The reprieve is real. The relief is conditional. The math has changed but not in the direction most operators read it.

What Order DA 26-12 Actually Did

On January 6, 2026, the Consumer and Governmental Affairs Bureau of the Federal Communications Commission released Order DA 26-12, extending the effective date of the portion of 47 C.F.R. § 64.1200(a)(10) commonly called the “revoke-all” or “global revocation” provision. The new compliance deadline is January 31, 2027 – moved from April 11, 2026, which had itself been moved from April 11, 2025. The Bureau cited “good cause” tied to implementation complexity and the agency’s pending Further Notice of Proposed Rulemaking, released October 29, 2025, asking whether the rule should be modified or eliminated entirely.

The headline reads as relief. The fine print does not. Only one provision moved. Single-topic revocation, the seven-business-day implementation window, and the rule treating opt-outs from exempted informational calls as full opt-outs all remain effective today. The portion that requires a single revocation request to cut across unrelated topics from the same caller – the operational nightmare for multi-brand and multi-product operators – is the only piece that slid to 2027.

That distinction matters because it changes the calculus of the build decision. An operator who reads the press cycle as “the rule was delayed” will under-prepare for parts of the rule that are fully enforceable now. An operator who reads it as “the FCC is killing the rule” will skip the strategic positioning work that distinguishes companies that thrive when regulations land from those that scramble. Neither read survives contact with the specific legal text.

This article walks the strategic decision facing operators in April 2026. It assumes readers understand the rule’s basic mechanics – those are covered separately in the site’s analysis of the global revocation rule and § 64.1200(a)(10). The focus here is the build-vs-wait math: when to invest, how much, what to build, what to instrument, and how to read the political signals between now and the deadline.

The Reprieve and What It Actually Changes

The January 6 order is narrow by design. The Bureau did not vacate the rule, did not stay enforcement of any other provision, and did not signal a change in the underlying policy direction. It granted breathing room to a specific class of stakeholders – primarily financial services and healthcare providers – who argued that cross-system integration across multi-bank holding companies and multi-facility hospital networks was operationally impossible on the original schedule.

For lead operators, the practical effects of the extension fall into three categories. The first is that single-topic suppression is fully effective and aggressively litigated. Plaintiff firms have been filing on the broader 47 C.F.R. § 64.1200(a)(10) since April 2025 – the seven-business-day window, the requirement to honor revocation made through “any reasonable means,” and the prohibition on requiring specific opt-out language. These are the highest-volume claim theories in the post-April-2025 docket and operators who treated the entire rule as delayed misunderstood the scope of the extension.

The second effect is that the deadline pressure for cross-business-unit infrastructure shifted from quarters to four full quarters away. April 2026 was a sprint deadline; January 2027 permits a build cycle. That changes which vendor approaches are feasible, which budgets fit in fiscal 2026 versus fiscal 2027 plans, and how much an operator can afford to wait on the FNPRM outcome before committing to architecture.

The third effect – and the one most operators are misreading – is that the second extension itself is a signal. The FCC has now extended a single rule provision twice over twenty months. That pattern reflects either an agency genuinely conflicted about the rule’s design or an agency telegraphing future modification. Combined with the October 29 FNPRM and Chairman Carr’s “Delete, Delete, Delete” deregulation initiative, the directional read is clear: the rule that takes effect on January 31, 2027 will not be the rule as written in October 2024. The question is how much of it survives, and that question is the one operators are pricing.

A reasonable base case from the comment record and FNPRM language: the broad cross-topic application survives in some form, narrowed to exclude exempted informational calls (fraud alerts, security breaches, healthcare reminders), with operators permitted to designate “exclusive means” of revocation rather than honoring all reasonable methods. A bull case for operators: the cross-topic application is dropped entirely, leaving single-topic revocation as the only enforceable rule. A bear case: the rule lands as written with a hard January 31 cliff and no further extensions.

The Rule Itself: Multi-Topic Suppression Mechanics

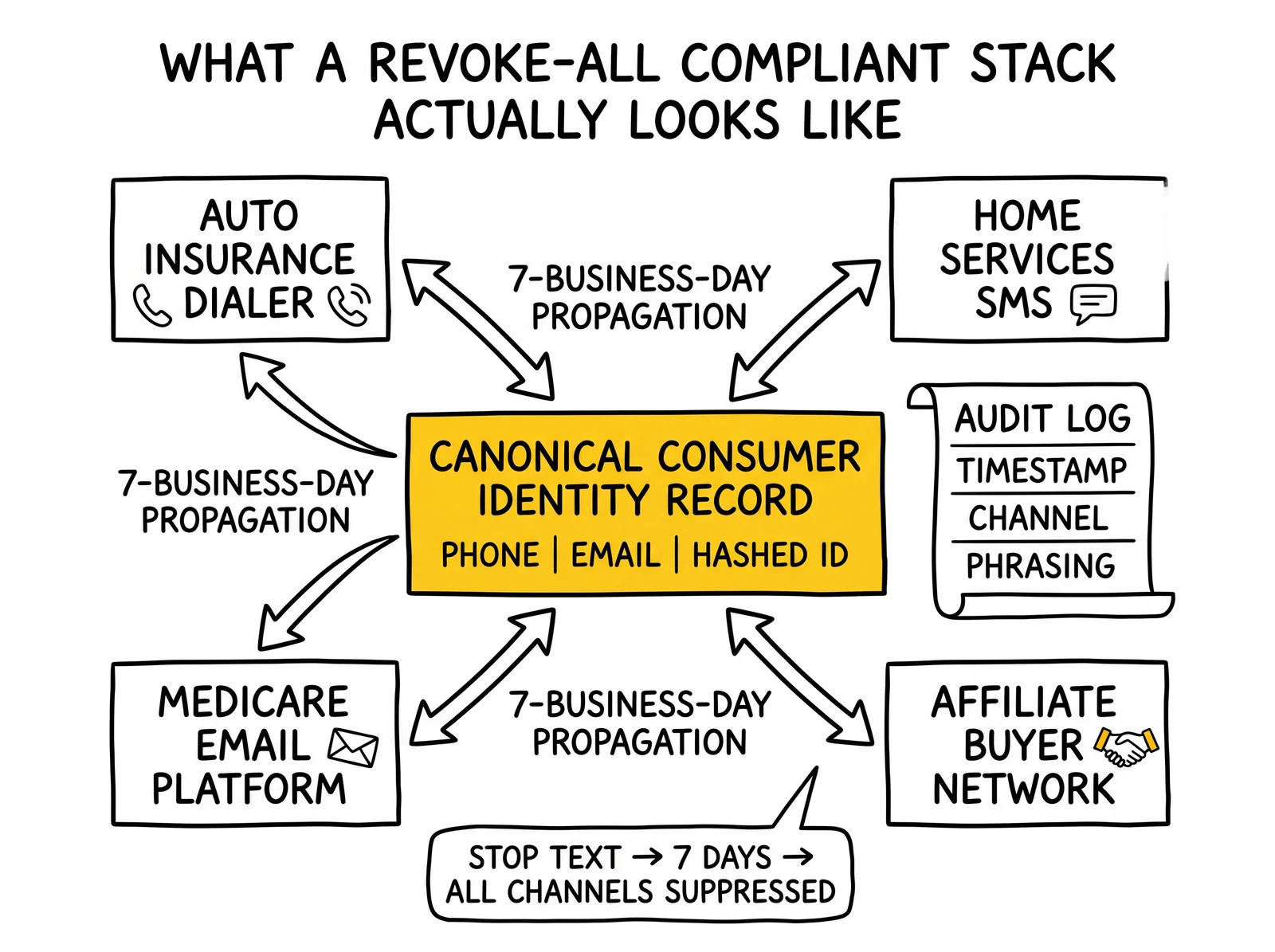

The revoke-all provision sounds simple. A consumer who opts out of one type of call from a caller is opting out of all calls from that caller on unrelated topics. The mechanical reality is that most lead operators are not architected to honor that opt-out at scale.

A typical multi-brand lead operation runs three to seven contact systems that do not share identity natively. The auto insurance dialer pulls leads from one CRM. The home services SMS platform sends from a different vendor. The Medicare email platform syncs to a marketing automation tool that does not natively connect to either. Each system has its own opt-out list, each list is keyed differently – phone-only, email-only, hashed identifier – and propagation between systems happens, when it happens, through nightly batch jobs measured in days rather than the seven-business-day window the rule requires.

The rule’s mechanical demand is that when a consumer texts “STOP” to the auto insurance SMS line, the home services dialer must know within seven business days, the Medicare email platform must know within seven business days, and any third-party affiliate calling on behalf of any of those brands must also know. The text of § 64.1200(a)(10) does not say “if technically feasible.” It says revocation is effective and the caller must implement it. The seven-day clock starts at receipt, not at the next batch job.

The technical architecture this requires is a single canonical identity record per consumer, federated across business units, with a real-time propagation trigger. In practice that means one of three patterns: a customer data platform that sits as the system of record for consent; an enterprise consent management platform (Salesforce Marketing Cloud’s Consent Data Model, OneTrust, Didomi, or similar) wired to every outbound system; or a custom integration layer that reconciles identity on each outbound call. Each pattern carries different costs, different vendor dependencies, and different ceilings on how messy the underlying systems can be while still complying.

The audit dimension compounds the complexity. Compliance is not just about not making the call – it is about being able to prove, in litigation, that the call was not made and that the suppression was effective. That requires immutable logs of opt-out timestamps, opt-out source channels, opt-out propagation timestamps to each downstream system, and the contact lookup that confirmed suppression at call time. Without those logs, a plaintiff firm’s discovery request – phone records that suggest a call to a number on a suppression list – becomes a settlement event rather than a defense.

Operators who already maintain rigorous consent documentation and retention practices have most of the audit infrastructure in place. Operators who treat consent receipts as a check-the-box artifact rather than an evidentiary record start the build from a deficit.

The Affiliate Flow-Down Problem

The dimension most operators underestimate is vendor flow-down. The rule applies to the “caller” – defined broadly enough to include the entity on whose behalf calls are made. A lead generator who sells to twenty buyers and whose buyers’ affiliates dial those leads has a flow-down obligation that runs through every contractual layer. If a consumer revokes consent through the lead generator’s web form, that revocation has to reach every buyer who received that lead, and every buyer’s affiliate calling on the lead, within the seven-day window.

That obligation is operationalized through suppression list APIs, contractual flow-down clauses, and ongoing audit. Most lead operations have the contractual clauses in place. Few have the API plumbing wired to push suppressions in real time, and fewer still have an audit mechanism to prove the suppression actually reached the dialer that made the call. The article on vendor TCPA liability and third-party exposure covers the legal contours; the operational gap is what closes the build.

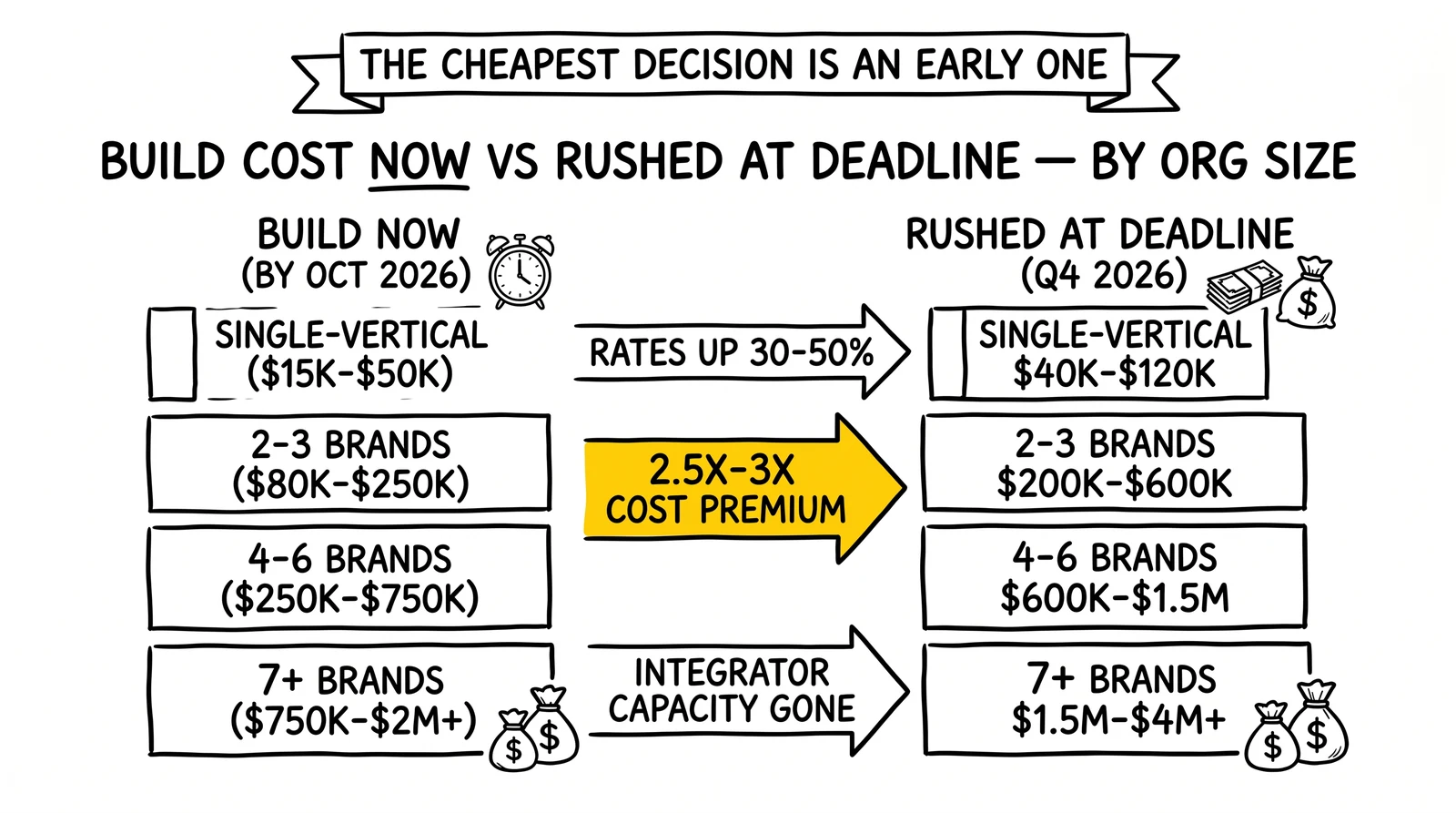

Build Cost vs Wait Risk: The Math by Organization Size

The build-vs-wait decision is fundamentally a probability-weighted cost calculation. The cost of building is the integration spend plus opportunity cost of internal resources. The cost of waiting is the probability the rule lands as written multiplied by the cost of a rushed build at the deadline, plus the probability of a litigation event during the wait period multiplied by the expected cost of that event.

The cost ranges below come from operator-reported budgets in late-2025 and early-2026 conversations, vendor implementation pricing, and the comment record submitted to the FCC’s FNPRM by industry associations describing real implementation experience. Numbers should be read as orders of magnitude, not point estimates.

| Organization Size | Stack Complexity | Build Cost (Now) | Build Cost (Rushed at Deadline) | Annual Platform Premium |

|---|---|---|---|---|

| Single vertical, 1 CRM, 1 dialer | Low | $15K–$50K | $40K–$120K | $5K–$15K |

| 2–3 brands, separate dialer + email + SMS | Medium | $80K–$250K | $200K–$600K | $20K–$60K |

| 4–6 brands, multiple acquisition vendors | High | $250K–$750K | $600K–$1.5M | $60K–$150K |

| 7+ brands, holding-company structure | Enterprise | $750K–$2M+ | $1.5M–$4M+ | $150K–$400K+ |

Cost ranges reflect vendor implementation fees, internal engineering time, legal review, and audit log infrastructure. Annual premium is the recurring cost of consent management platform fees plus integration maintenance.

The wait-risk side of the ledger has three components. The first is the probability the rule lands as written. Reasonable estimates from the FNPRM record and political signals: 25 to 40 percent that the rule lands substantively as currently written, 45 to 60 percent that it lands modified, and 10 to 25 percent that it is eliminated or vacated. The second is the cost of a rushed build versus a planned build, which the table above captures – typically 2.5x to 3x more expensive when crammed into the final 90 days before a deadline. The third is litigation exposure during the wait period from the parts of the rule already effective.

Litigation exposure is the most operator-specific number. TCPA class actions more than doubled in 2025 versus 2024, statutory damages run $500 to $1,500 per violation, and willful violations triple the per-violation damages to $1,500. An operator generating 100,000 calls per month to consumers who had revoked consent through a single-topic channel – perfectly legal under the unextended part of the rule – faces theoretical exposure of $50 million to $150 million in a single class action. Real settlements have run lower because class certification is difficult, but the QuoteWizard $19 million, Momentum Solar $30 million, and American Income Life $14 million 2025 settlements demonstrate the ceiling is high enough to bankrupt mid-market operators.

Run the math for a typical mid-market multi-brand operator: build cost now of $200,000 versus rushed cost of $500,000, multiplied by a 65 percent probability of needing the build (30 percent rule lands as-is plus 35 percent rule lands modified but still requires cross-system suppression), gives an expected build cost of waiting of $325,000 versus a known build cost now of $200,000. The wait math loses on cost alone, before accounting for litigation exposure. The conclusion flips for operators with stack complexity in the lowest tier or for whom the modification scenarios eliminate the cross-business-unit requirement entirely.

Three Operator Scenarios

The decision varies by operator profile. Three scenarios cover the dominant patterns observed in the market.

Scenario A: Build Now

The build-now scenario fits operators with high stack complexity, multiple verticals, multiple acquisition vendors, and a litigation profile that already carries serial-plaintiff exposure. The clearest archetype: a holding-company lead generator running 4 to 8 brands across insurance, financial services, and home services, with combined call volume above 5 million per month and at least one prior TCPA defendant entity in its corporate family.

For this operator, the modification scenarios in the FNPRM record do not change the architectural requirement. Even a narrowed rule that excludes exempted informational calls and permits “exclusive means” designation still requires a single canonical consumer record across brands and a real-time propagation trigger. The only modification path that eliminates the architectural requirement entirely is full elimination of the cross-topic application – a 10 to 25 percent probability outcome that does not justify a wait when the operator is already inside the litigation kill zone for unrelated TCPA theories.

The build-now operator commits a fiscal 2026 budget of $300,000 to $1 million depending on scale, retains a TCPA-experienced systems integrator (typical engagements run $150 to $300 per hour over 4 to 8 months), selects a consent management platform with multi-business-unit support, and treats the build as 70 percent integration, 20 percent process design, and 10 percent legal review. Completion target is October 2026, which provides a 90-day buffer for production hardening and vendor flow-down testing before the January 31 deadline.

Scenario B: Build Later

The build-later scenario fits operators with medium stack complexity who can plausibly compress the build into 4 to 6 months and want to see the FNPRM resolve before committing capital. The archetype: a 2 to 3 brand operator with $20 million to $80 million in revenue, stable acquisition channels, and existing investments in a unified CRM that is not yet wired to all outbound systems.

The build-later operator monitors three signals through 2026. The first is the FNPRM final order, expected based on the February 3, 2026 reply comment deadline and typical FCC rulemaking cycles to land between Q3 2026 and Q1 2027. The second is the political composition of the FCC – Commissioner turnover, Carr’s continued chairmanship, and any signals about enforcement priorities. The third is litigation activity targeting cross-channel revocation theories, which would indicate plaintiff firms are testing the broader rule’s exposure even before the formal effective date.

Build-later does not mean wait-and-do-nothing. The operator commits in the first half of 2026 to identity consolidation work – a single canonical contact record per consumer across brands – which is a no-regret action regardless of how the rule resolves. That work typically costs $30,000 to $100,000 and reduces the eventual integration build by 40 to 60 percent. The build trigger is either the FNPRM final order or October 2026, whichever comes first, with a 90-to-120-day implementation runway to the January 31 deadline.

Scenario C: Wait

The wait scenario fits a narrow operator profile: low stack complexity, single vertical, single CRM, single dialer, and acquisition channels that do not generate cross-product cross-sell. The archetype: a focused vertical operator (Medicare, solar, mortgage refinance) with one brand, one outbound channel, $5 million to $30 million in revenue, and existing single-topic revocation infrastructure that already operates within the seven-day window.

For this operator, the rule’s cross-topic application has limited operational impact because there are no other topics. A consumer who opts out of Medicare calls from this operator was not going to receive non-Medicare calls from this operator regardless of the rule. The wait strategy makes sense here because the build cost is genuinely lower if the rule lands as-is (a known $20,000 to $60,000 incremental work to harden cross-channel suppression within the same vertical) and the rule’s elimination scenario reduces the build to zero.

The wait operator does three things in 2026: maintains compliance with the already-effective portions of § 64.1200(a)(10), files comments to the FNPRM through trade associations to influence the modification path, and architects any new system selections (replacement dialer, replacement CRM) to support cross-business-unit suppression natively even though the operator does not currently need it. The cost of architectural readiness is near-zero on greenfield selections and trivial on platform upgrades.

The FNPRM Landscape: What’s Likely to Change

The October 29, 2025 Further Notice of Proposed Rulemaking is the document operators should be reading most carefully. It is the agency’s stated road map for what the January 31, 2027 rule actually looks like. Reply comments closed February 3, 2026, and the comment record now contains the substantive arguments the FCC is weighing.

Four modification themes dominate the FNPRM and the comment record. The first is exemption scope. Healthcare providers, financial institutions, and utility companies submitted detailed arguments that the rule’s breadth blocks legitimate, consumer-desired communications – fraud alerts, prescription refills, and outage notices – when consumers opt out of a marketing channel. The FNPRM explicitly asks whether the cross-topic application should be carved out for exempted informational calls. The base case is that this carve-out lands.

The second is the “exclusive means” question. The current rule requires callers to honor opt-out requests made through any reasonable means – text replies, voice prompts, IVR menus, email replies, web forms, written letters. The FNPRM asks whether callers should be permitted to designate specific exclusive channels. The industry comment record strongly supports designation; the consumer protection comment record opposes it. The base case is partial relief – designation of one or two reasonable channels rather than total flexibility.

The third is the “reasonable means” definition itself. Even if the exclusive-means question is denied, the FNPRM asks whether specific channels (postal mail, voicemail, third-party agents) should be excluded from the “reasonable means” obligation. The base case is narrowing – postal mail and voicemail get carved out, real-time digital channels remain.

The fourth is the broader question of whether the cross-topic application survives at all. The FNPRM does not propose elimination explicitly, but the language asking “how to modify the rule to balance consumers’ ability to stop unwanted calls with their interest in continuing to receive desired communications” leaves the door open. Industry commenters argued for elimination; the FCC staff record suggests modification rather than elimination is more likely.

Operators reading these themes for build planning should weight the architectural impact. The exemption scope question changes which calls require suppression but not whether suppression infrastructure is needed. The exclusive-means question changes the user-facing flow but not the back-end propagation requirement. Only the cross-topic survival question fundamentally changes whether the build is required at all, and that is the lowest-probability modification path.

Political Risk Math Through 2027

The political math compounds the FNPRM math. The rule was adopted under a different FCC composition than the one that will issue the final order. Chairman Carr’s “Delete, Delete, Delete” deregulation initiative has produced over 2,000 docket items proposed for elimination since early 2025, and the TCPA NPRM released in October 2025 was framed explicitly within that initiative.

Three political vectors matter for the build decision. The first is FCC Commissioner composition. Commissioner Simington’s term expired in early 2026; his replacement will be a Trump appointee and will likely align with Carr’s deregulation agenda. Commissioner Gomez (Democratic appointee) provides the dissenting voice. The 2-to-1 Republican majority through 2027 supports a modification trajectory.

The second vector is the threat of court challenges to the rule itself. The Eleventh Circuit’s January 24, 2025 vacatur of the FCC’s one-to-one consent rule in Insurance Marketing Coalition v. FCC established a precedent that the FCC’s TCPA rulemaking authority has limits where it conflicts with statutory text. Industry petitioners are reportedly preparing similar challenges to the revoke-all rule should it land in modified form. A successful challenge resets the entire timeline. The article on the one-to-one consent rule and its post-vacatur implications covers the precedent in detail.

The third vector is enforcement posture. Even if the rule lands as written, the FCC under Carr has signaled that aggressive monetary forfeitures are not the agency’s enforcement priority. Direct FCC enforcement risk is therefore lower than under prior leadership. Private litigation risk – class actions and serial plaintiffs – remains the dominant exposure and is unaffected by FCC enforcement posture. The site’s analysis of FCC enforcement actions and TCPA penalty trends covers the historical record.

The combined political read: the rule that lands on January 31, 2027 is most likely modified, narrowed in scope, and unlikely to expand. The probability that an operator who builds for the rule as currently written will have over-built is moderate; the probability that an operator who waits will have under-built is also moderate. The asymmetry favors building for the modified scenarios – exemption-aware, exclusive-means-capable architectures that support narrower rules without rework – rather than building for the rule as currently written.

Vendor Capability Comparison

Vendor selection drives the build cost more than any other factor. Operators who select a platform that natively supports cross-business-unit consent linkage cut integration time by 40 to 70 percent versus operators who custom-build on top of a platform that requires it as an afterthought.

The matrix below covers the platforms most commonly deployed in lead operations and their support for the architectural requirements of the rule. “Native” means the capability is a documented core feature; “Configurable” means the capability is achievable but requires implementation work; “Custom” means the capability requires substantial integration outside the platform’s standard documentation.

| Platform | Cross-Business-Unit Identity | Real-Time Suppression Propagation | Audit Log of Opt-Outs | Vendor Flow-Down API |

|---|---|---|---|---|

| Salesforce Marketing Cloud + Consent Data Model | Native | Configurable | Native | Configurable |

| HubSpot (with Internal Business Unit object) | Native | Configurable | Native | Configurable |

| boberdoo Dynamic Consent | Native | Native (at distribution) | Native | Native |

| Convoso (TCPA compliance toolkit) | Configurable | Native | Native | Configurable |

| Phonexa | Configurable | Configurable | Native | Configurable |

| LeadsPedia | Configurable | Configurable | Native | Configurable |

| OneTrust Universal Consent | Native | Native | Native | Native |

| Didomi | Native | Native | Native | Configurable |

Capability assessments based on vendor public documentation, implementation case studies, and FNPRM comment record references as of Q1 2026.

Several patterns emerge from the matrix. Lead-industry-native platforms (boberdoo, Convoso, Phonexa, LeadsPedia) support the operational primitives well but vary in cross-business-unit identity handling. boberdoo’s Dynamic Consent module is purpose-built for the cross-buyer suppression problem and ships closer to native than competitors. Generalist marketing platforms (Salesforce, HubSpot) handle the identity layer well but require more implementation work on the lead-distribution-specific flow-down. Dedicated consent management platforms (OneTrust, Didomi) handle every dimension natively but carry annual fees of $50,000 to $250,000 for mid-market deployments and require integration with every outbound system.

The vendor decision for a build-now operator usually lands in one of two patterns. Pattern A: existing Salesforce or HubSpot deployment, layered with a consent management platform that sits in front, with custom integration to lead-industry-specific outbound systems. Pattern B: existing lead-industry platform (boberdoo, Phonexa) extended with native consent modules and integrated with a general-purpose CRM for marketing operations. Pattern A typically costs more upfront and provides cleaner long-term architecture; Pattern B costs less upfront and locks the operator into the lead-industry vendor’s roadmap.

The 60-Day Decision Window

The strategic decision does not need to be made today. It needs to be made by approximately Q3 2026 to leave runway for either a build-now or a build-later execution. The 60-day decision window for build-now operators is roughly mid-2026 through August 2026 – the period when fiscal 2026 budgets are still actionable and integration partners have capacity. The 60-day decision window for build-later operators is October through December 2026, after the FNPRM final order has either landed or signaled its direction.

Three signals should trigger the decision earlier than the window suggests. The first is FNPRM final order publication. If the rule modification lands before Q3 2026, the build-vs-wait math collapses to either build-the-modified-rule or skip-the-build entirely. The second is litigation activity targeting cross-channel theories. If plaintiff firms file class actions in 2026 alleging that the underlying single-topic rule already implies cross-business-unit application, the wait strategy becomes untenable regardless of FNPRM timing. The third is M&A activity in the operator’s stack. Acquisition or divestiture changes the cross-business-unit footprint and forces a fresh architectural decision regardless of regulatory timing.

The cost of analysis paralysis through this decision window is real. Operators who delay the build-vs-wait decision into Q4 2026 face capacity constraints with implementation partners – by late 2026, every TCPA-experienced systems integrator is fully booked through the deadline, and rates rise 30 to 50 percent. The cheapest decision is an early one in either direction. The most expensive decision is no decision until December 2026.

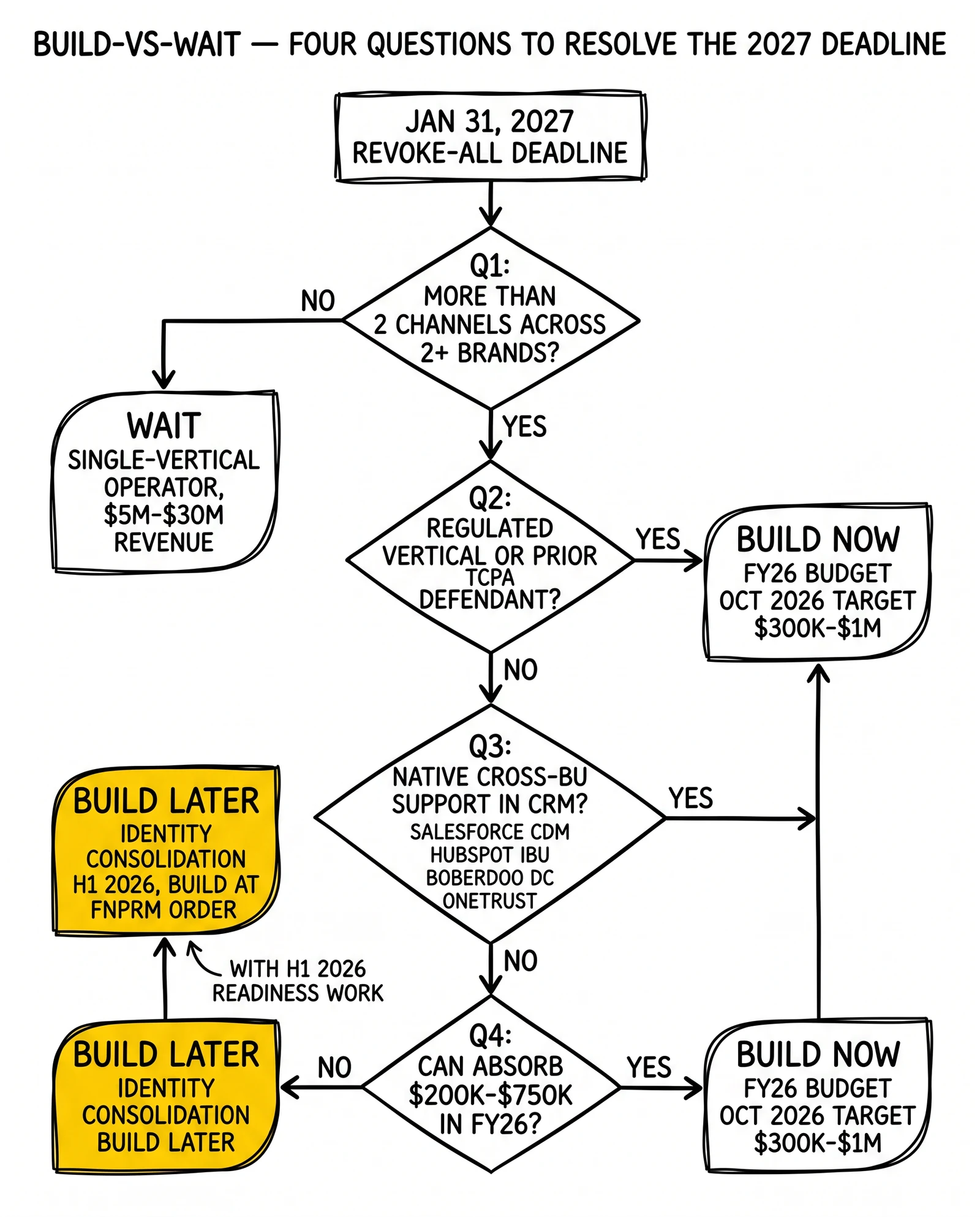

A Four-Question Decision Tree

The build-vs-wait decision reduces to four questions that operators can answer with available information today.

Question 1: Does the operation run more than two distinct outbound channels (voice, SMS, email) across two or more brands?

If no: the rule’s cross-business-unit application has limited impact. Wait scenario fits. Maintain single-topic compliance and architect new selections for cross-BU support without committing capital.

If yes: proceed to Question 2.

Question 2: Are any of the brands in highly regulated verticals (healthcare, financial services, debt collection) or have any corporate entities been TCPA defendants in the prior 36 months?

If yes: build-now scenario fits. The litigation profile and regulatory scrutiny eliminate the option to wait on the FNPRM outcome. Commit fiscal 2026 budget, retain a systems integrator, target October 2026 completion.

If no: proceed to Question 3.

Question 3: Does the existing CRM and outbound stack support cross-business-unit identity natively (Salesforce + Consent Data Model, HubSpot + IBU, boberdoo Dynamic Consent, OneTrust, Didomi)?

If yes: build-later scenario fits. The native support reduces eventual integration cost by 50 to 70 percent and makes a 4-to-6-month build feasible from October 2026. Commit to identity consolidation work in H1 2026 (under $100,000) and trigger the build at FNPRM final order or October 2026.

If no: proceed to Question 4.

Question 4: Can the operation absorb a $200,000 to $750,000 build cost in fiscal 2026 without triggering capital constraints, and does the leadership team have the cognitive bandwidth to execute a major systems integration in 2026?

If yes: build-now scenario fits. The asymmetric risk favors investment over waiting given stack complexity.

If no: build-later scenario fits, but with the architectural readiness work treated as a fiscal 2026 priority. The H1 2026 readiness work converts a 2027 cliff into a 2027 ramp.

Implementation Reality for the Build-Now Operator

For operators whose answer is “build now,” implementation lands in five workstreams running roughly in parallel from May through October 2026.

The first workstream is identity consolidation. A single canonical consumer record per individual, federated across brands and business units, with a unique identifier that maps to phone, email, hashed identifier, and any other contact attributes. This work typically runs 8 to 12 weeks and costs $50,000 to $250,000 depending on starting state. The output is a contact graph that downstream systems can query rather than each system maintaining its own consumer table.

The second workstream is consent management platform selection and configuration. The selection criteria include native cross-business-unit support, real-time API throughput at expected call volumes, audit log immutability, and integration coverage for the existing outbound stack. Selection runs 4 to 8 weeks; configuration runs 8 to 16 weeks. Total cost is typically $80,000 to $400,000 in implementation plus $50,000 to $250,000 in annual platform fees.

The third workstream is outbound system integration. Each dialer, SMS platform, and email platform queries the consent record at contact time and writes opt-out events back to the consent record in real time. Integration runs 4 to 8 weeks per system depending on platform openness. For a typical 4-brand operator with 3 outbound channels, this is 12 to 24 weeks of integration work, typically $150,000 to $400,000 total. The article on building a complete TCPA compliance program covers the broader programmatic infrastructure that wraps these technical integrations.

The fourth workstream is vendor flow-down. Every third-party affiliate and downstream buyer receives suppression updates through a dedicated API or webhook, with audit logging of receipt and acknowledgment. Flow-down runs 4 to 12 weeks depending on affiliate count and varies dramatically in cost – small affiliate networks under $50,000, large multi-buyer operations $100,000 to $300,000. The contractual layer (updated buyer agreements, flow-down clauses) runs in parallel with the technical layer.

The fifth workstream is process and audit. Standard operating procedures for handling opt-outs received outside the digital channels (postal mail, voicemail, agent escalations), audit log review cadence, and quarterly compliance verification testing. This work is the smallest line item ($20,000 to $80,000) but the most operator-specific and the one most often skipped by operators focused on the technical build.

The aggregate budget for a typical mid-market multi-brand build runs $400,000 to $1.2 million across the five workstreams over 5 to 7 months. Enterprise-scale builds run higher and longer. The defining variable is starting state – operators with a unified CRM and consent receipts already structured for cross-channel use can compress the timeline by 30 to 50 percent versus operators starting from disconnected systems.

Future Implications: What the Rule Settles

The revoke-all rule, in whatever final form it takes, settles a longer-term architectural question for the lead generation industry. The era of multi-brand operators running independent contact systems with no canonical consumer view is ending. State-level mini-TCPA laws (Florida’s FTSA, Oklahoma’s OTSA, Maryland’s MTCPA) already imply cross-channel suppression obligations. The EU’s GDPR has required canonical consent records since 2018. Plaintiff-firm theories increasingly assume operators can produce a single record per consumer.

Operators who treat the January 31, 2027 deadline as a one-time compliance project miss the strategic dimension. The build is not for the FCC rule alone. It is the foundation for handling every cross-jurisdictional consent requirement that follows. The infrastructure built for revoke-all compliance also handles state mini-TCPA requirements, supports CCPA and GDPR data subject rights requests, and provides the audit trail for any future regulatory regime that asks operators to prove they suppress contact when consumers ask them to.

The operators who emerge from 2027 with sustainable advantage are not those who built the cheapest possible compliance system. They are those who built consent infrastructure as a strategic asset – the consumer identity layer their entire data operation runs on. The rule is the forcing function. The infrastructure is the durable outcome.

Key Takeaways

-

The January 6, 2026 extension is real but narrow. Order DA 26-12 moved only the cross-topic application portion of § 64.1200(a)(10) to January 31, 2027. The seven-day implementation window, recognition of revocation through reasonable means, and exempted-informational-call treatment remain fully effective today, and plaintiff firms are filing on these provisions aggressively.

-

The October 29, 2025 FNPRM signals modification, not elimination. The base case from the comment record is exemption carve-outs (healthcare, fraud alerts), permitted “exclusive means” designation, and narrowed “reasonable means” definitions. The cross-topic application most likely survives in modified form, which still requires cross-business-unit suppression infrastructure.

-

Build cost runs 2.5x to 3x higher when crammed into the final 90 days before a deadline. Operators waiting until Q4 2026 face implementation partner capacity constraints and rate increases of 30 to 50 percent. The cheapest decision is an early one in either direction.

-

The wait scenario fits a narrow operator profile. Single-vertical, single-brand, single-channel operators with $5M to $30M in revenue and stable cross-product cross-sell can plausibly wait on the FNPRM outcome. Multi-brand operators with regulated-vertical exposure or prior TCPA defendant status do not have the same option.

-

Identity consolidation is a no-regret investment regardless of rule outcome. A single canonical consumer record per individual, federated across business units, costs $30,000 to $100,000 and reduces eventual integration build by 40 to 60 percent. State mini-TCPA, GDPR, and plaintiff-firm theories already assume operators can do this; the rule simply makes it federal.

-

Vendor selection drives 40 to 70 percent of integration cost variance. Native cross-business-unit support in the consent platform (Salesforce + Consent Data Model, OneTrust, Didomi, boberdoo Dynamic Consent) cuts implementation time substantially versus custom builds on top of platforms without native support.

-

Direct FCC enforcement risk is lower under Chairman Carr than under prior leadership. Private litigation risk – class actions and serial plaintiffs – remains the dominant exposure and is unaffected by FCC enforcement posture. The asymmetry favors operators who size litigation exposure rather than regulatory fine exposure when running the build-vs-wait math.

-

The Q3 2026 decision window is the practical deadline. Build-now operators must commit by August 2026 to leave runway for an October completion. Build-later operators must trigger by October-December 2026 with H1 2026 architectural readiness work already complete. Decisions delayed past December 2026 collapse into the no-options corner.

-

The infrastructure outlasts the rule. Whatever form § 64.1200(a)(10) takes on January 31, 2027, the consumer identity and consent infrastructure built to comply with it becomes the foundation for every subsequent regulatory regime. Operators who build for the strategic asset rather than the immediate rule emerge with durable advantage.

Frequently Asked Questions

What did the FCC actually change on January 6, 2026?

The FCC’s Consumer and Governmental Affairs Bureau issued Order DA 26-12 extending the effective date of the portion of 47 C.F.R. § 64.1200(a)(10) that requires a single revocation request to apply across unrelated topics from the same caller. The new effective date is January 31, 2027 – moved from April 11, 2026, which itself was moved from April 11, 2025. Other portions of the October 2024 revocation rules remain in effect, including the seven-business-day implementation window, recognition of revocation through any reasonable method, and treatment of revocation made in response to exempted informational calls.

Does the extension cover every part of the revocation rule?

No. The waiver applies narrowly to the “revoke-all” or “global revocation” provision – the requirement that an opt-out from one type of message stops all robocalls and robotexts from that caller on unrelated matters. Operators must still honor revocation requests made through any reasonable means, process them within seven business days, and treat opt-outs from exempted informational calls as full opt-outs. Single-topic suppression is fully enforceable today.

How likely is it that the rule changes before January 2027?

The probability of modification is high; the probability of elimination is moderate. The October 29, 2025 FNPRM explicitly asked whether the rule should be modified or scrapped, and Chairman Carr’s “Delete, Delete, Delete” deregulatory posture suggests the agency is looking for ways to narrow scope. However, an FNPRM is not a final order – the rulemaking process typically runs nine to eighteen months, and political turnover or court challenges could reset the clock. Counting on elimination is a reasonable bet for some operators and a catastrophic bet for others.

What does a revoke-all-compliant suppression system actually require?

At minimum: a single canonical identity record per consumer that links phone number, email, and any other contact channels across business units; a real-time API that any outbound system queries before contact; a trigger that propagates a single opt-out across all linked records within seconds; an audit log capturing the timestamp, channel, and exact phrasing of the opt-out; and a vendor flow-down provision ensuring third-party callers receive the suppression update within the seven-day implementation window. Most lead operators run two to five disconnected systems that cannot do this without integration work.

How much does a revoke-all build cost?

Costs scale dramatically with stack complexity. A single-vertical operator on one CRM platform may complete the work for $15,000 to $50,000 in vendor configuration, internal engineering, and legal review. A multi-brand operator with separate dialers, email platforms, and SMS systems typically faces $150,000 to $500,000 in integration work, plus annual platform fee increases of $20,000 to $100,000. Enterprise-scale operators with five or more brands and multiple acquisition vendors have reported budgets above $1 million.

What is the realistic enforcement risk if an operator misses the deadline?

Direct FCC enforcement under Chairman Carr is likely lower than under prior leadership, with a stated focus on infrastructure and deregulation rather than aggressive forfeitures. Private litigation is the larger risk – TCPA class actions more than doubled in 2025 versus 2024, and the statutory damages range of $500 to $1,500 per violation makes even modest call volumes catastrophic. A non-compliant operator generating 100,000 robocalls per quarter to consumers who had revoked consent through an unrelated channel faces theoretical exposure of $50 million to $150 million.

Which CRMs and dialers already support multi-topic suppression today?

Salesforce Marketing Cloud’s Consent Data Model and HubSpot’s Internal Business Unit object both support cross-brand consent linkage as of 2025. Among lead-industry platforms, boberdoo’s Dynamic Consent module handles cross-buyer suppression at distribution time, and Convoso publishes a TCPA compliance toolkit that includes opt-out propagation features. Phonexa and LeadsPedia support suppression list synchronization through API but require additional integration work to achieve cross-business-unit linkage. None of these platforms eliminates the operational design work required to map identity across systems.

Why did the FCC extend the deadline a second time?

The official rationale cited “good cause” tied to implementation complexity and the pending FNPRM. The practical driver was sustained advocacy from financial services trade groups – America’s Credit Unions, the Defense Credit Union Council, the American Bankers Association, and others – who argued that a March 12, 2025 waiver request had not provided sufficient runway for systems integration across multi-bank holding companies. Healthcare providers, utilities, and credit unions all submitted comments that the rule’s breadth would block legitimate, consumer-desired communications about fraud alerts, prescription refills, and outage notices.

Should a Series A-stage lead operator build now or wait?

For most early-stage operators with one to two verticals and a single primary outbound channel, the answer is wait – but instrument the system. A build now consumes 8 to 15 percent of typical Series A operating capital and may be invalidated by a 2026 final order. Instead, smaller operators should architect their CRM and consent records to make a future build trivial: one canonical contact record per consumer, channel-tagged consent receipts, and clean vendor data flows. That readiness work costs under $20,000 and is valuable regardless of how the rule resolves.

What is the no-regret action regardless of what happens to the rule?

Three actions are no-regret. First, consolidate consumer identity into a single canonical record across business units, because every state mini-TCPA, the EU’s GDPR, and most plaintiff-firm theories already assume operators can do this. Second, retain consent receipts and revocation receipts with timestamps and full source context, because this is the only defense against a serial litigator’s manufactured claim. Third, audit vendor flow-down clauses to ensure suppression updates reach affiliates within seven business days, because the underlying single-topic revocation rule is fully effective today and most operators are already non-compliant.

Sources

- Federal Communications Commission, Order DA 26-12, “Consumer and Governmental Affairs Bureau Extends the Effective Date of the TCPA’s Consent Revocation Rule,” released January 6, 2026.

- Federal Communications Commission, “CGB Extends the Effective Date of the TCPA’s Consent Revocation Rule,” official document page, January 2026.

- Wiley Rein LLP, “FCC Extends Limited Waiver for Part of the TCPA Consent Revocation Rule,” client alert, January 2026.

- Hunton Andrews Kurth LLP, “FCC’s TCPA Global Revocation Rules Now Effective January 2027,” Privacy and Information Security Law Blog, January 2026.

- Consumer Financial Services Law Monitor, “FCC Further Extends Effective Date for TCPA ‘Revoke-All’ Rule,” January 2026.

- Convoso, “FCC Delays TCPA Consent Revocation Rule to January 31, 2027,” company news release, January 2026.

- Privacy World (Squire Patton Boggs), “FCC Proposes Amendments to TCPA Consent Revocation Rules; Proposed Changes to DNC Rules Deleted from Final Text,” October 2025.

- Wiley Rein LLP, “UPDATE: 11th Circuit Vacates FCC’s One-to-One TCPA Consent Rule,” client alert, January 2025.

- The CommLaw Group, “FCC Extends ‘Revoke All’ Consent Rule Effective Date; Businesses Still Have Time to File Reply Comments by February 3,” January 2026.

- American Bankers Association, “Joint Letter to FCC re: Revocation of Consent Under the TCPA,” advocacy filing, 2025.

- Venable LLP, “Expectations for a Chairman Carr Led Federal Communications Commission,” January 2025.

- Federal Communications Commission, “FCC Chairman Carr Launches Massive Deregulation Initiative,” official announcement, 2025.