Ranking #1 used to mean traffic. In April 2026, it means a 38% chance of being cited in the answer the buyer actually reads – and a 0.61% chance of getting the click if the answer appears.

The 61% number, and what it actually understates

Lead generation operators have spent twenty years optimizing for a stable equation: impressions multiplied by click-through rate produced sessions, and sessions multiplied by conversion rate produced leads. Every layer of paid search bid management, every SEO content brief, every affiliate site’s editorial calendar assumed the equation held. In September 2025, Seer Interactive published the data that broke it.

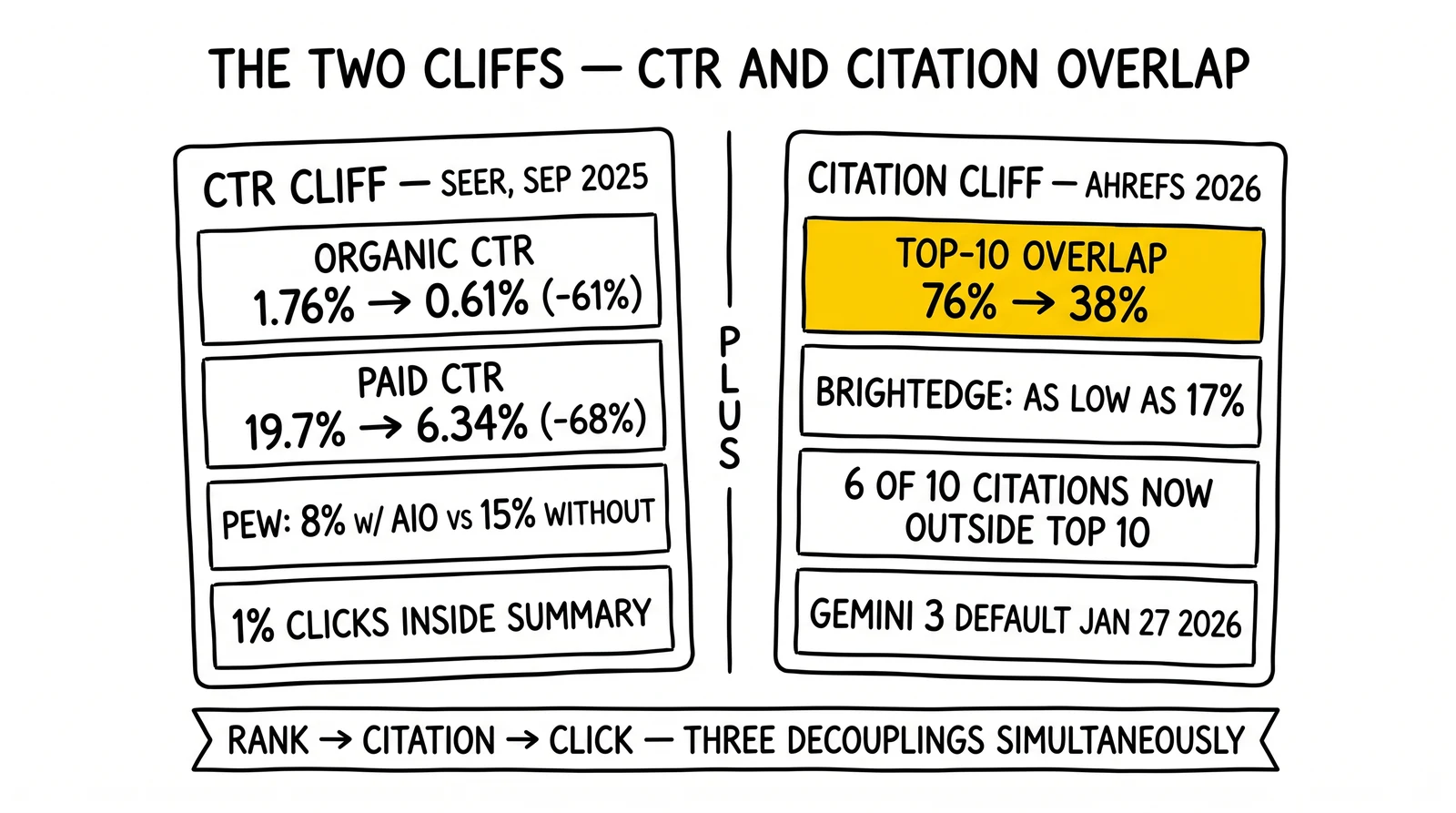

Across 3,119 informational queries spanning 42 organizations and 25.1 million organic impressions, organic click-through rate on queries that triggered an AI Overview fell from 1.76% to 0.61%. Paid CTR on the same query set fell from 19.7% to 6.34%. Seer’s published headline figure – minus 61% organic, minus 68% paid – circulated through trade press (Search Engine Land, Search Engine Journal, PPC Land) as “the AIO CTR cliff.” Note that the raw delta from 1.76% to 0.61% computes to a -65% drop; Seer published the impression-weighted figure as -61%. Either framing puts the cliff in the same severity range. Pew Research, working with a separate methodology and a 900-person browsing panel in March 2025, found 8% click-through on results pages with AI summaries versus 15% without – and exactly 1% of clicks landing inside the summary itself. Two independent studies, two methodologies, and the same direction of travel: the search result page is no longer a click-distribution mechanism. It is an answer-distribution mechanism, and only the cited domains participate.

The strongest single statistic in the data set is not the 61% CTR drop. It is the citation-overlap collapse documented by Ahrefs in early 2026. Analyzing 863,000 keywords against 4 million AI Overview URLs, Ahrefs found that 76% of cited pages also appeared in the organic top 10 in July 2025. By February 2026, that overlap had fallen to 38%. BrightEdge analysis of a different keyword set put it as low as 17%. Six of every ten AI Overview citations now point to pages outside the organic top 10 – meaning the rank-tracking dashboard that lead-gen operators have stared at since 2005 systematically misrepresents AI visibility. Position #1 in the blue links is no longer a reliable predictor of citation. Citation is no longer a reliable predictor of clicks. Clicks are no longer a reliable predictor of qualified leads. Three decoupling events, all happening simultaneously, all measured by independent research firms within a 12-month window.

For lead generation operators, the practical question is not whether to acknowledge the cliff. It is whether the funnel architecture they inherited from the SEO and PPC playbooks of 2010–2024 can be repaired, or whether it must be replaced. The data points to replacement.

Trigger rates by vertical: where the funnel actually breaks

AI Overview impact varies by an order of magnitude across verticals. Treating the problem as uniform – “AIO is killing search” – produces wrong strategic decisions. Healthcare publishers face a fundamentally different reality than rooftop-solar local affiliates, and conflating the two leads operators in low-trigger verticals to over-react and operators in high-trigger verticals to under-react.

BrightEdge data tracking AI Overview presence from February 2025 to February 2026 produced the clearest picture available. The aggregate across all queries climbed from approximately 31% to 48% of searches – a 58% year-over-year expansion. That aggregate hides extreme dispersion. In healthcare, AIO trigger rates climbed to 88% by December 2025; in education, 83%; in B2B technology, 82%. Pure-transactional eCommerce sat at 3.2% of queries through 2025 and rose only marginally in early 2026. Real estate and rooftop solar – both dominated by local-intent searches that Google still routes to map packs and local listings – registered AIO presence in the 5–6% range.

The table below summarizes verified trigger rates by vertical, drawn from BrightEdge’s February 2026 dataset and ALM Corp’s nine-industry analysis. These numbers update quarterly; operators should treat them as snapshots rather than steady-state benchmarks.

AI Overview trigger rate by vertical (February 2026)

| Vertical | AIO Trigger Rate | YoY Change | Lead-Gen Implication |

|---|---|---|---|

| Healthcare | 88% | +29 pp | Informational top-of-funnel decimated; first-touch shifts to citation-only |

| Education | 83% | +65 pp | Comparison and “best of” queries fully captured by AIO summaries |

| B2B Technology | 82% | +46 pp | SaaS comparison content under-clicks; demo-request funnels compress |

| Restaurants | 78% | +21 pp | Local search still routes to map; informational queries lose clicks |

| Legal | 77.7% | +18 pp | Mass-tort and personal-injury informational queries hit hardest |

| Insurance | ~63% | +46 pp | Quote-intent queries partially insulated; education content cliff |

| Finance | ~41.7% | +9 pp | Calculator and rate-table queries lose clicks; YMYL still favors top sites |

| Rooftop Solar (local) | ~6% | +2 pp | Local-intent insulated; educational subqueries still exposed |

| Real Estate | ~5.8% | +1 pp | Map pack dominates; AIO appears only on educational queries |

| Pure-transactional eCommerce | 3.2% | +0.5 pp | Buy-intent largely insulated; “best [product]” queries hit at 83% |

Sources: BrightEdge (February 2026 dataset), ALM Corp 9-industry analysis (March 2026), Visibility Labs eCommerce study (Q1 2026)

The actionable signal in this table is the dispersion. A legal lead-gen affiliate running mass-tort informational content faces 78% AIO presence – meaning roughly four of every five top-of-funnel impressions land on a SERP where the answer is provided before the click. A solar affiliate running geo-targeted “solar installers near me” pages faces 6% AIO presence, with the map pack and local listings still dominating. Both operators read the same Press Gazette headline (“Google traffic down 33% globally in 2025”), but their strategic responses should diverge sharply. The legal operator must rebuild for citation; the solar operator must defend a local-intent funnel that is partially insulated for now but will erode as Google extends AI Mode coverage to local queries through 2026 and 2027.

The split also shapes investment timing. Operators in 80%+ trigger verticals – healthcare, education, B2B tech – are out of runway. Operators in 30–60% trigger verticals – finance, insurance – have 12–18 months to migrate. Operators in sub-10% verticals have 24–36 months but should treat the timeline as a planning window, not a reprieve. The slope on the BrightEdge curve is monotonic.

Why ranking #1 no longer means citation

The citation-overlap collapse – 76% to 38% over seven months, per Ahrefs – represents a more fundamental change than the headline CTR drop. It says the Google ranking algorithm and the AI Overview citation algorithm are no longer the same algorithm. They consult overlapping signals, but they optimize for different outcomes, and the divergence is widening.

Three structural reasons drive the gap. First, AI Overviews use query fan-out: a single user query gets decomposed into 5–15 sub-queries, each of which retrieves its own candidate set. The citations in the final summary are aggregated across those sub-queries, meaning a page may be cited because it answered a sub-query that the original query did not literally contain. Operators ranking #1 for “best Medicare supplement plans” might never appear in the AIO summary for the same query because the model fanned out into “what does Medicare Part B cover,” “guaranteed issue rights,” and “Medigap vs Medicare Advantage trade-offs” – and the user’s article addressed only one of those.

Second, citation favors extraction-friendly structure over ranking-friendly authority. A 4,000-word pillar page with deep authority and high backlink count may rank #1 because the ranking algorithm rewards comprehensive coverage and link signals. The same page may go uncited because its key statistics live in three paragraphs of prose without schema, while a 600-word competitor with FAQPage markup, a comparison table, and a Wikidata-anchored entity provides cleaner extraction surface. Citation engineering is not the same as content depth. It is the discipline of making each citable claim independently extractable, attributable, and machine-verifiable.

Third, Gemini 3’s January 27, 2026 promotion to the default AI Overviews model changed selection behavior. Industry analysis from ALM Corp and Search Engine Journal flagged the post-Gemini-3 citation pattern as systematically different: more long-tail domain coverage, less reliance on top-10 organic results, and increased weight on entity-resolved sources. Operators who tracked their citation share through Q1 2026 reported volatility – domains that had been cited consistently through Q4 2025 dropped out, while domains in positions 11–50 began appearing more frequently. The Ahrefs methodology captured the median of this shift; individual sites experienced the volatility much more sharply.

This is the single hardest concept for SEO-trained operators to absorb. The instinct, when citations drop, is to push harder on rankings – build more links, ship more content, target higher-volume keywords. That instinct produces diminishing returns because the citation algorithm is not asking “which page ranks best?” It is asking “which set of extractable claims, drawn from authoritative sources with clean entity resolution, best answers each sub-query in the fan-out?” Different optimization target, different playbook.

AI Mode, query fan-out, and the prompt-cluster reality

In January 2026, Google expanded AI Mode to over 200 countries and 35 new languages, and in February 2026 added 53 additional languages. AI Mode is no longer a feature operators can ignore as US-only or English-only. The product runs on Gemini 3 Pro for most users and “Thinking with 3 Pro” for AI Pro and AI Ultra subscribers. Tapping “Show more” on an AI Overview now hands off seamlessly into AI Mode’s chat interface, where follow-up questions extend the session. Google’s published behavioral data from this transition: 26% of AI Mode sessions end without a click anywhere, versus 16% session-end on classic SERPs. The ten-percentage-point gap represents the “answered without clicking” cohort that lead generation funnels never see.

Query fan-out is the mechanism behind this. A user types “best home insurance for new homeowners in Texas.” Gemini 3 decomposes that into a cluster of underlying questions – what coverage do new homeowners need, what’s specific to Texas (windstorm, hail, flood), what carriers are highly rated in Texas, what’s the typical cost range, what discounts apply. Each sub-question retrieves a citation set; the model synthesizes an answer; the user reads it; in 26% of cases, the session ends there.

The implication for lead-gen content strategy is that keyword-targeted content is increasingly mismatched to the unit of work the model performs. The model’s unit is the prompt cluster – the 10–30 questions in the fan-out behind any given user-typed query. Operators chasing “best home insurance Texas” with one pillar page miss the fan-out entirely; the model finds its answers across multiple sources, citing none of them more than once or twice. Operators who have built coverage across the prompt cluster – separate, tightly-scoped, schema-marked pieces addressing each sub-question – show up in three or four citations within the same summary. The math compounds: more prompt coverage, more citation opportunities, more chances to drive the 1% inside-summary click and the branded-search lift that follows.

This is why the LLMO discipline diverges from the SEO playbook on content strategy. SEO teaches operators to consolidate authority on pillar pages because backlinks aggregate by URL. LLMO teaches operators to fragment coverage across prompt-aligned units because citations aggregate by claim. Both can be true simultaneously, and the highest-performing 2026 lead generation sites maintain both architectures: pillar pages for ranking and citation-anchor authority, plus a network of focused sub-pages mapped to prompt clusters for citation breadth. The site’s LLMO citation guide covers the architectural pattern in detail.

The five-schema citation engineering stack

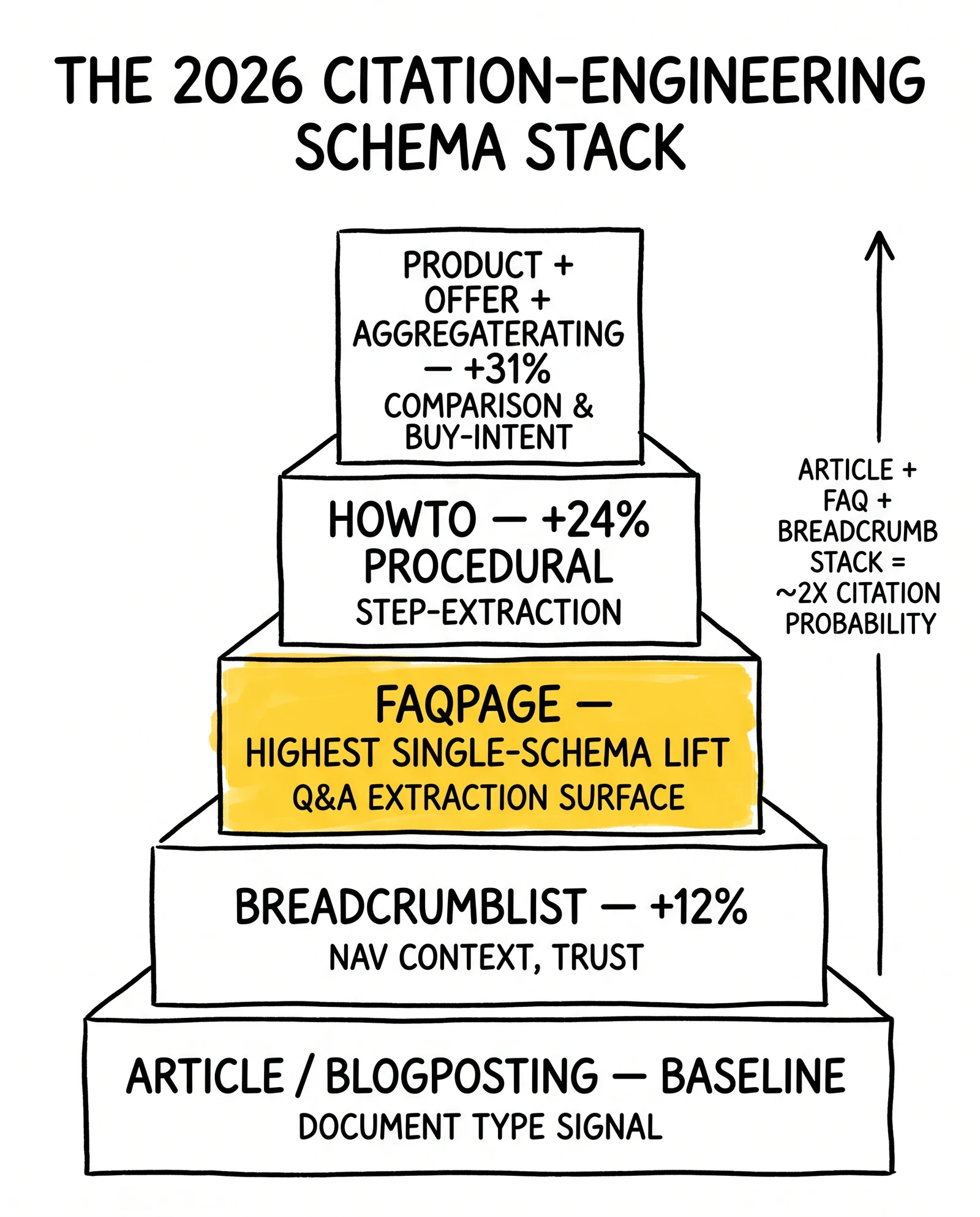

Schema markup moved from “nice-to-have” to load-bearing infrastructure between mid-2024 and early 2026. Research from frase.io and stackmatix, published across Q1 2026, established the citation lift attributable to specific schema combinations. The headline finding: FAQPage shows among the highest single-schema citation rates in vendor testing, and nesting FAQPage inside Article schema with BreadcrumbList navigation produces roughly 2x the citation probability of Article schema alone. The compound effect is not additive – it is multiplicative, because the schemas signal different aspects of the document that generative engines weight independently.

The table below maps the five-schema stack that defines citation-engineered pages in 2026, organized by citation lift and use case.

Schema stack citation lift by type

| Schema Type | Standalone Citation Lift | Compound Lift in Stack | Primary Use Case |

|---|---|---|---|

| Article (or BlogPosting) | Baseline | Baseline | Document type signal – required floor |

| FAQPage | Highest among single schemas | +2x compound with Article | Q&A extraction; voice and AI Overview citations |

| BreadcrumbList | +12% | Reinforces Article context | Navigation trail; trust signal |

| HowTo | +24% | +1.6x for procedural queries | Step-extraction; “how to” prompt clusters |

| Product + Offer + AggregateRating | +31% | +1.8x for commercial queries | Comparison and buy-intent citations |

Sources: Frase.io FAQ schema research (March 2026), Stackmatix structured data analysis (February 2026), Stackmatix AEO schema priority guide (January 2026)

The first-100-words rule operates alongside the schema stack and is independent of it. Generative engines weight the opening of an article disproportionately when extracting answers – partly because the lede typically contains the document’s thesis, partly because retrieval embeddings emphasize early-paragraph content. Operators who bury the citable answer in paragraph six lose extraction priority to competitors who front-load the same answer. The discipline: every page that targets a prompt cluster should answer the primary question, with a specific number or named entity, in the first 100 words. The schema then tells the model which span to extract; the prose tells the model what it says; the entity reference tells the model who said it.

Three failure modes recur in operator implementations. First, schema duplication: shipping FAQPage markup that duplicates copy already inside Article schema, which generative engines treat as adversarial signal and discount. Second, schema-prose drift: FAQ markup whose questions don’t appear verbatim in the page body, which fails Google’s structured-data validation and can trigger manual penalties. Third, entity vagueness: schema that references generic types (“Thing,” “Organization”) without sameAs anchors to Wikidata, Wikipedia, or industry-specific knowledge graphs. Each failure mode reduces citation probability without obviously affecting Google rankings, so operators who rely on rank dashboards never diagnose the problem. The site’s deeper coverage of schema markup for AI visibility and entity graph hardening covers the implementation specifics.

Robots.txt and llms.txt: a decision matrix that actually works

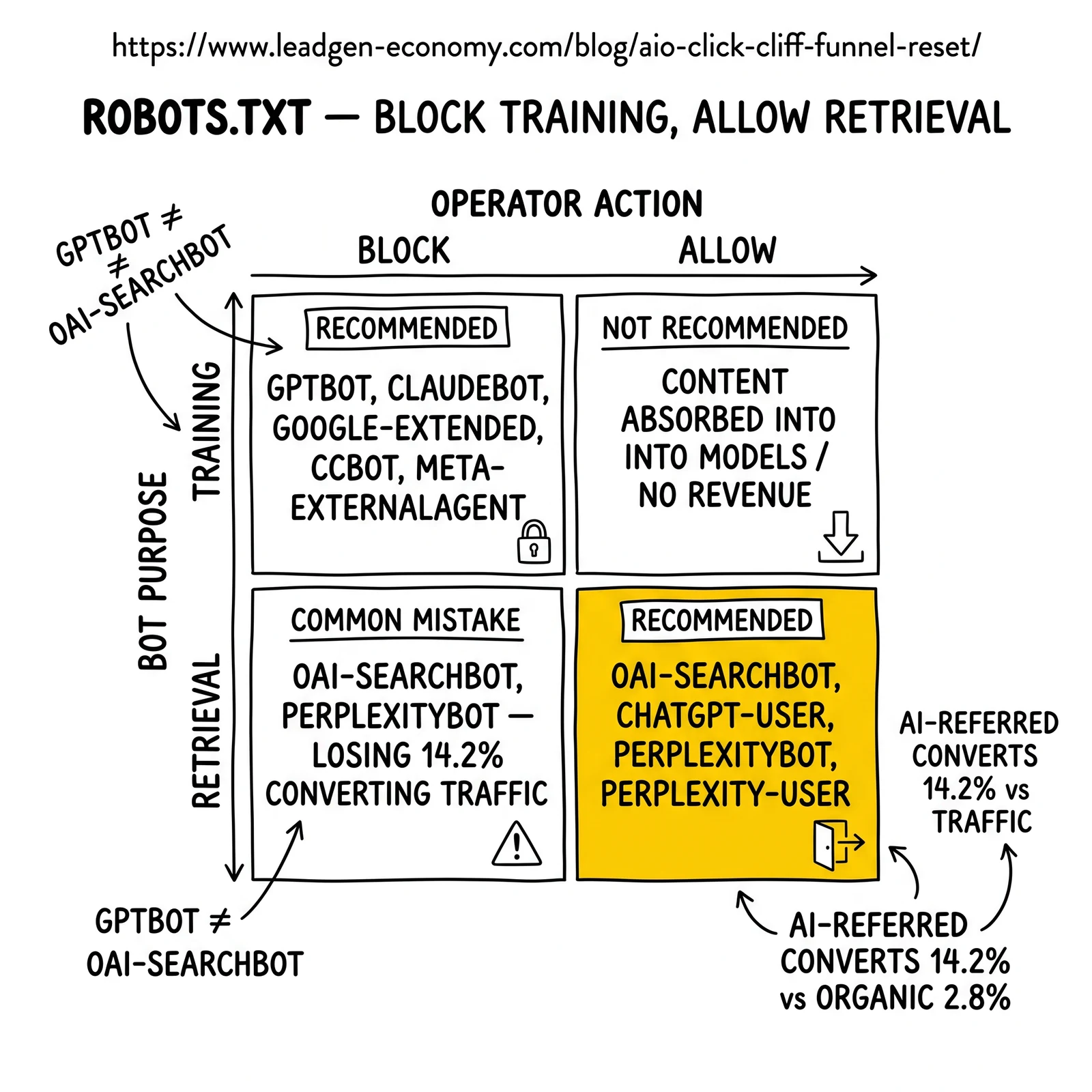

The robots.txt question for AI bots reduces to a decision that most operators get wrong on first attempt: training crawlers and retrieval crawlers are different bots from the same companies, and they should be treated separately. GPTBot crawls for OpenAI training. OAI-SearchBot crawls for ChatGPT search results. Blocking GPTBot has no effect on whether OAI-SearchBot can index the site for ChatGPT’s search feature. Most lead-gen operators, hearing “block AI bots,” end up blocking both – and lose the retrieval visibility that drives 14.2% conversion AI-referred traffic.

The defensible 2026 configuration for affiliate and lead-gen sites that monetize through traffic and conversions is straightforward.

Robots.txt allow/block matrix for lead-gen operators

| Bot | Category | Recommended Action | Reason |

|---|---|---|---|

| GPTBot | Training (OpenAI) | Block | No revenue from training; protects content asset |

| ClaudeBot / anthropic-ai | Training (Anthropic) | Block | Same logic as GPTBot |

| Google-Extended | Training (Google Gemini) | Block | Decoupled from Google search ranking |

| CCBot | Training (Common Crawl) | Block | Common Crawl feeds many models’ training |

| Meta-ExternalAgent | Training (Meta) | Block | Same logic |

| OAI-SearchBot | Retrieval (ChatGPT search) | Allow | Drives 14.2% conversion AI referrals |

| ChatGPT-User | Retrieval (user-triggered) | Allow | Activates only on explicit user request |

| PerplexityBot / Perplexity-User | Retrieval (Perplexity) | Allow | Citation source for Perplexity answers |

| Googlebot | Standard search | Allow | Required for organic search |

| Bingbot | Standard search | Allow | Required for Bing and Copilot retrieval |

Source: Cloudflare AI bot blocking documentation (2025); Playwire publisher guide; Mersel.ai bot configuration guide (2026)

The configuration above protects content from training-data absorption while preserving retrieval-time visibility. Sites with strong direct affiliate revenue and weak AI-referral monetization may consider blocking retrieval bots as well – but the data is increasingly clear that AI-referred conversion (14.2% per RankScience and Microsoft Clarity) materially exceeds Google organic conversion (2.8% per the same benchmarks). Even at less than 1% of total traffic, AI referrals can drive 5–10% of total conversions for sites with adequate citation footprint.

The llms.txt question is simpler. ProGEO.ai’s March 31, 2026 study found 7.4% Fortune 500 adoption – 37 of 500 companies – and Search Engine Land’s tracking experiments through 2025 found no measurable ranking, citation, or visibility lift attributable to the file. Anthropic proposed the standard in 2024; as of April 2026, neither OpenAI, Google, nor Anthropic has publicly confirmed using llms.txt to influence retrieval, ranking, or training. The standard is largely cosmetic in its current adoption state – operators who ship a 50-line llms.txt file as low-cost insurance will not be punished, but they should not expect citation lift, and they should not allow llms.txt implementation to displace work on schema markup, robots.txt configuration, or entity-graph hardening, all of which produce measurable signal. The site’s llms.txt and AI crawler optimization guide covers the file’s formal structure for operators who want to ship it for completeness.

Vertical playbooks: where to spend the next $100K

The dispersion in trigger rates means a single playbook does not fit all lead-gen verticals. The economics of a citation-engineering investment look very different in healthcare (88% trigger, severe cliff already happening) than in residential solar (6% trigger, runway intact). The playbooks below sketch the prioritization for six verticals where the site’s data and operator interviews produced enough signal to be specific.

Insurance. Auto, home, and life informational top-of-funnel queries are eroding fast – 63% AIO trigger and rising. Quote-intent queries (“home insurance quote Texas”) remain partially insulated because Google still surfaces local-listings and quote-form results, but educational queries (“how does umbrella insurance work”) are fully captured. Spend the next quarter rebuilding the educational sub-tree with FAQPage markup, sub-1,000-word focused pieces mapped to prompt clusters, and entity-graph anchoring to Wikidata for major carrier names. Ping-post infrastructure remains protected for now; the cliff is in awareness-stage content. Cross-reference the site’s auto insurance lead generation guide for downstream funnel implications.

Mortgage. AIO trigger is moderate (~50%) and concentrated in informational queries about rates, qualification, and process. The HPPA trigger-leads ban created an acute compliance reset in early 2026; layering AIO erosion on top means the mortgage funnel must be rebuilt on two axes simultaneously – compliance and citation. Priority: rebuild rate-table content with structured data (Property + MonetaryAmount schema), invest in branded-search velocity tracking, and use citation share as the leading indicator while purchase intent migrates from “search rate” to “ask the AI.”

Solar. Local-intent dominance (zip-code searches, “solar installers near me”) keeps direct trigger rates around 6%. The cliff is in educational queries – “how do solar panels work,” “solar payback period,” “battery storage vs no battery” – which trigger AIO at 70%+. Solar affiliates with a heavy informational top-of-funnel face the same cliff as healthcare; solar affiliates with local-listing dominance are insulated. Most operators run both, so the answer is dual: protect the local funnel with continued geo-targeting and citation-engineer the educational sub-tree.

Legal. Mass-tort and personal-injury informational queries face 77.7% AIO trigger. The vertical’s economics depend on retainer conversion from informational research, so the cliff bites hard. Priority: aggressive prompt-cluster mapping (each tort has 30–80 sub-questions in its fan-out), FAQPage markup at scale on settlement and eligibility content, and migration of measurement to citation share + branded-search velocity. The legacy keyword-volume model under-weights the long-tail prompts that the model’s fan-out actually pulls.

B2B SaaS. 82% AIO trigger plus the highest AI-referred conversion rates (Claude 16.8%, ChatGPT 14.2–15.9%) make B2B tech the vertical with the most upside from getting citation engineering right. Comparison content (“Salesforce vs HubSpot”) is fully captured in AIO, so the play is to be cited inside that summary rather than to rank for the comparison query directly. Investment: deep prompt-cluster coverage, entity-anchored brand schema, and a parallel content track aimed at being cited by ChatGPT, Perplexity, and Claude rather than by Google specifically. Track citation share on Profound or Ahrefs Brand Radar; ignore traditional rank tracking as a primary signal.

Medicare. YMYL classification means Google applies stricter authority filters; the AIO trigger rate for Medicare-specific queries sits near healthcare’s 88% with even stricter source preferences. CMS marketing rules add a compliance overlay. The vertical’s surviving operators have built content with clear authorship, named medical-reviewer attribution, and dense citation density to government and academic sources. Operators chasing Medicare top-of-funnel without those E-E-A-T signals are uncited regardless of rank. The site’s intent-to-lead mapping framework covers the prompt-cluster method that Medicare specifically requires.

The new top-of-funnel KPI stack

The metric migration is the part most operators delay because it requires rebuilding dashboards and re-educating boards. The delay is expensive. Optimizing for impressions and CTR in 2026 is optimizing for a metric whose conversion math has decoupled from revenue. The new KPI stack reflects what the AI-mediated funnel actually rewards: citation breadth, brand velocity, and AI-referred conversion quality.

Old funnel metric → new funnel metric

| Old Metric | New Metric | What It Measures Now |

|---|---|---|

| Impressions | Citation Share | % of relevant AI answers (AIO, ChatGPT, Perplexity, Claude) that mention the brand or domain |

| Position / Rank | Citation Position + Citation Source Diversity | Which AI surfaces cite, how many distinct ones, how often |

| Organic CTR | Click-from-Citation Rate + Branded Search Lift | Click-through from cited summaries + downstream branded-query velocity |

| Click-Through Rate | AI-Referred Sessions + Direct Traffic Spike | Sessions tagged from AI sources + the indirect lift from citation-driven research |

| Sessions | AI-Referred Conversion Rate (segmented) | Conversion by source: Claude 16.8%, ChatGPT 15.9%, Perplexity 12.4%, Gemini ~3% |

| Conversion Rate (organic) | AI Funnel CPL | Cost per qualified lead, with AI-referred and citation-attributed leads tagged separately |

| Keyword Volume | Prompt Coverage Breadth | Number of distinct prompts where the brand surfaces |

Sources: Microsoft Clarity AI traffic conversion study (2025); RankScience AI search benchmarks (Q4 2025); averi.ai citation tracking research (2026); Seer Interactive branded-search lift analysis (Q1 2026)

Citation share – the first new metric – is the single most important leading indicator. Tools including Profound, Ahrefs Brand Radar, and Semrush AI Tracking sample thousands of prompts daily across major models and report which domains are cited and how often. A site whose citation share is rising on healthcare prompts will see branded-search lift within 1 to 4 weeks, per Seer Interactive data, with corresponding lifts in direct traffic and AI-referred sessions. A site whose citation share is flat or falling will see the lagging indicators erode regardless of rank.

The branded-search lift number itself deserves careful framing. Trade press has cited “200–400% branded-search lift” for AIO-cited brands; that range is anecdotal and not reliably reproducible. The defensible benchmark, drawn from Seer Interactive’s 2025 analysis of cited domains, is +35% organic CTR and +91% paid CTR for cited brands on subsequent branded queries. Even hedged, those numbers represent meaningful lift – but operators planning campaigns around “200%+ branded lift from AIO citation” are planning around fiction.

AI-referred conversion segmented by source is the second crucial metric, because the spread is enormous and the optimization implications differ. A site that ranks well on Perplexity but invisibly on Gemini converts AI traffic at roughly 4x the rate Gemini-cited competitors achieve, despite citation parity. The difference is user intent at the moment of click: Perplexity users are deep into qualification when they click; Gemini AI Overview users are typically still in awareness mode. Tracking conversion by AI source reveals which citation investments are actually driving pipeline versus driving traffic.

The dashboard rebuild is non-trivial – UTM tagging schemes, GA4 custom dimensions, and integration with citation-tracking tools – but the work is one quarter of engineering effort plus an ongoing weekly review cadence. Operators who delay it are flying blind into a funnel that no longer behaves like the funnel they were trained to manage. The site’s AI search ROI measurement framework and first-touch vs last-touch attribution analysis cover the measurement architecture in detail.

What the publisher data foreshadows

Chartbeat’s March 2026 dataset, published exclusively to Axios, provides the cleanest available view of how the cliff affects different operator scales. Page views from Google Search and Google Discover fell 34% and 15% respectively from December 2024 to December 2025. The decline disproportionately punished smaller operators: small publishers (1,000–10,000 daily page views) lost 60% of search referrals over two years; medium publishers (10,000–100,000) lost 47%; large publishers (100,000+) lost 22%. ChatGPT referrals grew more than 200% in the same window but remained less than 1% of total page-view referrals – meaning the AI-traffic upside has not yet meaningfully offset the search-traffic downside for any publisher tier.

The pattern matters for lead generation operators because lead-gen affiliates and aggregators are functionally publishers. They monetize traffic. They depend on the same Google funnel. The Chartbeat data – small operators losing 60%, large operators losing 22% – almost certainly maps to lead-gen volume tiers as well. A small auto-insurance affiliate site running 5,000 daily visits in December 2024 likely generates 2,000 daily visits in April 2026 even with strong content output, because the underlying click-share has compressed. A large operator with 200,000 daily visits and a recognized brand has lost less, but is not insulated.

The brand-recognition asymmetry is the explanatory variable. Larger publishers with stronger brands face two advantages: their citation rates in AI Overviews tend to be higher (model preferences favor recognized sources), and their direct-traffic and branded-search bases are larger absolute numbers, which are not subject to the click cliff. The implication for small lead-gen operators is uncomfortable: the cost of building enough brand recognition to remain visible has gone up at the same moment that the click economics have eroded. The fundraising and consolidation that ran through publisher media in 2025 will run through lead generation through 2026 and 2027 – large operators absorbing small ones to consolidate brand authority for citation.

Implementation reality and the 12-month migration

Citation engineering is the rare 2026 marketing investment with a sub-12-month payback for operators who execute it sequentially. The discipline does not require new technology, new platforms, or new ad spend – it requires restructuring existing assets and rebuilding measurement. Phase 1 (months 1–3) covers the schema stack rebuild, robots.txt configuration, and entity-graph hardening; citation-tracking tools begin showing measurable lift in 6–8 weeks for sites with adequate underlying authority. Phase 2 (months 4–9) covers content rebuild for prompt coverage – replacing keyword-targeted articles with prompt-cluster pillar pages, adding FAQPage markup at scale, expanding citation-friendly content density (specific numbers, named sources, comparison tables, dated claims). Phase 3 (months 10–18) replaces the dashboard.

The most common implementation failure is compression. Operators who attempt to ship all three phases in 90 days typically rebuild surface assets without restructuring the underlying measurement model. They produce schema markup, but no entity hardening. They produce FAQ content, but with questions that do not appear in real prompt fan-outs. They produce dashboards that overlay AI metrics on top of the old funnel rather than replacing it. Six months later, citation share is flat, branded-search velocity is flat, and the operator concludes the strategy doesn’t work – having tested the wrong implementation of it.

The second-most-common failure is treating AIO as a Google-only problem. The discipline transfers across surfaces, but the optimization specifics diverge. Perplexity weights citation density and source recency differently than ChatGPT. Claude favors structured data and explicit reasoning chains. Gemini is the source most aligned with Google ranking signals – but per the citation-overlap data, even Gemini’s preferences have decoupled from the organic top 10. Operators optimizing only for AIO citation miss roughly half of available AI-referred traffic, since ChatGPT alone drives 87% of AI referral volume per Lantern’s published data.

The third failure mode is internal: the marketing leader who runs the migration without re-educating the board, the CFO, and the demand-gen team. Ranking dropped, organic traffic dropped, and the dashboard the executive team has watched for five years is showing red – but citation share, branded-search velocity, and AI-referred conversion are showing green. Without a re-educated audience, the migration looks like failure when it is succeeding. Building the new dashboard in parallel with the old one for one full quarter is the practical bridge.

Where this leaves the funnel in 2027

The AI-mediated funnel will not stabilize in 2026. Gemini 4 is widely expected in the second half of the year, with further model upgrades likely shifting citation behavior again. AI Mode adoption is climbing – Google’s own data shows 26% of AI Mode sessions ending without a click, and the share is growing as users adapt their query habits. ChatGPT search and Perplexity continue gaining share at small but compounding rates; Anthropic’s Claude rolled out browsing in Q1 2026. Each surface evolves its own citation logic, and operators tracking citation share across all of them simultaneously will outperform operators tracking any single one.

The structural endpoint, three to five years out, is a lead generation funnel where the awareness and consideration stages are conducted entirely inside AI assistants and the operator’s first user touchpoint is a high-intent click from a multi-turn qualification conversation. The conversion rate on that click is high – current data suggests 14.2% on average and as high as 16.8% from Claude – but the volume per cited brand is small. Winning the funnel will mean building citation share across many prompts rather than ranking for many keywords, and building landing-page experiences calibrated to warm AI-referred users rather than cold organic visitors.

The operators who emerge strongest from the 2026–2028 transition will not be those with the largest content footprints or the most aggressive paid spend. They will be the operators who recognized in early 2026 that the funnel architecture had structurally changed and rebuilt around the new physics – citation engineering, prompt-cluster coverage, and AI-source-segmented measurement – while competitors continued optimizing for the old metrics. The cliff is not a temporary disruption to navigate. It is the permanent reset of the top of the funnel.

Key Takeaways

-

Organic CTR on AIO-triggered queries fell from 1.76% to 0.61% – a -61% drop as Seer Interactive published the figure (25.1M-impression study; raw delta computes to -65%). Paid CTR fell 68% on the same query set. The decline is not noise; it reflects a structural shift in how SERPs distribute clicks versus answers.

-

The strongest single statistic is the citation-overlap collapse: 76% to 38% in seven months, per Ahrefs. Six of every ten AI Overview citations now point to URLs outside the organic top 10. Rank-tracking dashboards systematically overstate AI visibility – operators relying on them are flying blind on the metric that now matters.

-

Trigger rates vary by an order of magnitude across verticals. Healthcare 88%, Education 83%, B2B Tech 82%, Restaurants 78%, Legal 77.7%, Insurance 63%, Finance 41.7%, eCommerce 3.2%, Real Estate 5.8%, Solar ~6%. Local-intent verticals are partially insulated, but not for long. One-size-fits-all responses produce wrong investment timing.

-

The compound schema stack – Article + FAQPage + BreadcrumbList – roughly doubles citation probability versus Article alone. FAQPage shows among the highest single-schema citation rates in vendor testing on relevant queries. Combined with HowTo (procedural) and Product+Offer (commercial-intent), the five-schema stack defines 2026 citation engineering.

-

robots.txt should block training crawlers and allow retrieval bots. GPTBot ≠ OAI-SearchBot. ClaudeBot ≠ ChatGPT-User. Conflating the two categories costs visibility on AI-referred traffic that converts at 14.2% versus 2.8% for Google organic.

-

llms.txt is largely cosmetic in April 2026. ProGEO.ai found 7.4% Fortune 500 adoption with no measurable retrieval, ranking, or citation lift attributable to the file. Ship if engineering bandwidth allows; do not displace schema or robots.txt work.

-

The new top-of-funnel KPI stack is citation share, branded-search velocity, AI-referred conversion (segmented by source), and prompt-coverage breadth. Impressions, position, and organic CTR remain on the dashboard but are no longer leading indicators of pipeline.

-

Branded-search lift from citation is real but smaller than trade-press claims. Defensible benchmark: +35% organic CTR and +91% paid CTR on branded queries for cited brands, per Seer Interactive. Lift typically materializes 1–4 weeks after citation begins. The “200–400%” figures circulating are anecdotal.

-

AI-referred conversion is 5x Google organic but applies to a small base. Less than 1% of publisher referrals come from AI surfaces per Chartbeat, but those referrals convert at 14.2% versus 2.8%. Net contribution to total conversions is meaningful (5–10% for sites with adequate citation footprint) and growing.

-

Migration timeline is 12–18 months. Compression below six months produces failure. Phase 1 (schema, robots, entities) shows lift in 6–8 weeks. Phase 2 (content for prompt coverage) lifts citation share over 4–9 months. Phase 3 (dashboard replacement) consolidates the new funnel by month 18.

Frequently Asked Questions

The frontmatter faqs block above is the canonical FAQ source. The questions and full-paragraph answers covered in that block include:

- How much did Google CTR really drop because of AI Overviews?

- Does ranking #1 on Google still mean getting cited in the AI Overview?

- Which lead-gen verticals are hit hardest by AI Overviews?

- What schema markup actually drives AI Overview citations?

- Should lead generation sites adopt llms.txt?

- How should robots.txt be configured for AI search visibility?

- What top-of-funnel KPIs should replace impressions and clicks in 2026?

- Do AI-referred visitors actually convert better than Google organic?

- How is the lead generation funnel actually being redesigned for AIO?

- What’s the realistic timeline for migrating off the old top-of-funnel?

The funnel that defined two decades of lead generation – impressions to clicks to sessions to leads – runs on assumptions that the data no longer supports. Operators who rebuild around citation share, prompt-cluster coverage, and AI-source-segmented conversion outperform operators who optimize the old metrics harder. The cliff is not a passing storm. It is the new floor.

Sources

- Seer Interactive, “AIO Impact on Google CTR: September 2025 Update,” September 2025 – Original CTR collapse study; 3,119 informational queries, 25.1M organic impressions, 42 organizations

- Pew Research Center, “Google users are less likely to click on links when an AI summary appears in the results,” July 2025 – Independent corroboration; 8% click with summary vs 15% without; 1% click inside summary

- Chartbeat (via Axios), “Small publishers hit hardest by search traffic declines,” March 17, 2026 – Publisher referral decline by tier: small −60%, medium −47%, large −22%

- Ahrefs, “Update: 38% of AI Overview Citations Pull From The Top 10,” 2026 – Citation-overlap collapse; 863,000 keywords, 4 million AIO URLs

- ALM Corp, “Google AI Overview Citations From Top-10 Pages Dropped From 76% to 38%,” March 2026 – Analysis of the seven-month overlap shift and Gemini 3 implications

- ALM Corp / BrightEdge, “Google AI Overviews Surge 58% Across 9 Industries,” 2026 – Trigger rates by vertical: healthcare, education, B2B tech, finance, eCommerce

- Engadget, “Gemini 3 is now Google’s default model for AI Overviews,” January 27, 2026 – Gemini 3 promotion; AI Mode integration; rollout scope

- Google Blog, “AI Mode in Google Search expands to more than 40 new areas,” 2026 – AI Mode coverage in 200+ countries, 35+ new languages

- Frase.io, “Are FAQ Schemas Important for AI Search, GEO & AEO?,” 2026 – FAQPage citation rate research; schema combination effects

- Stackmatix, “Optimizing FAQ Schema for Google AI Overviews,” 2026 – Compound schema lift; FAQ + Article + BreadcrumbList stack

- ProGEO.ai (via GlobeNewswire), “ProGEO.ai research finds 7.4% of the Fortune 500 have implemented llms.txt,” March 31, 2026 – llms.txt adoption data

- Press Gazette, “Global publisher Google traffic dropped by a third in 2025,” 2026 – Cross-publisher confirmation of Google referral decline

- Microsoft Clarity, “AI Traffic Converts at 3x the Rate of Other Channels,” 2025 – AI-referred conversion benchmarks

- averi.ai, “AI Search Visitors Convert 23x Higher” / B2B SaaS Citation Benchmarks Report, 2025–2026 – Conversion segmentation by AI source: ChatGPT, Claude, Perplexity, Gemini

- Ahrefs, “Brand Radar – AI visibility tracking documentation,” 2026 – AI prompt tracking, citation-share methodology