The Fragmentation Problem May Be Hiding in Your Funnel

A meeting most operators in the lead economy will recognize: a buyer calls to dispute a batch of leads. The marketing director pulls the source data. The sales manager pulls the dialer logs. Operations pulls the routing rules. Compliance pulls the consent certificates. Finance pulls the invoices. After an hour, the team has five different versions of what happened to the same lead – five timestamps, five status labels, five identifiers – and no shared answer.

Nobody did anything wrong. The form fired. The validator validated. The router routed. The dialer dialed. Each system performed its job. The problem is that no system was responsible for the lead’s full commercial life. The record fragmented at every handoff, and reconstructing it became someone’s afternoon.

Operators often diagnose this as a sales problem or a marketing problem. It can be both. But underneath, it is usually an operating-architecture problem – and in lead-driven businesses, where leads carry acquisition cost, eligibility rules, consent evidence, routing logic, sales effort, return risk, and expected revenue all attached to a single record, that is the most expensive kind to leave unaddressed.

The MIT Lead Response Management Study, popularized by Harvard Business Review in 2011, found that companies calling an inbound web lead within five minutes were 21 times more likely to qualify it than companies waiting until minute thirty, and 100 times more likely to make initial contact at all. Fifteen years later, the average B2B response time across 939 companies surveyed in 2025 still sits measured in days rather than minutes, and only 23% of organizations contact a new lead within the five-minute window. The rules of the market have not changed. The architecture most companies use to operate inside those rules has not caught up.

Companies typically respond to revenue leakage by improving the visible parts of the funnel. They sharpen targeting. They tighten filters. They retrain reps. They add tools. Each can help. But once a lead leaves the form and starts moving through the stack, no one can reconstruct what happened to it without stitching together records from several systems and several people.

Every handoff may be defensible. Together, they create an open loop.

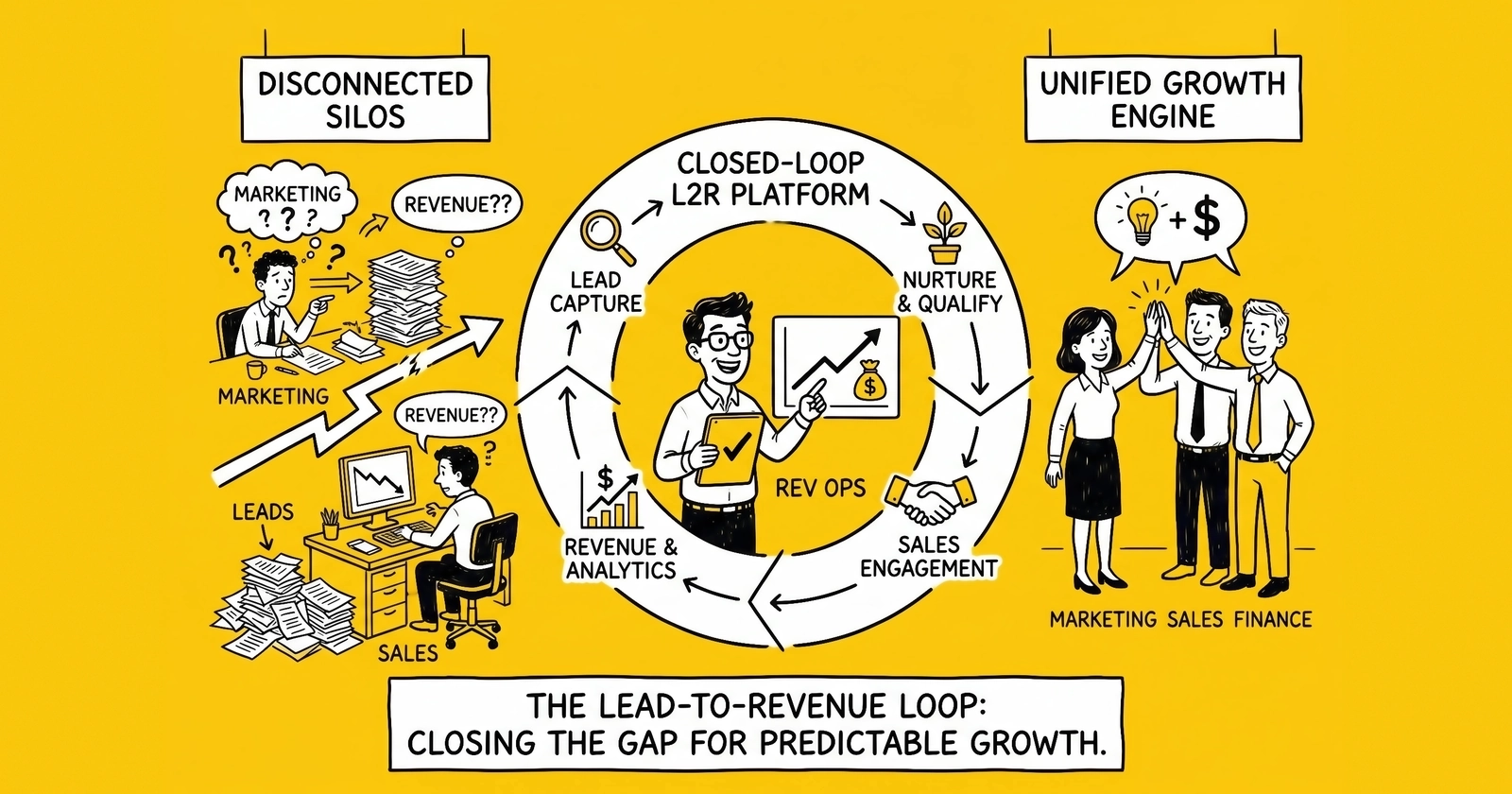

The next phase of lead-to-revenue performance will not be won by companies that generate more demand. It will be won by companies that can answer a harder managerial question: who owns the lead’s record from capture to revenue, return, refund, or loss? That is the case for closed-loop lead-to-revenue architecture.

Start With the Lead, Not the Software Stack

Most revenue-technology conversations begin with applications. CRM. Marketing automation. Dialer. Distribution. Attribution. Compliance vendor. Enrichment provider. That is how software is bought. It is not how revenue is produced.

Revenue is produced through a process. In lead-driven businesses, the process begins the moment a person expresses intent or is matched to a commercial offer. From that moment, the lead has a source, a timestamp, a consent record, qualification attributes, a routing path, an expected price or value, a buyer or owner, contact history, a disposition, and an eventual economic outcome. The managerial question is whether the business preserves those facts as the lead moves.

If the answer is no, the company is operating with an open loop. It may have dashboards, integrations, and sophisticated tools. But it still lacks a reliable, shared view of what happened to its asset.

A closed-loop lead-to-revenue platform is not a reporting layer. It is a system, or tightly integrated ecosystem, that manages the lead’s commercial life as a continuous operating record: capture, validation, compliance, routing, delivery, sales engagement, disposition, conversion, revenue attribution, and feedback to the source. Forrester’s 2024 Wave: Revenue Orchestration Platforms for B2B, which evaluated 12 vendors against 29 criteria, formalized a category that absorbs what used to be split between lead-to-revenue management and standalone revenue-marketing tools. When the analyst category structure shifts toward unified architecture, procurement frameworks follow.

The distinction matters because the alternative has scaled past its own logic. Scott Brinker and Frans Riemersma’s 2025 marketing-technology landscape catalogues 15,384 distinct martech products, up 9% from 14,106 in 2024. Gartner’s Marketing Technology Survey tracked stack utilization at 58% in 2020, 42% in 2022, 33% in 2023, and a partial recovery to 49% in 2025 – meaning roughly half of the capability organizations are paying for sits idle. Zylo’s 2025 SaaS Management Index, drawn from over 40 million licenses and $40 billion in spend under management, reports that 52.7% of provisioned SaaS licenses go unused, with the average organization wasting $21 million annually on those unused licenses alone, up from $18 million in 2024. The default trajectory of a stitched stack is duplication, drift, and waste.

When the lead record stays intact, leaders can answer questions that directly affect revenue: which sources produce profitable leads, which buyers reject most often and why, which routing rules introduce delay, which teams work high-value leads fastest, which compliance artifact belongs to a disputed record, which integrations are quietly creating leakage. When the record breaks, the business debates symptoms. Forrester’s 2024 State of Business Buying found that 86% of B2B purchases now stall during the buying process and 81% of buyers express dissatisfaction with the providers they ultimately select. Continuity of experience across the funnel has become a deal-determining variable, and continuity is what an open loop cannot deliver.

Four Tests of a Closed-Loop Lead System

The phrase closed loop is used loosely. A dashboard is called a loop. A spreadsheet reconciliation is called a loop. A CRM report is called a loop. None is enough.

A real closed loop passes four tests.

The first is shared identity. The same lead must remain the same lead across the revenue process. That requires a canonical identifier or a reliable identity strategy that survives movement across source, distribution, buyer, sales, finance, compliance, and reporting systems. Without it, attribution becomes guesswork. Compliance retrieval slows. Duplicate handling drifts. Source quality becomes nearly unmeasurable. A lead can exist in every system and still be understood in none.

The second is shared state. A lead is not static. It moves through condition: received, accepted, rejected, duplicated, enriched, capped, routed, sold, delivered, assigned, attempted, contacted, quoted, converted, returned, refunded, disqualified. The value of a lead-management system depends on whether those state changes are visible to the teams and partners that need them. If a source does not know why leads are being rejected, it cannot improve quality. If sales does not know source context, it cannot prioritize intelligently. If operations cannot see where a lead stalled, it cannot fix the process.

The third is shared accountability. When a lead fails, the organization needs to know why. Was the lead invalid? Did consent fail? Did the buyer reject it? Did the delivery endpoint time out? Did a rep not call? Did a call happen and go undispositioned? Did the disposition fail to flow back to the seller or source? In an open-loop stack, every vendor can plausibly point to another system. Forrester/SiriusDecisions data showing only 11% of organizations have jointly managed marketing-and-sales SLAs reflects how much definitional and accountability work most operations have deferred. In a closed-loop model, the process becomes diagnosable. Accountability moves from opinion to evidence.

The fourth is feedback latency. A loop is not closed merely because the company can inspect history after the fact. It is closed when downstream outcomes change upstream decisions quickly enough to matter. Close rates, returns, refunds, buyer feedback, source quality scores, compliance failures, sales dispositions – if any of these take days or weeks to reach acquisition, routing, pricing, and qualification decisions, the business is learning too slowly. The 2024 State of Attribution report from the Marketing + Media Alliance found that only 29% of marketers describe themselves as best-in-class at attribution, and 64% of CMOs say attribution directly drives their budgeting. The two findings together describe a market where most operators are budgeting from data they do not trust. In high-velocity lead markets, slow feedback is not an analytics inconvenience. It is a margin problem.

These four tests are diagnostic, not aspirational. They describe what an operating loop must do to deserve the name. Many systems that call themselves closed-loop fail at least one. Some fail all four and survive on the strength of a dashboard.

Where Open Loops Lose Money

The costs of an open loop are easy to misdiagnose. Leaders blame lead quality, rep discipline, channel mix, vendor performance. Those problems may be real. But in many organizations, the deeper issue is that the operating model cannot preserve lead state across handoffs. The symptoms recur in five places.

Speed-to-lead decay. A lead that should move instantly from inquiry to routing to contact loses minutes at each integration point. The form posts to a distribution system. The distribution system runs validation. The CRM receives the record. The dialer queues it. A rep is notified after assignment logic runs. Each step adds latency, and latency compounds. The 2025 lead-response benchmark covering 939 B2B companies found that leads contacted within five minutes close at 32% versus 12% for leads contacted after 24 hours – a 2.6× spread that is entirely a function of clock time. The five-minute rule is often discussed as a sales-discipline problem. In many companies, it is an architecture problem. Reps cannot work leads they have not received. Managers cannot enforce service levels they cannot measure. Marketers cannot optimize campaigns when response delays vary by source, buyer, campaign, and routing path.

Lead leakage that is really state loss. Lead leakage is usually described as leads falling through the cracks. The phrase is accurate but imprecise. Leads do not so much fall through cracks as get lost when the business loses state. The long-cited MarketingSherpa figure that 79% of marketing leads never convert points at the same pattern. Forrester/SiriusDecisions Demand Waterfall data put the average sales-accepted-lead rate at 42%, against 85%+ for tightly aligned organizations. A spread that large is rarely a coaching problem alone; it usually points to a handoff problem. Leads do not get rejected so much as get lost – assigned to a rep who left, queued under a status that the marketing team cannot see, or contacted with a script that conflicts with what the campaign promised.

Attribution that is really an identity problem. Marketing teams often believe they have an attribution problem when they actually have an identity problem. If a source platform, distribution system, CRM, dialer, and reporting database each represent the same lead with a different identifier, the organization will struggle to connect spend to revenue no matter how sophisticated the model. McKinsey’s Five Facts on Customer Analytics found that intensive analytics users are 2.6× more likely than peers to outperform on ROI – and that the leading source of that advantage is unified data, not superior algorithms. McKinsey’s separate research on personalization documents revenue lifts of 5–15%, marketing ROI improvements of 10–30%, and acquisition-cost reductions of up to 50%, but only for organizations whose data architecture supports execution. The market keeps spending – too often against delayed or incomplete signals.

Compliance evidence as a retrieval problem. In regulated categories, consent and auditability are not administrative details. They are part of the commercial product. A lead without retrievable consent evidence can become a liability even when the original acquisition was legitimate. When consent artifacts, source records, delivery logs, and contact history live in separate systems, compliance becomes a reconstruction exercise – and reconstruction at the moment a regulator, attorney, or buyer is asking is the wrong time to discover the chain has gaps. In the current TCPA environment, the practical question is no longer whether consent was collected. It is whether the company can retrieve the consent record quickly, in context, and attached to the disputed lead.

Support that scales with vendor count, not problem complexity. The least-discussed cost surfaces at three in the morning. A buyer says leads stopped arriving. A source says dispositions are missing. A sales manager says reps are receiving duplicates. A campaign owner says conversions are not attributing. The internal team coordinates across vendors whose systems each show only part of the event. Resolution time scales with the number of vendors involved, not the complexity of the problem. This is where single throat to choke has practical meaning. It is not about blame. It is about clock time. In revenue operations, the cost of a defect is multiplied by the time it takes to identify ownership.

The Hidden Product: Support and Operating Expertise

Of the five symptoms above, support fragmentation is the one operators most often discover only after they have lived with it. It deserves its own treatment, because the support model is not adjacent to the architecture. It is part of it.

In a closed-loop platform, support is not merely customer service. It is operational diagnosis. The vendor can see the lead state, the routing decision, the delivery attempt, the engagement history, and the outcome in one context. That changes the nature of support from ticket routing to process resolution.

The expertise dimension compounds the effect. Software alone does not consolidate a stack. The operator’s business process does, and translating that process into a platform’s state machine is where most consolidations succeed or fail. Vendors with category-specific operating histories carry institutional memory of regulatory cycles, attribution shifts, and consent-regime changes that generalist vendors do not – and that memory shows up in the customer success function at the moment a workflow needs to be redesigned, not the moment a feature ticket needs to be filed. Whether any specific vendor delivers on this promise is a question for reference customers and renewal histories. That the architectural opportunity exists at all is what separates a focused lead-to-revenue ecosystem from a generic stack.

This is the part of the consolidation case that does not appear in feature-comparison tables. It shows up in the resolution time when something breaks at three in the morning, in the workflow advice when a process needs to be redesigned, and in the implementation timeline when the people implementing the platform have done it before.

Which Seams Should Be Closed First?

The consolidation debate is usually framed as binary: platform or stack, all-in-one or best-of-breed. The better question is more precise. Which seams in the current process create the most economic, compliance, and operational risk?

In lead-driven businesses, four seams matter most.

The first is the seam between lead source and routing. If the source is not preserved cleanly through to the routing decision, quality feedback breaks immediately. The team can see that some sources produce more revenue than others; it cannot see why.

The second is the seam between routing and buyer delivery. If delivery state is unclear – was the lead accepted, rejected, capped, duplicated, lost – diagnosing buyer disputes becomes guesswork, and the seller’s pricing degrades because the feedback signal is too noisy to act on.

The third is the seam between delivery and sales engagement. If a lead reaches the buyer or sales queue but the action taken on it is delayed or invisible, the seller cannot learn and the buyer cannot optimize. This is where most speed-to-lead failures actually occur, and where they are hardest to attribute to a single owner.

The fourth is the seam between sales outcome and source feedback. If disposition and revenue do not flow back to the source quickly, the market cannot price quality accurately. The seller continues quoting averages. The buyer continues bidding on outdated quality scores. Both sides leave money on the table out of structural inertia.

A closed-loop platform creates value by closing these seams first. It does not have to replace every adjacent system on day one. In practice, most successful implementations are partially consolidated: they close the high-risk seams while preserving specialized tools where differentiation or contractual reality requires them. The honest planning question is not whether to consolidate but which seams the operation can no longer afford to leave open.

Why Best-of-Breed Often Breaks Down in Lead Operations

Best-of-breed software has a rational appeal. Specialized vendors move faster within their category, offer deeper features, and give buyers more leverage. For many enterprise functions, this logic remains sound. The lead economy is different because the commercial process is unusually handoff-sensitive.

The contrast is sharper when the dimensions are laid out together.

| Dimension | Best-of-Breed Stack | Closed-Loop Platform |

|---|---|---|

| Lead identity | Multiple identifiers reconciled across systems | One canonical identifier across the lifecycle |

| State changes | Synced via webhooks or batch jobs | Native, in shared data model |

| Speed-to-lead | Latency at every integration hop | Single chain, fewer hops, instrumentable |

| Attribution | Reconciled retrospectively from multiple stores | Built into the workflow |

| Compliance evidence | Distributed across consent, source, delivery systems | Stored against the lead record |

| Support model | Multi-vendor triage; operator runs point | Single-vendor accountability |

| Vendor leverage | Annual re-tender of each module | Concentrated in one renewal |

| Best fit | Differentiated capability, mature integration eng | Mid-market, latency-sensitive, compliance-heavy |

A best-in-class form tool, validator, CRM, dialer, and analytics platform may each perform well individually while the combined system performs poorly. The problem is not tool quality. It is process continuity.

The more handoffs a lead crosses, the more the business has to maintain – field mappings, status definitions, retry logic, duplicate handling, source identifiers, consent payloads, rejection reasons, buyer caps, call outcomes, suppression rules, billing records. At small volume, these seams are manageable. At high volume, they become the operating model. The company stops managing leads and starts managing integrations. Salesforce’s State of Sales found that 84% of sales teams without an all-in-one platform plan to consolidate their technology, a figure that reflects vendor self-interest in the conclusion but also a real operator preference: when the loop breaks, single accountability is faster than multi-vendor triage.

Best-of-breed remains the right call when a company has differentiated proprietary capability, mature integration engineering, unusual enterprise-scale leverage, or a sales motion materially different from the rest of the business. But many mid-market lead sellers, lead buyers, and performance marketers do not have those conditions. They need reliability, speed, traceability, and support more than they need theoretical modularity.

A Field Example: ClickPoint’s LeadExec and SalesExec

ClickPoint is a useful example because its products are organized around the commercial events that determine lead economics rather than around generic CRM objects. Founded in 2007 in Scottsdale, Arizona, the company has been shipping lead technology for roughly two decades, reports over 14,000 users on its public pricing page, and concentrates in the verticals where lead economics are most operationally exposed: mortgage, insurance, solar, higher education, home services, pest control, debt settlement, travel, and performance marketing.

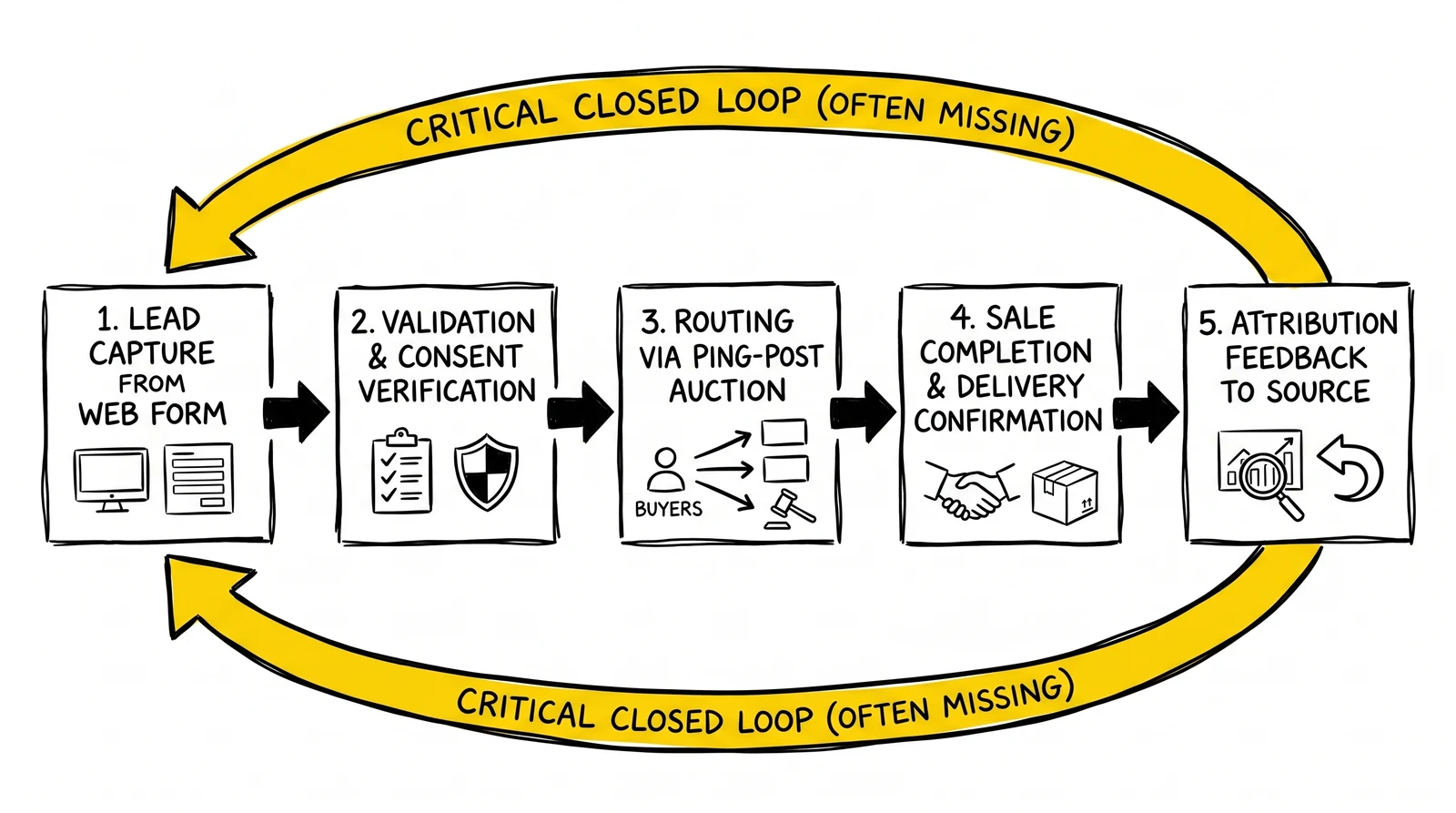

LeadExec addresses the seller-side and distribution mechanics: capturing, qualifying, routing, pricing, selling, and delivering leads to buyers, internal sales teams, branch locations, or other destinations. It is built for the realities of lead distribution – ping-post, lead selling, live call transfer, pay-per-call, delivery automation, consent-oriented capture. The customers who use it are lead generators, agencies, performance marketers, and aggregators who own the distribution side of the business. Pricing is unusually transparent for the category: a Starter tier at no cost for up to 250 leads and 10,000 pings per month, scaling through Growth ($660–$825 monthly), Agency ($1,650 monthly), and Premium ($2,500 monthly) tiers.

SalesExec addresses the buyer-side and sales-execution layer: lead management, prioritization, power dialing, SMS, email, reporting, call-center workflow, and sales-team follow-through. It is built to help the organization that receives or owns a lead work it quickly and consistently. Pricing starts at $450 per month for five users, with $72 per active user above the base.

The strategic significance is not that ClickPoint sells two products. It is that LeadExec and SalesExec connect the market-facing movement of a lead with the sales-facing work performed after receipt. Public ClickPoint documentation describes bidirectional data exchange between the two – synchronization of lead status, workflow, last action taken, and date closed – which is the operational substance of a closed loop. Sales outcomes can travel back into the lead-distribution record, so source feedback, routing decisions, buyer accountability, and dispute resolution all operate on the same record rather than on three reconciliations of it.

This pairing matters because broad horizontal CRMs often treat lead-market details as edge cases. Buyer caps, returns, duplicate rules, ping-post auctions, source-level quality feedback, branch routing, call transfers, delivery methods, contact attempts, disposition logic – in lead-driven markets, those details are not peripheral. They are the economics of the business. A platform that starts from those details rather than retrofitting them onto a generic contact object begins closer to the operator’s real workflow.

The publicly available customer outcomes are vendor-published and should be read accordingly. Two cases land cleanly because the architectural mechanism is identifiable. Direct Business Lending’s Roy Ferman reports moving from push-based routing with average first contact at 33 minutes to pull-based distribution targeting under five minutes – a 95% response-time compression that produced a 122% qualified-lead lift and a 35% revenue lift. The mechanism is the speed-to-lead arithmetic the article opens with, executed inside one platform rather than handed off across three. Rentokil’s Monica Brogan reports inside-sales contact rate moving from 22% to 65%, directionally consistent with what published research on local-presence dialing and priority cadence predicts when latency between lead arrival and first dial collapses. Other named ClickPoint customers – American Mortgage Group, TruGreen, Terminix, Steinway & Sons, Lendilio, Weboganic – report similar directional outcomes across mortgage, home services, global dealer networks, and performance-marketing operations.

The pattern, taken together, describes a class of architecture working as the underlying research says it should – not a guarantee that any individual case has been independently audited. Operators evaluating consolidation should treat published case studies as a starting point for reference calls, not a substitute for them.

ClickPoint is not presented here as the only model for closed-loop lead-to-revenue architecture. It is useful because it shows what the model looks like in a mid-market lead-economy context: seller-side distribution and buyer-side sales execution connected around the same lead record.

AI Raises the Cost of Bad Lead Data

The rise of AI strengthens the case for closed-loop architecture, and the strengthening is structural rather than thematic.

AI-assisted routing, scoring, qualification, summarization, coaching, next-best-action recommendations, and sales prioritization all depend on the quality and continuity of the underlying data. AI cannot reliably infer a broken lead record. It cannot know whether a missing disposition means a rep failed to act, a system failed to sync, a buyer rejected the record, or the lead converted somewhere else and the conversion never propagated back. It cannot safely optimize toward sources with high acceptance rates if downstream returns, refunds, and weak close rates never flow back into the model.

If source, consent, routing, contact history, and outcome are fragmented, AI does not solve the fragmentation. It adds confidence to an uncertain process. The model produces a recommendation that looks decisive on a slide and rests on data that cannot bear the weight. Salesforce’s State of Sales, 6th Edition found that 51% of sales leaders with AI initiatives say technology silos delay or limit their AI work – the operating data confirming the architectural argument.

This is why bolting AI features onto fragmented revenue stacks will disappoint many companies. The bottleneck is not model capability. It is operational context. A company that cannot preserve the state of a lead should be cautious about automating decisions based on that state. Closed-loop architecture gives AI something more useful to work with: a coherent sequence of events that the model can actually reason over. That does not make AI simple. It makes it grounded – and grounded automation is the kind that compounds rather than erodes operator judgment.

Implementation Reality

The case for closed-loop architecture is strong, but the migration deserves honest framing. Consolidation forces decisions that fragmented stacks let companies postpone, sometimes for years.

The first decision is data definition. What is a lead? What is a duplicate? What counts as accepted, rejected, returned, contacted, qualified, sold, converted, disqualified? Many organizations discover during migration that the same terms have meant different things to marketing, sales, buyers, finance, and support – and that the disagreements were silently producing reporting errors for years. Consolidation forces the definitional work the previous architecture allowed the company to skip.

The second decision is ownership of the lifecycle. If the lead is the unit of architecture, someone has to own the lead lifecycle as a whole – not just the CRM, not just marketing operations, not just sales operations, but the lifecycle itself. Many consolidations stall because no individual or team is willing to take that responsibility. The platform supports an owner; it does not create one.

The third decision is migration scope. Trying to replace every system at once creates unnecessary risk. A more disciplined approach starts with the seams where the business loses the most value – speed-to-lead, routing, compliance evidence, attribution, disposition feedback – and treats other consolidations as a second wave. The four-seam framing is a useful triage tool: close the seams first, then evaluate which adjacent tools the closed seams have made redundant.

The fourth decision is vendor concentration risk. Consolidation simplifies support and data flow, but it also increases dependency on the platform. Buyers should evaluate uptime, APIs, export capability, pricing structure, onboarding quality, roadmap credibility, and reference customers. Data-portability commitments and schema-export documentation belong in the contract, not in the renewal conversation three years later.

The fifth decision is change management. A better platform does not automatically create better behavior. Salesforce data places sales-rep selling time at roughly 28% of a typical week, with the remainder consumed by admin, prep, and system navigation. Reducing that overhead is the primary near-term ROI lever from consolidation. Capturing it requires retraining, workflow redesign, and frequently role consolidation. Underestimating this load is the single most common reason consolidation projects fail to deliver their stated business case in year one.

A reasonable benchmark for a mid-market operator: 90 days to migrate, six to twelve months to retire legacy systems fully, and 18–24 months before the consolidation’s productivity gains exceed its switching cost. Vendors with deep category playbooks and advisory-grade onboarding consistently report faster time-to-value than the headline benchmark suggests, but the timeline depends on whether the operator has done the definitional and ownership work the platform cannot do for them.

When Best-of-Breed Still Wins

A serious case for closed-loop platforms must hold space for where specialized tools remain rational.

Some organizations have proprietary scoring, identity resolution, compliance analytics, or sales-engagement logic that genuinely outperforms platform alternatives, and the differential matters enough to justify the integration overhead. Some have mature data engineering teams that treat integration architecture as a competitive advantage rather than a tax. Some sales motions are materially different enough from the rest of the business that a specialized engagement platform is worth keeping. Some procurement-scale operators negotiate per-unit pricing on best-of-breed tools that beats any platform offer at their volume.

Those conditions should be proven, not assumed. Many companies defend fragmented stacks because they value flexibility in theory while undercounting the daily cost of maintaining it. In lead operations, every integration is more than a technical connection. It is a place where lead state can break. The honest question is not whether best-of-breed is wrong. It is whether the organization can preserve identity, state, evidence, and feedback across its components reliably enough to earn the modularity.

Ten Questions for Operators Evaluating the Shift

Executives considering a closed-loop lead-to-revenue platform should resist turning the decision into a generic software comparison. The better evaluation starts with the process. Ten questions surface the answers that matter.

- What is our canonical lead identifier today, and how many systems carry their own version of it?

- Can we trace one lead from source to revenue, return, refund, or loss without manual reconciliation?

- Where does speed-to-lead latency enter the process, and which handoff contributes the most?

- How quickly do sales outcomes, buyer feedback, returns, and disputes flow back to acquisition and routing decisions?

- Where is consent evidence stored, and how quickly can we retrieve it in context for a regulator, an attorney, or a buyer?

- Which integrations generate the most support work, and which vendors are most often blamed for failures that turn out to be elsewhere?

- Which tools remain in the stack because of inertia rather than current value?

- What workflows truly require best-of-breed specialization, and what do those tools cost us at the seams?

- At our projected three-year headcount, do the platform’s per-seat economics still favor consolidation against a defensible best-of-breed alternative?

- Which vendor can support the process, not just the software module – and would they help us redesign a workflow, not just configure a tool?

The last question is the most revealing. A vendor that understands lead operations can advise on the workflow. A vendor that only understands its own feature set can only configure a tool. The difference shows up in the migration timeline, in the resolution time when something breaks, and in whether the AI roadmap of the next three years compounds the operator’s data or fragments it.

Key Takeaways

-

The four-test definition of a closed loop separates dashboards from real operating systems. Identity, state, accountability, and feedback latency are diagnostic, not aspirational; most operations describing themselves as closed-loop fail at least one. Run the four tests against the current architecture before evaluating any vendor.

-

Speed-to-lead arithmetic has not aged. The MIT/HBR finding that companies calling within five minutes are 21× more likely to qualify and 100× more likely to make contact is reproduced in 2025 data showing a 2.6× close-rate spread between five-minute and 24-hour responses. Architectural latency is a first-order revenue variable, not an IT concern.

-

Stack utilization is the underdiscussed cost of stitched stacks. Gartner’s 2025 data shows organizations using 49% of stack capability while paying for 100%; Zylo’s 40M+ license dataset places annual SaaS license waste at $21M per organization, up from $18M. The economic case for consolidation does not require a productivity miracle. It just requires retiring what is already not being used.

-

Support fragmentation is the cost most operators discover only at three in the morning. Resolution time on a stitched stack scales with the number of vendors involved, not the complexity of the problem. Forrester Total Economic Impact studies of unified IT support and endpoint platform consolidations have reported ticket-volume reductions of 35–65% and resolution-time reductions around 50% – directional read-across evidence from adjacent categories that the architecture is the leverage.

-

Vendor expertise belongs in the evaluation alongside features. TSIA’s 2025 research finds guided, structured digital customer-success journeys produce roughly a 30% net revenue retention lift over ad-hoc onboarding. Category-focused vendors with operating histories carry institutional memory that generalist vendors do not. Operators should evaluate whether the customer success function can advise on workflow redesign, not just configuration.

-

The four highest-risk seams are where the consolidation case is strongest. Source-to-routing, routing-to-delivery, delivery-to-engagement, and outcome-to-source-feedback are where lead state most often breaks in ways that affect revenue. Close those seams first; treat other consolidations as a second wave.

-

The ClickPoint LeadExec/SalesExec ecosystem illustrates the pattern at mid-market scale. The architecture is what travels – a lead-flow platform that connects distribution and sales execution around the actual economics of the lead lifecycle. Vendor choice matters; the architectural decision matters more.

-

AI raises the cost of bad lead data rather than fixing it. Salesforce data shows 51% of sales leaders with AI initiatives say technology silos delay their work. AI compounds whatever architecture it runs on. Operators investing in AI on a fragmented stack will find that the model amplifies the fragmentation rather than resolving it.

-

Migration realism beats migration optimism. A 90-day migration window, 6–12 month legacy retirement, and 18–24 months to productivity payback is the conservative benchmark. The variable that most reliably compresses that timeline is the vendor’s category experience.

-

An honest evaluation prices the consolidation against its less obvious costs. Vendor lock-in at renewal, per-seat economics at projected scale, the platform’s weakest module sitting in a critical workflow, and the reality that most working operations end up partially consolidated rather than fully unified. The architectural argument favors closing the high-risk seams; it does not require closing all of them.

Frequently Asked Questions

What is a closed-loop lead-to-revenue platform?

A closed-loop lead-to-revenue platform is a system or unified ecosystem that carries a lead through every state change in its commercial life – capture, validation, consent, routing, delivery, sales engagement, disposition, conversion, revenue attribution, and feedback to the source – without requiring human or batch reconciliation between systems. The practical test is whether the organization can trace a single lead from source to outcome using one canonical identifier and one shared state. Most operations describing themselves as closed-loop are not, by that test. The four diagnostic tests – shared identity, shared state, shared accountability, and feedback latency short enough to change upstream decisions – separate dashboards from real loops.

How is a closed-loop platform different from a CRM?

A CRM stores account, contact, opportunity, and activity records. A closed-loop lead-to-revenue platform manages the workflow around the lead itself, including the work a CRM typically delegates to upstream and downstream systems. It can include CRM-like capabilities, but its purpose is broader: preserve lead state across source, distribution, compliance, sales engagement, billing, and reporting. A CRM typically participates in the lead lifecycle; a closed-loop platform is designed around it. Forrester’s 2024 Wave: Revenue Orchestration Platforms for B2B, evaluating 12 vendors against 29 criteria, frames revenue orchestration as a unified layer adjacent to CRM rather than a feature of it.

Are unified platforms always better than best-of-breed point tools?

No. Best-of-breed remains rational when a company has differentiated proprietary capability, mature integration engineering, enterprise-scale per-unit pricing leverage, or a sales motion materially different from the rest of the business. The conditions should be proven against the operator’s actual data, not assumed. The unified-platform case becomes stronger as the cost of handoffs – speed-to-lead loss, attribution gaps, compliance retrieval, support fragmentation – exceeds the value of best-of-breed depth. Most mid-market operators in the lead economy are in that condition; many large enterprises are not.

Which handoffs deserve the most attention in a consolidation?

Four. Source-to-routing, routing-to-delivery, delivery-to-engagement, and outcome-to-source-feedback. These are the seams where lead state most often breaks in ways that affect revenue directly: quality feedback degrades, buyer disputes become unprovable, speed-to-lead decays at handoff, and pricing drifts because the market is bidding on outdated quality signals. A consolidation that closes these seams captures most of the available value. Other consolidations can follow as second-order decisions.

How much does a unified platform actually save on support?

Forrester’s Total Economic Impact studies of unified IT-support and endpoint-management consolidations have reported ticket-volume reductions of 35–65% and resolution-time reductions around 50% against prior multi-vendor baselines. Those studies are commissioned and cover adjacent categories rather than lead-to-revenue specifically, but the architectural mechanism reads across: when one organization owns every state transition, triage and resolution happen in one place. Gartner customer-effort research complements the picture from the demand side – low-effort interactions drive 96% loyalty versus 9% for high-effort ones, with reductions of up to 40% in repeat contacts and 50% in escalations. The exact savings vary by implementation; the directional signal is consistent.

Why does vendor expertise matter as much as platform features?

Software does not consolidate a stack. The operator’s business process does, and the work of translating that process into a platform’s state machine is where most consolidations succeed or fail. TSIA’s 2025 research finds that companies implementing guided, structured digital customer-success journeys see roughly a 30% lift in net revenue retention over ad-hoc onboarding. Vendors with category-specific operating histories carry institutional memory of regulatory cycles, attribution shifts, and consent-regime changes that generalist vendors do not. The customer-success function on a focused lead-to-revenue vendor can advise on workflow redesign; on a generalist vendor, it can usually only configure features. The difference shows up in implementation timelines and in resolution times when something breaks.

How long does a migration to a unified platform realistically take?

A defensible benchmark for a mid-market operation is 90 days for the technical migration, 6–12 months for full retirement of legacy systems, and 18–24 months before consolidation productivity gains exceed the switching cost. Operations that promise faster timelines tend to underestimate three things: the integration debt embedded in existing webhooks and reporting pipelines, the data-definition reconciliation required when “lead status” means different things in different systems, and the change-management load on sales and marketing teams. Forrester’s data showing only 11% of organizations operate jointly managed marketing-and-sales SLAs reflects how much definitional work most operations have deferred. Consolidation forces that work; it does not perform it.

Where does the lead-to-revenue category go from here?

Three trajectories are clear. The analyst category structure has consolidated – Forrester’s 2024 Wave: Revenue Orchestration Platforms for B2B treats unified architecture as the default. Buyer behavior has shifted toward self-directed multi-touchpoint journeys that punish architectural fragmentation: Gartner’s June 2025 Future of Sales research places rep-free buying preference at 61%, while Forrester’s 2024 State of Business Buying puts the average B2B buying group at 13 people across two or more departments. AI augmentation has emerged as the next investment frontier and depends on unified state to deliver compounding rather than incremental gains. None of these forces is a vendor’s marketing claim. They are the conditions every lead-economy operator now buys into when choosing an architecture, regardless of which specific platform they select.

Sources

- Oldroyd, J., McElheran, K., Elkington, D., “The Short Life of Online Sales Leads,” Harvard Business Review, March 2011 – drawing on the MIT Lead Response Management Study. https://hbr.org/2011/03/the-short-life-of-online-sales-leads

- Forrester Research, “The First Forrester Wave Evaluation of Revenue Orchestration Platforms Is Live” (announcement of the Q3 2024 Wave evaluating 12 vendors against 29 criteria). https://www.forrester.com/blogs/the-first-forrester-wave-evaluation-of-revenue-orchestration-platforms-is-live/

- Forrester Research, The State of Business Buying, 2024, press release, December 2024. https://www.forrester.com/press-newsroom/forrester-the-state-of-business-buying-2024/

- Forrester / SiriusDecisions, “When SLAs Between Marketing and Sales Are Really Just Marketing Selfies” – sales-marketing alignment and SLA research. https://go.forrester.com/blogs/whenslasbetweenmarketingandsalesarereallyjustmarketingselfies/

- Gartner, Marketing Technology research hub (2023 and 2025 Marketing Technology Survey, including stack-utilization series). https://www.gartner.com/en/marketing/topics/marketing-technology

- Gartner press release, “Gartner Sales Survey Finds 61% of B2B Buyers Prefer a Rep-Free Buying Experience,” June 25, 2025. https://www.gartner.com/en/newsroom/press-releases/2025-06-25-gartner-sales-survey-finds-61-percent-of-b2b-buyers-prefer-a-rep-free-buying-experience

- Gartner Customer Service & Support research, customer-effort score (CES) program. https://www.gartner.com/en/customer-service-support/research/customer-service-score

- McKinsey & Company, “Five Facts: How Customer Analytics Boosts Corporate Performance.” https://www.mckinsey.com/capabilities/growth-marketing-and-sales/our-insights/five-facts-how-customer-analytics-boosts-corporate-performance

- McKinsey & Company, “What Is Personalization?” (revenue, ROI, and CAC impact data). https://www.mckinsey.com/featured-insights/mckinsey-explainers/what-is-personalization

- Marketing + Media Alliance, State of Attribution 2024 – 8th Annual Marketer Benchmark Report. https://mmaglobal.com/documents/state-attribution-2024-marketer-benchmark-report

- Brinker, S. and Riemersma, F., “2025 Marketing Technology Landscape Supergraphic – 100x Growth Since 2011, but Now with AI,” chiefmartec.com, May 2025. https://chiefmartec.com/2025/05/2025-marketing-technology-landscape-supergraphic-100x-growth-since-2011-but-now-with-ai/

- Zylo, 2025 SaaS Management Index (40M+ licenses, $40B+ spend under management). https://zylo.com/news/2025-saas-management-index/

- Salesforce, State of Sales, 6th Edition, 2024. https://www.salesforce.com/resources/research-reports/state-of-sales/

- Forrester Consulting (commissioned by Microsoft), The Total Economic Impact of Microsoft Unified, 2024 – 35% reduction in product-related IT support tickets. https://tei.forrester.com/go/microsoft/unified/

- Forrester Consulting, Total Economic Impact of Workspace ONE UEM (Omnissa, formerly VMware), 2024 – 65% endpoint-ticket reduction and 50% MTTR reduction. https://www.omnissa.com/insights/blog/forrester-tei-report-170-roi-workspace-one-uem/

- TSIA, “The State of Customer Success 2025.” https://www.tsia.com/blog/the-state-of-customer-success-2025

- Optifai, 2025 Lead Response Time Benchmark (n=939 B2B companies). https://optif.ai/learn/questions/lead-response-time-benchmark/

- ClickPoint Software, lead-to-revenue platform (LeadExec, SalesExec). https://www.clickpointsoftware.com

Closing

Lead companies have spent years optimizing campaigns, landing pages, filters, buyer relationships, call scripts, sales cadences, and reporting dashboards. Those optimizations still matter. The next constraint is increasingly architectural.

A business that cannot see where a lead came from, where it went, who worked it, what happened, what it earned, and why it failed is managing revenue through fragments. A business that can preserve those facts is managing revenue through a loop. The distinction will compound as acquisition costs rise, buyers demand faster and more relevant responses, compliance scrutiny tightens, and AI pushes companies to automate decisions that depend on clean upstream data.

ClickPoint’s LeadExec and SalesExec ecosystem is one credible illustration of this shift – a focused lead-to-revenue platform connecting distribution and sales execution around the actual economics of the lead lifecycle. The lesson is larger than any single company. In lead-driven markets, architecture is not back-office plumbing. It is revenue governance: the operating system through which a company decides which leads to buy, which to sell, which to route, which to reject, which to work first, and which to stop funding.

The question is no longer just how many leads a company can generate. It is whether the company can account for what happens to them.