and a separate flat fee for LeadiD might in 2027 face a “consent-and-identity” bundle priced at $0.45 per cert with the identity layer included. That kind of repackaging is invisible to a buyer who is not actively monitoring the line item.

The table below compares the rough pricing structure across the consolidation event.

| Pricing Element | 2024–2025 (Pre-Merger) | 2026 (Post-Merger) | 2027 Forecast |

|---|---|---|---|

| TrustedForm Retain per cert | $0.15–$0.50 | $0.15–$0.50 (unchanged at announcement) | $0.20–$0.60 with bundle pressure |

| Jornaya LeadiD per cert | $0.20–$0.40 (custom) | $0.20–$0.40 (unchanged at announcement) | Bundled with TrustedForm or InfutorData enrichment |

| Effective dual-cert cost | $0.35–$0.90 | $0.35–$0.90 | $0.40–$0.95, with redundancy increasingly questioned |

| Buyer leverage at renewal | High (bilateral price discipline) | Low (sole-source) | Low; recovered only via MFN clauses and audit rights |

Source: ActiveProspect pricing page, secondary-market reporting on LeadiD enterprise contracts, vendor-concentration precedent from credit-data and public-records consolidations. The 2027 column is a site planning scenario, not a published market forecast.

The numbers in the 2027 column are planning-scenario estimates anchored to historical comparables, not source-supported forecasts. The structural direction – upward pressure on per-cert pricing absent active buyer-side leverage – is supported by the precedent set in adjacent data markets after similar consolidations, but the specific 8 to 15 percent band is a site model rather than a vendor-published or analyst-published projection.

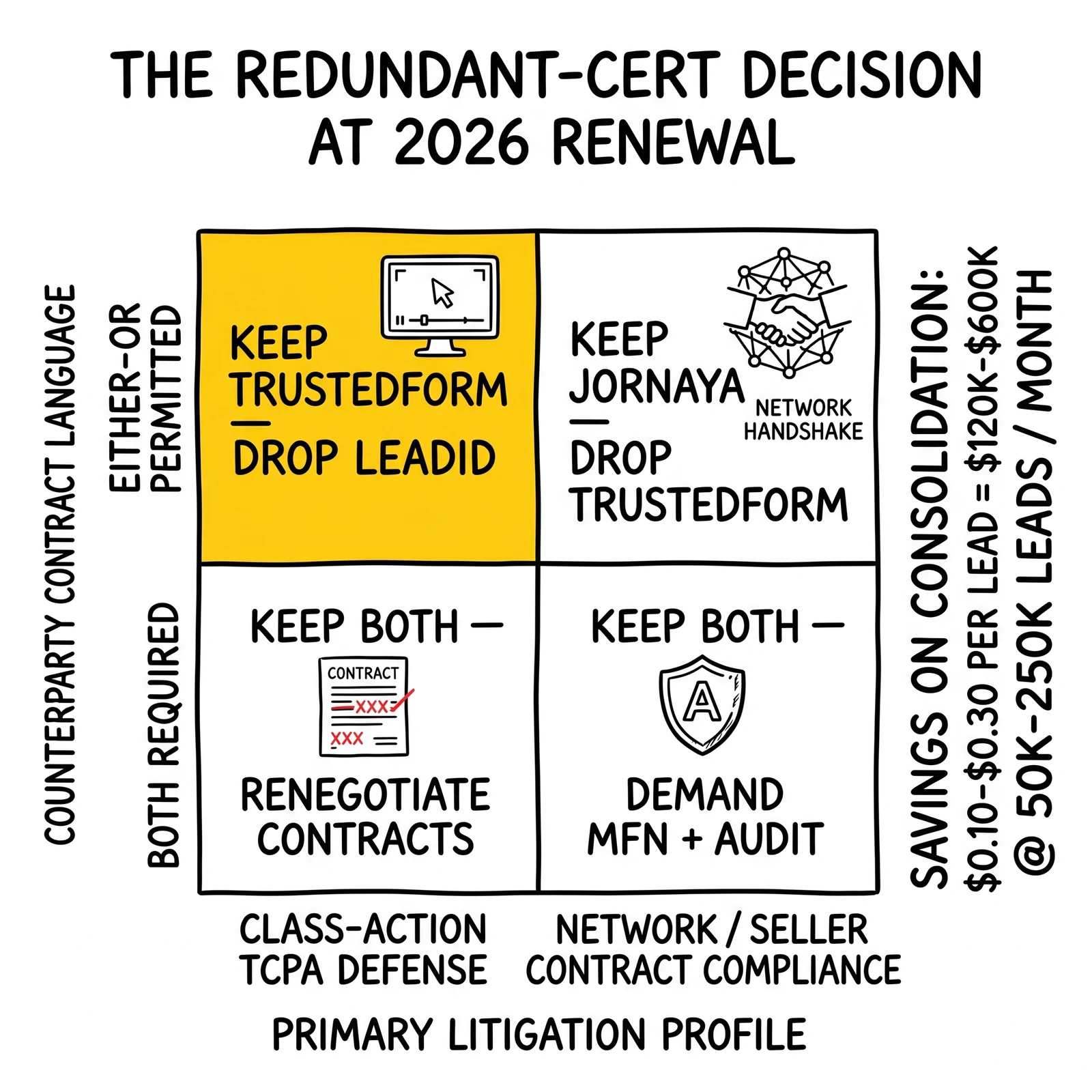

The Redundant-Cert Decision

The decision to drop one of the two certificates is the most concrete operational question facing buyers in 2026. Three factors drive the answer: vertical norms, litigation profile, and counterparty contract language. None of them favors a one-size-fits-all answer.

Vertical norms create the strongest constraint. In the mortgage and auto-insurance verticals, large seller networks and aggregator platforms specified Jornaya LeadiD in their integration documentation for years before TrustedForm achieved comparable enterprise penetration. Buyers who source from those networks often have inbound contracts that require a LeadiD on every record. Dropping LeadiD in those contexts means renegotiating with sellers, which usually means renegotiating price. In the legal-leads and Medicare verticals, TrustedForm reached broader penetration earlier and is more commonly the contractual default. Operators in mixed-vertical buyer portfolios should run the audit by counterparty rather than across the book.

Litigation profile is the second factor. Defendants whose primary TCPA exposure runs through class-action discovery typically lean on TrustedForm because the visual session replay produces evidence courts can interpret without expert testimony. ActiveProspect’s analysis of TCPA cases reports that defendants with valid third-party certification – TrustedForm, Jornaya, or equivalent – won dismissal or summary judgment in 73 percent of cases versus 41 percent for defendants without certification. The 73 percent figure does not isolate TrustedForm from Jornaya, and existing case law treats both as third-party-witness evidence. The practical defense difference between the two products is more about which certificate the buyer can produce on demand during 30-day discovery deadlines than about which one carries more weight in a final ruling.

Counterparty contract language is the most underappreciated factor. Many buyer-seller contracts written between 2020 and 2024 specify “TrustedForm or Jornaya” as either-or, which gives buyers freedom to consolidate. Many other contracts written in the same period specify both, often because a procurement team copied template language from a different vertical without auditing the specific operational requirements. Operators considering dropping a redundant cert need to grep every active contract for the specific language and identify the contracts that constrain consolidation. The companies that move first – that audit, renegotiate, and consolidate before competitors do – capture the per-cert savings and lock them in before vendor pricing adjusts to the new equilibrium. The companies that move last face the same per-cert cost but with less buyer-side leverage and a vendor that has already absorbed the easy renegotiation gains.

For a typical mid-market buyer running 50,000 leads per month with both certificates active, the savings math is direct. Dropping one cert at an average $0.20 per-cert cost saves $10,000 monthly, $120,000 annually. At 250,000 leads per month, the savings reach $600,000 annually. Those numbers compound over multi-year contracts and against the alternative of accepting a 10 percent annual price increase from a sole-source vendor.

Identity-Graph Reach Across Verticals

The InfutorData identity graph is the asset that separates this deal from a simple martech merger. Per the InfutorData public marketing as of April 2026, the TrueSource identity graph references roughly 260 million U.S. consumer profiles tied to more than 120 million households, with the company reporting 100 million daily updates from authoritative and permissibly licensed sources. The Total Consumer Insights product layer adds behavioral and household-attribute data on roughly 266 million U.S. consumers, drawing on the legacy Infutor-and-Jornaya combined dataset.

For lead operators, the identity graph matters in three ways. Identity resolution lets a buyer match a submitted lead – a name, address, phone, email – to a verified consumer record in real time, before paying for the lead. That match is the foundation of fraud-and-duplicate detection at the buyer side. Cross-channel match keys allow a buyer to associate the same consumer across email, phone, and address even when one identifier degrades, which matters for nurture and remarketing flows where the original phone number may go stale within months of submission. Household-level data underwrites the risk-and-rate models that drive bid prices in insurance verticals – a household with a recent home purchase, two drivers, and a 720+ credit profile is worth a meaningfully different bid than a household with one driver and a sub-600 score.

The cross-vertical implications of consolidation become visible when the certificate event and the identity graph live under one vendor. Before the merger, an enterprise buyer in the auto-insurance vertical typically integrated TrustedForm for consent capture, Jornaya for journey analytics, and a third identity-resolution vendor (often LiveRamp, Acxiom, or Neustar before its TransUnion acquisition) for consumer match. After the merger, ActiveProspect’s combined platform can theoretically deliver consent capture, behavioral signal, and identity match in one workflow against one billing relationship.

The table below summarizes the identity-graph reach by vertical use case.

| Vertical | Primary Cert Used Pre-Merger | Identity-Graph Use Case | InfutorData Reach |

|---|---|---|---|

| Auto insurance | Jornaya (seller-network default) | Household risk profile, multi-driver match | 120M+ households with vehicle and household attributes |

| Mortgage | Jornaya + TrustedForm (often both) | Property and life-event triggers | Property and address-level coverage on 260M+ consumer records |

| Medicare | TrustedForm (CMS-aligned defaults) | Age-band and eligibility match | Demographic match on the 65+ population per Total Consumer Insights |

| Legal leads (mass tort) | TrustedForm | Plaintiff identity verification | Address and contact match against U.S. adult population |

| Solar | Mixed | Homeownership and roof-suitability indicators | Property attributes layered onto consumer match |

Source: InfutorData product pages and case studies, vendor-network documentation across verticals.

The cross-vertical reach is the strategic asset that justifies the deal price for ActiveProspect even if certificate pricing held flat. Identity resolution as a category has historically commanded higher gross margins than commodity certificate pricing, and ActiveProspect’s customer base – 40,000-plus websites and the buyers connected through them – gives the InfutorData product a built-in distribution channel. The risk for buyers is that the bundled product replaces three separately negotiated relationships with one, and bundled-pricing models historically erode buyer leverage.

Operator Playbook: 2026 RFP Leverage, MFN Clauses, Audit Rights

Operators entering 2026 RFP and renewal cycles need a different playbook than the one that worked through 2024. The bilateral price discipline that defined the prior decade is gone. The leverage that remains comes from contract terms negotiated at signing rather than from competitive pressure between vendors. Three contract terms matter most.

Most-favored-nation pricing language is the first lever. An MFN clause ties the buyer’s per-certificate rate to the best published or negotiated rate the vendor offers any comparable customer. The clause matters more after vendor consolidation because it neutralizes price discrimination across post-merger account tiers. ActiveProspect, like every consolidator, has incentive to introduce new tiers that segment customers – enterprise-strategic, enterprise-standard, mid-market, growth – and to price each tier separately. An MFN clause forces the vendor to disclose comparable-customer pricing or to cap the buyer’s rate at the lowest published tier. The drafting matters: a poorly scoped MFN can be evaded through bundle restructuring, so the clause needs to apply to per-certificate cost on a per-unit basis rather than to total contract value.

Audit rights are the second lever. The right to sample certificate retrieval, verify uptime, and confirm certificate retention protects against quiet roadmap changes. ActiveProspect retains certificates for the full TCPA five-year statute window per its current product documentation, but the contract should state that retention period explicitly with the buyer’s right to retrieve any certificate within 24 hours during the retention window. Audit rights should also cover data-export format and pricing – buyers who plan to migrate off the platform need to know in advance what an export of five years of certificates will cost and how it will be delivered. Vendors who push back on audit-rights language are typically signaling that they expect to change those mechanics post-signing.

Data-portability and certificate-retention clauses are the third lever. Even buyers who plan to stay on ActiveProspect indefinitely should negotiate the right to retrieve every certificate the platform generated under the contract for the full five-year window after termination. The litigation timeline does not align with vendor-contract timelines: a TCPA case filed in year four of a contract may settle in year seven, two years after the contract expired. If the buyer cannot produce the certificate during settlement discovery, the certificate’s existence does not matter. Buyers who skip these terms at signing have no leverage when the vendor changes packaging, raises rates, or sunsets a product.

Beyond contract terms, the operator playbook needs a 60-day audit cadence. Pull every active seller and buyer agreement and grep for the strings TrustedForm, Jornaya, LeadiD, ActiveProspect, Verisk, and Infutor. Note which certificates are required, which are optional, and which are described as either-or. Map the certificate-cost line item against the lead volume from each counterparty to compute the per-lead burden. Identify contracts up for renewal in the next 12 months and flag those for renegotiation. Cross-reference with consent-documentation retention requirements and the company’s actual TCPA-defense playbook. Operators who run this audit early enter their renewal cycles with leverage; those who do not will accept whatever pricing and packaging the consolidated vendor presents.

Alternatives to Single-Vendor Lock-In

The realistic alternatives to single-vendor lock-in are narrow in 2026 but they exist. Three categories are worth evaluating: dialer-and-distribution-platform consent capture, call-side certification, and in-house consent-capture builds.

Convoso and Phonexa offer integrated consent tracking inside their dialer and lead-distribution platforms. Both vendors record the consent event with timestamp, IP, user-agent, and the specific consent language displayed. The records are admissible as business-records evidence in TCPA cases, but they lack the third-party-witness independence that courts have credited to TrustedForm and Jornaya. Defense counsel typically treat dialer-side consent records as supporting evidence rather than as the primary evidentiary foundation. For buyers whose TCPA exposure runs through their own dialer rather than through purchased leads, the integrated approach can be sufficient. For buyers in shared-lead and ping-post markets where independent third-party evidence is the contract default, the integrated approach does not substitute for TrustedForm or LeadiD.

RingBA and similar pay-per-call platforms capture call-side consent for the click-to-call ecosystem. The model is structurally different: the consent moment lives on the publisher’s landing page before the call connects, and the platform records call-routing data with timestamps that link to the upstream consent capture. For buyers whose business model is primarily inbound call rather than form-fill leads, the call-side certificate ecosystem is a viable substitute and was always a parallel market. For buyers whose volume is form-fill, RingBA does not solve the problem.

In-house consent-capture builds are the third option and the most operationally demanding. A defensible in-house capture requires a logged JavaScript event store, session replay or equivalent visual reproduction of the consent moment, immutable retention with chain-of-custody documentation, and legal review by counsel familiar with TCPA evidentiary standards. The total cost of building, maintaining, and litigation-testing an in-house solution typically exceeds the per-certificate cost of TrustedForm or LeadiD until the buyer reaches roughly 10 million certificates per month. Below that volume, the build cost dominates the savings. Above it, the math can work – but only with sustained engineering investment and a willingness to test the build’s defensibility in actual litigation rather than in theoretical legal review.

The narrow conclusion: enterprise lead buyers in 2026 do not have a credible commercial substitute for TrustedForm or Jornaya at the volume tier where most of them operate. The leverage that remains comes from contract terms rather than from competitive pressure. Buyers who negotiate aggressively at signing – MFN, audit rights, data portability – preserve the value the prior bilateral structure delivered automatically. Buyers who do not negotiate aggressively will pay for the consolidation through pricing increases and bundle restructuring over the next three years.

What Happens at TCPA Defense When One Vendor Controls the Evidence

The TCPA-defense implications of single-vendor evidence control are subtle and underappreciated. Courts treat third-party consent certificates as business records under Federal Rule of Evidence 803(6), which allows their admission without the certificate vendor appearing as a witness. The vendor’s independence – its arms-length relationship with the defendant – has historically reinforced the records’ reliability. After consolidation, that independence narrative weakens.

The narrative weakening does not change admissibility. Courts will continue to admit TrustedForm and Jornaya certificates as business records, and the underlying evidence – visual session replay, behavioral signal, timestamp data – remains the same. What changes is the cross-examination. Plaintiffs’ counsel will now have a single-vendor target to probe on independence, conflict-of-interest, and integration with the defendant’s broader marketing stack. A plaintiff’s lawyer can question whether ActiveProspect’s commercial relationship with the defendant – through TrustedForm, Jornaya, and InfutorData identity-resolution products combined – creates a financial incentive to shape evidence in the defendant’s favor. The argument is unlikely to win on the admissibility side, but it can affect jury perception in cases that survive summary judgment.

The bigger TCPA-defense risk is operational rather than evidentiary. Buyers who rely on certificate retrieval during 30-day discovery deadlines need the certificate vendor to be operationally responsive. A vendor going through post-merger integration is statistically more likely to have outages, backlog issues, or staff turnover that delays retrieval. ActiveProspect’s track record on certificate retrieval has been strong, but the integration of InfutorData adds infrastructure and team complexity that did not exist before January 8, 2026. Defense-counsel teams should test certificate-retrieval response times during 2026 against the same SLAs that applied in 2024 and 2025, and should escalate any degradation to vendor account management before it becomes a litigation issue.

The one-to-one consent rule’s vacatur in the Eleventh Circuit’s January 24, 2025 decision in Insurance Marketing Coalition v. FCC also affects the analysis. The vacatur removed the federal regulatory mandate that drove much of the 2024 buying behavior on consent certificates and effectively reset the legal baseline to the pre-2024 TCPA prior-express-written-consent standard. Class-action filings continued at high rates through 2025 – TCPA exposure remains the dominant compliance risk for buyers regardless of the regulatory environment. The vacatur weakens one specific argument for redundant certification (that two certs together build a stronger one-to-one consent record) and strengthens the case for buyers to consolidate to a single cert at renewal.

The 12-Month Outlook

The next twelve months will reveal which version of the consolidation thesis the market accepts. The bull case for ActiveProspect is straightforward: the combined company has $100 million-plus in ARR, a unified platform spanning consent and identity, no commercially significant U.S. competitor in independent third-party certification, and growth-equity backing from Five Elms Capital with capacity to fund further acquisitions or product expansion. Steve Rafferty’s stated 2026 priorities – expansion into call leads, deeper partner collaboration, growth across social lead channels, and more flexible seller distribution – read as the natural next moves for a category leader consolidating around a platform pitch.

The bear case is more textured. The deal eliminates the bilateral price discipline that defined buyer-side economics for a decade. Buyer renegotiation cycles in 2026 and 2027 will produce data on how aggressively ActiveProspect pushes for bundle pricing, multi-year lock-ins, and tier-based discrimination. If pushback is strong – if enterprise buyers walk to in-house builds, force MFN clauses through procurement, or coordinate around new entrants – the consolidation premium ActiveProspect paid for VMS will compress. If pushback is weak, the platform thesis works and ActiveProspect emerges as a category-defining business in time for a 2027-or-2028 strategic exit or recapitalization.

The most likely scenario is segmented. Enterprise buyers – the top 200 lead-buyer accounts that drive most of the certificate volume – will negotiate hard at renewal, secure MFN and audit terms, and hold per-certificate pricing roughly flat through 2027. Mid-market buyers without procurement leverage will face annual price increases and bundle pressure inside the site planning scenario described above (8 to 15 percent as a base case, not a published forecast). Small buyers will accept whatever the standard pricing tier offers because the alternative is operating without certification, which the contractual ecosystem does not permit. The total revenue captured by ActiveProspect will grow regardless, but the distribution of that growth across customer tiers will reveal how durable the platform thesis really is.

For operators, the question is not whether the consolidation matters but how to extract leverage from a market that has lost most of its commercial alternatives. The contracts signed in 2026 will determine the per-certificate cost line for the rest of the decade. The audit, the renegotiation, the MFN drafting, and the data-portability clause are not theoretical exercises – they are the only mechanisms left for buyers to protect the value the prior bilateral structure delivered automatically. Operators who treat the rebrand as a formality and sign whatever the vendor presents will pay for that decision through the next three renewal cycles. Operators who treat it as a forcing function for contract discipline will preserve pricing and leverage that competitors give up.

The March 1 rebrand is not the end of the consolidation – it is the start of the next round of repackaging.

Key Takeaways

-

The deal eliminates the only commercial substitute for independent third-party consent certification in the U.S. market. TrustedForm and Jornaya LeadiD are now under common ownership, and no comparable independent vendor operates at enterprise scale. Buyer-side leverage that came from bilateral vendor competition is gone; the leverage that remains comes from contract terms negotiated at signing.

-

Pricing has not changed at the announcement; the 8-to-15 percent annual-increase range is a site planning scenario rather than a published market forecast. Adjacent data-market consolidations – Equifax, Experian, LexisNexis Risk Solutions – produced single-digit to mid-teens annual price increases on enterprise contracts post-merger, and ActiveProspect faces less competitive constraint than those mergers did, which is why the band is the planning baseline this analysis recommends operators stress-test against.

-

The redundant-cert decision now turns on counterparty contract language rather than vendor competition. Buyers should grep every active seller and buyer agreement for required-cert clauses, audit by counterparty, and target either-or contracts for consolidation savings of $0.10 to $0.30 per lead.

-

MFN pricing, audit rights, and data-portability clauses are the only remaining buyer-side leverage mechanisms. Operators entering 2026 RFP cycles need these terms drafted at the per-unit level rather than at total-contract-value level to prevent evasion through bundle restructuring.

-

The InfutorData identity graph is the strategic asset that justifies the deal price independent of certificate pricing. TrueSource references 260M-plus consumer profiles across 120M-plus households, and the cross-vertical reach gives ActiveProspect a bundled-product pitch that erodes the standalone certificate market.

-

TCPA-defense fundamentals remain unchanged but operational risk has increased. Defendants with valid third-party certification still win dismissal or summary judgment at roughly 73 percent versus 41 percent without per ActiveProspect’s case analysis. The operational risk is post-merger integration affecting certificate retrieval during 30-day discovery deadlines.

-

Five Elms Capital’s growth-equity backing implies a 2027-to-2028 liquidity event timeline. Pricing decisions and product packaging during this window will reflect EBITDA-optimization pressure, including price increases and bundle restructuring designed to maximize multiple at exit.

-

The Eleventh Circuit’s January 2025 vacatur of the FCC one-to-one consent rule weakens one argument for redundant certification but does not change the litigation environment that drives most enterprise compliance spend. Class-action filings continued at high rates through 2025; consent infrastructure remains the dominant TCPA-defense investment.

-

Alternatives to single-vendor lock-in are narrow. Dialer-side consent capture lacks third-party independence; in-house builds make economic sense only above 10 million certs per month; call-side certification covers only inbound-call business models. Most enterprise buyers do not have a credible commercial substitute.

-

The 60-day audit window after the rebrand is the operationally most valuable moment for buyers. Operators who run the audit and renegotiate before competitors do capture the consolidation savings; operators who do not will accept the new pricing equilibrium without leverage.

Frequently Asked Questions

What is InfutorData and when did it launch?

InfutorData is the rebranded identity-and-data business that ActiveProspect acquired from Verisk Analytics. The acquisition of Verisk Marketing Solutions was announced January 8, 2026 and the rebrand to InfutorData took effect March 1, 2026. The unit consolidates the legacy Infutor identity graph with the Jornaya behavioral data and LeadiD certificate product. ActiveProspect, the buyer, continues to operate the TrustedForm consent certificate platform separately. The combined company exceeds 100 million dollars in annual recurring revenue and is backed by Five Elms Capital. InfutorData’s TrueSource identity graph references roughly 260 million U.S. consumer records across more than 120 million households, drawing on data sources Verisk had assembled through the December 2020 Jornaya acquisition (terms not publicly disclosed; trade press reported figures in the $125 to $145 million range that were never officially confirmed) and the $225 million Infutor purchase in February 2022.

Does ActiveProspect now own both TrustedForm and Jornaya?

Yes. ActiveProspect acquired Verisk Marketing Solutions, the parent of Jornaya, on January 8, 2026, and on March 1, 2026 rebranded the data unit as InfutorData while continuing to operate the Jornaya LeadiD product under that umbrella. TrustedForm and Jornaya LeadiD have been the only two commercially significant independent consent-certificate vendors in the U.S. lead generation market for roughly a decade. With both certificates now owned by a single vendor, buyers who previously required dual certification for redundancy are now paying one company for two products that serve overlapping TCPA-defense functions. ActiveProspect has stated the two product lines will continue to operate, but pricing, packaging, and roadmap decisions sit with one executive team.

Will TrustedForm or Jornaya certificate pricing increase in 2026?

Public pricing has not changed as of April 24, 2026, but concentration economics point toward upward pressure on enterprise contracts at renewal. TrustedForm Retain certificates list at roughly 0.15 to 0.50 dollars per certificate depending on volume and contract terms; Jornaya LeadiD has historically used custom enterprise pricing without published rates. With the only direct substitute now under common ownership, buyers lose the bilateral leverage that previously held volume discounts in place. Comparable vendor consolidations – Equifax-led credit data, Experian-led identity-resolution, LexisNexis-led public records – produced single-digit to mid-teens annual price increases on enterprise contracts in the three years following the merger event. The 8 to 15 percent annual-increase range is a site planning scenario, not a published market forecast: operators planning 2026 and 2027 renewal cycles should model it as a base case while pressure-testing it against their actual contract terms and counterparty mix.

Should buyers drop one of the two certificates now that ActiveProspect owns both?

The redundant-cert decision depends on litigation profile, vertical, and counterparty contracts. Buyers in mortgage, auto insurance, and Medicare verticals where seller-side networks historically standardized on Jornaya may keep LeadiD because their seller agreements specify it. Buyers whose primary risk is TCPA class-action exposure typically lean on TrustedForm because of its visual session replay, which courts have treated as direct evidence of what the consumer actually saw and clicked. Defendants with valid third-party certification – TrustedForm, Jornaya, or equivalent – won dismissal or summary judgment 73 percent of the time according to ActiveProspect’s analysis of TCPA cases, versus 41 percent for defendants without certification. Dropping a redundant cert can save 0.10 to 0.30 dollars per lead, which compounds at scale, but only after auditing every active seller and buyer contract for required-cert clauses.

What is InfutorData’s identity graph and why does it matter to lead operators?

InfutorData’s TrueSource identity graph contains roughly 260 million U.S. consumer profiles tied to more than 120 million households, with the vendor reporting 100 million daily updates from authoritative and permissibly licensed sources. For lead operators, the graph matters in three ways: identity resolution lets buyers match a submitted lead to a verified consumer record before paying for it, which reduces fraud and duplicate spend; cross-channel match keys allow attribution across email, phone, and address even when one identifier degrades; and household-level data enables risk-and-rate models in insurance and financial-services verticals. With InfutorData and ActiveProspect under one roof, the lead-flow event captured by a TrustedForm certificate can theoretically be enriched against the identity graph in the same workflow, eliminating one vendor handoff.

Are there alternatives to TrustedForm and Jornaya for TCPA consent certification?

There are no equivalent independent third-party certification vendors operating at TrustedForm or Jornaya scale in 2026. Smaller competitors exist in adjacent layers: Convoso and Phonexa offer integrated consent tracking inside their dialer and lead-distribution platforms, but those records lack the third-party-witness independence that courts have credited to TrustedForm and Jornaya in TCPA defense. RingBA captures call-side consent for the click-to-call ecosystem. In-house consent-capture builds – typically a logged JavaScript event store plus session replay – can produce defensible evidence but require legal review, ongoing engineering investment, and a credible chain-of-custody story for litigation. Most enterprise lead buyers continue to require TrustedForm or LeadiD by contract, which forecloses substitution at the smallest end of the market.

How does the 2025 Eleventh Circuit ruling on one-to-one consent change the picture?

The Eleventh Circuit’s January 24, 2025 decision in Insurance Marketing Coalition v. FCC vacated the FCC’s one-to-one consent rule before its scheduled January 27, 2025 effective date, holding that the agency exceeded its statutory authority under the TCPA. That ruling removes the federal regulatory mandate that drove much of the 2024 buying behavior on consent certificates. It does not reduce the litigation environment that drives most enterprise compliance spend. Class-action filings continued at high rates through 2025, and many enterprise buyers still require TrustedForm or LeadiD certificates by contract. The vacatur weakens one specific argument for redundant certification – that two certs together build a stronger one-to-one consent record – and strengthens the case for buyers to consolidate to a single cert at renewal.

What contract terms should lead buyers demand at 2026 renewal?

Three terms matter most. Most-favored-nation pricing language ties the buyer’s per-certificate rate to the best published or negotiated rate offered to comparable customers; this discipline matters more after vendor consolidation because it neutralizes price discrimination across post-merger account tiers. Audit rights – the contractual ability to sample certificate retrieval and verify uptime, certificate retention, and data export – protect against quiet roadmap changes. Data-portability and cert-retention clauses ensure that if the buyer migrates off the platform, every certificate generated under the contract remains retrievable for the full TCPA five-year statute-of-limitations window. Buyers who skip these terms at signing have no leverage when the vendor changes packaging, raises rates, or sunsets a product line.

What does the Five Elms Capital backing imply about ActiveProspect’s roadmap?

Five Elms Capital is a Kansas City growth-equity firm that manages roughly 3 billion dollars across founder-owned B2B software companies, with typical check sizes of 15 to 150 million dollars. The firm took a strategic growth investment in ActiveProspect in April 2020 and has continued to back the company through the Verisk Marketing Solutions acquisition. Growth-equity capital structures generally aim for liquidity within five to seven years through either a sale or an IPO, which suggests ActiveProspect is on a 2026-to-2028 path toward a strategic exit or recapitalization. The implication for buyers: pricing decisions and product packaging during this window will reflect EBITDA-optimization pressure, including price increases, bundle restructuring, and a push toward multi-year contracts that lock in revenue.

How should operators audit existing seller and buyer contracts after the rebrand?

Run a four-step audit within the first 60 days. Pull every active seller and buyer agreement and grep for the strings TrustedForm, Jornaya, LeadiD, ActiveProspect, Verisk, and Infutor; note which certificates are required, which are optional, and which are described as either-or. Map the certificate-cost line item against the lead volume from each counterparty to compute the per-lead burden. Identify contracts up for renewal in the next 12 months and flag those for renegotiation in light of the new single-vendor reality. Finally, document the chain-of-custody for certificate retrieval – who pays, who retrieves, who retains the cert during the five-year window. Operators who run this audit early enter their renewal cycles with leverage; those who do not will find themselves accepting whatever pricing and packaging the consolidated vendor presents.

Sources

- Verisk Announces Sale of its Marketing Solutions Business to ActiveProspect (GlobeNewswire, January 8 2026)

- Verisk Announces Sale of its Marketing Solutions Business to ActiveProspect (Verisk Newsroom, January 8 2026)

- ActiveProspect Has Acquired Verisk Marketing Solutions (ActiveProspect blog, January 2026)

- ActiveProspect Rebrands Verisk Marketing Solutions as InfutorData (Infutor.com, March 1 2026)

- WOAH: Huge TCPAWorld News as ActiveProspect Devours Jornaya (Eric Troutman, TCPAWorld, January 8 2026)

- Verisk Acquires Identity Resolution & Consumer Intelligence Leader Infutor (GlobeNewswire, February 24 2022)

- Verisk to Acquire Behavioral Data and Intelligence Leader Jornaya (GlobeNewswire, December 15 2020)

- ActiveProspect Receives Growth Investment From Five Elms Capital (PR Newswire, April 21 2020)

- Insurance Marketing Coalition v. FCC, opinion vacating one-to-one consent rule (U.S. Court of Appeals for the Eleventh Circuit, January 24 2025)

- One-to-One Consent Rule for TCPA Prior Express Written Consent, DOC-408396A1 (Federal Communications Commission, January 2024)

- TrustedForm Pricing (ActiveProspect, accessed April 2026)

- InfutorData – Consumer Insights: Identity, Behavior, Inbound Leads, TCPA Protection (Infutor.com, accessed April 2026)

- Designing a Better Lead Ecosystem for 2026 (ActiveProspect, January 2026)