MDL 3060 crossed 11,371 plaintiffs in June 2026 - and the intake math that funded that ramp is now the math every late-entry operator is racing to defend.

The Number That Reset the Docket

The Judicial Panel on Multidistrict Litigation reports 11,371 cases pending in MDL 3060, In re: Hair Relaxer Marketing, Sales Practices, and Products Liability Litigation, as of June 2026. The docket sits before Judge Mary M. Rowland in the U.S. District Court for the Northern District of Illinois, who took the consolidation on February 6, 2023 after the JPML’s transfer order pulled 50-plus federal-court actions into a single pretrial pipeline. Roughly 15,000 new cases were filed during the 2026 calendar year through the June reporting cutoff. Cumulative case count, including resolved and dismissed actions, sits near 15,500.

For a docket that started 2024 below 9,900 pending cases, the trajectory is the steepest in the federal mass tort book outside the legacy AFFF and Bard Hernia Mesh growth phases. MDL 3060 is now the fourth-largest active MDL by case count and the largest open intake market in mass torts after the AFFF docket closed its filing window in September 2025. For lead operators, plaintiff-firm intake managers, and the brokers between them, the June 2026 number is the cleanest snapshot of a market that has roughly tripled in size in 30 months and is about to enter the price-discovery phase that bellwether trials always trigger.

This analysis maps the intake economics: the scientific anchor that underwrites general causation, the qualifying-condition gates that define a sellable lead, the named Plaintiffs’ Steering Committee firms that set the bid side of the market, the verified-versus-unverified CPL spread that determines defensible margin, the retainer-to-claim ratios operators should benchmark against, and the procedural calendar that will reprice every lead in the funnel over the next 18 months. It does not predict a settlement framework. It explains the math that intake firms are running against the framework’s range of plausible outcomes.

The Scientific Anchor: Sister Study and the 4.05 Percent Number

Every operator pricing hair relaxer inventory should be able to recite three numbers: 4.05 percent, 1.64 percent, and 50 percent. They come from the National Institutes of Health Sister Study analysis published October 17, 2022 in the Journal of the National Cancer Institute under lead author Che-Jung Chang. The study followed 33,497 women, average follow-up 10.9 years, with extensive baseline data on hair-product use, and reported that frequent users of chemical hair straighteners - defined as more than four uses in the prior 12 months - faced 4.05 percent uterine cancer incidence by age 70, versus 1.64 percent among never-users. The hazard ratio for frequent users versus never-users was 2.55. A subsequent 2024 NIEHS analysis from the same cohort reported a 50 percent increased ovarian cancer risk associated with frequent use.

The Sister Study sits at the top of the general-causation evidence stack for MDL 3060 because it is a federally funded prospective cohort study, not a pharma-industry retrospective. The NIEHS funding source, the JNCI publication venue, and the cohort design make the study harder to attack on Daubert grounds than the typical epidemiological inputs in product-liability MDLs. Roughly 60 percent of the women who reported straightener use in the prior year self-identified as Black, a demographic skew that maps directly to the racial pattern of the docket’s plaintiff population and informs both targeting strategy and the eventual disparate-impact narrative every PSC opening statement will run.

For intake operators, the Sister Study matters less as evidence and more as a screening anchor. Every qualifying intake script the named PSC firms run will collect: brand of product used, frequency of use (mapped to the more-than-four-per-year Sister Study threshold), duration of use, age at first use, and qualifying diagnosis date. Each field maps to a specific Daubert-defensible exposure metric. Leads delivered without those fields are not unscreened intake - they are economically inert intake that any plaintiff firm with a working intake team will reject inside 48 hours. The 60-to-75 percent rejection rate on unverified Facebook traffic that runs across mass torts is, in this docket, primarily a function of incomplete exposure documentation rather than incomplete medical documentation. The medical side is usually easier; the patient knows whether she has been diagnosed with uterine cancer. The exposure side requires effortful recollection across years or decades.

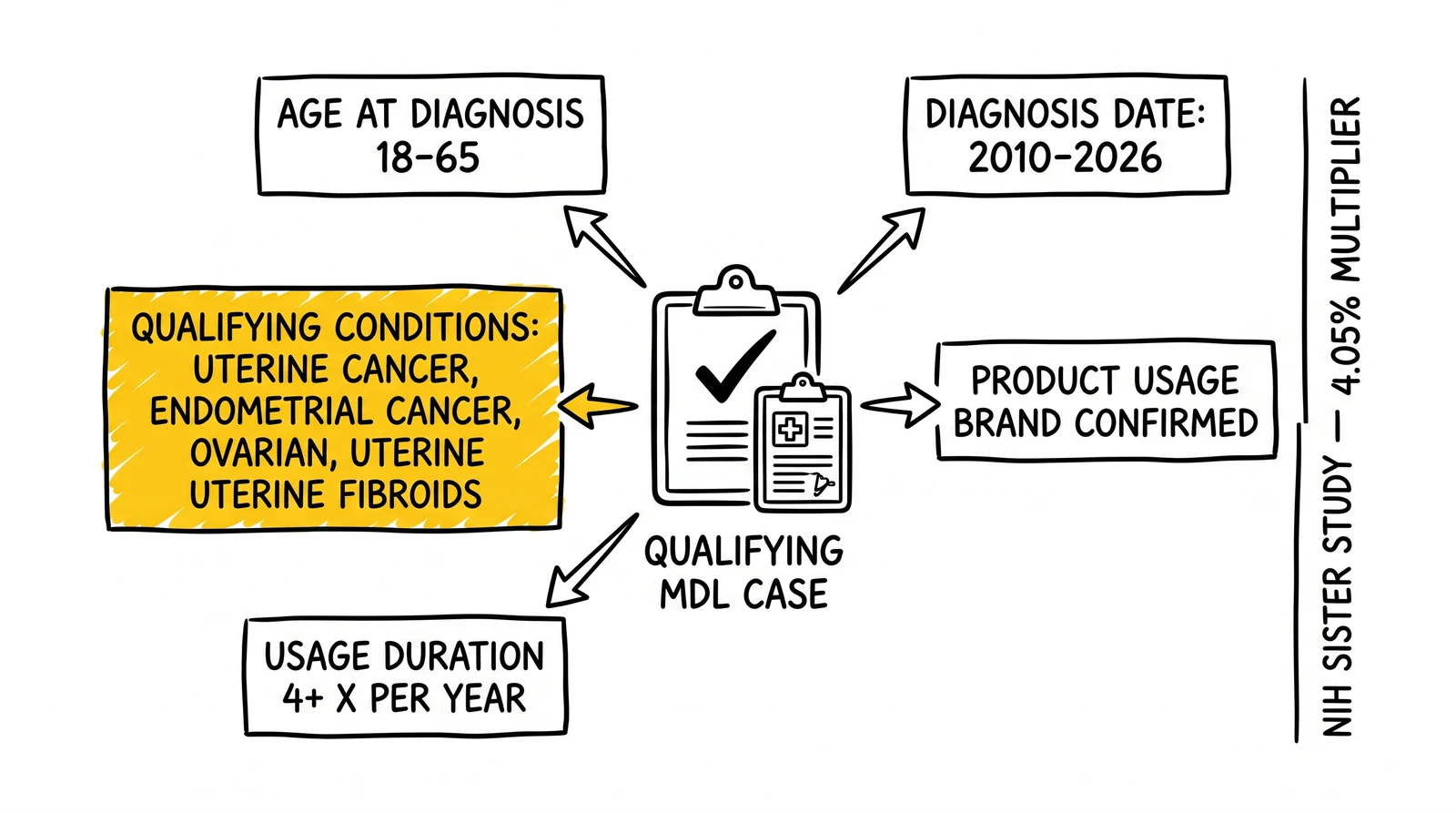

Qualifying Conditions: What Counts as a Signable Case

MDL 3060 pleads four primary cancer endpoints and one secondary track. The primary endpoints are uterine cancer (most common in the docket), endometrial cancer, ovarian cancer, and uterine leiomyosarcoma. Uterine fibroids requiring hysterectomy are pled as a secondary track and are tiered at substantially lower expected per-case settlement value by every named PSC firm. Some intake operators have begun running fibroid-only campaigns separately, treating the fibroid pool as a portfolio adjuster rather than primary intake, but the cleanest CPL-justifying inventory remains the cancer endpoints.

A signable case in the docket typically requires the intake to clear six gates. First, regular product use over at least 4 years - the Sister Study frequency-of-use threshold, refined upward by most PSC firms to require duration as well as frequency. Second, first exposure ideally before age 18, capturing the disproportionate pediatric initiation pattern documented across the Sister Study cohort and the racial-disparity data. Third, a qualifying diagnosis between 2000 and the present. Fourth, statute-of-limitations compliance under the filing-state’s discovery rule, which most plaintiff firms now interpret as a diagnosis date within roughly the prior 2 to 5 years given state-specific tolling and the late-2022 NIEHS publication as the public-knowledge anchor. Fifth, no prior representation by another firm or signed retainer in the docket - a clean conflict-check pass. Sixth, documented product-use history sufficient to identify at least one named defendant brand.

The most consequential gate in 2026 is the third - the qualifying diagnosis window. State statutes of limitations vary from 1 to 6 years, with discovery-rule tolling that pushes some claims past the 2022 Sister Study publication date and forecloses others. Operators running national campaigns without state-by-state SOL filtering routinely deliver leads that the PSC firms cannot file, which depresses headline conversion and corrupts the operator’s published CPL claims. The cleaner intake operations route the lead’s state of residence and diagnosis date into an SOL-eligibility check before delivery and price the residual inventory accordingly. The pricing differential between SOL-screened and unscreened inventory is roughly 30 to 50 percent at the verified tier; at the raw tier it can be a binary signable-or-not result.

The pediatric-initiation gate matters as well, and not for the reason the Sister Study language suggests. Most state SOL regimes toll the limitations period during minority, which makes claims first-exposed before age 18 mechanically harder for defense counsel to dispose of on SOL grounds even when the diagnosis date is older. Plaintiff firms price that legal durability into the intake tier above the headline use-frequency benchmark.

The Plaintiffs’ Steering Committee: Who Sets the Bid

Judge Rowland appointed the MDL 3060 leadership structure in a March 3, 2023 order. The leadership tier defines the demand side of the intake market: these are the firms with the inventory budgets, the verification operations, and the post-bellwether settlement positions that price every operator’s CPL ceiling. Operators selling into MDL 3060 without a clear view of which leadership-tier firm is the eventual buyer of the inventory are running blind.

Co-Lead Counsel: Benjamin L. Crump (Ben Crump Law Firm), Fidelma L. Fitzpatrick (Motley Rice LLC), Michael A. London (Douglas & London), and Diandra “Fu” Debrosse Zimmermann (DiCello Levitt LLC). Plaintiffs’ Liaison Counsel: Edward A. Wallace (Wallace Miller).

Plaintiffs’ Executive Committee: Brian Barr (Levin Papantonio Rafferty), Tim Becker (Johnson Becker), Jayne Conroy (Simmons Hanly Conroy), Kelly M. Dermody (Lieff Cabraser Heimann & Bernstein), Jennifer Hoekstra (Aylstock, Witkin, Kreis & Overholtz), LaRuby May (May Jung), Rene F. Rocha (Morgan & Morgan), Larry Taylor (The Cochran Firm), and Navan Ward (Beasley Allen).

Plaintiffs’ Steering Committee: Anne Andrews (Andrews & Thornton), Greg Cade (Environmental Law Group), Thomas P. Cartmell (Wagstaff & Cartmell), Andrew Childers (Childers, Schleuter & Smith), Erin Copeland (Fibich Leebron Copeland Briggs), Maria Fleming (Napoli Shkolnik), Lee Floyd (Breit Biniazan), Kendra Y. Goldhirsch (Chaffin Luhana), Kristine Kraft (Schlichter Bogard & Denton), Buffy Martines (Laminack, Pirtle & Martines), Melanie Muhlstock (Parker Waichman), David A. Neiman (Romanucci & Blandin), Michelle Parfitt (Ashcraft & Gerel), Syreeta Poindexter (Babin Law), EricaRae Garcia (Weitz & Luxenberg), Steve Rotman (Hausfeld), Richard W. Schulte (Wright & Schulte), Ashlie Case Sletvold (Peiffer Wolf Carr Kane Conway & Wise), Chris Stewart (Stewart Miller Simmons), Aimee Wagstaff (Wagstaff Law Firm), and Mikal Watts (Watts Guerra).

The leadership composition tells operators three things. First, this is a docket led by firms with deep mass tort balance sheets - Motley Rice, Beasley Allen, Lieff Cabraser, Aylstock Witkin, Wagstaff & Cartmell, and Watts Guerra collectively hold hundreds of millions in advanced case costs across the federal MDL system. They have the capital to fund intake at scale and the operational discipline to reject 60-to-75 percent of unverified inventory without flinching. Second, the inclusion of Morgan & Morgan and The Cochran Firm signals that high-volume regional and national-brand firms are buying alongside the specialist tier - which broadens the demand curve and supports defensible CPL through bellwether trials. Third, the absence of certain notable plaintiff brands suggests parallel state-court pipelines and direct-action pools outside the MDL, which is consistent with the industry-wide pattern of routing select inventory into more favorable forums.

For brokers, the practical move is to maintain a current intake-disposition file at three or four PSC firms across different tiers and run inventory against the file’s documented rejection patterns. The published agency rate cards undervalue the inventory that hits Co-Lead and PEC firms’ qualification criteria and overvalue inventory that does not.

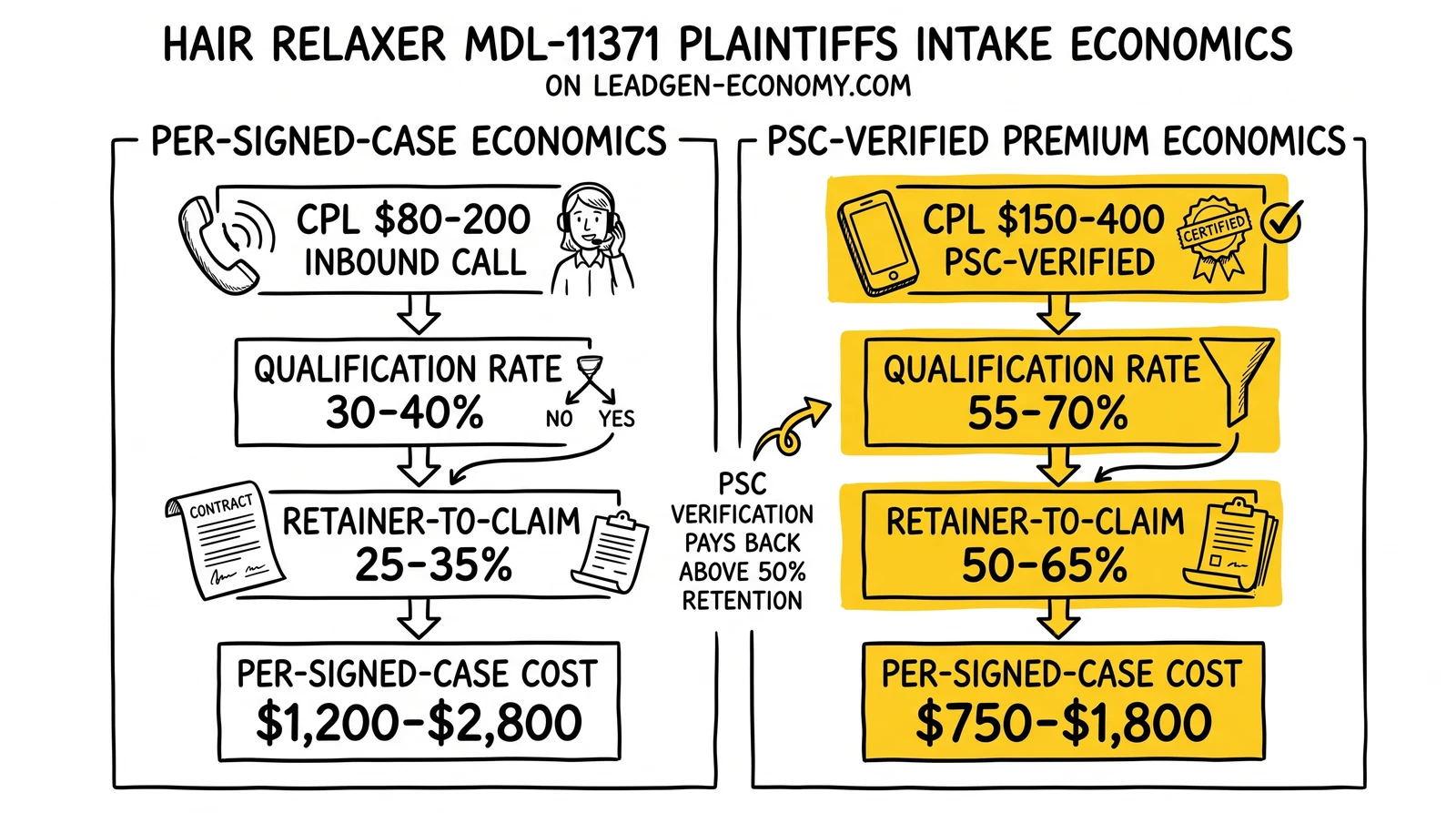

CPL Math: The Verified Premium That Defines the Margin

Raw qualified hair relaxer leads run roughly $50 to $120 per record on Facebook paid traffic, the dominant intake channel in mid-2026. That published range, anchored on agency rate-card disclosures from Mass Tort Ad Agency’s May 2026 update and corroborated against private rate decks from several PSC firms, prices a Facebook click-to-form lead that has cleared a 36-question intake script and a TrustedForm or Jornaya consent capture. Verified inventory - leads carrying product-use affidavits, dated diagnosis documentation, salon-employment records where applicable, and an SOL-eligibility check - trades at roughly 2 to 2.5x raw pricing. Call it $225 to $325 raw and $550 to $750 verified at the June 2026 market clearing price.

The April-to-June 2026 bellwether-selection window pushed verified pricing into the upper end of the range as PSC firms expanded intake budgets ahead of expert exchange. The August 3, 2026 defense expert disclosure is the next clean pricing event. Operators should expect CPL compression of 15 to 25 percent in the 60 days that follow as plaintiff firms reassess the verified intake stack against tighter trial timelines. The full bellwether-calendar pricing framework applies here in textbook form: docket events reprice inventory faster than media-buying spreadsheets can model.

The verified premium math runs through three variables. Conversion rate: 5 to 8 percent on unverified Facebook traffic, 18 to 25 percent on inventory that arrives pre-verified. The 4x conversion lift on roughly a 2.5x price translates into a verified-tier per-signed-case acquisition cost roughly 40 percent below the unverified tier, before accounting for plaintiff-firm intake labor. Expected per-case settlement value: $150,000 to $750,000 in the public range for cancer cases, with most plaintiff-side models running internal midpoints near $250,000 to $350,000 after haircutting for SOL exposure, comparative-fault risk in the Sister Study cohort’s confounders, and the documented Revlon insurance coverage limit constraints. Attorney fee structure: 40 percent contingent on post-filing cases, 33⅓ percent if the case settles pre-filing - and for a docket this size, pre-filing settlement is essentially impossible at the case level outside a global resolution framework.

Plug those into the settlement-multiple model honestly. A $300,000 expected settlement at 40 percent fees and 20 percent verified-tier conversion supports $24,000 in maximum sustainable acquisition cost per signed case before the operator’s cost stack. Net of $250 per record of intake labor, verification, and capital cost across roughly 5 records per signed case, the model supports verified-tier CPL up to roughly $4,500. Verified inventory clearing at $550 to $750 leaves a margin structure that explains why specialist agencies expanded hair relaxer verification operations through 2025 and 2026 while the lead-volume side of the market consolidated.

The math breaks where it always breaks. Conversion rate is the variable operators most often inflate. Operators publishing 8 percent unverified conversion are typically reporting the rate on the cleanest tier of their inventory; the blended rate runs closer to 5 to 6 percent across the full delivery. Cost stack is the variable operators most often understate. Intake-labor cost at $25 to $35 per hour for trained mass tort intake specialists, verification at $50 to $150 per case, and capital cost on the 60-to-90-day inventory hold between intake and retainer signing add $200 to $350 per signed case beyond the headline CPL. And expected per-case settlement is the variable most exposed to the next Daubert ruling. A defense Daubert win that excludes the Sister Study or the Chang general-causation expert testimony could compress expected settlement by 30 to 50 percent inside a quarter. The June 30 plaintiffs’ expert disclosure and August 3 defense disclosure are the pricing inputs that will tell operators whether the current verified-tier pricing holds through fall 2026.

The Bellwether Schedule and What Comes Next

The procedural calendar through 2027 is the single most reliable forecasting input for hair relaxer CPL. Case-specific fact discovery closed February 16, 2026, having been extended from the original 2025 cutoff to accommodate the discovery pool’s growth. Judge Rowland ruled on bellwether case selection March 2, 2026 and named 10 initial bellwether cases on April 8, 2026 - an expansion from the originally planned 3-case selection that signaled the court’s intent to widen the evidentiary base before the first verdicts land. The bellwether pool size grew to 32 cases for discovery purposes, with the trial-track 10 drawn from that pool through a combined plaintiff-defendant selection process.

General causation Daubert motions were due April 1, 2026. Plaintiffs’ expert disclosures landed June 30, 2026. Defense expert disclosures are due August 3, 2026. Plaintiffs’ rebuttal expert disclosures follow in early Q4. Daubert oral argument is scheduled for late Q4 2026, with the court’s general-causation ruling expected in Q1 2027. First bellwether trials are projected for mid-2027, with the standard MDL pattern of two-to-four trials in the first wave before settlement discussions structure around the verdict band.

Special Settlement Master Ellen K. Reisman was appointed in April 2025. Reisman previously served in similar capacities in the J&J talc, 3M Combat Arms, and DePuy hip-implant MDLs. The appointment is a routine procedural staging move - not a signal that a global resolution framework is imminent. The historical lag between Special Master appointment and announced settlement framework in dockets of this size runs 18 to 36 months. Operators reading the Reisman appointment as a near-term settlement catalyst typically misprice intake by assuming a 2026 or early 2027 resolution that the bellwether calendar makes effectively impossible.

The 2026-to-2027 calendar implies four pricing windows operators should map against intake commitments. Window one, June through August 2026: verified CPL holds at the upper bound of the $550-to-$750 range through expert exchange, with compression risk on adverse Daubert filings. Window two, October 2026 through January 2027: Daubert ruling-driven repricing, with 15 to 35 percent volatility in either direction depending on the court’s general-causation order. Window three, Q2 to Q3 2027: bellwether trial-driven repricing, with the first verdict band tightening the expected-settlement variable and triggering plaintiff-firm intake-budget recalibration within 60 to 90 days. Window four, late 2027 through 2028: post-bellwether settlement-framework discussions with the Special Master, during which intake demand typically spikes briefly and then compresses sharply as plaintiff firms close inventory pipelines ahead of any global resolution.

Operators carrying inventory into Window three should pressure-test verified-tier pricing against the November 2022 post-publication run-up in CPL, the August 2025 post-Marston-scintigraphy reset in Ozempic, and the February 2026 post-Bayer-class-settlement repricing in Roundup. The pattern across each of those events is consistent: a 60-day price-discovery window, a 30 to 60 percent move in CPL, and a 90-day stabilization phase. Hair relaxer operators who built 2026 intake budgets on a smooth pricing curve through bellwether verdicts will discover the same volatility every other major mass tort has surfaced.

Channel Mix, Compliance, and Verification Operations

The dominant intake channel for hair relaxer leads in 2026 is Facebook paid traffic. The audience-targeting logic is mechanical: women ages 30 to 65, layered against geographic targeting in metro markets with concentrated Black demographic populations, with interest-and-behavior overlays for chemical-relaxer brand affinity. Lookalike audiences anchored on prior signed-retainer pools at PSC firms outperform cold demographic targeting by 30 to 50 percent in initial Facebook A/B tests, which is why the largest PSC firms guard their conversion-cohort data as a competitive asset.

Channel diversification beyond Facebook is shallower than it should be. Connected-TV inventory remains underbought relative to comparable mass torts - the audience overlap with daytime broadcast is favorable, and PSC firms running both channels report meaningful incrementality. Search inventory is small but high-converting on long-tail diagnosis-plus-product queries. Direct-response radio sustained the early-docket intake ramp in 2023 to 2024 and remains a defensible channel in Southern and Midwestern markets, though Facebook absorbed most of the budget shift by mid-2025.

Compliance overhead has tightened materially. TCPA exposure on hair relaxer intake is structurally lower than in many mass torts because most intake runs through form submission with consent capture rather than outbound dialing, but the TrustedForm or Jornaya session-replay record is now table stakes for any inventory the PSC firms will buy. The named PSC firms vary in their tolerance for consent-capture gaps; the larger firms reject inventory without certified session replays at the qualification gate. California-targeted creative now sits under SB 37 disclosure requirements that took effect January 1, 2026, which has pushed California-eligible CPL roughly 10 to 20 percent above the national blend. Operators routing California traffic should expect to maintain a separate funnel with explicit attorney-involvement and fee-structure disclosures at form submission.

Verification operations on hair relaxer inventory remain less mature than the AFFF or Ozempic markets but are professionalizing. The verification stack runs through three documents: a product-use affidavit (often executed via DocuSign in the intake flow), a dated diagnosis-record request authorization, and where applicable, a salon-employment record request for occupational-exposure claims. The affidavit-and-authorization combination clears most PSC firm qualification gates and supports the 18-to-25 percent verified-tier conversion rate. Adding a confirmed diagnosis record before delivery - rather than an authorization to obtain one - is what moves inventory into the upper bound of the verified pricing range and pushes conversion past 25 percent. Operators have generally not moved to that fully-verified tier because the additional 30-to-60-day inventory hold compresses cash-on-cash returns enough to make the headline price gain unattractive, even when the per-signed-case math works.

The intake-disposition feedback loop is the discipline that separates durable operators from the rest. The PSC firms running mature intake report rejection-reason data to their best vendors on 30-day cohorts, allowing the vendor to retune targeting, creative, and intake scripts against actual disposition patterns rather than presumed ones. Brokers that resist sharing disposition data with operators - or operators that resist sharing it with the agencies that run their traffic - are pricing from information asymmetry rather than optimization. The vendor evaluation framework from the bellwether-calendar article applies here in full, with the hair-relaxer-specific overlay focusing on Sister Study documentation depth and SOL screening rigor.

What Operators Should Do Through Year-End 2026

The next 180 days are the cleanest planning window the docket has offered since fact discovery closed. First 60 days, through August defense expert exchange: hold verified-tier intake budgets at the upper bound of current spend and prioritize cohorts that document product-use frequency above the Sister Study threshold with dated diagnosis records. Avoid scaling raw-tier intake into a market that the August disclosure is likely to compress. Second 60 days, through October Daubert briefing close: redirect 20 to 30 percent of verified-tier budget into SOL-screened inventory in states with discovery-rule tolling that extends qualifying-diagnosis windows past the Sister Study publication date. The legal durability premium on those cohorts is the most underbought margin in the docket. Final 60 days through year-end: rebuild intake forecasts with explicit scenario branches on the Daubert ruling - one branch assuming admission and 25 percent expected-settlement uplift, one assuming partial exclusion and flat pricing, one assuming exclusion of any major Sister Study-anchored expert and a 30 to 50 percent expected-settlement compression.

Sell-side operators should audit retainer-to-claim ratios against actual PSC firm 30-day cohort dispositions, not aggregated published rate-card claims. Operators that cannot defend conversion claims against named-firm disposition data should be repriced down at the next contract renewal. Buy-side firms should require TrustedForm or Jornaya certified records on a 100-lead sample, audit verification-document samples on a representative case sample, and require references from at least two PSC-tier firms with active retainer pipelines before committing to volume contracts on unfamiliar vendors.

The single largest forecasting risk through the bellwether period is overconfidence in the $150,000-to-$750,000 per-case projection. The range was assembled from analog-docket precedents in advance of the docket’s own evidentiary record. Operators sizing intake CPL against the midpoint of the range without haircutting for the pre-bellwether information deficit are building retainer-to-claim ratio models on a settlement number that has not yet been priced by the only mechanism that prices mass tort settlements credibly - jury verdicts. The 30-to-40 percent haircut against the public midpoint is the defensible operating posture until at least three bellwether verdicts are on the board.

The intake market for hair relaxer plaintiffs will tighten through 2027. The combination of declining new-case yield as the qualifying-condition pool exhausts, increasing PSC-firm selectivity as bellwether picks generate case-specific lessons, and the regulatory overhead of SB 37 and adjacent state lead-gen statutes will compress operator margins faster than the published rate cards reflect. Operators that built the market through 2024 to 2025 will retain the verification operations, the disposition feedback loops, and the PSC-firm relationships that defend through the cycle. Late entrants pricing off published Facebook CPL without operating that infrastructure will discover the same lesson the post-Marston Ozempic and post-vacatur AFFF markets taught - the mass tort intake market does not reward operators who price off headline numbers without owning the qualification stack.

Key Takeaways

- MDL 3060 holds 11,371 pending plaintiffs as of June 2026, with roughly 15,000 cases filed during the calendar year and the docket now the fourth-largest active MDL in the federal system - intake demand is at its peak and CPL pricing is entering a procedural-event-driven repricing cycle.

- The Sister Study’s 4.05 percent uterine cancer incidence for frequent users versus 1.64 percent for never-users is the general-causation anchor that defines screening logic, and every signable lead must document product-use frequency, duration, age at first exposure, brand, and SOL-eligible diagnosis date.

- Co-Lead Counsel are Crump, Fitzpatrick (Motley Rice), London (Douglas & London), and Debrosse Zimmermann (DiCello Levitt); the PEC and PSC include Aylstock Witkin, Wagstaff & Cartmell, Watts Guerra, Beasley Allen, Lieff Cabraser, and Morgan & Morgan among the named seats - operators selling without a current view of which firm is the buyer are running blind.

- Raw qualified Facebook leads cleared $50 to $120 in mid-2026; verified inventory with documented exposure, dated diagnosis, and SOL screening cleared $225 to $325 raw and $550 to $750 verified - the 2-to-2.5x verified premium is the cleanest defensible margin structure in the docket.

- Verified-tier conversion (18 to 25 percent) at roughly 4x unverified-tier conversion (5 to 8 percent) on a 2.5x price produces a per-signed-case acquisition advantage near 40 percent before PSC firm intake labor - the verified tier is the only sustainable margin position for late-entry operators.

- Bellwether selection landed April 8, 2026 (10 initial cases from a 32-case discovery pool); plaintiff expert disclosures June 30, defense disclosures August 3, Daubert ruling expected Q1 2027, first trials mid-2027 - the August expert exchange is the next clean pricing event.

- Special Settlement Master Ellen Reisman was appointed April 2025; the typical 18-to-36-month lag between appointment and announced framework rules out near-term settlement-driven CPL compression, and operators pricing for a 2026 or early 2027 resolution are mispricing inventory.

- Defendants L’Oreal (Dark & Lovely, Mizani, Optimum, SoftSheen-Carson), Revlon (Creme of Nature, Realistic), Godrej, Strength of Nature, and Namaste anchor settlement projection through L’Oreal’s $225 billion-plus market capitalization and Revlon’s preserved insurance coverage from the Chapter 11 carve-out.

- The public $150,000-to-$750,000 cancer-case settlement range is pre-bellwether and pre-Daubert; defensible operating models haircut the midpoint 30 to 40 percent until three bellwether verdicts are on the board.

- The 90-day playbook: hold verified-tier intake through August expert exchange, redirect 20 to 30 percent of budget into SOL-screened inventory in discovery-rule states, rebuild forecasts with explicit Daubert scenario branches, and audit retainer-to-claim ratios against actual PSC firm 30-day cohort disposition data rather than published rate-card claims.

Sources

- Judicial Panel on Multidistrict Litigation - MDL Statistics Report

- JPML Transfer Order MDL 3060 (Feb 6, 2023)

- Chang et al., Use of Straighteners and Other Hair Products and Incident Uterine Cancer, JNCI (Oct 17, 2022)

- NIH News Release - Hair Straightening Chemicals Associated With Higher Uterine Cancer Risk

- Northern District of Illinois - MDL 3060 Case Management Portal

- MDL 3060 Leadership Order (PSC Appointments, March 3, 2023)

- Verus LLC - MDL 3060 Leadership Team Appointments

- Lawsuit Information Center - Hair Relaxer Lawsuit June 2026 Update

- Miller & Zois - Hair Relaxer Lawsuit May 2026 Update

- Mass Tort Ad Agency - Hair Relaxer Mass Tort Opportunity (May 2026)

- Wagstaff & Cartmell - In re Hair Relaxer MDL Practice Page