The federal docket sets mass tort lead pricing more reliably than any media-buying spreadsheet – and April 28, 2026 is the date that resets the table.

Daubert Day: April 28, 2026

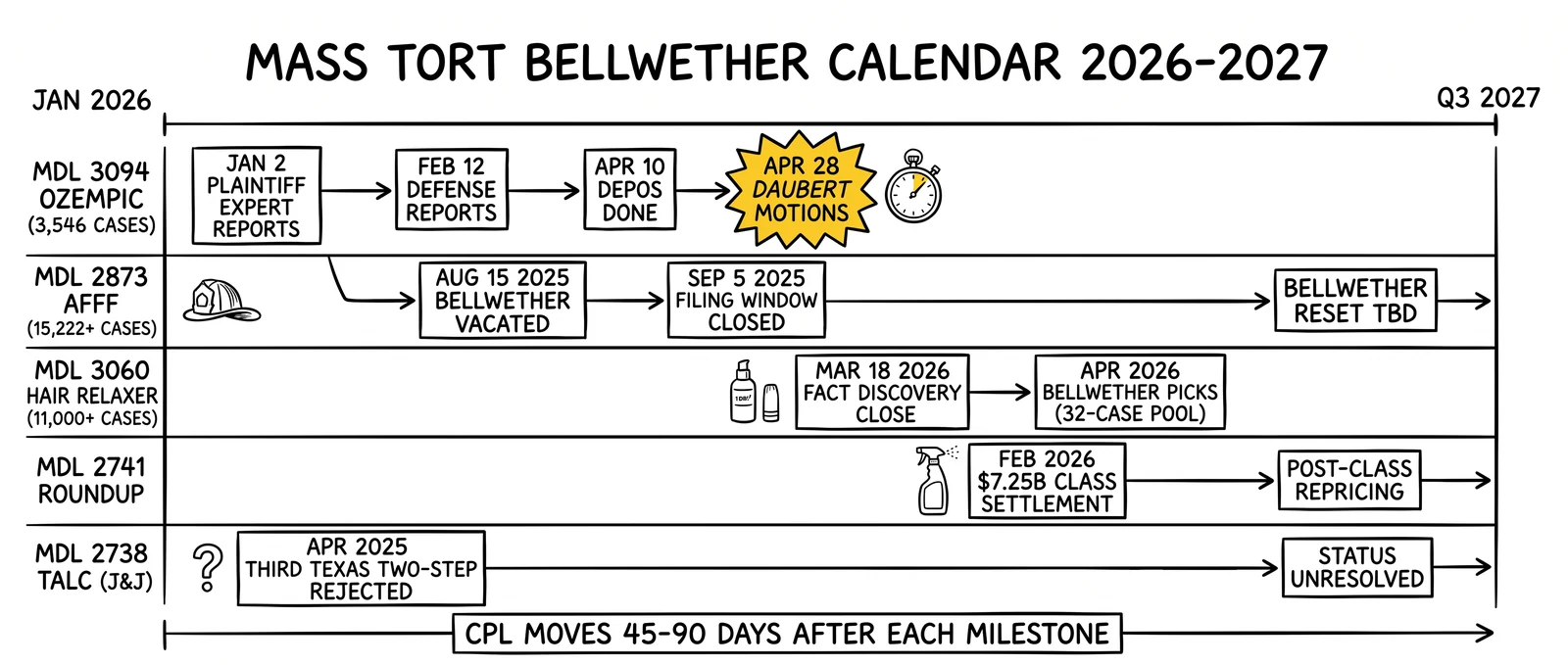

April 28, 2026 is the deadline for Daubert motions in In re: Glucagon-Like Peptide-1 Receptor Agonists (GLP-1 RAs) Products Liability Litigation, MDL 3094, before Judge Karen S. Marston in the U.S. District Court for the Eastern District of Pennsylvania. As of April 2026 the docket holds 3,546 consolidated cases across four injury categories – gastroparesis at roughly 75% of the pool, ileus at 18%, gallbladder injury at 8%, and non-arteritic anterior ischemic optic neuropathy (NAION) administered separately in MDL 3163. The April 28 deadline closes a discovery sequence that began with plaintiffs’ expert reports on January 2, defense reports on February 12, and plaintiff rebuttal on February 23. Expert depositions wrapped April 10. Once the motions land, settlement probability stops being narrative and starts being math.

For mass tort lead operators, this is the cleanest pricing event of the calendar year. Daubert motions test whether expert testimony on general causation meets Federal Rule of Evidence 702 – the federal standard for admissible scientific evidence. If Marston excludes a plaintiff’s general-causation expert, an entire injury category can collapse out of the MDL within a quarter. If she admits plaintiff experts and excludes a defense expert, settlement values rise sharply and the CPL spread between verified and unverified inventory widens. Either outcome rewires the unit economics of every operator carrying GLP-1 inventory. The Ozempic Daubert deadline is not an isolated event. It sits inside a 2026-2027 calendar that includes the AFFF MDL 2873 reset under Judge Richard Gergel after the vacated October 2025 bellwether, the hair relaxer MDL 3060 fact-discovery close on March 18, 2026 followed by April bellwether picks, the post-class-settlement repricing of Roundup MDL 2741, and the unresolved status of J&J talc after the third Texas Two-Step rejection in April 2025. Each milestone repositions the settlement-multiple model that defines maximum sustainable cost per lead.

This analysis maps the docket, builds the math, and gives operators a framework for translating procedural milestones into pricing decisions. It does not predict outcomes. It explains how the market has historically repriced around them, what the 2024 lead arbitrage taught about ignoring the calendar, and how California SB 37 and the post-vacatur TCPA environment have changed the cost stack. The audience is operators buying or selling mass tort leads, plaintiff-firm intake managers, and the agencies sitting between them.

What Daubert Actually Decides

A Daubert motion challenges the admissibility of expert testimony under Federal Rule of Evidence 702, which the 2023 amendments tightened to require the proponent to establish, by a preponderance of evidence, that the testimony reflects reliable principles and methods reliably applied to the facts of the case. The standard takes its name from the Supreme Court’s 1993 decision in Daubert v. Merrell Dow Pharmaceuticals and applies in every federal MDL with a contested-causation theory. In product-liability mass torts, the most consequential Daubert ruling addresses general causation – whether the substance at issue is capable of causing the alleged injury at the doses and exposure routes plaintiffs claim. Specific causation, the question of whether this plaintiff’s injury was caused by this exposure, follows.

Marston’s August 15, 2025 ruling in MDL 3094 illustrated how a single causation order can rewrite a docket. The order required gastroparesis claimants to produce objective gastric-emptying scintigraphy results to advance their cases, effectively converting a clinical diagnosis category into an imaging-verified one. The practical effect on lead inventory was immediate. Leads documenting only patient-reported gastroparesis symptoms became economically inert because plaintiff firms could not screen them through the new gate without ordering imaging that costs roughly $400-800 per study. Operators carrying scintigraphy-verified inventory captured a step-function pricing premium. The April 28, 2026 Daubert briefing will test whether plaintiff experts can sustain general causation under that standard across the full injury spectrum, with the ileus, gallbladder, and NAION categories drawing distinct expert lineups.

For lead buyers, the Rule 702 calendar matters more than any individual ruling because it tells operators when settlement probability becomes a tradable variable. Pre-Daubert, expected per-case settlement is a wide-distribution guess. Post-Daubert, with admissibility established or denied, the band tightens. Plaintiff firms reset intake budgets, often within 30-60 days. Brokers reprice. The lag between a Daubert ruling and the corresponding CPL move runs roughly 45-90 days based on the post-Roundup, post-3M Combat Arms, and post-Camp Lejeune Justice Act precedents. Operators who track docket entries the way insurance lead operators track Federal Reserve rate decisions outperform those who treat the calendar as background noise.

The 2026-2027 Bellwether Calendar

The federal MDL docket runs five mass torts that move CPL meaningfully in 2026-2027. The table below summarizes the procedural milestones with direct pricing implications. Source: Judicial Panel on Multidistrict Litigation case-management orders and individual court dockets, current as of April 2026.

| MDL | Court | Judge | Cases (Apr 2026) | Next Pricing Event | CPL Range (raw) | CPL Range (verified) |

|---|---|---|---|---|---|---|

| 3094 GLP-1 | E.D. Pa. | Marston | 3,546 | April 28, 2026 Daubert motions | $35-65 | $90-180 |

| 2873 AFFF | D.S.C. | Gergel | 15,222+ | Bellwether reset post-Aug 15, 2025 vacatur | $260-340 | $700-900 |

| 3060 Hair Relaxer | N.D. Ill. | Rowland | 11,000+ | April 2026 bellwether picks (32-case pool) | $225-325 | $550-750 |

| 2741 Roundup | N.D. Cal. | Chhabria | Active post-class | Post-Feb 2026 $7.25B class settlement | $265-375 | $600-850 |

| 2738 Talc | D.N.J. | Shipp | Post-Apr 2025 | Status uncertain after third Two-Step rejected | Volatile | Volatile |

Raw CPL ranges anchor on the Lawsuit Information Center July 2024 rate card, the most recent published industry benchmark, with verified ranges reflecting the 2-3x multiple consistently observed across the four largest dockets. The numbers move with each procedural event. Several specifics deserve attention.

Ozempic MDL 3094 carries the cleanest near-term catalyst. Plaintiffs’ expert reports filed January 2, defense reports February 12, plaintiff rebuttal February 23, depositions complete April 10, Daubert motions due April 28. The injury-category split – gastroparesis 75%, ileus 18%, gallbladder 8%, NAION in the parallel MDL 3163 – means a single adverse ruling on any one category truncates roughly one-fifth to three-quarters of expected settlement value. Verified scintigraphy inventory for the gastroparesis category should hold value through Daubert. Unverified gastroparesis inventory was already discounted after the August 2025 Marston order and faces further compression if defense Daubert challenges land on imaging-interpretation methodology. The May 2024 Lawsuit Information Center rate card placed GLP-1 retainers at $350-750 per signed case, rising to $500-700 by the July 2024 update – a tightening that preceded the Marston scintigraphy order and almost certainly understated the post-order spread between verified and unverified inventory.

AFFF MDL 2873 is the largest active mass tort by case count, holding 15,222+ personal-injury cases as of April 2026 across firefighter occupational exposure and resident water-contamination claims. Judge Richard Gergel vacated the October 2025 bellwether on August 15, 2025 and closed the new-filing window September 5, 2025, freezing the inflow of fresh inventory and pushing pricing into a six-month holding pattern. The verified-versus-unverified spread is wider here than in any other major docket because firefighter occupational claims require either International Association of Fire Fighters membership records or DD-214 service documentation showing fire-suppression duty at qualifying installations. Operators carrying that documentation routinely clear $700-900 per lead against the $260-340 raw range. The 2-3x multiple is not a benchmark – it is a market clearing price set by plaintiff-firm rejection rates that run 60-75% on unverified intake.

Hair relaxer MDL 3060 closed fact discovery on a 32-case bellwether pool March 18, 2026, with bellwether selection in April. Judge Mary Rowland in the Northern District of Illinois consolidated 11,000+ cases alleging chemical hair relaxers caused uterine cancer, ovarian cancer, and uterine fibroids. The April bellwether pick is the next pricing event. Verification requirements include salon-employment records for occupational exposure claims and a documented product-use history paired with a qualifying diagnosis date. Verified inventory in this docket has historically traded at 2.5x raw, with the spread narrowing as cases approach trial because plaintiff firms become more selective when bellwether trials surface adverse fact patterns.

Roundup MDL 2741 sits in a distinct phase. Bayer announced a $7.25 billion class settlement in February 2026, layered on top of the cumulative $11 billion in individual settlements paid since the original 2018-2020 wave. The class component reset the post-class CPL range upward as plaintiff firms refilled intake pipelines for newly eligible claimants. The Roundup market remains the deepest in mass torts, with multiple specialist plaintiff firms and a long verification history, but expected per-case settlement values for newer claimants are below the original wave’s averages.

Talc – primarily In re: Johnson & Johnson Talcum Powder Products Marketing, Sales Practices, and Products Liability Litigation, MDL 2738 – is the volatility outlier. Johnson & Johnson’s third Texas Two-Step bankruptcy strategy was rejected in April 2025, the latest in a sequence that began with the original 2021 LTL Management filing. The $9 billion settlement framework J&J had floated under bankruptcy collapsed with the dismissal. As of April 2026 the path to resolution remains unclear, which has made talc CPL one of the most volatile in mass torts – operators price defensively and plaintiff firms pause intake during procedural events that suggest renewed bankruptcy attempts.

Beyond the five primary dockets, two adjacent litigations move smaller volumes of mass tort CPL. Necrotizing enterocolitis (NEC) baby formula litigation, consolidated in MDL 3026 before Judge Rebecca Pallmeyer in the Northern District of Illinois, completed several bellwethers with mixed results that have kept verified-versus-unverified spreads narrower than the AFFF or hair relaxer markets. Depo-Provera meningioma litigation, consolidated in MDL 3140 before Judge M. Casey Rodgers in the Northern District of Florida, is earlier in its procedural arc with intake demand running ahead of supply through 2026. Operators allocating across the full mass tort book treat NEC and Depo-Provera as portfolio adjusters rather than primary plays.

The Settlement-Multiple Model

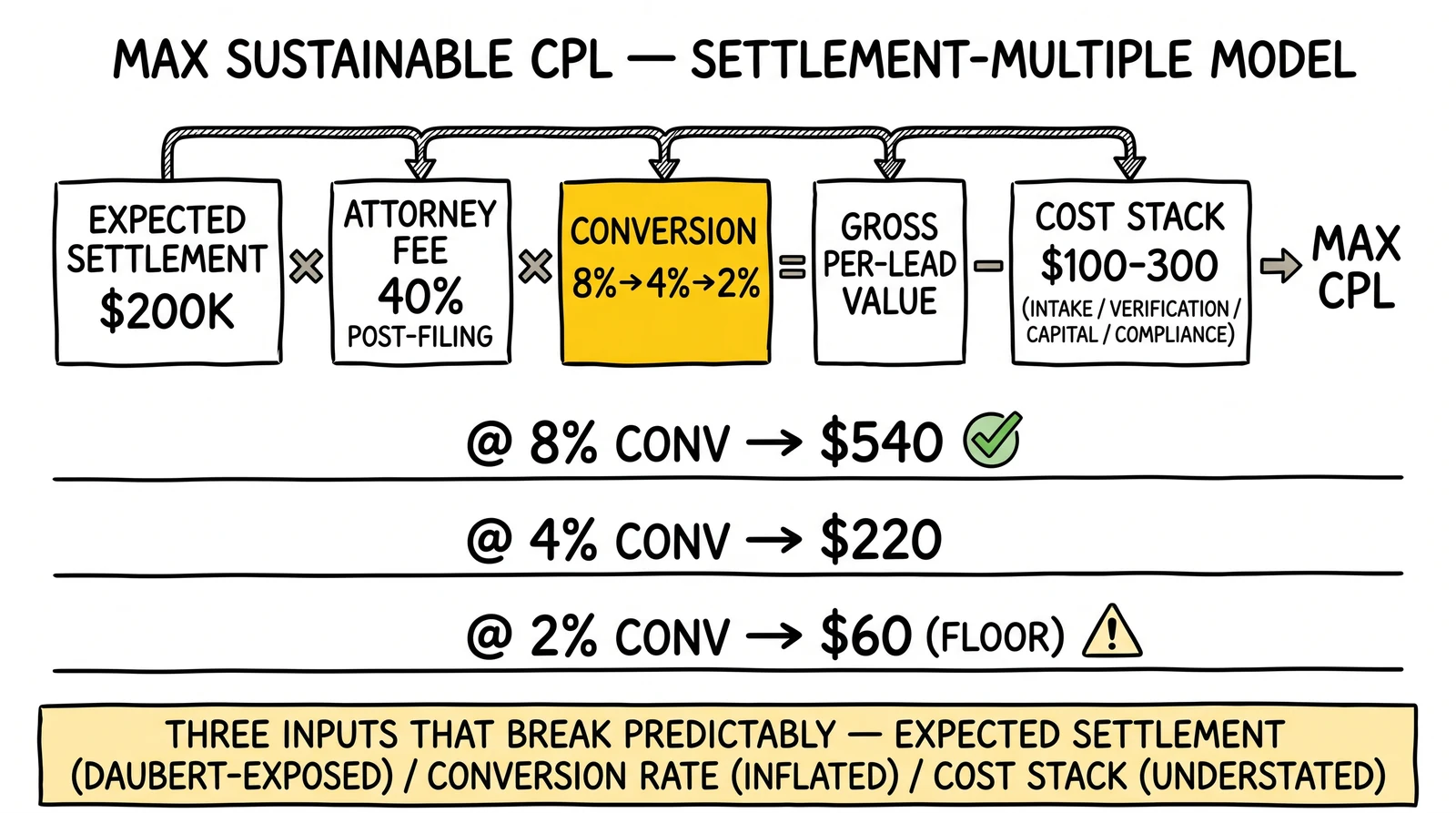

Maximum sustainable CPL is a derived number, not a market price. The formula:

Max CPL = (Expected per-case settlement × Attorney fee % × Lead-to-signed-case conversion rate) − Cost stack

Each variable carries a defensible range that shifts with the bellwether calendar. Expected per-case settlement is the gross dollar amount the plaintiff firm projects for the median case in the docket, weighted by injury category. Attorney fee percentage runs 33⅓% on pre-litigation settlements and 40% on cases that proceed past filing – the common contingent-fee structure in U.S. plaintiff practice. Lead-to-signed-case conversion is the rate at which raw leads survive intake screening and convert into signed retainer agreements. Cost stack is the operator’s full per-lead cost beyond raw acquisition: intake labor, verification, qualification overhead, marketing operations, capital cost on cash tied up in unsold inventory, and compliance overhead.

The math is brutal when run honestly. Take a hypothetical Ozempic gastroparesis case with a $200,000 expected settlement, a 40% post-filing fee structure, an 8% lead-to-signed conversion rate, and a $100 cost stack covering intake and verification. Maximum sustainable raw CPL is $200,000 × 0.40 × 0.08 − $100, or $6,300 per signed case yielding a maximum lead price of $540. At the published $35-65 GLP-1 raw range, the model suggests substantial margin – until the conversion rate moves. At a 4% conversion, sustainable max CPL drops to $220. At a 2% conversion, it drops to $60, hitting the published market floor.

The same exercise applied to AFFF firefighter inventory with a $500,000 expected settlement, 40% fees, a 12% conversion rate on verified leads (the 2024 Mohr Marketing-style benchmark for verified firefighter intake), and a $250 cost stack yields maximum sustainable verified CPL of roughly $2,150. Verified inventory clearing at $700-900 leaves margin headroom that explains why the AFFF verified market has remained more stable through the post-vacatur freeze than unverified pricing. Hair relaxer with $300,000 expected settlement, 40% fees, 6% conversion on verified inventory, and a $200 cost stack yields a $1,000 ceiling against the $550-750 verified market. The verified premium on hair relaxer remains underbought relative to economic logic, which is why several specialist agencies expanded hair-relaxer verification operations through 2025-2026.

The model breaks predictably in three places. First, expected per-case settlement is the most volatile input and the one most exposed to Daubert outcomes. A defense Daubert win can reduce expected settlement by 50-80% within a quarter; a plaintiff Daubert win compresses the timeline to settlement and pushes expected values up. Second, conversion rate is the variable operators most often inflate. The 8% rate carried into many 2024 spreadsheets reflects pre-Marston-order screening; post-order, gastroparesis conversion on unverified inventory ran closer to 2-3% at most plaintiff firms. Third, cost stack is the variable operators most often understate. Intake labor at $25-35 per hour for trained mass tort intake specialists, verification at $50-150 per case depending on documentation depth, and capital cost on inventory held 60-90 days before retainer signing routinely add $150-300 to the per-lead cost stack that headline CPL ignores.

Plaintiff firms run the same model in reverse. They derive maximum lead acquisition cost from expected settlement value, divide by historical conversion benchmarks, subtract their own intake and case-development overhead, and bid the residual. Operators who understand the buyer’s math negotiate from a stronger position than operators who anchor on published rate cards. The cost-per-lead benchmarks across the broader industry track this dynamic in slower-moving verticals; the difference in mass torts is that the Daubert and bellwether calendar accelerates revaluation cycles from years to quarters.

Verified vs. Unverified: The 2-3x Spread

Verification is the single largest determinant of mass tort lead value beyond docket selection. The 2-3x spread between verified and unverified inventory holds across AFFF, hair relaxer, and post-Marston Ozempic, and the underlying mechanics are consistent. Plaintiff firms reject roughly 60-75% of unverified intake at qualification because the documentation gap forces firms to either spend on verification themselves – pulling military records, ordering imaging, requesting employment histories – or pass on cases where the documentation cost approaches the marginal case value. Verified inventory bypasses that gate.

AFFF firefighter verification typically requires either IAFF membership records confirming active fire-suppression duty during the exposure window, or DD-214 service records for military firefighters showing assignment to qualifying installations. Operators with established verification operations source these documents through plaintiff-side networks and disclosed-consent processes. The verification adds $80-150 per lead in cost but multiplies the price by 2-3x – a margin structure that has supported the AFFF specialist tier through the post-vacatur freeze.

Ozempic gastroparesis verification post-Marston requires gastric-emptying scintigraphy, the radiological study that quantifies stomach-emptying delay against age-and-gender-adjusted norms. The study is ordered by the patient’s treating physician and costs $400-800 depending on facility. Operators do not order the study directly – that would create a clear practice-of-medicine and possibly capper-runner exposure – but they document scintigraphy results obtained in the ordinary course of treatment and route those leads to the verified tier. The post-order spread between scintigraphy-verified and patient-reported gastroparesis inventory is wider than the published 2-3x because plaintiff firms now treat unverified gastroparesis as effectively unsignable absent operator-funded imaging.

Hair relaxer verification combines product-use history (brand, frequency, duration), salon employment for occupational claims, and qualifying diagnosis dates within the statute-of-limitations window. The verification process is more administrative than medical – affidavits, employment records, dated medical documentation – but the conversion-rate impact is comparable. The market has not yet fully priced hair relaxer verification at the level the AFFF market prices firefighter verification, which represents an inefficiency that specialist operators continue to exploit.

The verified-unverified spread is a stable feature of mature mass tort markets and a leading indicator for newer ones. NEC and Depo-Provera both show narrower spreads because the verification protocols are still consolidating across plaintiff firms. As any docket matures, the spread widens, then stabilizes, then compresses near settlement as plaintiff firms become indifferent between verified and well-documented unverified inventory in the rush to file before deadlines. Operators reading the spread correctly time their entry into and exit from verification investment. For deeper context on qualification economics, see the legal lead qualification case-value framework and the legal lead ROI model that subtracts intake, overhead, and 24-month collections from gross fee.

The Vendor Landscape

The verified active vendor list as of April 2026 splits across three operating models. Media-buying agencies – CAMG, LeadingResponse, Whitehardt, iLawyer Marketing, Foster Web Marketing – run paid-traffic operations across television, programmatic display, paid search, and increasingly connected-TV inventory. Their margin structure is closer to the agency model than the broker model: they bill plaintiff firms on a managed-services basis with paid-media pass-through plus retainer or performance components. Pure lead aggregators – Tort Experts, Mass Tort Strategies, Mass Tort Alliance, On Point Legal Leads, Legal Calls, Best Case Leads, Casewise Partners, Top Shelf Logic, Pinpoint Legal Marketing, TruLaw, Revolt Inc. – operate broker margins between traffic acquisition and plaintiff-firm sales, with the spread depending on verification depth and exclusivity tier. AI-enabled qualification platforms – MassTortLeads.ai, MTAA.AI, DoppCall – sit between the two models, applying conversational AI to intake qualification and routing while charging on a per-qualified-lead basis.

Mohr Marketing and TSEG occupy a hybrid position with deep verification operations and direct plaintiff-firm relationships that compress the spread from the firm side. Buyer due diligence across all three models centers on three documentation tests. Consent-capture quality: does the vendor produce TrustedForm or equivalent session-replay records demonstrating express written consent at the moment of submission? Verification depth: what specific documents support the verified tier – IAFF cards, DD-214s, scintigraphy reports, salon employment records – and at what audit pass-rate? Disposition transparency: will the vendor share the plaintiff firm’s intake-disposition data, including rejection reasons, on a 30- or 60-day cohort basis?

Vendors that resist the third question are pricing from information asymmetry. Vendors that volunteer it tend to operate at smaller margins on better-aligned terms because the disposition data validates their conversion claims. The buyer-side framework for evaluating vendors borrows directly from the broader evaluating lead vendors checklist, with mass-tort-specific overlays for MDL exposure, expert-report sensitivity, and verification documentation depth.

The vendor list above explicitly excludes operators whose presence in the mass tort market could not be independently verified through public docket filings, plaintiff-firm references, trade-association membership rolls, or sustained advertising activity. Operators evaluating an unfamiliar vendor should require references from at least two plaintiff firms with active retainer agreements, verification-document samples on a representative case sample, and TrustedForm or equivalent consent-record documentation on a 100-lead sample.

What Killed the 2024 Lead Arbitrage

The 2024 mass tort lead arbitrage – the spread between cheap top-of-funnel traffic and plaintiff-firm willingness to pay for raw inventory at scale – compressed for three identifiable reasons. Operators who modeled 2026 economics on 2023-2024 conversion rates and settlement multiples found the math unrecognizable.

First, adverse and clarifying Daubert rulings reduced expected settlement values for marginal claims while raising verification requirements. Marston’s August 15, 2025 scintigraphy order is the cleanest example: a single causation-evidence ruling rewrote the entire gastroparesis subcategory’s economics by converting an unverified claims tier into a verification-mandatory tier. Similar dynamics played out in adjacent dockets through 2025. The aggregate effect was to shift expected per-case settlement values lower for unverified inventory and to widen the verified-unverified spread to historic levels.

Second, California Senate Bill 37 took effect January 1, 2026 and tightened the regulatory perimeter on legal advertising and intake-funnel design. SB 37 banned guaranteed-outcome advertising in California legal marketing, imposed new disclosure requirements on intake funnels, and raised the documentation burden on operators routing leads to attorneys. The practical effect on operators running California-targeted creative was a 10-20% increase in cost-per-lead because creative-testing cycles slowed, landing pages required additional disclosure modules, and consent-capture infrastructure had to document fee structures, attorney involvement, and outcome disclaimers at submission. National campaigns increasingly route California traffic through a separate funnel with state-specific disclosures. The California regulatory direction is also a leading indicator – New York, Illinois, and Massachusetts have all opened comparable inquiries.

Third, the post-vacatur TCPA environment removed the regulatory tailwind that had been pricing into broker margins. The Eleventh Circuit in Insurance Marketing Coalition v. FCC vacated the FCC’s one-to-one consent rule before its January 2025 implementation date, eliminating an anticipated supply shock that lead operators had priced into 2024 forecasts. Brokers who had structured 2024 contracts around the assumption that one-to-one consent would compress competitive supply found 2025-2026 clearing prices below those assumptions. The TCPA environment remains active – class action volume runs in the high hundreds per quarter, and individual statutory damages of $500-1,500 per violation continue to drive enforcement risk – but the regulatory pricing impulse the 2024 market expected did not arrive. For operators sizing TCPA compliance investment against expected enforcement, the TCPA defense strategies analysis with $6.6 million average settlement data is the relevant reference point.

The combined effect of Daubert revaluation, SB 37 cost increases, and the TCPA non-event was to reset the unit economics of mass tort lead generation at a level 15-30% below 2023-2024 expectations on unverified inventory while simultaneously pushing verified inventory to 2-3x the unverified level. Operators who carried verified inventory through the transition outperformed by roughly the same factor.

Settlement Comparables

Settlement comparables anchor the expected-value side of the model. Three reference points define the 2023-2026 mass tort settlement environment.

3M Combat Arms Earplug litigation, MDL 2885, settled for approximately $6 billion in 2023 across roughly 260,000 claimants. The settlement included a defective-product allocation framework with verified-versus-unverified tiering that became a template for subsequent mass tort resolutions. The 3M outcome lifted the implied settlement value for similarly structured veteran and occupational-exposure dockets, including AFFF firefighter claims.

Bayer Roundup litigation in MDL 2741 paid an estimated cumulative $11 billion in individual settlements across the 2018-2024 period and added a $7.25 billion class settlement in February 2026 for newly eligible claimants. The class component reset the post-class CPL range as plaintiff firms refilled intake pipelines for the new eligibility window. Expected per-case settlement values for the post-class wave run below the original wave’s averages because the class structure caps individual recovery at lower levels.

Johnson & Johnson talc litigation reached a different outcome. The April 2025 dismissal of J&J’s third Texas Two-Step bankruptcy attempt – the LTL Management strategy of bankrupting a subsidiary to corral talc liability – collapsed the $9 billion settlement framework J&J had floated under bankruptcy. The talc docket has remained unresolved into 2026, with no clear settlement path. The talc outcome stands as the cautionary case: a docket can sit in procedural limbo for years while operators carrying inventory absorb capital cost on aging leads. The general principle is that defensive bankruptcy strategies introduce uncorrelated risk to mass tort lead pricing – risk that does not diversify across the rest of the book.

These comparables matter because they bound the expected per-case settlement input to the multiplier model. Operators running the model with $200,000 expected settlement for Ozempic gastroparesis are anchoring on the lower end of the recent comparable range. Operators running it with $500,000 for AFFF firefighter cases are anchoring on the high end. The accuracy of the input determines the accuracy of the maximum sustainable CPL output. Loose inputs produce dangerous outputs, which is the proximate cause of most of the 2024 mass tort lead failures.

The 90-Day Operator Playbook

Translating the bellwether calendar into operating decisions requires a sequenced playbook with three 30-day phases. The framework assumes an operator running mixed inventory across at least two MDLs with active 2026-2027 milestones.

The first 30 days focus on inventory audit and concentration. Map current inventory against the bellwether calendar above, identifying which dockets carry pricing events inside the next 180 days. Concentrate spend in dockets with discovery milestones inside that window – Ozempic through April 28 Daubert and the subsequent class-cert and trial-prep stages, hair relaxer through the April 2026 bellwether picks and the trial calendar that follows, AFFF if Gergel resets the bellwether before mid-2026. Reduce or freeze spend in dockets in procedural limbo, particularly talc until the post-Two-Step path becomes clearer. Cohort existing inventory by docket, injury category, verification tier, and lead age, then run capital-cost calculations on inventory aged beyond 60 days.

The second 30 days focus on verification depth. Audit every active intake funnel for documentation gates – gastric-emptying scintigraphy capture for Ozempic gastroparesis, IAFF or DD-214 documentation for AFFF firefighters, salon-employment and product-use documentation for hair relaxer, qualifying-diagnosis documentation across all dockets. Where documentation gates do not exist, build them. The economics of verification investment are clearer than they appear: a $100 verification add-on that lifts CPL from the unverified band to the verified band returns 5-10x on the incremental cost. The operational discipline required is consistent – verification must be embedded at intake rather than retrofitted at qualification, because retrofitting fails on consent-capture grounds and forfeits the pricing premium.

The final 30 days focus on financial and contractual structure. Rebuild the settlement-multiple model with post-Daubert assumptions, particularly on conversion rates that reflect 2025-2026 plaintiff-firm screening rather than 2023-2024 baselines. Audit California SB 37 compliance across all creative and intake funnels, with particular attention to disclosure modules and consent-capture documentation. Renegotiate vendor contracts to net-30 terms tied to retainer-signing milestones rather than raw delivery volume – the contractual structure that aligns broker incentives with plaintiff-firm conversion outcomes. Where possible, structure exclusive-supply agreements with single plaintiff firms on specific verified-inventory categories, trading volume scale for margin stability. The operators who outperform across procedural cycles are the ones who treat the docket calendar as the primary input to their pricing model and the cost stack as the second-most-important. The law-firm lead-buying framework comparing retainer purchase versus signed-case purchase provides the contractual structure most operators converge on.

The playbook does not predict outcomes. It builds the operating discipline to survive any specific Daubert ruling, bellwether result, or settlement announcement without the model breaking. That discipline is the central asset in mass tort lead generation. Operators who lack it find that 18 months of inventory becomes worthless in a quarter; operators who have it find that the same procedural shocks create asymmetric upside.

Key Takeaways

-

April 28, 2026 is the cleanest mass tort pricing event of the year. Ozempic MDL 3094 Daubert motions test general causation under Rule 702 across gastroparesis, ileus, and gallbladder claims. Operators carrying scintigraphy-verified gastroparesis inventory hold value through the ruling; unverified inventory in any category faces compression.

-

The verified-unverified spread is the dominant variable in mass tort CPL. Across AFFF, hair relaxer, and post-Marston Ozempic, verified inventory trades at 2-3x unverified pricing because plaintiff firms reject 60-75% of unverified intake at qualification. Verification investment returns 5-10x on the incremental cost.

-

The settlement-multiple model breaks predictably on three inputs. Expected per-case settlement is the most volatile and most exposed to Daubert outcomes. Conversion rate is the variable operators most often inflate. Cost stack is the variable operators most often understate. Honest math on all three avoids the 2024 arbitrage failure pattern.

-

The 2026-2027 bellwether calendar concentrates pricing events in five dockets. Ozempic April 28 Daubert, AFFF bellwether reset, hair relaxer April bellwether picks, post-class Roundup repricing, and unresolved talc each move CPL in the 45-90 day window after the procedural milestone. Operators tracking the docket outperform those tracking only published rate cards.

-

California SB 37 has raised cost-per-lead 10-20% on California traffic since January 1, 2026. The disclosure and intake-funnel requirements affect creative-testing velocity and consent-capture infrastructure. National campaigns increasingly route California through a separate funnel. The regulatory direction extends beyond California – New York, Illinois, and Massachusetts have all opened comparable inquiries.

-

The post-vacatur TCPA environment removed the supply shock priced into 2024 broker margins. The Eleventh Circuit’s Insurance Marketing Coalition vacatur of the FCC one-to-one consent rule eliminated an expected regulatory tailwind. Brokers who had structured 2024 contracts around the assumption found 2025-2026 clearing prices 15-30% below baseline.

-

Vendor due diligence centers on three documentation tests. Consent-capture quality (TrustedForm or equivalent), verification depth (specific documents at audit-passable rates), and disposition transparency (plaintiff-firm intake-disposition data on cohort basis). Vendors that resist disposition data are pricing from information asymmetry.

-

The 90-day operator playbook is sequential discipline. Inventory audit and concentration in the first 30 days, verification depth in the next 30, financial and contractual restructuring in the final 30. The operators who survive procedural shocks are the ones who treat the docket calendar as the primary input and the cost stack as the second-most-important.

Frequently Asked Questions

What happens to Ozempic lead pricing after April 28, 2026?

April 28, 2026 is the deadline for Daubert motions in MDL 3094 (E.D. Pa., Judge Marston). Once the parties file challenges to general-causation experts, settlement probability becomes a tradable variable rather than a guess. Operators with verified gastroparesis claims documented by gastric-emptying scintigraphy hold inventory worth roughly 2-3x unverified leads, because Marston’s August 15, 2025 ruling made objective imaging the qualification gate. Pricing typically tightens 15-25% in the 60 days after Daubert briefing while plaintiff firms reassess intake budgets against a clearer settlement timeline.

Which mass tort MDLs are driving CPL movement in 2026?

Five dockets dominate. Ozempic MDL 3094 with 3,546 cases and the April 28 Daubert deadline. AFFF MDL 2873 with 15,222+ personal-injury cases after Judge Gergel vacated the October 2025 bellwether and closed the new-filing window September 5, 2025. Hair relaxer MDL 3060 with 11,000+ cases and the March 18, 2026 close of fact discovery on a 32-case bellwether pool. Roundup MDL 2741, repriced after Bayer’s $7.25 billion class settlement in February 2026. Talc, depending on whether J&J’s third Texas Two-Step survives the April 2025 dismissal.

What is the settlement-multiple model for mass tort CPL?

Maximum sustainable CPL equals the expected per-case settlement value multiplied by the attorney fee percentage (33⅓% pre-filing, 40% post-filing) and the lead-to-signed-case conversion rate, minus the operator’s full cost stack. A $200,000 expected settlement at 40% fees and 8% conversion supports roughly $640 in raw lead acquisition before intake, qualification, marketing overhead, and capital cost. Operators who skip the cost-stack subtraction blow up reliably – a 2024 lesson the AFFF and hair relaxer markets relearned the hard way.

How much does verification change AFFF lead value?

Verified AFFF firefighter leads – those with IAFF membership confirmation or DD-214 service records documenting fire-suppression duty at qualifying installations – trade at 2-3x unverified pricing. Unverified leads enter the $260-340 range cited in the Lawsuit Information Center July 2024 rate card; verified inventory routinely clears $700-900. The premium reflects acceptance rates: most plaintiff firms reject roughly 60-75% of unverified AFFF intake at qualification, which makes the headline CPL deeply misleading without an attached conversion assumption.

What killed the 2024 mass tort lead arbitrage?

Three forces compressed the spread simultaneously. Bellwether delays and adverse Daubert rulings (especially the August 2025 Marston scintigraphy order) reduced expected settlement values for marginal claims. California SB 37, effective January 1, 2026, banned guaranteed-outcome ads and tightened intake-funnel disclosures, raising compliance cost per lead. And the Eleventh Circuit’s vacatur of the FCC one-to-one consent rule before its 2025 implementation removed the regulatory tailwind that had been pricing into broker margins. Operators who built models on 2023 conversion rates and 2024 settlement multiples found 2026 economics unrecognizable.

Which mass tort vendors are operating in 2026?

Verified active vendors include Mohr Marketing, Tort Experts, Mass Tort Strategies, TSEG, Legal Calls, Mass Tort Alliance, On Point Legal Leads, iLawyer Marketing, Whitehardt, Best Case Leads, Casewise Partners, MassTortLeads.ai, DoppCall, CAMG, LeadingResponse, MTAA.AI, Top Shelf Logic, Pinpoint Legal Marketing, Foster Web Marketing, TruLaw, and Revolt Inc. The market splits between media-buying agencies (CAMG, LeadingResponse, Whitehardt), pure lead aggregators (Tort Experts, Mass Tort Alliance, Casewise Partners), and AI-enabled qualification platforms (MassTortLeads.ai, MTAA.AI). Buyer due diligence focuses on consent-capture documentation, verification depth, and willingness to share intake-disposition data.

What does California SB 37 change for mass tort intake?

SB 37 took effect January 1, 2026 and bans guaranteed-outcome advertising in California legal marketing while imposing new disclosure requirements on intake funnels that route leads to attorneys. Operators running California-targeted creative must now document fee structures, attorney involvement, and outcome disclaimers at form submission. The practical effect: California-eligible mass tort leads now cost 10-20% more to produce because creative testing cycles slow, landing pages need extra disclosure modules, and DocuSign-style consent capture is no longer optional. Nationwide campaigns increasingly route California traffic to a separate funnel.

Why does the Daubert motion deadline matter for lead buyers?

Daubert motions test whether plaintiff and defense experts meet Federal Rule of Evidence 702 – the standard for admissible scientific testimony – on general causation. If the court excludes a plaintiff’s general-causation expert, the entire injury category may collapse out of the MDL, making leads in that category nearly worthless. If the court admits the expert and the defense expert gets excluded, settlement probability spikes and CPL typically rises 25-50% within a quarter. The April 28, 2026 Ozempic deadline is the cleanest pricing event of the year because Marston’s August 2025 scintigraphy order already telegraphed how she treats causation evidence.

How does the bellwether selection process affect CPL?

Bellwether trials are representative cases the parties try first to gauge jury reactions and settlement bands. The pool size, selection criteria, and trial schedule directly affect CPL because each step de-risks settlement projections. Hair relaxer MDL 3060 closed fact discovery on a 32-case pool March 18, 2026 with bellwether picks expected in April – a window that historically pushes verified CPL up 10-15%. AFFF’s vacated October 2025 bellwether did the opposite, freezing pricing for six months while operators waited for Gergel to reset the calendar.

What is the 90-day operator playbook for the 2026 calendar?

First 30 days: audit inventory mix against the bellwether calendar and concentrate spend in dockets with discovery milestones inside the next 180 days. Next 30 days: tighten verification – gastric-emptying scintigraphy for Ozempic gastroparesis, IAFF or DD-214 for AFFF firefighters, salon-employment records for hair relaxer occupational exposure – because verified inventory holds value through Daubert events that destroy unverified pricing. Final 30 days: rebuild the settlement-multiple model with post-Daubert assumptions, audit California SB 37 compliance across creative and intake funnels, and renegotiate vendor contracts on net-30 terms tied to retainer-signing milestones rather than raw delivery volume.

The federal docket is not a backdrop to mass tort lead pricing – it is the primary input. Operators who track the bellwether calendar, build the settlement-multiple model honestly, and invest in verification ahead of plaintiff-firm screening cycles outperform those who anchor on published rate cards. The April 28, 2026 Ozempic Daubert deadline is one event in a sequence that will continue through the 2026-2027 calendar and beyond. The discipline that survives any specific ruling is the same discipline that captures the asymmetric upside when rulings break in the operator’s favor.

Sources

- U.S. Judicial Panel on Multidistrict Litigation, “MDL Statistics Report and Pending MDLs,” JPML.uscourts.gov, April 2026

- U.S. District Court for the Eastern District of Pennsylvania, “In re: Glucagon-Like Peptide-1 Receptor Agonists Products Liability Litigation, MDL 3094 – Case Management Orders,” 2025-2026

- Lawsuit Information Center, “Mass Tort Lead Pricing and Retainer Rate Cards (May and July 2024),” Miller and Zois, 2024

- Cornell Legal Information Institute, “Federal Rule of Evidence 702 – Testimony by Expert Witnesses (2023 amendments),” law.cornell.edu, 2023

- California Legislative Information, “Senate Bill 37 – Legal Advertising and Intake-Funnel Disclosures,” leginfo.legislature.ca.gov, effective January 1, 2026

- Bayer AG, “Glyphosate Litigation Update and Class Settlement Announcement,” bayer.com, February 2026

- U.S. Court of Appeals for the Eleventh Circuit, “Insurance Marketing Coalition Limited v. Federal Communications Commission,” ca11.uscourts.gov, January 2025

- Reuters, “U.S. Judge Rejects Johnson & Johnson Talc Bankruptcy Strategy for Third Time,” reuters.com, April 2025

- U.S. District Court for the District of South Carolina, “In re: Aqueous Film-Forming Foams Products Liability Litigation, MDL 2873 – Bellwether Vacatur and Filing Window Order,” August 15 and September 5, 2025

- U.S. District Court for the Northern District of Illinois, “In re: Hair Relaxer Marketing, Sales Practices, and Products Liability Litigation, MDL 3060 – Fact Discovery Close and Bellwether Selection Orders,” March 2026