Native advertising economics differ by vertical in ways that determine which platforms work for which lead types. The aggregated benchmarks operators see in vendor pitch decks are nearly useless until they are decomposed by vertical, platform, and funnel stage.

The Vertical Performance Question in Native Advertising

Native advertising matured into a primary traffic channel for lead generation through the 2020s, offering access to premium publisher audiences at costs substantially below search. According to EMARKETER, U.S. native display ad spending reached approximately $108 billion in 2024, with content recommendation networks (the format most lead generators run) capturing a meaningful share of nonsocial native budget. Taboola, Outbrain, MGID, and Revcontent collectively reach billions of monthly users across thousands of publisher properties, creating scale that rivals the major walled gardens for top-of-funnel reach.

Native ads appear as content recommendations alongside editorial content, reaching users during content consumption rather than during active product search. This positioning captures users earlier in the consideration journey, typically at lower cost than search but requiring different creative approaches and conversion expectations. For lead generators, native represents both a significant cost reduction opportunity and a strategic challenge that demands vertical-specific expertise. Understanding how native-generated leads convert differently requires strong multi-touch attribution to measure true channel value across longer windows than search demands.

Aggregated benchmarks obscure more than they reveal. A “native advertising CPL” tells lead generators almost nothing useful because performance varies dramatically by vertical. Insurance leads on Taboola operate on entirely different economics than personal injury legal leads on Outbrain. Solar leads on MGID convert differently than debt consolidation leads on Revcontent. Platform selection, creative strategy, and performance expectations must reflect these vertical-specific realities, not industry-wide averages that apply to no specific situation.

This analysis compiles vertical-specific performance benchmarks across the major native platforms, examining what CPL ranges to expect, which platforms perform best for which verticals, and how the 2025 Privacy Sandbox shutdown changed the measurement stack. The numbers below are drawn from platform investor disclosures, the WordStream 2024 PPC benchmarks (used as a search comparator), Bloomberg Law mass tort advertising reporting, and operator-reported ranges that should be treated as directional rather than precise. Operators should validate every range against their own A/B test data before committing budget.

Native Advertising Platform Overview

Before examining vertical-specific performance, understanding platform characteristics enables informed interpretation of benchmark data. Each platform has developed distinct positioning, publisher relationships, and advertiser capabilities. These differences affect which verticals perform best on each platform, what optimization approaches work, and what performance to expect.

Taboola Platform Profile

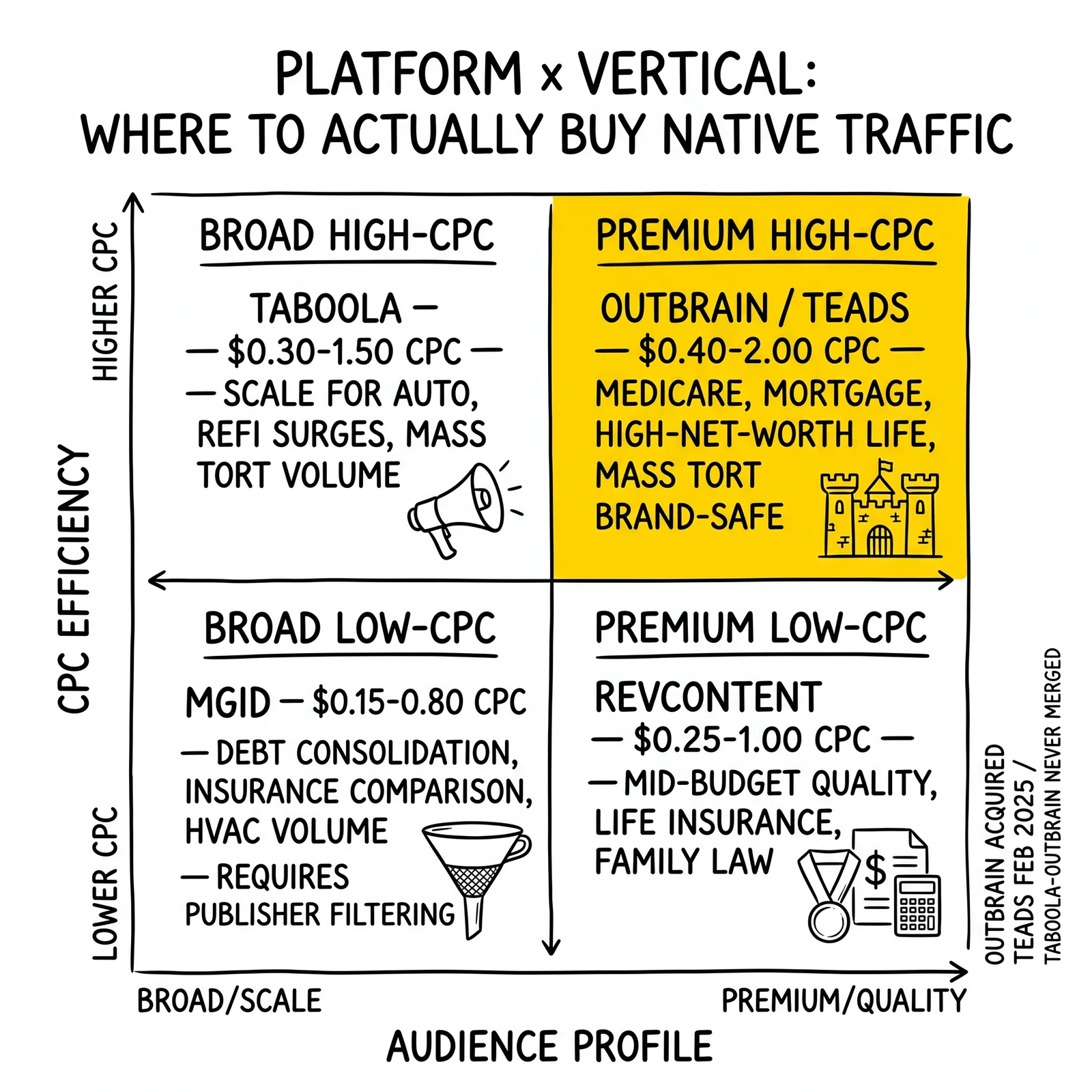

Taboola (NASDAQ: TBLA) operates one of the two largest native advertising networks by reach. The company’s 2025 Investor Day disclosures indicate approximately 600 million daily active users across publishers including NBC News, Yahoo, USA Today, Bloomberg, and Samsung mobile devices. Taboola expects to pay over $1.5 billion to publishers and OEMs in 2025 according to its Realize platform announcement. The platform’s 2024 launch of Realize repositioned the offering from pure native to a broader performance advertising suite addressing what CEO Adam Singolda called a “$55 billion opportunity in performance advertising” beyond search and social.

Targeting options include interest categories across hundreds of taxonomies, demographic targeting (age, gender, income indicators), geographic targeting to state, DMA, and postal code, device and operating system targeting, contextual targeting based on content consumption, first-party data integration for custom audiences, and lookalike modeling from conversion data. Bidding supports CPC (the default), Smart Bid (automated CPA optimization once conversion data accumulates), and Maximize Conversions (fully automated bidding toward conversion goals). Minimum daily budgets typically range from $500 to $1,000 for performance campaigns, with self-serve options at lower thresholds.

Campaign approval typically takes 24-48 hours, with additional review for regulated verticals including financial services, insurance, and healthcare. Creative guidelines prohibit clickbait, misleading claims, and content that violates editorial standards designed to maintain publisher relationships. Operators running aggressive direct response creative regularly bump against these standards and learn the platform’s tolerances through rejected campaigns.

Outbrain Platform Profile

Outbrain pioneered the content recommendation widget and operated as the second-largest network by reach until February 2025, when it closed its $900 million acquisition of Teads and rebranded the combined company under the Teads name. The deal consolidated two of the largest publisher-side advertising networks - the new Teads partners with more than 10,000 publishers and 20,000 advertisers globally according to the Outbrain press release announcing the closing.

This is a critical correction worth flagging because the original 2019 Taboola-Outbrain merger plan, which would have created a combined company valued at over $2 billion, was terminated in September 2020 amid disagreements over revised deal terms during the COVID ad-market downturn. Operators reading older industry coverage frequently encounter the abandoned merger reference and assume Taboola and Outbrain are now combined; they are not, and remain direct competitors with distinct publisher networks.

Outbrain’s 2024 10-K filing reports reach to approximately 2.2 billion consumers globally across 10,000 media environments. U.S. monthly reach historically tracked around 240 million unique visitors per public comScore measurements, though the platform no longer publishes that figure with the same regularity post-Teads consolidation. Publisher partners include CNN, MSN, The Washington Post, and Fox News among premium properties. Outbrain emphasizes publisher quality over raw reach, typically delivering higher-income audiences than broader networks.

Targeting capabilities include interest categories with premium publisher context, demographic overlays, geographic targeting, device targeting, custom audience integration, and Conversion Bid Strategy (CBS) for CPA-optimized bidding. Outbrain maintains stricter editorial standards than some competitors, rejecting headlines with excessive sensationalism or quality concerns - a higher bar that creates a cleaner competitive environment but requires more thoughtful creative development.

MGID Platform Profile

MGID operates a global native advertising platform with strong presence in emerging markets and more permissive content policies than premium platforms. The company’s 2025 advertiser disclosures cite a publisher network spanning over 32,000 sites across 60+ countries, with roughly 185 billion monthly ad impressions and reach across 70+ languages. MGID positions itself for performance-focused advertisers willing to actively manage publisher quality in exchange for lower CPC.

For U.S. lead generation, MGID offers competitive CPCs on a smaller but serviceable publisher network. CPCs typically run 30-50% below Taboola and Outbrain levels. Faster approval cycles (12-24 hours) and more flexible content guidelines enable testing approaches that premium platforms might reject. Publisher quality varies more widely than premium platforms, and not all inventory meets brand safety standards that some advertisers require. Performance requires more hands-on optimization to identify quality placements and exclude underperforming sites - operators routinely whitelist 50-200 publishers and blacklist hundreds more during campaign maturation.

A small clarification on the often-cited “850 million monthly users” figure: MGID’s media kits report 1+ billion unique monthly visitors, with some legacy materials citing 850 million; either figure is closer to a global impression-adjacent metric than a deduplicated U.S. user count. For U.S. lead generation purposes, MGID’s effective addressable audience is materially smaller than Taboola or Outbrain.

Revcontent Platform Profile

Revcontent positions as a premium alternative with strict publisher quality standards, operating a smaller network than Taboola or Outbrain but with higher average publisher quality and engagement. Publisher partners include Newsweek, Weather.com, Sports Illustrated, and Tribune Publishing properties, with monthly content recommendations exceeding 250 billion per the platform’s longstanding public disclosure. The platform focuses primarily on U.S. publishers, creating strong domestic reach without global complexity.

Revcontent often delivers favorable cost per conversion for mid-tier budgets, with fewer competing advertisers per placement than the largest platforms. Strong customer support for mid-market advertisers and ROAS-focused optimization capabilities support performance. The platform’s smaller scale limits maximum reach but creates opportunities for advertisers who value quality over pure volume.

Platform Comparison Summary

| Platform | Reach Disclosure | CPC Range (USD) | Editorial Standards | Best For |

|---|---|---|---|---|

| Taboola | ~600M daily users (Investor Day 2025) | $0.30-$1.50 | Moderate | Scale, broad targeting |

| Outbrain (now Teads) | ~2.2B global consumers (10-K 2024); ~240M U.S. monthly historical | $0.40-$2.00 | Strict | Premium audiences |

| MGID | ~32,000 sites, 185B monthly impressions | $0.15-$0.80 | Flexible | Cost efficiency |

| Revcontent | 250B+ monthly recs (long-standing) | $0.25-$1.00 | Strict | Quality on budget |

Reach figures from each platform’s most recent investor or media kit disclosure. CPC ranges are operator-reported across U.S. lead generation campaigns and should be validated against current auction conditions.

Insurance Vertical Benchmarks

Insurance leads represent one of the strongest performing verticals on native advertising, with CPL savings of 40-60% versus search across most sub-categories. The vertical’s strong native performance reflects demographic alignment and purchase psychology. Many insurance buyers - particularly Medicare and life insurance prospects - spend substantial time consuming news and informational content where native ads appear. The considered nature of insurance purchases means prospects are receptive to educational content that native advertising delivers effectively.

Medicare and Health Insurance Performance

Medicare leads perform exceptionally well on native platforms because the target audience (55+) actively consumes content on sites where native ads appear. News consumption, health information seeking, and general content browsing align with native placement. Performance shows strong seasonality around the Annual Enrollment Period (October 15-December 7) and Open Enrollment Period (January 1-March 31). CPLs during enrollment periods may run 20-40% higher than off-season due to increased competition from Medicare Advantage carriers and FMOs. Operators running Medicare lead generation across AEP and OEP cycles routinely budget for this seasonal compression.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.40-$1.00 | 0.20-0.45% | 4-8% | $18-$38 | Strongest scale, good AEP performance |

| Outbrain | $0.50-$1.20 | 0.25-0.50% | 5-10% | $16-$35 | Higher quality, premium 55+ demo |

| MGID | $0.25-$0.65 | 0.15-0.35% | 3-6% | $15-$32 | Cost efficient, requires filtering |

| Revcontent | $0.35-$0.85 | 0.22-0.48% | 4-9% | $15-$30 | Strong for mid-budget operators |

Operator-reported ranges across U.S. Medicare campaigns 2024-2025. Search comparator: WordStream 2024 benchmarks place Health and Medical Google Ads CPL between $40-$80 for analogous targeting.

Advertorial content performs particularly well for Medicare, with educational content about plan options, enrollment deadlines, and coverage changes driving high engagement from an audience seeking information before decisions. Operators frequently report 80-120% CVR uplift from advertorial intermediation versus direct landing pages.

Auto Insurance Performance

Auto insurance leads on native platforms show more variable performance than Medicare, with success depending heavily on landing page strategy and creative quality.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.35-$0.90 | 0.18-0.40% | 3-7% | $14-$35 | Volume available, CTR-dependent |

| Outbrain | $0.45-$1.10 | 0.22-0.45% | 4-8% | $15-$38 | Premium demo, better targeting |

| MGID | $0.20-$0.55 | 0.12-0.30% | 2-5% | $12-$28 | Requires quality filtering |

| Revcontent | $0.30-$0.75 | 0.20-0.42% | 3-7% | $12-$30 | Solid mid-range option |

Auto insurance native creative benefits from comparison messaging that positions rate shopping as smart consumer behavior. Headlines emphasizing savings percentages or new discount programs capture attention in content environments. State-specific targeting enables geographic optimization matching buyer requirements, though narrower targeting typically increases CPC. National campaigns run cheaper per click but may generate leads in states without buyer coverage - a routing problem operators solve with vertical-specific waterfall logic rather than broader targeting.

Life Insurance Performance

Life insurance shows moderate native performance, with lead quality often stronger than search-generated leads due to the educational journey native supports.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.45-$1.20 | 0.15-0.35% | 3-6% | $22-$50 | Education-driven, longer CTAs |

| Outbrain | $0.55-$1.40 | 0.18-0.40% | 4-7% | $25-$55 | Premium audiences, higher policy value |

| MGID | $0.28-$0.70 | 0.10-0.28% | 2-5% | $18-$40 | Cost efficient, lower quality mix |

| Revcontent | $0.38-$0.95 | 0.16-0.38% | 3-6% | $20-$45 | Balanced performance |

Life insurance native advertising works well for final expense targeting (senior demographic heavily represented on news sites) and term life for young families (parenting and family content contextual targeting). Conversion timelines for life insurance leads from native sources tend to be longer than search leads because prospects enter the funnel during research phases and require nurturing. Advertisers expecting immediate conversions undervalue native life insurance leads. The framework for insurance lead nurturing and converting cold leads addresses how native funnel-entry leads should be worked over 30-90 day windows rather than the 7-day search-style cadence.

Home Insurance Performance

Home insurance leads show variable native performance depending on targeting approach and seasonal factors.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.40-$1.00 | 0.18-0.38% | 3-6% | $18-$42 | Event-driven spikes (disasters) |

| Outbrain | $0.50-$1.20 | 0.20-0.42% | 4-7% | $20-$48 | Premium homeowner demo |

| MGID | $0.25-$0.60 | 0.12-0.30% | 2-5% | $15-$35 | Volume available, mixed quality |

| Revcontent | $0.35-$0.85 | 0.18-0.40% | 3-6% | $16-$38 | Consistent performer |

Home insurance native advertising sees demand spikes following weather events, natural disasters, and news about coverage issues. Contextual targeting around home improvement content reaches homeowners actively thinking about property. Operators in hurricane-exposed states report 2-3x CTR uplift in the 14-day window following named storms.

Financial Services Vertical Benchmarks

Financial services verticals show strong native performance for mortgage, refinance, and debt products, with savings versus search often exceeding 50%. The vertical benefits from native advertising’s ability to reach prospects during research phases that precede active product search. Homeowners considering refinance, consumers researching debt consolidation options, and prospective homebuyers all engage with financial content before they begin actively comparing specific product offers.

Mortgage and Refinance Performance

Mortgage leads on native platforms deliver substantial CPL savings versus search, with advertorial content particularly effective for rate-conscious consumers.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.50-$1.40 | 0.20-0.45% | 3-6% | $22-$60 | Rate environment sensitive |

| Outbrain | $0.60-$1.60 | 0.25-0.50% | 4-7% | $25-$65 | Premium homeowner demo |

| MGID | $0.30-$0.80 | 0.14-0.32% | 2-5% | $18-$48 | Cost efficient option |

| Revcontent | $0.42-$1.10 | 0.22-0.46% | 3-6% | $20-$52 | Balanced performance |

Operator-reported. WordStream 2024 search comparator places Finance Google Ads CPL at $60-$200 depending on sub-vertical.

Mortgage native advertising performs differently across rate environments. During rate declines, refinance messaging drives surge demand and increased competition. During elevated rates, cash-out refinance and purchase messaging maintain relevance with different headline framing. Purchase mortgage leads from native sources tend toward earlier funnel stages than search leads because prospects researching home buying encounter native content months before active purchase search. Lead nurturing capability affects conversion from these earlier-stage leads.

Debt Consolidation and Personal Loans

Debt-related products show strong native performance because the content-driven approach resonates with borrowers seeking information rather than immediate action.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.38-$0.95 | 0.22-0.48% | 4-8% | $14-$35 | Strong debt consolidation |

| Outbrain | $0.48-$1.15 | 0.26-0.52% | 5-9% | $16-$38 | Higher credit profile |

| MGID | $0.22-$0.55 | 0.15-0.38% | 3-6% | $12-$28 | Volume available |

| Revcontent | $0.32-$0.78 | 0.20-0.46% | 4-8% | $13-$32 | Consistent performer |

Debt consolidation messaging on native platforms benefits from educational framing that explains options without judgment. Content addressing “how to consolidate debt” or “debt relief options explained” captures searchers earlier than direct response advertising. Credit quality from native debt leads varies by platform and placement: premium platforms (Outbrain, Revcontent) tend toward higher credit profiles; broader platforms include more subprime prospects. Lenders running tiered offers should match platform mix to credit tier targeting.

Credit Card and Banking

Credit card and banking products show moderate native performance, with results depending heavily on offer specifics and creative quality.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.35-$0.85 | 0.18-0.38% | 2-5% | $18-$40 | Offer-dependent |

| Outbrain | $0.45-$1.05 | 0.22-0.42% | 3-6% | $20-$45 | Premium card seekers |

| MGID | $0.20-$0.50 | 0.12-0.28% | 2-4% | $14-$32 | High volume, low quality |

| Revcontent | $0.30-$0.72 | 0.16-0.36% | 2-5% | $16-$36 | Mid-range option |

Credit card native advertising requires compelling offers - rewards programs, sign-up bonuses, or introductory rates drive engagement. Generic card offers underperform dramatically.

Legal Vertical Benchmarks

Legal lead generation shows substantial CPL savings on native platforms versus search, though conversion rates require patience given longer legal sales cycles. The vertical presents unique characteristics for native advertising: legal matters often emerge suddenly - an accident, a diagnosis, a workplace issue - creating prospects who need education about their options before they can effectively search for representation. Native advertising reaches these newly-emerged prospects during the content consumption that often accompanies difficult circumstances.

Personal Injury Performance

Personal injury leads from native sources show variable performance based on case type, geography, and creative approach.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.80-$2.20 | 0.15-0.32% | 2-4% | $120-$320 | Volume for mass tort |

| Outbrain | $1.00-$2.60 | 0.18-0.36% | 3-5% | $130-$350 | Higher case value leads |

| MGID | $0.45-$1.20 | 0.10-0.25% | 1-3% | $90-$220 | Cost efficient, mixed quality |

| Revcontent | $0.65-$1.70 | 0.14-0.30% | 2-4% | $100-$280 | Balanced option |

Operator-reported. WordStream 2024 search comparator: Attorneys & Legal Services Google Ads CPC averaged $8.94, with mass tort and personal injury keywords routinely $50-$200+ per click.

General personal injury (auto accidents, slip and fall) shows less dramatic native advantage over search because the immediate need drives search behavior that native’s discovery format cannot capture as effectively. The native advantage concentrates in mass tort campaigns where specific conditions can be targeted contextually.

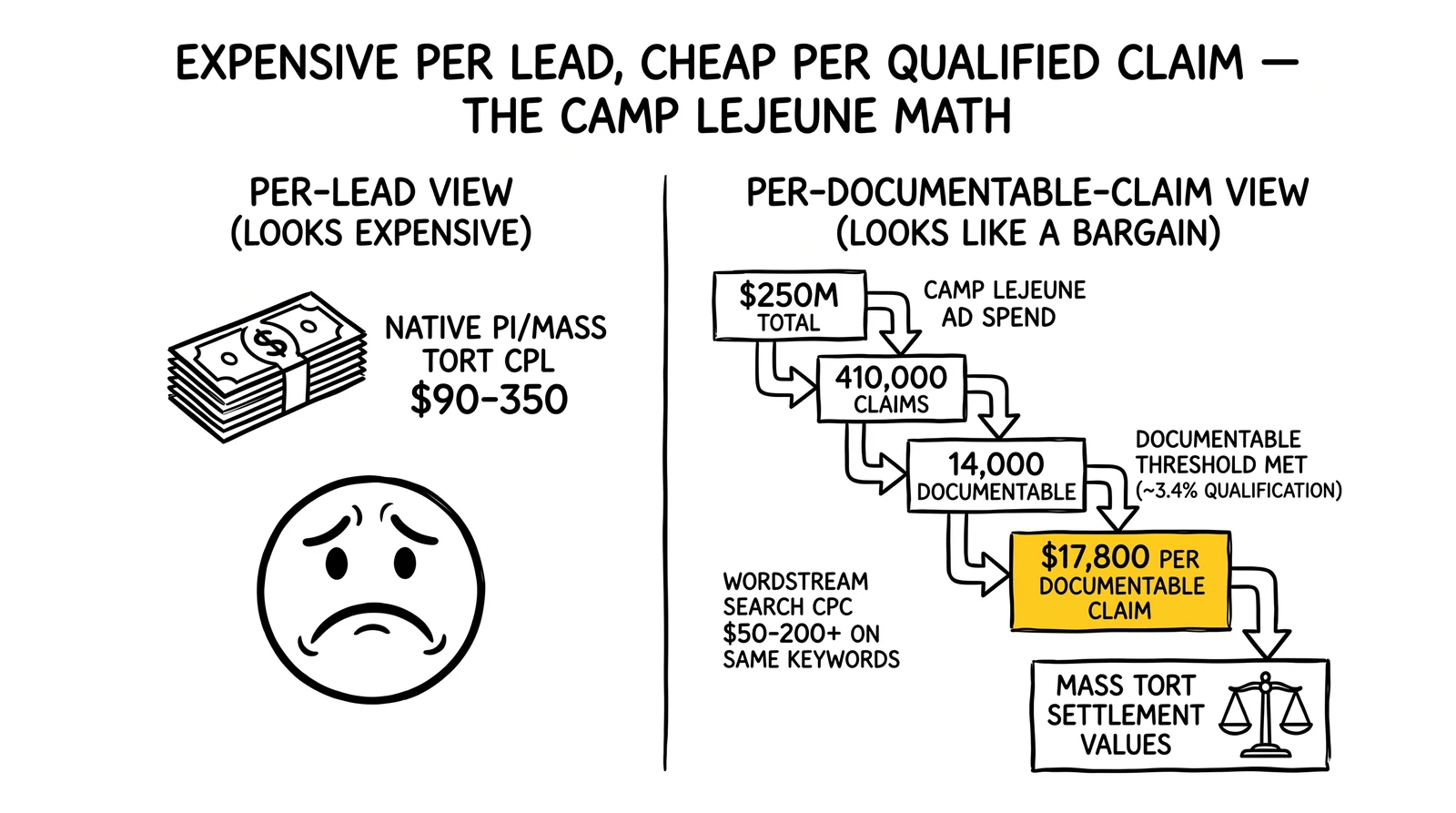

Mass Tort Campaign Performance – Camp Lejeune Case Study

Mass tort campaigns represent a native advertising strength, with content-driven discovery matching how affected populations learn about potential claims. The Camp Lejeune Justice Act campaign provides the clearest recent reference: Bloomberg Law reported the mass tort marketing industry spent approximately $250 million on Camp Lejeune advertising by 2023, generating roughly 410,000 claims of which only about 14,000 met initial documentation thresholds. That works out to approximately $17,800 per documentable claim in advertising spend alone - a number that reframes “expensive” mass tort CPLs as bargains relative to the qualified-claim economics.

Camp Lejeune campaigns ran heavily on native placements adjacent to military, veterans affairs, and health content. Geographic targeting concentrated around Marine Corps bases (Lejeune itself in North Carolina, plus secondary exposure populations near Quantico and Pendleton) and around states with high Marine veteran populations. Headlines tested variations on “Diagnosed with [condition] after serving at Camp Lejeune?” and “Marines exposed to Camp Lejeune water may qualify for compensation.” Native advertising delivered this discovery at scale to populations that would not have searched for legal representation absent the prompt.

The 3M Combat Arms Earplug litigation followed a similar pattern but with different geographic concentration - native campaigns targeted Army post adjacencies and ran across health and military content. AFFF (firefighting foam) exposure campaigns concentrated around airports, military airfields, and industrial sites with documented contamination. The pattern across mass tort native is consistent: contextual placement plus geographic targeting plus medical-condition-driven headlines outperforms broad demographic targeting by significant margins.

Family Law and Estate Planning

Family law and estate planning leads show moderate native performance, with educational content driving engagement.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.50-$1.30 | 0.14-0.30% | 2-4% | $35-$90 | Life event targeting |

| Outbrain | $0.60-$1.50 | 0.16-0.34% | 3-5% | $38-$95 | Premium demographic |

| MGID | $0.30-$0.75 | 0.10-0.24% | 1-3% | $28-$70 | Cost efficient |

| Revcontent | $0.42-$1.05 | 0.13-0.28% | 2-4% | $32-$80 | Balanced performance |

Family law native advertising often targets life event signals - content around divorce, custody, or separation reaches audiences actively experiencing situations requiring legal guidance. Estate planning native targets demographic signals (55+) and contextual placement on retirement, financial planning, and health content where estate considerations become relevant.

Home Services Vertical Benchmarks

Home services lead generation on native platforms shows strong performance for high-consideration projects like solar and roofing, with more variable results for lower-ticket services. High-ticket improvements like solar panels, roofing, and window replacement involve extended research phases where native excels. Homeowners spend months considering these projects, consuming related content, and evaluating options before committing. Lower-ticket services with shorter consideration windows show less dramatic native performance advantages because the compressed timeline limits content-driven nurturing opportunity.

Solar Lead Performance

Solar leads represent a native advertising strength, with CPL savings of 55-70% versus search common for well-optimized campaigns.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.55-$1.40 | 0.22-0.48% | 4-8% | $25-$65 | Strong scale available |

| Outbrain | $0.65-$1.60 | 0.26-0.52% | 5-9% | $28-$70 | Premium homeowner demo |

| MGID | $0.32-$0.80 | 0.15-0.35% | 3-6% | $20-$50 | Cost efficient option |

| Revcontent | $0.45-$1.15 | 0.20-0.45% | 4-8% | $22-$55 | Consistent performer |

Operator-reported across U.S. residential solar campaigns 2024-2025. The full solar lead generation complete guide addresses CAC economics in depth - Sunrun, the largest residential solar installer, reports total CAC in the $3,000-$6,000 range, which contextualizes the per-lead native CPL within full-funnel economics.

Solar native advertising benefits from the extended research timeline solar purchases require. Tax credit and incentive messaging performs strongly - federal Investment Tax Credit headlines, state incentive programs, and utility rebates capture attention from cost-conscious homeowners. Policy change content (tax credit extensions, utility rate increases) provides timely hooks. Geographic targeting matters significantly: Sun Belt states with high solar potential and supportive policies generate different economics than northern states with shorter solar seasons and less aggressive incentive structures.

Roofing Lead Performance

Roofing leads show solid native performance, particularly for storm damage and scheduled replacement campaigns.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.45-$1.15 | 0.18-0.40% | 3-6% | $22-$55 | Event-driven spikes |

| Outbrain | $0.55-$1.35 | 0.22-0.45% | 4-7% | $25-$60 | Premium homeowner demo |

| MGID | $0.28-$0.70 | 0.12-0.30% | 2-5% | $18-$42 | Volume available |

| Revcontent | $0.38-$0.95 | 0.16-0.38% | 3-6% | $20-$48 | Balanced option |

Roofing native shows geographic and seasonal patterns. Storm-affected regions see demand spikes that native can capture with timely creative addressing hail damage, wind damage, or storm response. Seasonal replacement campaigns (spring preparation, fall winterization) provide recurring timing hooks. Operators with pre-built creative libraries for hail and wind events capture demand windows that competitors take days to respond to.

HVAC and Windows Performance

HVAC and window leads show moderate native performance, with results improving for higher-ticket projects and premium positioning.

| Platform | CPC Range | CTR Range | CVR Range | CPL Range | Notes |

|---|---|---|---|---|---|

| Taboola | $0.40-$1.00 | 0.16-0.36% | 2-5% | $22-$58 | Seasonal patterns |

| Outbrain | $0.50-$1.20 | 0.20-0.40% | 3-6% | $25-$62 | Premium segments |

| MGID | $0.25-$0.62 | 0.10-0.26% | 2-4% | $18-$45 | Cost efficient |

| Revcontent | $0.35-$0.85 | 0.14-0.32% | 2-5% | $20-$50 | Balanced option |

HVAC native aligns with seasonal demand patterns - heating campaigns in fall and winter, cooling campaigns in spring and summer. Energy efficiency messaging resonates in contexts of rising utility costs or extreme weather coverage. Window replacement native benefits from energy efficiency positioning and home improvement contextual placement, with tax credit and rebate messaging driving engagement from cost-conscious homeowners.

Privacy Sandbox Shutdown and the Server-Side Migration

The native advertising measurement stack changed materially in late 2025 and early 2026. Google announced the deprecation of the Topics API and most other Privacy Sandbox advertising technologies in October 2025, with formal removal scheduled across Chrome 144 through 150 builds. The shutdown abandoned years of industry preparation for cookieless targeting after the APIs failed to gain meaningful adoption. The UK Competition and Markets Authority found that publisher revenue declined approximately 30% when using Privacy Sandbox tools instead of third-party cookies, per AdExchanger reporting on the CMA’s June 2025 findings.

The practical effect on native advertising is more modest than on programmatic display. Taboola, Outbrain, and MGID always relied primarily on contextual signals and publisher-side data rather than third-party cookies for targeting and bidding. The networks’ core mechanism - matching ads to publisher content context - was never cookie-dependent in the way that retargeting and lookalike modeling were on social platforms. Chrome retained third-party cookies under user-choice flags, so existing measurement pipelines continued to function, though with degrading signal as users exercise privacy preferences.

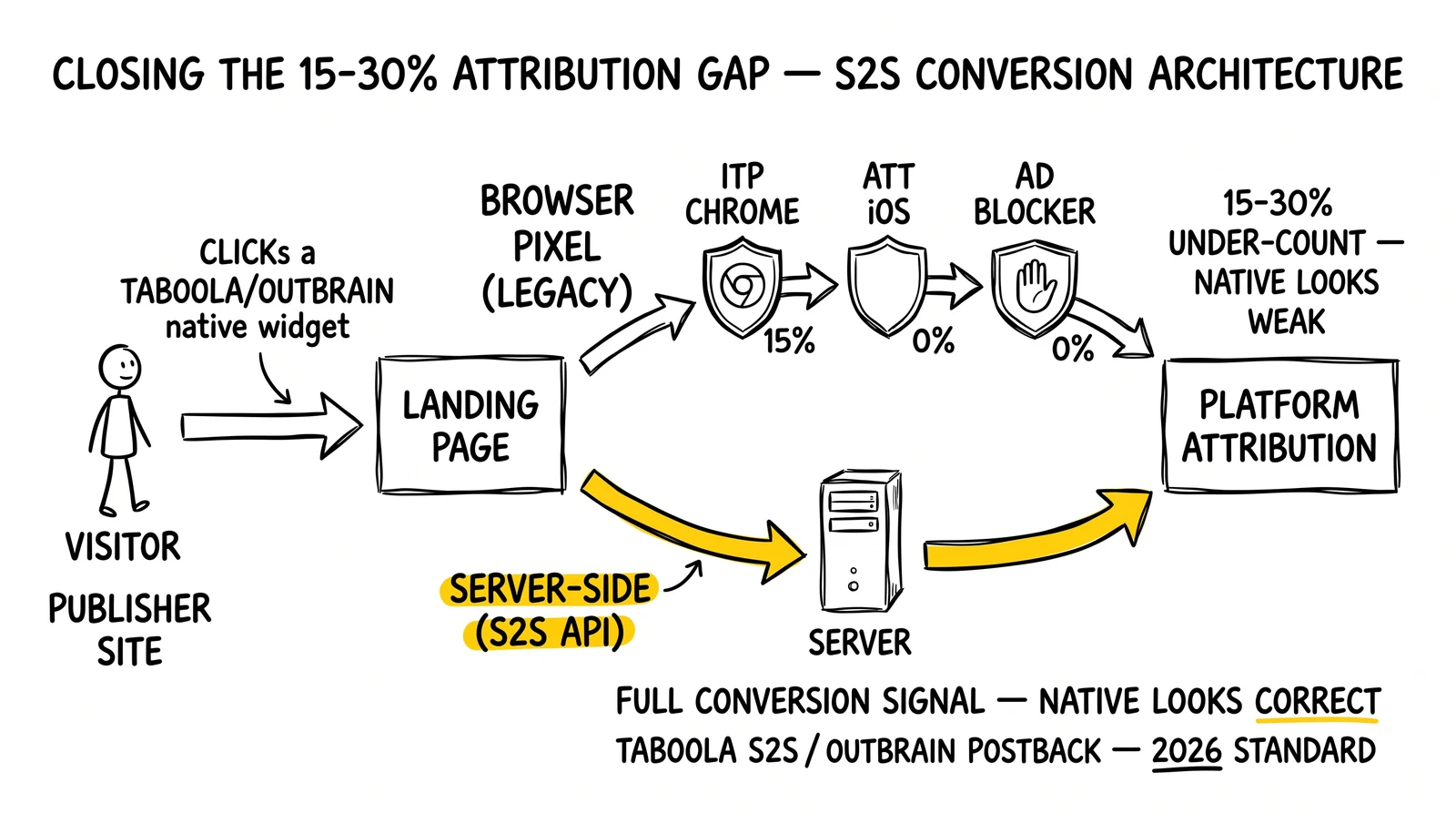

The bigger 2026 shift is the migration to server-to-server conversion APIs. Taboola’s S2S endpoint and Outbrain’s server postback infrastructure now constitute the primary recommended conversion tracking mechanism for both platforms. Operators running native without server-side conversion tracking are reporting 15-30% under-attribution versus their actual conversion volume - a measurement gap that systematically undervalues native versus search in attribution comparisons.

For lead generators, the practical 2026 takeaway is straightforward. Server-side conversion tracking is no longer optional. Operators running Facebook CAPI for cross-channel server-side tracking should extend the same architecture to Taboola and Outbrain conversion endpoints. Contextual targeting deserves more campaign-level attention than it received in the cookie-rich era - native platforms reward content-context matching with lower CPCs and stronger CVR. And the death of third-party cookies and its lead generation impact reframes channel attribution: native, which always under-attributed in last-click models, looks materially stronger in marketing mix and incrementality frameworks.

Platform Selection by Vertical

Vertical-specific performance patterns suggest platform selection strategies that optimize for each lead type rather than defaulting to single-platform habits.

Insurance Platform Recommendations

For Medicare and health insurance, Outbrain’s premium publisher network delivers the target demographic (55+) with higher income profiles and clearer intent. Taboola provides scale for volume targets. Revcontent offers balanced performance for mid-tier budgets. For auto insurance, Taboola’s scale enables testing at volume to identify winning combinations; MGID’s cost efficiency works for operators with strong quality filtering; Outbrain’s premium demo supports higher-value policy targeting. For life insurance, Outbrain’s premium audiences align with higher policy value segments; Taboola provides scale for final expense targeting; Revcontent delivers consistent mid-range performance.

Financial Services Platform Recommendations

For mortgage leads, Outbrain’s homeowner demographic concentration provides efficient targeting; Taboola offers scale during refinance surges; MGID delivers cost efficiency for rate-sensitive operations. For debt consolidation, Taboola’s scale enables high-volume testing; MGID’s cost efficiency supports aggressive CPL targets; Outbrain’s premium audiences deliver higher credit profiles.

Legal Platform Recommendations

For mass tort campaigns, Taboola’s scale reaches affected populations at volume; MGID’s cost efficiency extends campaign reach; Outbrain’s premium placement provides brand-safe positioning for sensitive case types where law firm reputation is exposed. For personal injury, performance varies by case type - auto accident leads typically favor search over native because of immediate intent; medical malpractice and product liability benefit from native’s educational approach.

Home Services Platform Recommendations

For solar leads, all platforms perform with proper optimization - Outbrain delivers premium homeowner demographics, Taboola provides scale, MGID offers cost efficiency, Revcontent balances quality and cost. For roofing, Taboola’s scale enables rapid response to storm events; geographic and temporal flexibility matters for weather-driven demand. HVAC and window campaigns split similarly across platforms with seasonal calibration.

Cross-Vertical Optimization Strategies

Certain optimization strategies apply across verticals while requiring vertical-specific calibration.

Creative Testing by Vertical

Headline testing intensity should reflect vertical competition. High-competition verticals (insurance, mortgage) require continuous creative refresh - 8-12 active headlines with weekly rotation of the bottom quartile. Lower-competition verticals can sustain winning creatives longer. Image selection patterns differ by vertical: insurance responds to human faces conveying security or relief; financial services benefits from aspirational lifestyle imagery; legal requires careful balance between approachability and authority; home services performs with before-after or project completion imagery. Creative fatigue timelines vary by reach: verticals targeting broad audiences (auto insurance) experience faster fatigue than narrow verticals (mass tort) due to higher impression frequency among target populations.

Landing Page Optimization by Vertical

Advertorial length should match vertical consideration timeline. High-consideration purchases (solar, mortgage) support longer advertorials (1,200-1,800 words). Lower-consideration products (insurance quotes) can use shorter formats (600-900 words). Form placement and progressive disclosure vary by vertical: complex verticals benefit from multi-step forms that educate while qualifying; simpler verticals can use shorter forms with fewer friction points. Trust signals require vertical-specific calibration: insurance emphasizes carrier relationships and coverage specifics; financial services requires rate disclosures and lender identification; legal needs attorney advertising compliance and case type clarity.

Geographic Optimization by Vertical

Geographic targeting granularity should match vertical economics. National insurance campaigns can run broadly with buyer routing handling distribution. Local service verticals (roofing, HVAC) require tighter geographic targeting matching service areas. Regional performance variations create optimization opportunity: coastal markets perform differently than inland markets for home services; state regulatory environments affect insurance and legal performance; climate patterns influence solar and HVAC demand. Mass tort campaigns warrant explicit ZIP-level targeting around exposure sites.

Platform Budget Allocation by Vertical

Multi-platform strategies should reflect vertical-specific platform strengths. Insurance budgets might weight toward Outbrain for Medicare (premium 55+ demo) and Taboola for auto (scale). Financial services might concentrate on Outbrain (homeowner demo) with MGID for cost efficiency testing. Testing allocation should provide sufficient volume for statistical significance on each platform - typically $2,000-5,000 minimum per platform before making allocation decisions based on performance data. Operators who allocate $500 across each platform and conclude the platforms don’t work are reading noise, not signal.

Key Takeaways

-

Native advertising performance varies dramatically by vertical, making aggregated benchmarks unusable for specific campaign planning. Insurance leads show 40-60% CPL savings versus search; financial services 55-70% for mortgage and debt; legal 50-60% with mass tort representing native’s strongest case; home services 60-70% for solar.

-

Outbrain and Taboola did not merge. The original 2019 merger was terminated in September 2020. Outbrain’s actual 2024 transaction was the Teads acquisition, which closed February 3, 2025 for $900 million. Outbrain now operates under the Teads brand. Operators running campaigns based on the false assumption of a combined Taboola-Outbrain entity should correct their platform mental model.

-

Platform selection should reflect vertical-specific strengths rather than habit. Outbrain (now Teads) delivers superior demographics for Medicare, mortgage, and high-net-worth segments. Taboola enables volume testing and broad reach. MGID supports aggressive CPL targets for verticals with strong downstream qualification. Revcontent balances quality and cost for mid-market operations.

-

Advertorial content outperforms direct landing pages across nearly all lead generation verticals. The advantage is most pronounced for high-consideration purchases where native captures research-phase users. Advertorial length should match consideration timeline - longer for complex decisions, shorter for simpler products.

-

Mass tort native economics reframe expensive CPLs as bargains. Camp Lejeune campaigns spent approximately $250 million in advertising to generate 410,000 claims, of which 14,000 met documentation thresholds - $17,800 per documentable claim per Bloomberg Law. Operators evaluating mass tort native CPLs in isolation miss the qualified-claim economics that justify the channel.

-

Seasonal patterns significantly affect performance and should inform budget allocation. Medicare spikes during AEP and OEP. Solar peaks in spring and summer. Storm damage creates roofing spikes. Tax season affects financial services. Flat budgets across variable seasons leave material lead volume on the table.

-

Server-side conversion tracking is no longer optional. Operators running native without S2S conversion endpoints under-report conversions by 15-30% versus actual volume, systematically undervaluing native versus search in last-click attribution. Taboola’s Conversions API and Outbrain’s server postback are the 2026 standard.

-

Privacy Sandbox shutdown affected native less than programmatic. Native always relied primarily on contextual signals and publisher-side data, not third-party cookies. The bigger shift is the contextual targeting renaissance - content-context matching now deserves campaign-level attention, not just default settings.

-

Quality measurement must extend beyond CPL to downstream conversion. Native advertising captures earlier-funnel users who show lower 7-day conversion but stronger 60-day conversion than search. Tracking across 60-90 day windows reveals true performance differences that first-week analysis obscures.

-

Multi-platform strategies enable optimization across platform strengths. Most successful native operations run two or more platforms simultaneously, allocating budget based on vertical-specific performance data. Single-platform dependency creates auction-cost exposure that platform diversification mitigates.

Sources

- Outbrain Inc., “Form 10-K Annual Report for Fiscal Year 2024,” U.S. Securities and Exchange Commission, March 2025. SEC filing

- Outbrain Inc., “Outbrain Completes the Acquisition of Teads,” GlobeNewswire press release, February 3, 2025. Press release

- Taboola, “Taboola Investor Day 2025 Recap,” Taboola corporate communications, March 2025. Investor Day

- Ingrid Lunden, “Taboola and Outbrain Call Off Their $850M Merger,” TechCrunch, September 8, 2020. TechCrunch coverage

- EMARKETER (formerly Insider Intelligence), “How Native Advertising Works: Ad Types, Benefits to Marketers, and Recent Data,” EMARKETER Industry KPIs, 2024. EMARKETER native ad spending

- WordStream, “Google Ads Benchmarks 2024: New Trends & Insights for Key Industries,” WordStream Research, May 2024. WordStream 2024 benchmarks

- Allison Schiff, “Google Pulls the Plug on Topics, PAAPI and Other Major Privacy Sandbox APIs (As The CMA Says ‘Cheerio’),” AdExchanger, October 2025. AdExchanger Privacy Sandbox

- Roy Strom, “Camp Lejeune Ads Surge Amid ‘Wild West’ of Legal Finance, Tech,” Bloomberg Law, 2023. Bloomberg Law mass tort

- U.S. Federal Trade Commission, “Native Advertising: A Guide for Businesses,” FTC Business Guidance, updated 2023. FTC native ad guide

- MGID, “MGID for Advertisers: Global Native Advertising Platform,” MGID corporate disclosures, 2025. MGID advertisers

Closing

The companies winning native advertising in 2026 are not the operators with the deepest budgets or the most sophisticated agency partners. They are the operators who treat the channel with the vertical specificity it demands, who refuse to read aggregated benchmarks as actionable, and who built server-side conversion infrastructure before the measurement stack started failing them. Outbrain’s transition to Teads, Taboola’s pivot toward the broader Realize platform, and the Privacy Sandbox shutdown all point toward a market that rewards operational discipline over campaign volume. The vertical CPL ranges in this analysis are starting points, not endpoints - the operators who validate them through structured testing, calibrate platform mix to their vertical economics, and integrate native into multi-touch attribution frameworks will compound advantages that single-channel competitors cannot reach.

Performance benchmarks current as of April 2026 and reflect operator-reported ranges across U.S. lead generation campaigns 2024-2025 plus platform investor disclosures. Native advertising performance varies based on platform algorithm changes, competitive dynamics, and market conditions. Validate current benchmarks through structured A/B testing before major budget commitments.