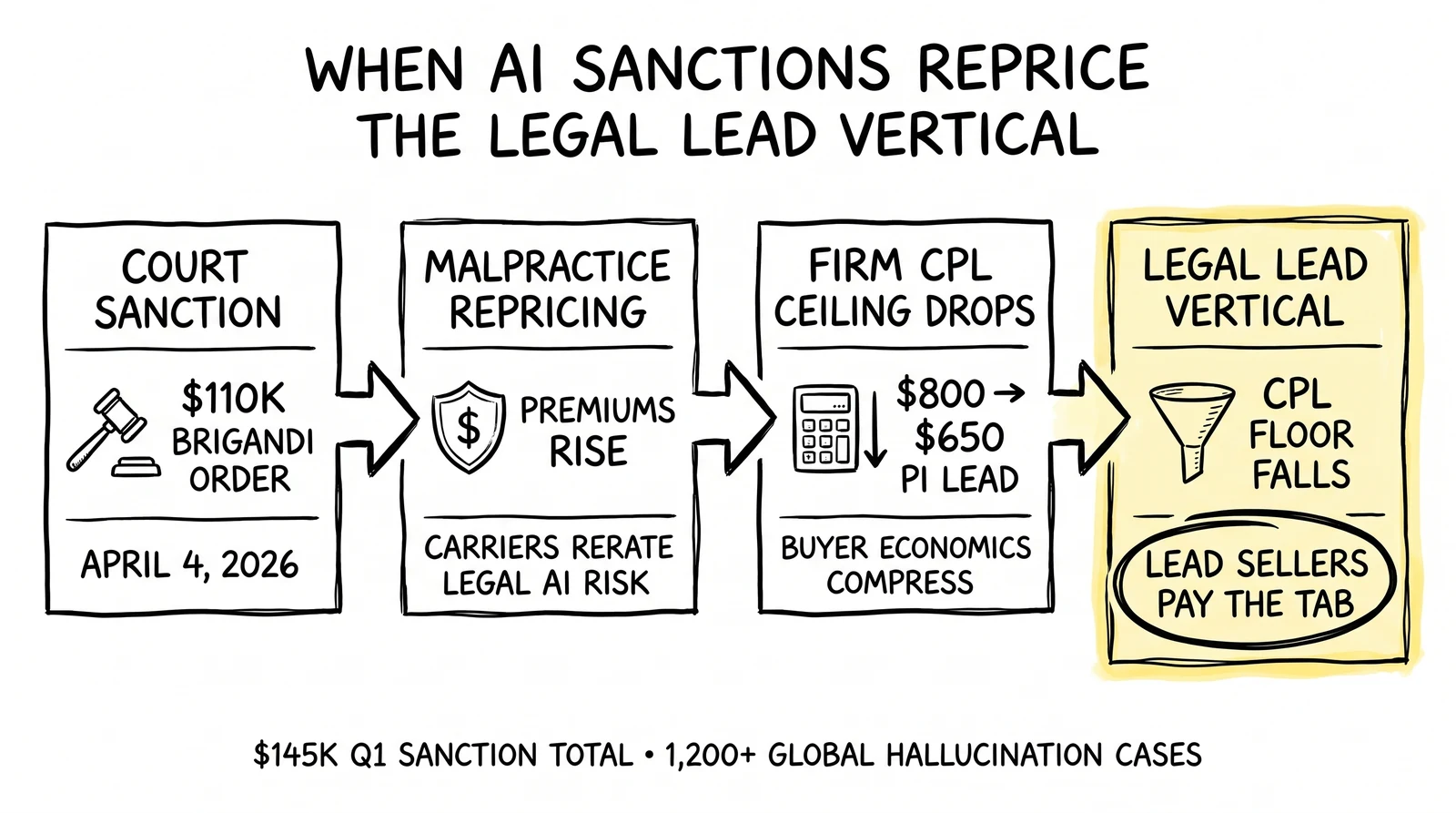

Early-2026’s documented AI hallucination court sanctions exceeded $145,000, anchored by an April 4, 2026 Oregon order of roughly $110,000 against attorney Stephen Brigandi. The sanctions land on the law firm. The economic consequences land further upstream – on the legal lead generation vertical, where buyers about to be repriced by their malpractice carriers will reprice the leads they buy in turn.

A $145,000 Quarter the Legal Lead Vertical Cannot Ignore

On April 4, 2026, U.S. Magistrate Judge Mark Clarke of the District of Oregon entered a sanction order that should have been read in two places. The first place – the legal trade press – read it as a story about attorney Stephen Brigandi, twenty-three fabricated citations, eight false quotations, three filings, and a $96,000 direct monetary sanction that climbed to roughly $110,000 once the related penalties were added. The second place – the legal lead generation vertical – largely missed it. That second readership is where the structural story sits.

By any reasonable accounting, early-2026’s documented AI hallucination sanctions in U.S. courts crossed $145,000. Researcher Damien Charlotin, who maintains the most-cited public database of hallucinated-citation rulings, has reported “10 cases from 10 different courts on a single day” in early 2026 and a global running total above 1,200 cases. The Fifth Circuit issued a $2,500 sanction over hallucinated citations in briefing reportedly drafted with vLex’s CoCounsel platform. Lower courts have been issuing $1,000-to-$10,000 orders at a steady cadence since the original 2023 Mata v. Avianca decision. The Brigandi order is the new ceiling, not an outlier.

Meanwhile, the supply side of legal AI has not slowed. Harvey AI, deployed across approximately 100,000 lawyers including the majority of the AmLaw 100, was valued at $11 billion in 2026 and has been pushing its Spectre autonomous matter-management agent into production firms. Anthropic released Claude for Microsoft Word in April 2026, putting AI-driven lease review and contract analysis directly into the Word authoring environment that transactional and litigation associates already live in. Generative AI is moving from a research-and-drafting assistant to an embedded layer of how legal work product is produced.

The lead generation vertical has been treating “legal” as the highest-CPL, highest-stakes category for a decade. Personal injury intake leads commonly clear $200 to $800 per qualified lead, with mass tort sign-up costs in some matters running into four figures per signed claimant. Those CPL benchmarks were built in a world where the dominant risk to the buyer was conversion friction – the slow march from inquiry to retainer. The April 2026 sanction wave introduces a different risk profile. The dominant risk is shifting from “did the lead convert” to “did the matter the firm won using this lead survive contact with a federal judge who reads citations.” When that risk repositions on the buyer side, every clause in every legal-vertical lead supply agreement is subject to revision. This article examines what the early-2026 sanction wave actually signals for legal lead operators, why the Brigandi order is the data point that matters most, how malpractice insurance repricing flows downstream into lead pricing, and what operators in the criminal defense, employment law, mass tort, and estate planning segments should be doing in the next ninety days.

What Actually Happened in Early 2026 – The Evidence Stack

The legal-vertical reading of the sanction wave depends on getting the underlying facts right. Five named events define the quarter.

The Brigandi order

On April 4, 2026, Magistrate Judge Clarke imposed a sanction package against Oregon attorney Stephen Brigandi totaling approximately $110,000. The direct monetary sanction was reported at $96,000, with the balance composed of related penalties tied to the same conduct. The trigger was three federal filings that, on judicial review, contained twenty-three fabricated citations and eight false quotations – citations to opinions that did not exist and quoted language that did not appear in the cases purportedly cited. The order made the underlying conduct clear: the citations had been generated by AI tools without verification, and the resulting filings were submitted to the court without the attorney having read or confirmed the cited authority. The numbers matter because Brigandi’s $96,000 direct sanction is, as of late April 2026, the largest publicly reported single-attorney AI hallucination sanction in U.S. federal court.

The Charlotin trajectory

Damien Charlotin’s hallucination case database has become the most-cited running tally of fabricated-citation rulings worldwide. The database documents court decisions in which the court itself identified hallucinated citations in filed work product, with cases logged from U.S. federal and state courts as well as comparable jurisdictions internationally. Public reporting on the database describes Charlotin documenting “10 cases from 10 different courts on a single day” in early 2026 and a global total exceeding 1,200 cases. The trajectory matters more than any single number. The slope of the curve through 2024 and 2025 was steep; the slope through early 2026 has been described by Charlotin and his commentators as steeper still. The shift from a few high-profile cases per quarter to ten-plus per day is the structural change.

The Fifth Circuit’s $2,500 order

A Fifth Circuit decision in late 2025 / early 2026 imposed a $2,500 sanction on counsel for citations later identified as hallucinated, with reporting that linked the underlying drafting to vLex’s CoCounsel platform. The dollar figure is small. The signal is large: the sanction was at the federal appellate level, and the court named a specific commercial AI-drafting tool in connection with the conduct. Appellate sanctions tend to set tone for the trial-court bench beneath them. The lower-court cadence of hallucination sanctions through early 2026 is consistent with a bench that is now actively looking for fabricated authorities and willing to act when it finds them.

The Harvey AI footprint

Harvey AI’s reported deployment numbers – approximately 100,000 lawyers, the majority of the AmLaw 100, an $11 billion valuation reported in 2026, and the Spectre autonomous-agent product – establish the scale at which generative AI is now embedded inside the buy side of legal lead generation. Plaintiff-side mass tort firms, defense-side personal injury firms, and the large national firms that participate in MDL leadership all overlap with the Harvey deployment cohort. Whatever quality-control policies those firms have written for AI use are now being tested against actual production work. The early 2026 sanction list does not, to public knowledge, name Harvey-drafted filings as the source of any specific sanction order; the relevant point is the deployment surface area, not any single product attribution.

The Anthropic Claude for Word release

In April 2026, Anthropic released Claude for Microsoft Word, integrating Claude-powered drafting and review – including lease and contract review – into the Word authoring environment. The release matters for the legal vertical because Word is the document layer that almost all legal work product flows through. Embedding a generative model in that layer collapses the workflow distance between “AI assistance” and “filed document.” That collapse increases the operational risk surface for the firms that buy legal leads, even where the firms have not affirmatively adopted Harvey, vLex, or any other domain-specific AI tool.

The five events form a coherent picture: rising sanction frequency, larger sanction sizes, named commercial-tool involvement, dominant deployment of AI inside the buy side, and a workflow-layer integration that lowers the barrier to AI-mediated drafting. Each of those is independently relevant to the lead vertical. Stacked, they describe a buy side whose risk profile is being repriced.

How Sanction Risk Becomes Lead Pricing Risk

The Brigandi sanction lands on a single Oregon attorney. The economic chain that runs from that order to the price of a personal injury lead in Houston is shorter than it appears.

Step one: malpractice insurance repricing

Lawyers Professional Liability (LPL) carriers price firm premiums on a forward-looking expected-loss basis. An LPL underwriter looking at the early 2026 sanction data has three new inputs: the rising frequency of sanction events, the rising severity of the largest events, and the increased likelihood that hallucinated authority survives review long enough to prejudice a client matter. None of these is hypothetical anymore. Public reporting through 2025 and 2026 has documented carriers issuing AI-specific underwriting questions, AI exclusions, and tiered premium adjustments tied to firm-level AI governance policies. The Brigandi-scale order does not change the pricing model so much as confirm the loss-cost trajectory the model already anticipated. Carriers that priced AI risk into 2026 renewals are now revisiting 2027 renewals upward; carriers that did not are accelerating the underwriting changes.

Step two: firm-level cost-of-acquisition revision

A law firm’s lead acquisition budget is not a fixed line item. It is a residual of the firm’s expected case economics minus all upstream costs – including malpractice premiums, e-discovery costs, ALSP costs, and the cost of the AI tools the firm has chosen to deploy. When malpractice premiums move materially upward, the residual narrows. Firms either accept lower per-case profitability, raise their per-case price (rare in commoditized verticals like personal injury), or lower their cost of acquisition. The dominant lever has historically been the third – and the dominant target of that lever is the lead supply chain.

Step three: contractual repricing of legal lead supply

The repricing happens in three places. First, in headline CPL: firms push back on $200-to-$800 personal injury CPLs, $300-to-$1,200 mass tort sign-up costs, and the equivalent benchmarks across employment, criminal defense, and family law. The push usually fails on price alone – supply economics constrain how far CPLs can move – but it succeeds in adjacent terms. Second, in return windows: firms ask for longer dispute windows (from seven to fourteen days, or fourteen to thirty), broader return reasons, and softer documentation standards for returns. Third, in provenance and quality terms: firms demand documentation about how leads were generated, whether AI was involved in qualification or scoring, and what consent and verification artifacts attach to each lead.

The price is not what changes. The terms around the price are what change. That is the first-order consequence of the early-2026 sanction wave for the legal lead vertical’s CPL benchmarks.

Step four: spillover to the lead seller’s working capital

When return windows widen, the lead seller’s working capital cycle lengthens. A lead sold today and not returnable for thirty days carries a higher financing cost than a lead with a seven-day window. For mid-sized lead operators with monthly origination volumes in the tens of thousands of legal leads, the working-capital implication of moving from seven-day to thirty-day windows is material – typically a low-single-digit percentage of revenue moved into receivables, with corresponding pressure on lines of credit and origination pacing. Operators who do not price the working capital impact into their wholesale CPL find themselves margin-compressed without an obvious cause.

Step five: legal vertical mix shifts inside aggregator portfolios

Lead aggregators that run a portfolio across legal, mortgage, insurance, and home services treat each vertical as a margin contributor. When legal-vertical margin compresses for the reasons above, aggregators rebalance – pushing media spend toward higher-margin verticals and pulling back on legal until the terms recover. The pullback is asymmetric. Aggregators continue to participate in mass tort matters with strong fee economics (catastrophic injury, large-pharma defective-drug matters) while pulling back from lower-margin legal sub-verticals (small-dollar consumer claims, marginal employment matters). The result is a tighter legal supply with a wider quality-tier dispersion – exactly the market structure that makes due diligence on leads more important and harder to perform simultaneously.

The chain from “Brigandi order” to “aggregator rebalancing” is not theoretical. Some of it is already visible in the contract negotiations underway with carriers and firms in April and May 2026. The rest will arrive on a six-to-twelve-month lag as carriers complete renewal cycles and firms revise their lead supply agreements.

The Sub-Vertical Math: Where the Repricing Hits Hardest

The legal lead vertical is not one market. It is at least seven markets – personal injury, mass tort, criminal defense, family, employment, estate planning, and small-business legal – each with its own CPL economics, conversion math, and exposure to the AI-hallucination repricing. The sanctions wave hits each differently.

Personal injury and mass tort: the highest exposure, the slowest reprice

Personal injury and mass tort verticals carry the highest CPLs in legal lead generation because the case economics – contingent fees on settlement values that can range from low five figures to seven figures or more – support the spend. They also carry the highest exposure to AI-hallucination risk because the volume of motion practice, the pressure on associate hours, and the appeal of AI-assisted legal research are all maximal. Yet these same verticals will reprice slowest, because the underlying case economics absorb a lot of cost increase before they break.

What changes first is dispute economics. A mass tort firm participating in a bellwether-driven calendar that historically accepted leads with a seven-day return window will request fourteen to thirty days, citing the increased intake-team scrutiny required to verify lead authenticity in an AI-saturated environment. Firms will request AI-attestation language in lead supply agreements – a representation by the seller that AI tools, where used in lead generation, were used with documented quality controls and that no fabricated information has been introduced into the lead record. Firms will also request that lead aggregators document any AI-mediated scoring, qualification, or consent processes used in lead capture. None of these requests changes headline CPL. All of them change net realized CPL.

Criminal defense: the fastest reprice, the smallest dollars

Criminal defense leads carry lower CPLs than personal injury – $50 to $250 is a common range, with high-dollar exposure tied to specific case types like DUI or white-collar – but they carry the fastest sanction-wave reprice. Two reasons: criminal defense firms are smaller on average, more sensitive to malpractice premium increases, and less able to absorb working-capital expansion; and the courts hearing criminal matters have been particularly aggressive about AI-hallucination conduct, where the consequences of fabricated authority can directly prejudice a defendant. Operators running criminal defense lead programs should expect the contractual terms conversation to start in Q3 2026, not Q1 2027.

Employment law: the most fragmented, the most quality-sensitive

Employment law leads – discrimination, wrongful termination, FLSA wage-and-hour claims – span a wide CPL range from $80 (high-volume FLSA) to $400 or more (specialized discrimination matters). The sub-vertical is fragmented across plaintiff-side and defense-side, with different malpractice profiles. Plaintiff-side employment firms will be the most aggressive about AI-attestation language, because they operate on contingency and any matter that gets dismissed for procedural defects (including AI-tainted briefing) is a write-off. Defense-side employment work, billed hourly, has different incentives but the same exposure. Lead sellers in this sub-vertical will face two distinct buyer profiles asking for related but not identical contractual changes.

Estate planning and elder law: the most insulated, the most patient

Estate planning leads – including elder law and trust matters – carry CPLs in the $100 to $300 range with case economics that are less sensitive to per-matter sanction risk because the work is largely transactional rather than litigation-driven. Hallucinated authority in a trust document is rarer and lower-stakes than hallucinated authority in a brief. Estate planning firms will reprice slower and less aggressively, but they will adopt the AI-attestation language as it diffuses through the legal industry, on the same compliance-tracking logic that drove their adoption of cybersecurity language in 2018-2020.

The CPL benchmark across the vertical

The headline CPL numbers that anchor the legal vertical’s benchmark math – $200 to $800 personal injury, $300 to $1,200 mass tort sign-up, $50 to $250 criminal defense, $80 to $400 employment, $100 to $300 estate – will not move dramatically in 2026. What will move is the realized net CPL after returns, dispute resolutions, and contractual quality-tier discounts. A reasonable working assumption: a five to fifteen percent net realized CPL compression across the personal injury and mass tort segments by Q4 2026, driven entirely by terms changes, with smaller compression in the other sub-verticals on a six-to-twelve-month lag.

The Operator Postures That Will Underperform

Three responses to the early-2026 sanction wave are visible in operator conversations across the vertical. Each will produce worse outcomes than its proponents expect.

The first is the it-is-a-law-firm-problem posture. Operators in this camp read the Brigandi order as an attorney-discipline event – relevant to bar associations, insurance carriers, and ethics committees, but disconnected from lead supply economics. The argument is that lead sellers do not draft briefs, do not file motions, and bear no Rule 11 exposure for their buyers’ work product. The argument is procedurally correct and economically wrong. Lead sellers do not bear direct sanction exposure, but they bear the full economic impact of their buyers’ downstream cost increases. The malpractice carriers do not raise premiums on lead sellers; they raise them on law firms, who then push back on lead supply terms. An operator who treats sanction events as outside the lead vertical’s frame will be surprised by Q3 2026 contract renewals.

The second is the wait-for-clarity posture. Operators in this camp acknowledge the relevance of the sanction wave but conclude that any contractual changes should wait until carriers, courts, and bar associations have published settled standards. The argument is that pre-emptive contract changes will create disadvantageous precedents that lock in unfavorable terms before the market settles. The argument is risk-managed and timing-wrong. Settled standards are not coming in 2026. The carriers are pricing month by month based on incremental data; the bar associations are issuing guidance that varies state by state; the courts are issuing per-case orders without uniform doctrine. An operator who waits for settled standards waits past the moment when contracts can be renegotiated proactively, and ends up renegotiating reactively when a buyer triggers a dispute.

The third is the deny-AI-everywhere posture. Operators in this camp respond to the sanction wave by writing contractual representations that AI is not used in any part of their lead generation operation. The argument is that buyers want AI-free leads and that the cleanest representation is a categorical denial. The argument is buyer-aware and operationally untrue. Modern lead generation depends on AI in dozens of places – ad creative testing, fraud detection, scoring, transcription, intake QA. A categorical denial is either inaccurate (and discoverable as such in dispute proceedings) or so narrowly worded as to be useless. The operators who go this route end up with representations they cannot defend, which is worse than representations they can stand behind.

The pattern across these three approaches is the same: each underestimates the speed and structure of the buyer-side repricing, and each fails to recognize that the right response is neither denial nor delay but a documented and defensible operational posture on AI use in lead generation.

The Strategic Reframe: Three Principles for the Repriced Legal Vertical

The right response to the early-2026 sanction wave starts from a different premise. The buyer side is repricing risk, and the lead seller’s job is to produce a unit of inventory whose risk profile is documented well enough to support its price. Three principles flow from that premise.

Principle one: document AI provenance as a sellable attribute

In the old legal lead market, the sellable attributes were exclusivity (exclusive vs. shared), recency, vertical match, and TCPA consent compliance. In the repriced market, AI provenance joins that list. A lead delivered with documentation of where AI was used in its capture (none, scoring only, intake transcription, full conversational AI), what model class was used, what human-review checkpoints were applied, and what artifact retention policies attached, is a structurally different unit of inventory from a lead delivered without that documentation. Buyers will increasingly accept the former and reject the latter – or, more precisely, accept both but at different price points.

The work to make AI provenance a sellable attribute is operational. It requires the lead operator to map AI use across the funnel, formalize the human-review checkpoints, retain the artifacts, and produce buyer-facing documentation. The operators who build this documentation in Q2 and Q3 2026 will sell into a buyer market that is just beginning to price provenance into its bid. The operators who skip this work will sell against operators who have it.

Principle two: rebuild dispute documentation around AI-aware quality control

The legacy lead quality control framework was built around three categories: invalid contact (bad number, bad email), no-intent (consumer denies submitting the lead), and out-of-criteria (does not match buyer’s vertical or geographic filters). The repriced framework adds a fourth category: AI-tainted information (lead record contains information that, on review, appears to have been generated rather than collected). AI-tainted disputes will surface in two ways – buyers reviewing leads against external verification sources and finding inconsistencies, and consumers themselves contesting lead-record details that they did not provide. Operators need a quality-control framework that handles AI-tainted disputes specifically: a defined triage path, an investigation protocol, and a pricing-and-credit logic for partial-credit outcomes.

This is not theoretical work. Some buyers, particularly the larger firms running internal intake-QA functions at scale, are already running consumer-record inconsistency audits as part of their normal lead acceptance process. The lead seller who can show the dispute resolution data – disputes received, disputes investigated, dispute resolution times, dispute rates by source – has a far stronger negotiating position with carriers and buyers than the seller who cannot. The framework is also defensive: a documented dispute management process is what protects the seller from buyer-side overreach when terms negotiations move into the contractual fine print.

Principle three: tier buyers by AI-policy maturity, not just by price

The legacy buyer waterfall ranked buyers on price, exclusivity tier, and pay-stability. The repriced waterfall adds AI-policy maturity as a tiering input. A buyer with a documented internal AI governance policy, a stated AI-attestation requirement, and a clear dispute protocol is structurally a different counterparty than a buyer who has no policy. The mature-policy buyer is harder to onboard but more valuable per lead and more durable as a long-run customer. The no-policy buyer is faster to onboard but more likely to surface a dispute in twelve months that the lead seller has no documentation to defend against.

The right tiering logic puts mature-policy buyers in the top tier – exclusive or near-exclusive inventory, premium pricing, longer term commitments – and routes shared inventory through mid-tier buyers whose policies are still developing. Lowest-tier buyers, with no policy and a history of opportunistic disputes, become a residual destination only for inventory that does not clear the upper tiers. The result is a waterfall that correlates revenue per lead with relationship durability, which is the only correlation that matters in a vertical undergoing structural repricing.

Evidence and Early Movers: Harvey, vLex, Anthropic, and the Big-Firm Cohort

The repricing is not happening uniformly. Three named platform deployments and one general-purpose release set the pace.

Harvey AI’s deployment across roughly 100,000 lawyers and the majority of the AmLaw 100 is the most-named force in the buy side of the legal lead vertical. Harvey’s Spectre autonomous agent for matter management, public reporting on which has tracked through early 2026, is positioned as a layer that can take an intake record and execute matter setup, conflict checks, and initial triage with limited human input. The product capability matters for the lead vertical because it changes the buyer-side intake workflow that lead sellers are routing into. A firm running Spectre on its intake queue absorbs leads at higher velocity but with different verification hooks than a firm running a manual intake team – and the contractual representations the Spectre-running firm wants from its lead suppliers are different too. Lead operators routing into Harvey-deployed firms should expect more sophisticated buyer-side QA and more pointed AI-attestation requests.

vLex’s CoCounsel, named in the Fifth Circuit’s $2,500 sanction, occupies a different segment. CoCounsel is positioned as a research and drafting tool, used by firms across the size spectrum from solo practitioners to mid-market plaintiff and defense shops. The Fifth Circuit naming is the data point that matters – once a court has identified a specific commercial AI tool in connection with a sanction order, opposing counsel and judicial clerks will look for the same tool’s fingerprints in subsequent filings. Firms that deploy CoCounsel internally are now under increased scrutiny for their internal QA, which translates downstream into stricter intake and lead-acceptance protocols.

Anthropic’s Claude for Microsoft Word, released in April 2026, addresses a different layer of the workflow. Claude for Word is positioned around lease review, contract review, and drafting assistance – not litigation research. The release matters for the legal vertical because it makes Claude available inside the document layer that almost every transactional and litigation associate works in. The release also matters because Anthropic is one of the more conservative model providers on hallucination control, and its public posture on accuracy and refusal behavior has been part of its enterprise pitch. Whether Claude for Word reduces or increases the system-wide hallucination rate depends on adoption patterns and on what firms substitute it for. The first-order effect for lead operators: a meaningful share of legal work product will now be produced with a Claude layer in the workflow, which means buyer-side AI governance policies will need to address Claude specifically.

The big-firm cohort – the AmLaw 100 firms running Harvey, the mid-market firms running CoCounsel, the transactional firms running Claude for Word – is the cohort that will set the contractual expectations for the rest of the legal lead market. These firms have the budgets, the legal-operations teams, and the carrier relationships to lead the policy build. The middle and lower tiers of the legal market will adopt their language, their attestation forms, and their dispute frameworks on a six-to-twelve-month lag. Lead operators tracking only their immediate buyers miss the leading-indicator value of watching the AmLaw 100 cohort’s contract templates.

What the Charlotin database tells operators

The Charlotin hallucination case database is the most useful single research artifact for operators trying to size the trajectory. Three patterns visible in the database through early 2026 are particularly relevant. First, the geographic distribution is wide – sanction orders are coming out of district courts across at least twenty states, not concentrated in a single jurisdiction. Second, the firm-size distribution is heavy on solo and small firms but increasingly includes mid-market and BigLaw filings, suggesting the conduct is no longer limited to under-resourced practices. Third, the case-type distribution spans civil litigation, criminal matters, immigration, and family law – meaning the sanction risk is not isolated to a single legal sub-vertical.

Each of those patterns is independently relevant. Geographic dispersion means lead operators cannot avoid the issue by jurisdiction filtering. Firm-size dispersion means even premium-tier buyers carry the risk. Case-type dispersion means every legal sub-vertical that lead operators sell into is in scope.

Implementation Reality: What the AI-Aware Lead Operation Actually Requires

The strategic reframe is straightforward. The implementation is operational and non-trivial.

Resource requirements

Building an AI-provenance-documented lead operation requires four investments most legal-vertical operators have not budgeted for. The first is an AI inventory of the funnel – a documented map of every AI-mediated step from media buying through delivery, with the model class, vendor, and purpose noted at each step. For a mid-sized legal lead operator running multi-channel acquisition, this is a three-to-five-week mapping engagement, typically performed by a cross-functional team including marketing operations, engineering, and compliance.

The second is a human-review checkpoint design. For each AI-mediated step in the funnel, the operator needs to define what human-review hook applies, what artifact the review produces, and what retention policy attaches. Some steps will not need human review (creative testing, fraud scoring on clearly-bot-pattern traffic). Others will (intake transcription, AI-mediated qualification scoring on borderline cases, any AI-generated text that propagates into the lead record). The design work is roughly two-to-four weeks for a focused team and produces the operating procedures that turn the inventory into a defensible posture.

The third is artifact retention infrastructure. The AI-provenance representation an operator wants to make to a buyer (“this lead was processed through an AI scoring step on Date X using Model Y, with human review by Reviewer Z, with retained artifact in System W”) requires the underlying retention infrastructure to exist. Most legal-vertical lead operators retain consent artifacts, recordings, and form submission data; few retain AI-decision logs at the granularity needed. Building the retention layer is typically a four-to-eight-week engineering project plus storage cost increases that are non-trivial at scale.

The fourth is the buyer-facing documentation package – an AI provenance disclosure schema that buyers can ingest, an attestation template that legal can sign, and a QA process for matching what the operation actually does to what the disclosure claims. This is a two-to-three-week legal-and-operations effort, but it is the deliverable that the buyer relationship actually consumes.

Timeline expectations

A realistic implementation timeline for a mid-sized legal-vertical lead operator:

| Phase | Duration | Key Activities |

|---|---|---|

| AI inventory of the funnel | 3-5 weeks | Map every AI-mediated step, identify model class and vendor at each step |

| Human-review checkpoint design | 2-4 weeks | Define review hooks, artifacts, and retention rules per step |

| Artifact retention build | 4-8 weeks | Engineer the AI-decision log and retention infrastructure |

| Buyer-facing documentation | 2-3 weeks | Schema, attestation template, QA process |

| Buyer onboarding | 4-8 weeks | Communicate AI-provenance posture to existing buyers; renegotiate terms |

| Total elapsed time | 4-6 months | Conservative estimate for a platform without prior AI-governance investment |

Source: Composite of operator interviews, ABA Formal Opinion 512 guidance, and analysis of carrier-driven AI underwriting questionnaires

Common obstacles

Three obstacles consistently slow these implementations beyond the nominal timeline. The first is the AI inventory itself. Most legal lead operations have absorbed AI tools incrementally over two to three years, with different teams adopting different vendors for different purposes, often without central documentation. The first inventory pass usually surfaces five to ten AI-mediated steps that the operator’s leadership did not know existed. The investigation work to confirm the inventory is longer than expected, and the inventory cannot be skipped – every step that is not on the inventory is a hole in the eventual buyer attestation.

The second is the retention infrastructure cost. AI-decision logs at the granularity needed for buyer attestation are larger than most operators expect. A funnel processing tens of thousands of leads per month, with five AI-mediated touchpoints per lead, generates millions of decision-log entries per month. Storage and access costs are not catastrophic, but they are line-item visible and require budget approval that operators sometimes underestimate.

The third is the buyer-side variance in what they want documented. Some buyers will want extensive provenance documentation and will pay for it. Others will want a simple categorical attestation and will resist providing the legal review needed to ingest a more detailed schema. The operator running a single AI-provenance schema across all buyers ends up over-engineering for the simple buyers and under-engineering for the sophisticated ones. The tier-aware design – different attestation depth by buyer tier – is what addresses this, but it requires the buyer tiering to be in place before the documentation work begins.

The implementation is hard. The operators who complete it before the rest of the market reprices will run a six-to-twelve-month structural margin advantage on the legal vertical.

Future Implications: The 2026-2028 Trajectory of the Legal Lead Vertical

The early-2026 sanction wave is the first inflection point in a multi-year sequence. The shape is reasonably predictable from the structure of the market.

In the next twelve months, the malpractice insurance repricing cycle completes a full pass through 2027 renewals. Carriers that issued AI-specific underwriting questions in 2025 will tighten those questions for 2027; carriers that did not will introduce them. AI-policy attestations will become a standard underwriting input. Premium increases for firms without documented AI governance will run materially above baseline; premium increases for firms with strong governance will track baseline. The premium dispersion across the buyer set will widen, and that widening will translate into a wider dispersion in what those firms can pay for legal leads.

In the next twenty-four months, the dispute and contract template across the legal lead vertical standardizes around AI-aware language. The leading firms publish their AI-attestation forms; the standard forms used by aggregators and lead networks incorporate similar provisions; the operators who entered 2026 with thin AI-provenance posture either upgrade or exit the higher-tier buyer relationships. By mid-2027, AI provenance documentation is table stakes for any operator selling into the AmLaw 200 cohort and is a meaningful tiering input across the broader market.

In the next thirty-six months, the structural relationship between AI tooling and lead pricing stabilizes. The early-moving operators have built provenance documentation as a competitive advantage; the rest of the market has caught up; the documentation requirement becomes a cost of doing business rather than a margin lever. The premium for high-provenance leads narrows. The compression of net realized CPL that started in 2026 plateaus, and a new equilibrium establishes itself with slightly lower headline CPLs and meaningfully tighter contract terms across the vertical.

The longer-term shift is more interesting. The early-2026 sanction wave is a precedent for what happens when courts confront a specific failure mode of generative AI deployed at scale in a regulated profession. Other regulated professions – medicine, accounting, engineering – operate under similar dynamics, with professional liability insurance, malpractice exposure, and lead-flow economics that intersect in similar ways. The patterns that play out in legal in 2026-2028 are a leading indicator for adjacent vertical lead markets in 2027-2030. Operators with a multi-vertical portfolio should track the legal trajectory closely.

For lead generators specifically, the strategic implication is to design the operation for the world after the next AI-related court cycle, not just the current one. An operation architecture that treats AI provenance as a first-class data attribute, that retains the artifacts that support attestation, and that prices AI-policy maturity into buyer tiering is a more durable architecture than one optimized only for the April 2026 sanction wave.

Key Takeaways

The early-2026 AI hallucination sanction wave – anchored by the April 4, 2026 Brigandi order at $96,000 in direct sanctions and approximately $110,000 with related penalties, and aggregating to more than $145,000 across U.S. courts so far – is a structural repricing event for the legal lead generation vertical. Treating it as an attorney-discipline story underestimates the downstream effect on lead supply terms.

The Damien Charlotin hallucination case database has crossed 1,200 documented cases globally, with reporting describing ten cases from ten different courts on a single day in early 2026. The slope of the curve is steeper than the slope through 2024-2025, and the geographic, firm-size, and case-type distributions are widening. The risk is no longer concentrated in any single jurisdiction or practice profile.

Harvey AI’s deployment across approximately 100,000 lawyers and the majority of the AmLaw 100, the Fifth Circuit’s $2,500 sanction implicating vLex’s CoCounsel, and Anthropic’s April 2026 release of Claude for Microsoft Word together establish that generative AI is now embedded across the buy side of legal lead generation. Buyer-side intake workflows are changing, and lead operators routing into AI-deployed firms should expect more sophisticated QA and more pointed AI-attestation requests.

The economic chain runs from sanction events to malpractice insurance repricing, from repricing to firm cost-of-acquisition revision, from acquisition revision to contractual repricing of legal lead supply. Headline CPLs will not move dramatically in 2026; the terms around the price – return windows, dispute reasons, AI-attestation language, provenance documentation – will. A reasonable working assumption is five to fifteen percent net realized CPL compression across personal injury and mass tort by Q4 2026, with smaller compression in other sub-verticals on a six-to-twelve-month lag.

Three operator postures will underperform: it-is-a-law-firm-problem (misses the buyer-side cost-pass-through), wait-for-clarity (waits past the moment when contracts can be renegotiated proactively), and deny-AI-everywhere (creates representations that are inaccurate or so narrow as to be useless). The right posture is documented AI provenance, AI-aware quality control, and AI-policy-maturity buyer tiering.

Implementation requires four investments most legal lead operators have not budgeted for: an AI inventory of the funnel, human-review checkpoint design, artifact retention infrastructure, and a buyer-facing documentation package. A realistic timeline is four to six months end-to-end, with AI inventory and retention infrastructure as the longest paths.

The 2026-2028 trajectory points to a malpractice premium dispersion that widens through 2027 renewals, dispute and contract template standardization around AI-aware language by mid-2027, and a stabilization of the structural relationship between AI tooling and lead pricing by 2029. The premium for high-provenance leads narrows over that period, but the operators who build documentation as a competitive advantage in 2026 capture the margin window before it closes.

For legal lead operators in personal injury, mass tort, criminal defense, employment, family, estate planning, and small-business legal, the next ninety days are the planning window. The next one hundred and eighty days are the build window. The first contract renewals that incorporate AI-aware language are landing in Q3 2026; the operators who arrive at those negotiations with documented provenance and tiered buyer logic capture the favorable terms. The operators who arrive later sign what is offered.

Frequently Asked Questions

What was the Brigandi sanction and why does it matter for lead generators?

On April 4, 2026, U.S. Magistrate Judge Mark Clarke of the District of Oregon imposed a $96,000 direct monetary sanction on attorney Stephen Brigandi for filing twenty-three fabricated citations and eight false quotations across three federal filings, with related penalties bringing the total order to approximately $110,000. The case matters for lead generators because it is, as of late April 2026, the largest publicly reported single-attorney AI hallucination sanction in U.S. federal court – and because it confirms the trajectory that malpractice insurance carriers have been pricing into firm premiums for the past eighteen months. The repricing in the carrier market translates directly into firm cost-of-acquisition revision, which translates into contractual repricing of legal lead supply terms.

How big is the Damien Charlotin AI hallucination case database and what does it show?

The Charlotin database documents court decisions worldwide that identify fabricated AI-generated citations in legal filings. As of early 2026, public reporting on the database describes more than 1,200 documented cases globally, with Charlotin himself reporting “10 cases from 10 different courts on a single day” in early 2026. The relevant patterns visible through early 2026: geographic distribution across at least twenty U.S. states, a firm-size distribution that has expanded from solo and small firms into mid-market and BigLaw filings, and a case-type distribution spanning civil litigation, criminal matters, immigration, and family law. The trajectory shows the conduct is not isolated to any single jurisdiction, firm size, or practice area.

Why does Harvey AI’s $11 billion valuation matter for the legal lead vertical?

Harvey AI is the most widely deployed legal-specific generative AI platform, used by approximately 100,000 lawyers including the majority of the AmLaw 100. The $11 billion valuation reported in 2026 reflects the market’s pricing of Harvey’s deployment surface area inside the buy side of legal services. For lead generators, the deployment matters because Harvey-deployed firms – particularly firms running the Spectre autonomous matter-management agent – have different intake workflows, different verification hooks, and different AI-attestation expectations than firms running manual intake. Lead operators routing into the Harvey-deployed cohort should expect more sophisticated buyer-side QA and more pointed contractual representations about AI use in lead generation.

What did the Fifth Circuit’s $2,500 sanction involving vLex CoCounsel actually decide?

A Fifth Circuit decision in late 2025 / early 2026 imposed a $2,500 sanction on counsel for citations later identified as hallucinated, with reporting linking the underlying drafting to vLex’s CoCounsel platform. The dollar figure is small relative to the Brigandi order. The signal is large because the sanction was at the federal appellate level and because the court’s discussion named a specific commercial AI tool in connection with the conduct. Appellate sanctions tend to set tone for trial courts, and naming a specific tool tends to focus opposing counsel and judicial clerks on that tool’s fingerprints in subsequent filings. The cadence of lower-court sanctions through early 2026 is consistent with that pattern.

How does Anthropic’s Claude for Microsoft Word change the legal lead vertical?

Anthropic released Claude for Microsoft Word in April 2026, integrating Claude-powered drafting and review – including lease and contract review – directly into the Word authoring environment. Word is the document layer that almost all legal work product flows through, so embedding a generative model in that layer shortens the workflow distance between AI assistance and filed document. The release matters for the legal lead vertical because a meaningful share of legal work product will now be produced with a Claude layer in the workflow, which means buyer-side AI governance policies will need to address Claude specifically and lead-supply attestations will need to anticipate Claude as a workflow component the buyer is using.

What does AI-attestation language in a legal lead supply agreement actually look like?

The language varies by buyer and stage, but the typical structure includes three elements. First, a representation by the seller about whether AI tools are used in lead generation, with specific categories (none, AI-mediated scoring, AI-mediated transcription, AI-generated content). Second, a representation about the quality controls applied to any AI-mediated step, including human-review checkpoints and artifact retention. Third, a representation that no fabricated information has been introduced into the lead record by AI. The operator who can sign these representations honestly and back them with documentation occupies a higher tier in the buyer waterfall than the operator who cannot. The operators who write categorical denials they cannot defend tend to surface those denials in dispute proceedings later, with worse outcomes than a documented and bounded representation would have produced.

How will malpractice insurance repricing actually flow through to lead pricing?

Lawyers Professional Liability carriers price firm premiums on a forward-looking expected-loss basis. The early 2026 sanction data feeds into that model as evidence of rising frequency, severity, and prejudice-likelihood of AI-related events. Carriers that priced AI risk into 2026 renewals are revisiting 2027 renewals upward; carriers that did not are accelerating the underwriting changes. The premium increases land on law firms, who absorb them by lowering cost of acquisition – most often by pushing back on lead supply terms. Headline CPLs will not move dramatically in 2026, but return windows widen, dispute reasons broaden, and AI-attestation language enters the supply contract. The net realized CPL – what the lead seller actually collects after returns and disputes – compresses by an estimated five to fifteen percent across personal injury and mass tort by Q4 2026, with smaller compression in other sub-verticals on a six-to-twelve-month lag.

Which legal sub-verticals are most exposed to the early-2026 sanction wave?

Personal injury and mass tort carry the highest absolute exposure because the volume of motion practice, associate-hour pressure, and AI-assisted research appeal are all maximal. They will reprice slowest because case economics absorb cost increases. Criminal defense will reprice fastest because firms are smaller, more premium-sensitive, and more exposed to courts that are aggressive on hallucinated authority where defendants can be directly prejudiced. Employment law spans plaintiff-side (contingency, write-off-sensitive) and defense-side (hourly, different incentives), with both sides moving to AI-attestation language. Estate planning and elder law are the most insulated because the work is largely transactional, but they will adopt the language on standard compliance lag. Lead operators should expect different timelines and intensities in each sub-vertical and should not run a single uniform contractual response across the whole portfolio.

What is AI provenance documentation in lead generation?

AI provenance documentation is a record of where AI was used in capturing and processing a lead, what model class was used at each step, what human-review checkpoints applied, and what artifacts were retained. The documentation can be coarse (a categorical disclosure) or fine (a per-step decision log), with different buyers wanting different depths. The minimum useful provenance posture: an inventory of AI-mediated steps in the funnel, a defined human-review checkpoint per step, retained artifacts that support attestation, and a buyer-facing documentation package that maps the operation to standard buyer schemas. Operators who can produce this documentation occupy a higher tier in the buyer waterfall and command more durable terms than operators who cannot.

How long does it take to build an AI-aware lead generation operation?

A realistic timeline for a mid-sized legal-vertical lead operator is four to six months end-to-end. The work breaks into five phases: AI inventory of the funnel (three to five weeks), human-review checkpoint design (two to four weeks), artifact retention build (four to eight weeks), buyer-facing documentation package (two to three weeks), and buyer onboarding with terms renegotiation (four to eight weeks). The longest paths are typically the AI inventory (because most operators have absorbed AI tools incrementally without central documentation) and the retention infrastructure build (because AI-decision logs at the granularity needed for buyer attestation are larger than expected). Operators who start the buyer conversations in parallel with engineering work, rather than sequentially, tend to compress the overall timeline.

What about lead operators who already do not use AI in their funnels?

The number of operators in this category is smaller than they think. Most legal lead operations have absorbed AI in fraud detection, ad creative testing, intake transcription, scoring, and reporting layers – often without a central inventory. The first work is therefore the AI inventory, which often surfaces five to ten AI-mediated steps that the operator’s leadership did not know existed. Operators who, after a complete inventory, conclude that they genuinely do not use AI in lead generation can sign clean categorical representations and occupy a defined niche in the market – typically with buyers who explicitly want AI-free supply. The niche is real but narrow. Most buyers will not require AI-free supply; they will require documented AI use with appropriate controls.

What is the 2026-2028 outlook for legal lead pricing under the AI-hallucination repricing?

The trajectory has three phases. In the next twelve months, malpractice insurance repricing completes a full pass through 2027 renewals, AI-policy attestations become a standard underwriting input, and premium dispersion across the buyer set widens. In the next twenty-four months, the dispute and contract template across the legal lead vertical standardizes around AI-aware language, with leading firms publishing attestation forms and aggregator standard contracts incorporating similar provisions. In the next thirty-six months, the structural relationship between AI tooling and lead pricing stabilizes, the premium for high-provenance leads narrows, and net realized CPL compression plateaus at a new equilibrium. The operators who build provenance documentation as a competitive advantage in 2026 capture the margin window before the documentation requirement becomes a cost of doing business.

Sources

Tier 1: Primary Court, Regulatory, and Bar Sources

- Federal Rules of Civil Procedure, Rule 11 – https://www.law.cornell.edu/rules/frcp/rule_11

- American Bar Association, Model Rule 1.1 Competence (Comment 8 on technology competence) – https://www.americanbar.org/groups/professional_responsibility/publications/model_rules_of_professional_conduct/rule_1_1_competence/

- American Bar Association, Formal Opinion 512: Generative Artificial Intelligence Tools – https://www.americanbar.org/groups/professional_responsibility/publications/formal_opinions/

- U.S. District Court for the District of Oregon, Sanction Order in In re Brigandi (April 4, 2026, public reporting) – https://www.ord.uscourts.gov/ 4a. Justia, Couvrette v. Wisnovsky et al., No. 1:21-cv-00157 (D. Or.), Document 225 – Opinion and Order on sanctions against Stephen Brigandi by Magistrate Judge Mark D. Clarke (April 4, 2026), accessed April 2026 – https://law.justia.com/cases/federal/district-courts/oregon/ordce/1:2021cv00157/158388/225/

- Mata v. Avianca, Inc., 22-cv-1461 (S.D.N.Y.), the original 2023 federal AI hallucination sanction order that anchors the line of cases – https://www.law.cornell.edu/

Tier 2: Established Industry Research and Trade Press

- Damien Charlotin, AI Hallucination Cases Database – https://www.damiencharlotin.com/hallucinations/

- Reuters, “Oregon judge sanctions lawyer over AI-generated fake citations,” April 2026 – https://www.reuters.com/legal/government/oregon-judge-sanctions-lawyer-over-ai-generated-fake-citations-2026-04-04/

- Stanford HAI, “Hallucinating Law: Legal Mistakes with Large Language Models Are Pervasive” – https://hai.stanford.edu/news/hallucinating-law-legal-mistakes-large-language-models-are-pervasive

- Above the Law, ongoing coverage of AI hallucination sanction orders – https://abovethelaw.com/

- Law.com / The American Lawyer, ongoing coverage of Harvey AI deployment and AmLaw 100 AI adoption – https://www.law.com/americanlawyer/

- Bloomberg Law, ongoing coverage of generative AI in legal practice – https://news.bloomberglaw.com/

- Reuters Westlaw, Practical Law guidance on AI use in litigation – https://legal.thomsonreuters.com/en/products/practical-law

Tier 3: Industry and Vendor Statements

- Harvey AI, company blog and product announcements (Spectre, deployment milestones) – https://www.harvey.ai/blog

- Anthropic, “Claude for Microsoft Word” announcement, April 2026 – https://www.anthropic.com/news/claude-for-microsoft-word

- vLex / Thomson Reuters CoCounsel, product documentation and platform announcements – https://vlex.com/

- American Lawyers Professional Liability (ALPS) and other LPL carrier underwriting guidance on AI use, 2025-2026 publications – https://www.alpsinsurance.com/

- Professional Liability Underwriting Society (PLUS), AI-related underwriting commentary – https://plusweb.org/

Tier 4: Supporting Industry Commentary

- LawNext podcast, ongoing interviews on legal AI deployment and risk – https://www.lawnext.com/

- Artificial Lawyer, ongoing coverage of legal AI tooling – https://www.artificiallawyer.com/

- Legal IT Insider, ongoing coverage of legal technology adoption – https://www.legaltechnology.com/

- ABA Journal, ongoing coverage of AI ethics in legal practice – https://www.abajournal.com/

- The Practising Law Institute (PLI), CLE programming on AI use and malpractice exposure – https://www.pli.edu/

Closing

The early-2026 AI hallucination sanction wave will be remembered for the wrong reason. The headlines treated it as an attorney-discipline story – a sequence of bar-association referrals, judicial scoldings, and the occasional six-figure order against an outlier practitioner. That framing misses what actually happened. The structural event was the confirmation, by federal courts in at least twenty states and at the Fifth Circuit appellate level, that generative AI deployed inside the legal-services supply chain produces a specific, identifiable, sanctionable failure mode that has now been priced into malpractice insurance underwriting and will be priced into legal lead supply contracts on a six-to-twelve-month lag. The legal lead operators who treat the wave as a law-firm problem will spend 2026 and 2027 watching their net realized CPL compress without an obvious cause and signing contracts whose terms tightened while they were not paying attention. The operators who treat it as a structural repricing – and who build the AI provenance documentation, the AI-aware quality control framework, and the AI-policy-maturity buyer tiering that the repriced market will reward – capture the margin window that the slower operators give up. The decision about which group to be in is being made now, in the next ninety days of planning and the next one hundred and eighty days of build. There is no comfortable third option.

Court orders, sanction figures, and platform deployments reflect publicly reported conditions through April 28, 2026. Court sanction practice, malpractice insurance pricing, and AI vendor product capabilities change continuously; verify current conditions through primary sources before making operational decisions. This article provides general industry analysis and does not constitute legal, professional liability, or compliance advice. Consult qualified counsel for specific compliance questions related to AI use in lead generation, attestation language in lead supply agreements, and dispute documentation under evolving professional responsibility standards.