Eighteen months in, the SDK is the single point of failure no insurance lead-gen operator can ignore.

Eighteen Months Later, the Allstate File Reads Like an Operator Playbook in Reverse

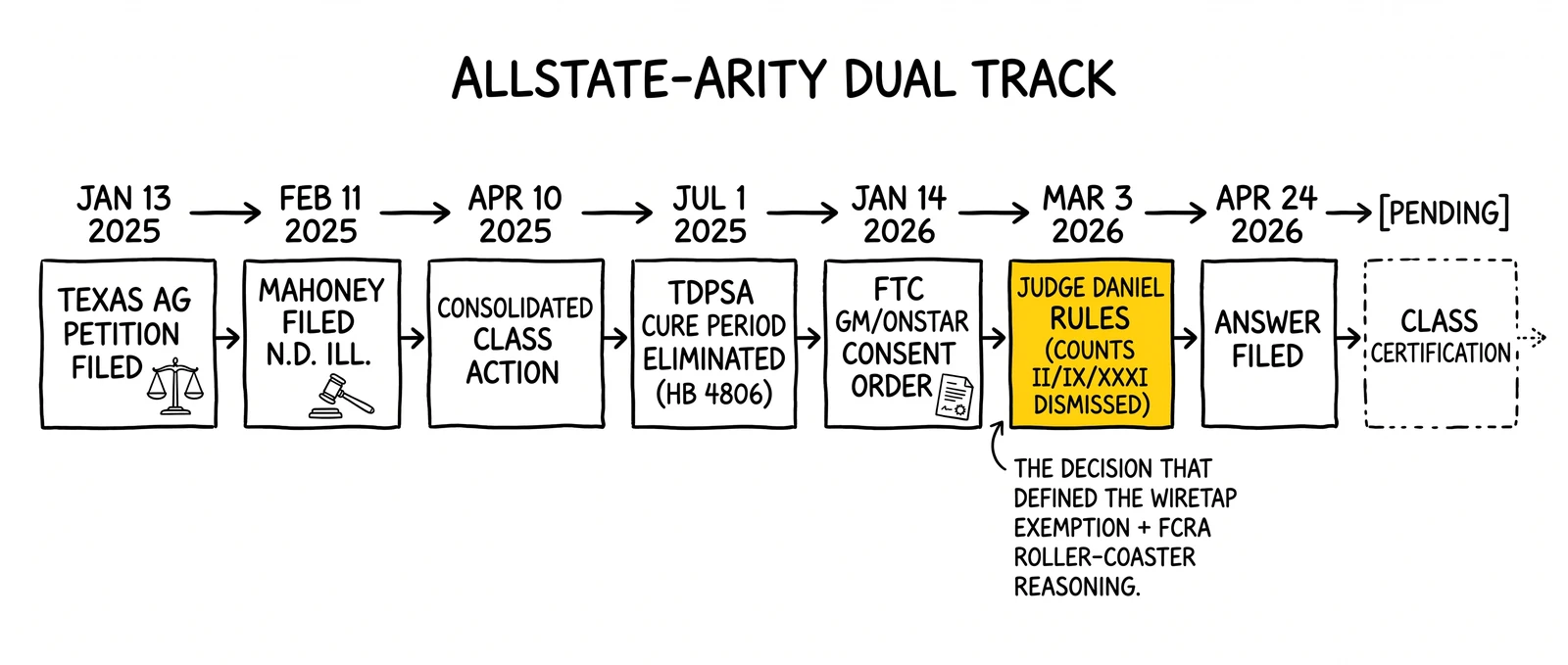

On January 13, 2025, the Texas Attorney General filed State of Texas v. Allstate Corporation et al. and made the case file the first ever comprehensive-privacy-law enforcement action by a state AG in U.S. history. The petition named Allstate Corporation and three Arity entities and alleged that defendants paid third-party app developers to embed an SDK in Life360, GasBuddy, Fuel Rewards, and Routely to collect geolocation and driving-behavior data from over 45 million Americans without notice, consent, or an opt-out, then sold that data into the insurance underwriting market.

Eighteen months later, the file has produced a parallel federal class action (Mahoney v. Allstate Corporation et al., No. 1:25-cv-01465, N.D. Ill.) that survived a motion to dismiss on wiretap and Fair Credit Reporting Act counts, an answer from defendants filed April 24, 2026, and a working compliance template every insurance lead-gen SDK embedder, ping-post operator, and telematics data buyer now inherits whether or not they litigated a thing. The compliance posture defined by these two cases is the one regulators, plaintiffs’ lawyers, and class-action insurers will price against for the rest of the decade.

The lead-generation implication is direct. Any operator running an SDK inside a third-party mobile app, any carrier buying telematics-enriched insurance leads, and any data partner monetizing geolocation now has to read the Texas petition and Judge Daniel’s March 3, 2026 ruling the way TCPA operators read Mims v. Arrow Financial Services: as the legal substructure under everything they do. The Allstate-Arity file is not a story about Allstate. It is the operator playbook in reverse – the explicit catalog of what state regulators and federal courts will treat as actionable.

The Texas Petition: First TDPSA Action, First Real Test of the State-AG Privacy Toolkit

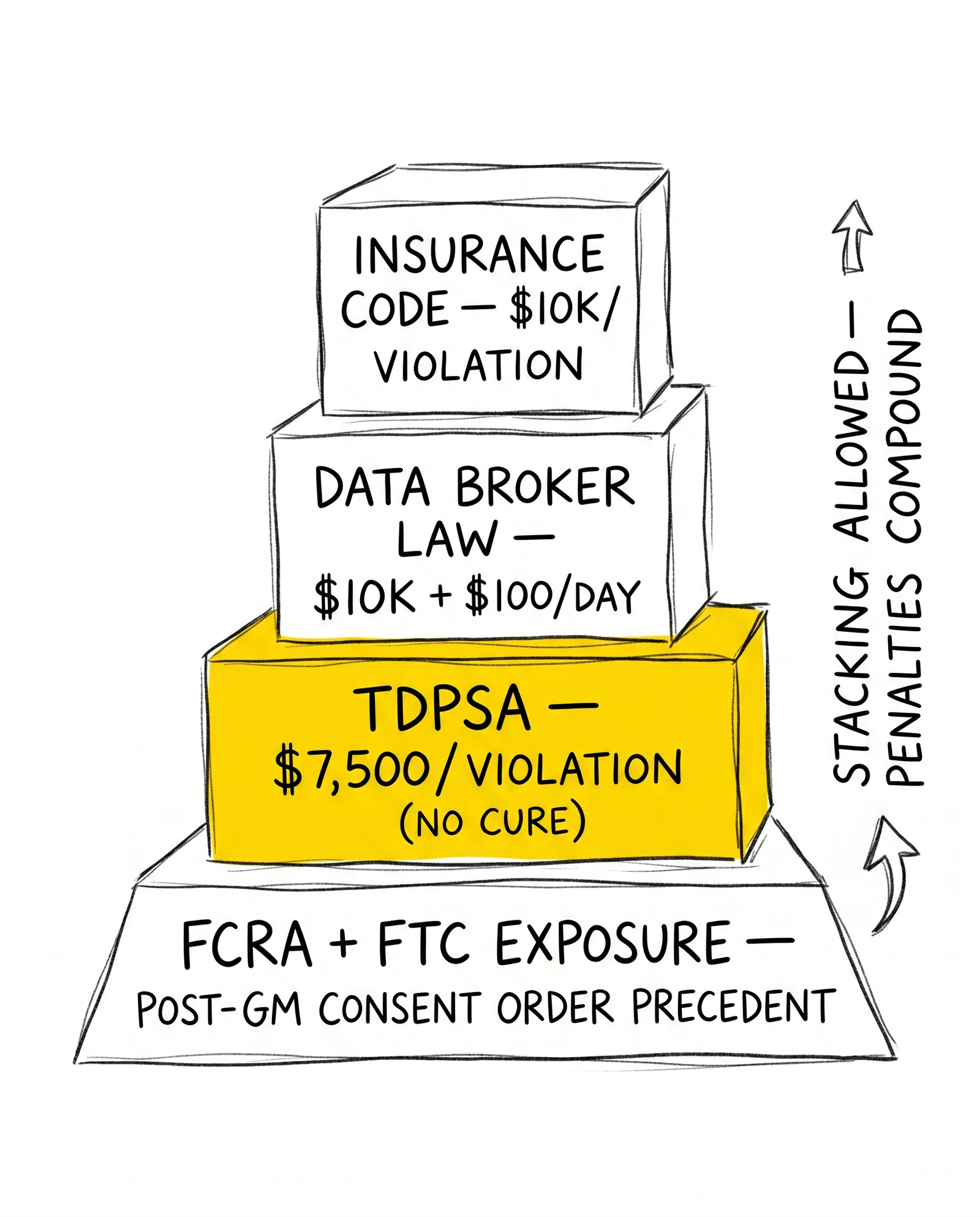

The Texas Data Privacy and Security Act took effect July 1, 2024 and is among the most operator-relevant comprehensive privacy laws in the country because Texas is the second-largest auto-insurance market by direct written premium. The statute gives the Texas Attorney General exclusive enforcement authority. It does not provide a private right of action, which means the AG petition is the operative threat vector – not class actions filed under the TDPSA itself.

Civil penalties run up to $7,500 per violation, and each affected consumer is treated as a separate violation. For a 45-million-consumer dataset, the arithmetic exceeds $300 billion in theoretical exposure if every record counted as a separate violation, which no court will allow but which establishes the negotiating posture the Texas AG brought to settlement talks. The Texas Insurance Code adds $10,000 penalties per violation for unfair or deceptive practices in the insurance industry. The Texas Data Broker Law adds another $10,000 per registration violation plus $100 per day of unregistered operation.

The petition pleads four buckets of TDPSA conduct: failure to provide a reasonably accessible and clear privacy notice; failure to obtain consent for sensitive data processing (geolocation is sensitive under TDPSA § 541.001(28)); failure to provide an opt-out for sale of personal data; and failure to recognize and respond to opt-out preference signals. The petition then layers on the Texas Data Broker Law (Bus. & Com. Code Ch. 509) for failure to register and the Texas Insurance Code for treating SDK-acquired data as driving behavior for underwriting purposes without verifying consent.

What the Cure Period Was and Why It Is Gone

The TDPSA originally included a 30-day cure period during which the AG would notify a company of an alleged violation and give it a window to fix the conduct before suit. Operators relied on this period as a compliance lifeline. Texas HB 4806, signed in 2025 and effective September 1, 2025, eliminated the automatic cure period and made any cure-period grant discretionary with the AG. After September 2025, new TDPSA enforcement is filed without any pre-suit cure window at the AG’s option, and the Texas Insurance Code counts attached to insurance defendants never had a cure period to begin with.

For lead-gen operators, that change means the audit window closed retroactively. Anyone running an SDK in 2024 had a soft landing if they cured before notice. Anyone running one now faces direct suit and the negotiating leverage that comes with a $7,500-per-consumer civil penalty cap.

Five-State Cluster: Texas Is Just the First

State attorneys general in California, Colorado, Connecticut, Oregon, and Virginia all have active comprehensive privacy laws with operator-direct enforcement authority. The California Privacy Protection Agency has separately taken the position that insurance companies meeting CCPA thresholds must comply with the CCPA for personal information not covered under the California Insurance Code’s insurance-transaction definition, and that interpretation became effective January 1, 2026. The CPPA’s position narrows the historic safe harbor that insurance-sector data was outside CCPA scope and brings telematics-derived data inside the CCPA’s sensitive personal information opt-out regime.

The Colorado Privacy Act, Connecticut’s CTDPA, Virginia’s VCDPA, and Oregon’s OCPA all include opt-in obligations for sensitive data including precise geolocation. None of these AGs has filed an Allstate-style action yet, but each one has the legal authority to do so on the same fact pattern. Operators should expect at least one to follow Texas’s lead before the Mahoney class certification motion is decided.

Mahoney v. Allstate: What the March 3, 2026 Ruling Actually Held

Michael Mahoney and Scott Schultz filed Mahoney v. Allstate Corporation et al. in the Northern District of Illinois on February 11, 2025, less than a month after the Texas AG petition. On April 10, 2025, the court consolidated Mahoney with several parallel class actions filed in the same window. Plaintiffs filed the consolidated complaint on May 27, 2025. Defendants moved to dismiss on July 10, 2025. After briefing closed, U.S. District Judge Jeremy C. Daniel ruled on March 3, 2026, denying most of the motion and dismissing only Counts II, IX, and XXXI.

The surviving counts include the federal wiretap claim under Title III of the Omnibus Crime Control and Safe Streets Act, the Fair Credit Reporting Act claims targeting Arity as a consumer reporting agency, state consumer protection statute claims across multiple jurisdictions, and common-law intrusion-upon-seclusion claims. Defendants filed their answer to the surviving claims on April 24, 2026, which starts the discovery clock and the class certification briefing schedule. The court has not set a trial date.

The Crime/Tort Exemption Argument the Court Bought

The wiretap holding is the load-bearing element of the ruling. Defendants argued the apps that embedded the SDK had consented to interception of communications through their terms of service with users, and that party consent is a complete defense to wiretap liability. The court agreed the apps had consented but ruled plaintiffs successfully invoked the crime/tort exemption, which nullifies the party consent defense when the interception is conducted for the purpose of committing an independent criminal or tortious act.

Plaintiffs argued that the independent tortious purpose was the sale of geolocation data to insurance carriers without consumer consent under state privacy and consumer protection law, which itself constituted a tort. The court declined to dismiss that theory on the pleadings, which means SDK-based interception now reaches a jury on a federal wiretap theory wherever the underlying data sale is alleged to violate state law. That is a significantly broader risk surface than the party-consent rule alone left open.

The FCRA Holding and the Roller-Coaster Footnote

The court declined to dismiss the FCRA counts on the theory that Arity functions as a consumer reporting agency because its outputs are used by insurance carriers to make eligibility and pricing decisions. The court specifically noted plaintiffs’ allegation that the SDK records phone movement and labels it driving behavior even when the user is riding as a passenger on a bus, in a taxi, or on a roller coaster, which goes to whether the resulting reports are reasonably accurate as required under 15 U.S.C. § 1681e(b).

The FCRA holding has independent significance for any lead-gen operator whose product feeds into an underwriting or eligibility decision. Arity is already listed on the Consumer Financial Protection Bureau’s consumer reporting companies list, which is the agency’s public registry of entities receiving consumer disputes. Operators selling enriched leads into eligibility, pricing, or pre-screen flows should assume the same FCRA classification analysis will apply to them.

What Got Dismissed and Why It Matters Less

Counts II, IX, and XXXI were dismissed. The Computer Fraud and Abuse Act count fell because plaintiffs could not plead the access-without-authorization element on facts where the apps had embedded the SDK voluntarily. Two state-law counts fell on standing or jurisdictional grounds. None of the dismissals reached the core wiretap, FCRA, or state consumer-protection theories. The case proceeds to discovery on the substantively material claims.

The Consolidated Complaint’s Class Definitions and Why They Matter for Operator Reserves

The Mahoney consolidated complaint pleads multiple subclasses, including a nationwide federal-claims class for wiretap and FCRA violations, a Texas subclass tied to the conduct also pleaded by the Texas AG, an Illinois subclass under the Illinois Biometric Information Privacy Act and state consumer protection statutes, and California and Florida subclasses under state-specific privacy and consumer protection laws. The subclass structure determines the damage exposure if the case reaches certification and trial.

The federal wiretap statute provides statutory damages of the greater of $100 per day of violation or $10,000 per plaintiff, plus punitive damages and attorneys’ fees. With 45 million putative class members and an alleged multi-year collection window, the statutory damage math under the wiretap counts alone reaches into the trillions of dollars before any settlement discount. No court will award the full statutory cap, but the negotiating posture sets the floor for any class-wide resolution.

FCRA statutory damages run from $100 to $1,000 per violation for willful violations, plus actual damages for negligent violations and attorneys’ fees. The subclass mechanics under FCRA depend on whether the court treats each consumer report furnished as a separate violation, which is the prevailing approach in the Seventh Circuit. Operators evaluating their own FCRA exposure should run the math at $1,000 per affected consumer, not the lower $100 floor.

The class certification motion is the next major inflection point. The court has not set a schedule, but discovery is now active under the April 24, 2026 answer. Realistic timing puts the certification briefing in late 2026 or early 2027, with a ruling in the first half of 2027. Operators should not assume the case will settle before certification – defendants who fight motion to dismiss this aggressively typically fight certification as well, and the cleanest defense path runs through arguing common-issue failure on the consent record.

The FCRA Holding Read Carefully: Consumer Reporting Agency vs. Furnisher

The FCRA holding deserves a separate look because most lead-gen operators read FCRA exposure through the furnisher lens – the obligation under § 1681s-2 to report accurate information to consumer reporting agencies. Mahoney runs through the consumer reporting agency lens – the broader and harder-to-escape obligation under §§ 1681a(f), 1681b, 1681e, and 1681g that attaches to any entity that regularly assembles or evaluates consumer credit information for the purpose of furnishing consumer reports to third parties.

Arity is alleged to be a CRA because it assembles driving behavior data, derives a driver score from it, and furnishes that score to insurance carriers for use in eligibility, pricing, and underwriting decisions – all of which qualify as permissible purposes under § 1681b(a). The classification matters because CRAs carry obligations furnishers do not: the maximum-possible-accuracy reasonable procedures requirement of § 1681e(b), the disclosure obligations to consumers under § 1681g, the reinvestigation duties under § 1681i, and the prohibition on furnishing reports for impermissible purposes.

For lead-gen operators whose data products feed into eligibility or pricing decisions, the FCRA classification analysis runs in two steps. First, does the operator regularly assemble or evaluate consumer information? If yes, then second, does the operator furnish that information to third parties for use in decisions about credit, insurance, employment, or other FCRA-permissible purposes? If yes again, the operator is a CRA and inherits the full CRA obligations regardless of how the operator describes itself.

The Mahoney ruling’s specific quote – that the SDK records phone movement and labels it driving behavior even when the user is riding as a passenger on a bus, in a taxi, or on a roller coaster – goes to the § 1681e(b) maximum-possible-accuracy obligation. The court held plaintiffs adequately pleaded that Arity’s procedures do not meet that standard because the SDK cannot distinguish driver from passenger. That theory generalizes immediately to any lead-gen operator whose data product cannot reliably distinguish the labeled behavior from confounding behavior. A telematics product that cannot distinguish driver-vehicle from passenger-vehicle, a behavioral product that cannot distinguish account-holder from co-resident, an eligibility flag that cannot distinguish current state from historical state – all of those are § 1681e(b) exposure under the Mahoney reading.

The CFPB Listing and Why It Is the Cheapest Diagnostic

Arity appears on the Consumer Financial Protection Bureau’s consumer reporting companies list. That listing is the CFPB’s public registry of entities consumers can dispute reports with, and it is the cheapest diagnostic for whether the agency itself treats a company as a CRA. Operators whose data feeds insurance, credit, employment, or eligibility decisions should check whether they appear on the list. If they do, the FCRA classification debate is effectively over and the compliance obligations attach. If they do not, they should still run the two-step classification analysis above and be prepared to register if the analysis indicates CRA status.

The Lead-Gen Operator Math: What Changes in the Next 12 Months

The Allstate file rearranges the compliance pricing on three operator profiles. Each one has to make decisions before the Mahoney class certification motion gets briefed.

Profile 1: Operators Running Their Own SDK Inside Third-Party Apps

This is the Allstate-Arity profile. If an operator embeds an SDK in a partner app to acquire data the partner’s user did not directly disclose to the operator, the operator now carries: TDPSA exposure in Texas; CCPA sensitive-information exposure in California; opt-in exposure in Colorado, Connecticut, Virginia, and Oregon; federal wiretap exposure under the crime/tort exemption framework; FCRA exposure if the data feeds underwriting; data broker registration exposure in California, Vermont, Texas, and Oregon; and class-action exposure under state privacy torts.

The mitigation set is narrow. The operator needs an explicit consent capture inside the partner app’s onboarding flow that names the operator, names the data categories, names the downstream commercial purposes including insurance underwriting and data sales, and is paired with a documented opt-out path. A blanket privacy policy buried in app settings is not adequate. A click-wrap consent with a single accept-all button does not name the operator separately from the app and does not survive the Allstate fact pattern.

Profile 2: Carriers Buying Telematics-Enriched Insurance Leads

Carriers buying telematics-enriched auto-insurance leads from ping-post networks or data partners now carry derivative exposure. Under TDPSA, the carrier is a controller receiving personal data and inherits the obligation to verify that the data was processed lawfully upstream. The FTC’s January 14, 2026 consent order with General Motors and OnStar bans GM from disclosing precise geolocation and driver-behavior data to consumer reporting agencies for five years and requires affirmative express consent for 20 years on certain connected-vehicle data, which is the federal signal of where this enforcement direction is heading.

Carriers should require contractual representations from data sellers that include the consumer’s specific consent record, the SDK provenance chain, the registered data broker status in every applicable state, and the opt-out compliance record. Generic data-quality reps that do not address SDK provenance are not adequate. The contractual chain has to terminate at a consumer-level consent record, not at the data seller’s own statement.

Profile 3: Ping-Post Networks Routing Enriched Auto Leads

Ping-post auto-insurance networks have historically priced telematics-derived risk segments as a premium-CPL category because driving-behavior scoring lifted bid prices from multiple carriers. After Mahoney, enrichment data with an upstream SDK provenance carries two new risk dimensions: provenance risk (whether the original consent meets the strictest state’s standard), and re-use risk (whether downstream buyers’ use violates the original notice). Both risks attach to the network because the network is the data flow’s commercial nexus, even if the network never touched the SDK directly.

The operational change is that networks need to segment enrichment data by provenance class and price each class with a corresponding compliance reserve. SDK-derived enrichment data from third-party app embeds is the highest-risk class. Operator-disclosed quote-form data from a known consent capture flow is the lowest. Mixed-provenance data needs to be priced at the higher class. Networks that treat all telematics enrichment as a single bid-priced category are mispricing risk relative to the post-Mahoney legal environment.

What Counsel and Operators Should Do Now, Before the Class Certification Motion Lands

The Mahoney class certification motion will not be briefed for several quarters, but the procedural visibility it produces will catalyze copy-cat suits in other federal districts. Operators should treat the next three to six months as a compliance audit window.

Audit 1: Consent Capture Inventory

Pull every consent capture flow that touches geolocation, driving behavior, or any sensitive-data category. Document the disclosure language verbatim, the consent action (click, swipe, toggle), the linked privacy notice, and the data flow diagram showing every downstream recipient including third-party data buyers. Any capture flow that does not name the receiving operator separately from the app, does not enumerate downstream commercial purposes, and does not offer a contemporaneous opt-out is a Mahoney-exposed flow.

Audit 2: Data Broker Registration Status

California’s Delete Act, effective January 1, 2026, requires data brokers to register annually with the California Privacy Protection Agency and participate in the DROP centralized deletion system. Texas, Vermont, and Oregon have parallel registration regimes. The Texas Data Broker Law’s $10,000 penalty plus $100-per-day unregistered-operation penalty is the per-state operator math. Operators monetizing third-party-app-derived data should confirm registration in every state with an active regime and confirm they appear on the CFPB consumer reporting companies list if their outputs feed eligibility or pricing.

Audit 3: Vendor Contract Reps and Indemnities

Carriers and ping-post networks buying enriched leads need contractual representations from data sellers covering SDK provenance, consent record retention, registered data broker status, opt-out compliance, and indemnification for state-AG and class-action exposure. Generic data-quality reps are not adequate after Mahoney. The contractual chain needs to terminate at a consumer-level consent record producible on discovery demand.

Audit 4: FCRA Classification Review

Any data feeding into an insurance eligibility, pricing, or pre-screen decision should be assumed to trigger FCRA classification analysis. Operators should review whether the use of their data by downstream buyers makes the operator a consumer reporting agency under 15 U.S.C. § 1681a(f) and whether their reporting practices meet the § 1681e(b) reasonable accuracy standard, including the roller-coaster issue Judge Daniel flagged.

Audit 5: Document Retention and Litigation Hold Posture

The Mahoney consolidated complaint is now the working template plaintiffs’ bar will use for parallel suits in other federal districts. Operators with SDK exposure should confirm document retention policies cover SDK source code, deployment configuration, consent capture screens, partner agreements, and revenue records, and should be prepared to issue litigation holds on receipt of demand letters.

The Lead-Generation Industry’s Two Questions It Has Not Answered

The Allstate file forces the insurance lead-generation industry to answer two structural questions it has avoided.

Question 1: Is the Telematics-Enriched Lead Category Still Profitable After Compliance Reserves?

Telematics-enriched auto leads command a CPL premium because driving-behavior scoring lifts carrier bid prices. If networks now have to price a compliance reserve into every SDK-provenance lead to cover state-AG and class-action exposure, the net economics may not survive. The category may collapse back to disclosed-consent quote-form data with self-reported driving-behavior fields, which is a meaningful step backward in lead quality. Operators should run the economics with realistic litigation reserves before assuming the enrichment category will continue at current pricing.

Question 2: Will the SDK-Embedding Model Survive State-Level Opt-In Convergence?

If California, Colorado, Connecticut, Virginia, and Oregon all converge on an opt-in standard for SDK-acquired sensitive data – and the trajectory of the FTC’s GM-OnStar consent order suggests they will – the operational model of paying app developers to embed an SDK and harvest passive geolocation may not be viable at any consent-conversion rate that produces the dataset volume Arity built. The 45-million-American dataset Arity assembled is not reproducible under opt-in. New entrants should not assume they can replicate the model.

The strategic answer for new entrants is to build the dataset through directly disclosed consent flows at the point of data origination – quote forms, comparison shopping flows, dedicated insurance apps – where the consumer knows the operator and the commercial purpose. That is a slower and more expensive dataset to assemble, but it is the only one that survives the post-Mahoney legal environment intact.

Key Takeaways

- The Texas Attorney General filed the first comprehensive-privacy-law enforcement action in U.S. history on January 13, 2025, naming Allstate Corporation and three Arity entities for SDK-acquired driving data from over 45 million Americans, and seeking up to $7,500 per TDPSA violation plus Texas Insurance Code and Data Broker Law penalties. The case is the operator template for state-AG privacy enforcement in 2026.

- U.S. District Judge Jeremy C. Daniel denied most of defendants’ motion to dismiss in Mahoney v. Allstate on March 3, 2026, with surviving wiretap, FCRA, state consumer protection, and privacy tort claims. The crime/tort exemption ruling means SDK-based geolocation harvesting can reach a jury on a federal wiretap theory wherever the underlying data sale violates state law.

- Defendants filed their answer on April 24, 2026, which starts the discovery clock and the class certification briefing schedule. The certification motion will produce procedural visibility that catalyzes copy-cat suits in other federal districts.

- Texas eliminated the TDPSA’s automatic 30-day cure period via HB 4806 effective September 1, 2025. New TDPSA enforcement now proceeds without a pre-suit compliance lifeline at the AG’s discretion.

- California’s CPPA insurance-sector clarification effective January 1, 2026 closed the previous safe harbor for insurance-transaction data and brings telematics-derived data inside the CCPA’s sensitive personal information opt-out regime.

- The FTC’s January 14, 2026 consent order with General Motors and OnStar bans precise-geolocation and driver-behavior sharing with consumer reporting agencies for five years and requires affirmative express consent for 20 years, signaling federal enforcement direction on connected-vehicle data.

- Arity is listed on the Consumer Financial Protection Bureau’s consumer reporting companies list, providing a public consumer dispute pathway. Operators whose data feeds insurance eligibility or pricing decisions should assume FCRA consumer-reporting-agency classification analysis applies.

- Lead-gen operators running SDKs in third-party apps, carriers buying telematics-enriched leads, and ping-post networks routing enriched data each carry distinct post-Mahoney compliance exposure. The mitigation set is narrow and requires explicit consent capture flows naming the operator, downstream uses, and an opt-out path.

- The two unanswered industry questions are whether the telematics-enriched lead category remains profitable after realistic compliance reserves and whether the SDK-embedding model survives state-level opt-in convergence. The 45-million-American dataset Arity assembled is unlikely to be reproducible under opt-in standards.

Sources

- Attorney General Ken Paxton Sues Allstate and Arity for Unlawfully Collecting, Using, and Selling Over 45 Million Americans’ Driving Data to Insurance Companies (Texas Attorney General, January 13, 2025)

- Allstate and Arity Petition Filed (Texas Attorney General, January 2025)

- Mahoney et al v. Allstate Corporation et al, 1:25-cv-01465, U.S. District Court for the Northern District of Illinois (Justia Dockets)

- Mahoney et al v. Allstate Corporation et al, Complaint (PACER via Duane Morris, February 2025)

- Massive Win for Plaintiffs: Federal Court Keeps Wiretap and FCRA Claims Alive in Allstate/Arity SDK Tracking Class Action (National Law Review / CIPAWorld, March 2026)

- Allstate Driving Data Privacy Litigation Case Page (Keller Rohrback)

- Texas AG Brings First Ever Lawsuit Under a State Comprehensive Privacy Law (WilmerHale, January 21, 2025)

- Texas AG Sues Allstate for Violations of Texas Privacy Law (Hunton Andrews Kurth, January 2025)

- Texas Attorney General’s Landmark Privacy Lawsuit Signals New Era in Data Privacy Enforcement (White & Case)

- Court Allows Suit Alleging Allstate Collected and Sold Consumer Data to Move Forward (Repairer Driven News, March 19, 2026)

- Federal Court Allowing Allstate Auto Data Collection Class Action to Proceed (AM Best)

- Arity Consumer Reporting Company Listing (Consumer Financial Protection Bureau)

- How Allstate’s Data Broker Arity Sells Driver Data (U.S. PIRG)

- Texas Data Privacy and Security Act (Texas Office of the Attorney General)