The compliance spine of U.S. lead generation has been prior express written consent since the Telephone Consumer Protection Act of 1991. In the first four months of 2026, four institutions – MetaComp, Sumsub, Mastercard with Google, and NIST – independently shipped the components of a parallel identity layer called Know Your Agent. KYA does not replace TCPA consent. It sits above it, answering a question consent cannot: who is the agent submitting the form, and who delegated authority. KYA is the forward-looking identity framework for agent-originated submissions; the multistate AG civil investigative demand playbook covered separately is the present-tense 72-hour enforcement reality operators are already absorbing. The consent-and-scope layer – the cryptographically signed AP2 Mandate that scopes what the agent is authorized to do – is covered in a separate companion analysis. Together, the two layers form the agentic-commerce compliance stack lead buyers will demand by Q4 2026.

A Framework Born in 120 Days

On January 29, 2026, Sumsub announced AI Agent Verification – described as a first-of-its-kind binding of AI-driven automation to a real, verified human identity, sitting inside what the company called its Know Your Agent framework. On February 4, Trulioo and PayOS published a white paper introducing the Digital Agent Passport. On February 5, the National Institute of Standards and Technology released a concept paper titled Accelerating the Adoption of Software and AI Agent Identity and Authorization, with public comment open through April 2. On March 5, Mastercard and Google launched Verifiable Intent, an open-standard cryptographic audit trail for AI-agent purchases, with reference implementation hosted at verifiableintent.dev. On April 22, at Money20/20 Asia in Bangkok, Singapore-licensed financial institution MetaComp Pte. Ltd. launched the StableX Know Your Agent Framework, claiming the first such framework from a regulated FI.

Four institutions. One acronym. Roughly twelve weeks. The component vendors do not all agree on the details, but they agree on the shape: an agent has a verified identity, that identity is bound to a human principal, the principal’s instruction is captured in a tamper-resistant record, and the agent’s behavior is monitored against the scope of that instruction. The Sumsub Identity Fraud Report 2025-2026 sits underneath the entire effort as the threat-model justification – a documented 180 percent year-on-year increase in sophisticated, multi-step coordinated attacks during 2025 and a finding that deepfakes accounted for 11 percent of first-party fraud schemes.

For lead operators, the story arrives downstream of payments and identity verification but matters earlier. The form-fill funnel is the canonical lead-generation event, and the form-fill funnel in 2026 is increasingly receiving submissions from agents acting under a consumer’s delegated mandate rather than from the consumer typing into a browser. Mastercard’s Verifiable Intent spec is built around payments, but the underlying architecture – identity, intent, action, audit trail – is the architecture of any agent-mediated commercial interaction, including the moment a lead enters a buyer’s CRM.

This analysis treats KYA specifically as the identity-and-authority layer of the agentic-commerce compliance stack: it answers who the agent is, who the human principal is, and what cryptographic chain links them. The consent-and-scope layer – what that authority is permitted to do, scoped to a specific seller and outcome through the AP2 Mandate – is treated in the companion piece on AP2 Mandates and Mastercard Verifiable Intent. Operators will need both layers in production by Q4 2026; this article walks through what the identity-layer substrate consists of, what it asks operators to verify, and what the consequences are for funnels that continue to operate on a consent-only assumption without the identity-binding artifacts that make the consent itself meaningful in an agent-mediated submission.

What KYA Actually Verifies – Three Dimensions Most Operators Are Missing

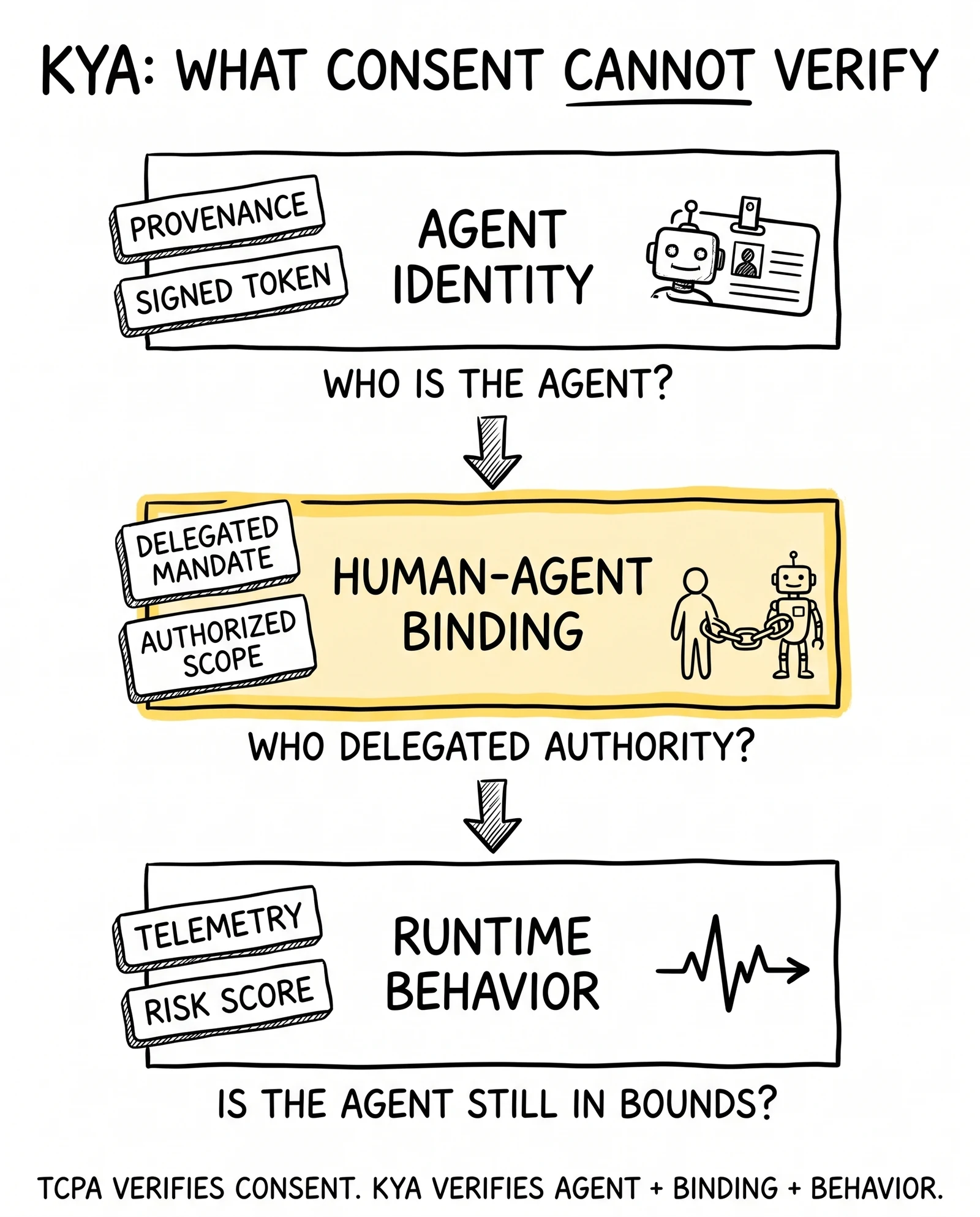

The KYA acronym borrows from KYC (Know Your Customer), and the borrowing creates a misleading mental model. KYC verifies one entity: the human customer. KYA verifies three: the agent, the human principal, and the chain of authority connecting them. Operators who treat KYA as “KYC for bots” miss two of the three layers and build infrastructure that buyers will reject in onboarding review.

Dimension one: agent identity and provenance

The first verification layer is the agent itself. Trulioo and PayOS describe this as provenance in the Digital Agent Passport framework – a tamper-proof token that identifies which model, which developer, and which deployment the agent originated from. Skyfire’s KYAPay implementation expresses the same concept as a signed JSON Web Token built on existing OAuth2, JWKS, and OpenID Connect infrastructure, with the IETF draft-skyfire-kyapayprofile-01 specification describing the token contents. NIST’s February 5 concept paper concludes that adaptation of existing standards – OAuth, SPIFFE, OpenID Connect – is preferred over invention; the agent identity layer should be expressible in token formats that today’s identity providers can already issue and verify.

For a lead generator, the practical implication is that an inbound form submission from an agent should carry a verifiable identity claim. The submission either includes a signed token that resolves to a recognized agent registry entry, or it does not. If it does, the operator can inspect the agent’s provenance – what model, what developer, what deployment – and route the lead accordingly. If it does not, the submission falls into a “non-attributable agent” bucket that buyers will price below human-originated leads and below agent-originated leads with verifiable identity. The two-tier inventory split is the immediate revenue consequence of the agent identity dimension.

Dimension two: human binding and the delegated mandate

The second verification layer is what Sumsub calls agent-to-human binding: the cryptographic record linking the agent to a verified human principal who has authorized the agent’s activity. In the Mastercard Verifiable Intent specification, the binding is expressed through three linked artifacts – the cardholder’s authentication of the agent, the cardholder’s specific instructions to the agent, and the agent’s interaction with the merchant – held together in a privacy-preserving record using Selective Disclosure techniques drawn from the FIDO Alliance, EMVCo, IETF, and W3C standards. Google’s Agent Payments Protocol describes the same binding through its AP2 mandate object, which records the principal’s instructions and the chain of authority under which the agent acts.

The lead-generation analog is direct. A consumer who instructs an agent to “find me three home insurance quotes within the next forty-eight hours” creates a delegated mandate. The agent’s subsequent submission of a lead form to a home insurance aggregator is an action under that mandate. The lead operator needs to verify two things about that action: that the underlying mandate exists and is fresh, and that the mandate’s scope authorizes the specific submission being made. A mandate scoped to “home insurance quotes” does not authorize the operator’s downstream sale of the lead to an auto insurance buyer or a solar buyer. The mandate is not consent in the TCPA sense – it is a narrower authorization tied to a specific commercial intent – and operators who treat it as a consent equivalent will misfire on both compliance and conversion.

Dimension three: behavioral telemetry and continuous risk scoring

The third verification layer is the runtime behavior of the agent, not just its identity. The Trulioo/PayOS Digital Agent Passport names two of its five checkpoints in this category: real-time behavior telemetry and continuous risk scoring. Sumsub’s AI Agent Verification adds device intelligence, mule-network signal analysis, and liveness detection that can be invoked when risk thresholds are crossed. The MetaComp StableX Framework names “behavior monitoring and risk intelligence” as one of its four pillars alongside agent identity, authority and permission control, and ecosystem governance.

The point is not that an agent identity, once issued, is permanent. The point is that the verification is continuous: an agent that begins acting outside its mandated scope, exhibits patterns consistent with credential stuffing, or shows signs of compromise should have its operating privileges curtailed in real time. For lead operators, the practical implication is a feedback loop with the verification provider – agent submissions are evaluated not only at the moment of capture but against the agent’s running behavioral profile, and operators receive risk signals that inform pricing and routing.

The composite picture is a verification stack with three runtime questions: who is this agent (identity), under whose authority and for what purpose (binding and mandate), and is the agent currently behaving consistently with that authority (telemetry). All three must be answered to deliver a lead the buyer will accept under post-August 2026 EU AI Act high-risk system requirements. Answering one or two is not enough – and the consent capture infrastructure most lead generators run today answers none of them.

Why Consent-Only Compliance Will Underperform Through 2027

Three responses to the KYA shift are visible in early industry chatter. Each is a plausible reading of the situation, and each will produce worse outcomes than its proponents expect. The reasons are worth being explicit about, because the argument structure repeats across other compliance transitions and the same patterns will surface elsewhere.

The “consent is consent” posture

The first response treats KYA as a payments-and-identity story that does not affect lead generation. The argument runs that TCPA prior express written consent, the FCC’s vacated one-to-one consent rule, and existing state-level consent regimes are sufficient to govern agent-originated lead capture. If the agent collected the consumer’s consent, the consent flows through to the lead buyer the same way it does for a human form-fill. KYA is for fintech and merchants; the lead operator’s compliance stack does not need to change.

The argument was reasonable through 2024 and is wrong by April 2026. Three independent forcing functions have already begun to break the equivalence. EU AI Act high-risk system requirements taking full effect on August 2, 2026 impose technical documentation, transparency, human oversight, and post-market monitoring obligations on AI systems whose use falls under the regulation’s high-risk categories – and AI agents acting in commercial transactions on behalf of consumers will, in many configurations, fall within those categories. Compliance with high-risk requirements is not satisfied by a TCPA-compliant consent capture. Mastercard’s Verifiable Intent specification and Google’s AP2 mandate format establish a documentary expectation that an agent transaction carries a tamper-resistant record of intent – an expectation that lead buyers ingesting agent-originated leads will adopt as an onboarding prerequisite once their payments-side compliance teams notice the asymmetry. NIST’s concept paper signals federal direction toward agent-identity standards; whatever the final guidance contains, the trajectory is incompatible with a “consent is consent” posture.

The operator who insists that consent capture is sufficient will be technically correct on TCPA grounds, structurally underprepared on EU AI Act grounds, and commercially disadvantaged when buyers begin tiering inventory by KYA verification status. The composite consequence is margin compression starting in Q3 2026 and accelerating through 2027.

The “wait for the regulator” posture

The second response acknowledges that KYA is real but argues that the prudent move is to wait for federal regulatory direction before changing compliance infrastructure. NIST has only published a concept paper. The EU AI Act’s August 2 enforcement is months away. The FCC has not spoken on agent-mediated lead capture. The wait-and-see operator continues current practice and plans to react when the regulators speak.

The flaw in this posture is that the regulators are not going to speak first in a recognizable sense. NIST’s February 5 concept paper explicitly frames its work as building on industry-developed standards – OAuth, SPIFFE, OpenID Connect, and the IETF and W3C work that Skyfire’s KYAPay protocol references. The federal direction is to ratify and adapt what industry is already building, not to issue a top-down standard the industry must implement. The EU AI Act’s high-risk requirements set obligations but do not prescribe the technical form of compliance; the form is being defined by Mastercard, Sumsub, Trulioo, MetaComp, and the standards bodies their work draws from. By the time regulators speak in a way that satisfies the wait-and-see operator, the industry will already have settled on a default verification stack, and the wait-and-see operator will have a six-to-twelve-month catchup project rather than a parallel build with the early movers.

The “operator-passive credential” posture

The third response goes the other direction. It treats KYA as a bilateral obligation – the agent must arrive at the operator’s form with KYA credentials in hand, and the operator does not need to do verification work because the agent is delegated that task. The operator’s role is to detect the credential, accept the lead if present, and reject the lead if absent.

The argument misreads what KYA is. KYA is not a credential the agent presents and the operator passively accepts. It is a verification stack the operator must run, with the agent’s submitted identity claim as one input among several. The Trulioo/PayOS framework names continuous risk scoring as a checkpoint specifically because static credential checks are insufficient – an agent identity issued in good faith on Monday can be compromised by Wednesday. The Sumsub framework explicitly invokes targeted liveness checks when risk indicators warrant. The MetaComp framework lists behavior monitoring as a pillar coordinate with identity. An operator who treats the verification as the agent’s responsibility ends up with a checkbox that satisfies no one – the lead buyer’s onboarding review will examine the operator’s verification logs, and a pure pass-through claim will fail the audit. The cost of building the verification stack is not avoided by the pass-through approach; it is deferred to a moment when the buyer-onboarding clock is running, which is a worse moment to build.

The common pattern across the three approaches is the same: each underestimates how much of the verification work falls on the lead operator rather than on the agent or the regulator, and each treats KYA as a discrete event rather than a continuous runtime obligation. The funnels that will perform well in 2027 are funnels whose operators read the early 2026 announcements as a build list rather than as a wait list or a delegation list.

The Strategic Reframe: Three Principles for the Agent-Originated Lead

The right starting point for KYA implementation is a different premise about what a lead is. A lead in 2024 was a record of a consumer’s consent to be contacted, captured at a point in time, with the consent text retained for compliance purposes. A lead in 2027 will be a record of three coordinated artifacts: the agent that submitted it, the human principal under whose mandate the agent acted, and the runtime behavioral context at the moment of submission. The shift is not from one compliance layer to another. It is from a single-artifact lead record to a multi-artifact lead record. Three principles flow from that premise.

Principle one: capture the mandate, not just the consent

The legacy lead form captures the consumer’s consent to be contacted. The KYA-aware lead form captures the mandate under which the agent is acting on the consumer’s behalf, which includes the consent but also the scope, the duration, and the chain of authority. A consumer who instructs an agent to comparison-shop home insurance creates a mandate scoped to that purpose; the operator’s form should capture the mandate identifier, the principal’s binding to it, the scope, and the expiration. The capture mechanism is technical – the form ingests a signed mandate token rather than a checkbox – and the operator’s consent retention policies need to extend to mandate retention with the same chain-of-custody discipline.

What this requires operationally is a form layer that can ingest mandate tokens from multiple agent ecosystems – Mastercard Agent Pay’s intent APIs, Google’s AP2 mandate format, Skyfire’s KYAPay tokens, the MetaComp AgentX ecosystem accessible through Model Context Protocol, and others. The format work is substantial because the ecosystems have not converged on a single token structure. The operator who completes a multi-format mandate ingestion layer in 2026 will run a funnel that accepts agent traffic from any major ecosystem; the operator who picks one ecosystem and discovers in 2027 that the consumer’s preferred agent is on a different ecosystem will rebuild.

Principle two: tier inventory by verification depth

The legacy buyer waterfall priced leads on a relatively flat verification base – every lead carried a similar consent record, and tiering was driven by source quality, exclusivity, and buyer-specific filters. The KYA-aware waterfall has a more complex base. Some leads will carry full three-dimensional verification: agent identity, mandate binding, behavioral telemetry. Others will carry partial verification – identity and mandate, but no telemetry; or identity only, with no mandate binding. Some will carry no agent verification at all because they were submitted by humans through traditional forms. A handful will carry suspicious or stale identity claims that the verification stack flags as unreliable.

Each verification depth has a different value to a lead buyer. A buyer running auto-dial outbound under TCPA constraints will value mandate-bound leads over consent-only leads because the mandate provides a stronger documentary trail under regulatory scrutiny. A buyer routing leads to a carrier-direct insurance program will value telemetry-enriched leads because the runtime context informs the conversion-likelihood model. The waterfall tiering should reflect the verification depth, with higher-tier exclusive buyers receiving fully-verified leads and lower-tier shared buckets receiving leads with shallower verification. The operator who runs a verification-flat waterfall will systematically misprice inventory once buyers start asking for verification metadata in onboarding review, which is a Q3 2026 conversation in payments-adjacent verticals and a Q1 2027 conversation in the rest of the lead-generation market.

Principle three: log every verification step against the agent registry

The third principle is the one most operators get wrong on the first build. KYA is not a verification event; it is a verification log. Every check the operator runs against the agent’s identity, mandate, and behavior should be retained with cryptographic chain of custody, indexed against the agent’s registry identifier, and made available for downstream audit. The Trulioo/PayOS framework names continuous risk scoring as a checkpoint precisely because static checks are insufficient; the operator’s compliance role is to retain the running log, not just the most recent score.

What this requires is a logging substrate that the operator’s existing consent retention infrastructure does not currently provide. Consent retention typically captures the consent text, the timestamp, the IP address, and the form session – a relatively shallow record optimized for TCPA defense. KYA logging adds the agent identity token, the mandate token, the verification-provider response payloads, the behavioral telemetry stream, and the running risk score. The data volume is materially higher, the retention horizon is longer, and the access-control requirements are stricter because the data includes information about agent behavior that is itself sensitive. Operators planning the build should size storage and compliance-review budgets accordingly; the KYA log will be larger than the consent log by approximately one order of magnitude per lead in early benchmarks, though the benchmark will move as compression and aggregation techniques mature.

Evidence: How MetaComp, Sumsub, Mastercard, and NIST Each Pushed the Stack Forward

The case for treating KYA as a compliance substrate rather than a vendor pitch rests on the convergence of independent institutional moves over the first four months of 2026. Five of those moves merit detailed examination.

MetaComp StableX: a regulated FI implementation

MetaComp’s April 22 launch matters because of who launched it. MetaComp Pte. Ltd. is a licensed financial institution in Singapore, and its regulatory status puts the StableX KYA Framework into a different category than vendor-issued frameworks. The framework is organized around four pillars: agent identity and registration; authority and permission control; behavior monitoring and risk intelligence; and ecosystem and interaction governance. It was developed in alignment with the Singapore Infocomm Media Development Authority’s Model AI Governance Framework for Agentic AI, which IMDA published in January 2026 as the first cross-sector governance framework for AI agents from a national regulator.

MetaComp announced the same day an expansion of its AgentX agentic financial services Skill ecosystem, accessible across Claude, Claude Code, and other Model Context Protocol-compatible AI platforms. The framework is paired with an MCP-accessible commercial agent ecosystem that demonstrates it in production. For lead operators in financial-services verticals, MetaComp’s approach is the near-term reference architecture for what regulated-FI-grade KYA looks like, and the buyer side of those verticals will likely look something like the MetaComp model within twelve to eighteen months.

Sumsub AI Agent Verification: the threat model becomes operational

Sumsub’s January 29 announcement puts a measurable threat model behind the verification stack. The Sumsub Identity Fraud Report 2025-2026, released in late November 2025, documented a 180 percent year-on-year increase in sophisticated multi-step coordinated attacks during 2025 and a finding that deepfakes accounted for 11 percent of first-party fraud schemes. Synthetic identity document fraud surged 300 percent in the U.S. across 2025. The aggregate fraud rate worldwide moved from 2.6 percent in 2024 to 2.2 percent in 2025 – a modest decline in volume that masks a sharp shift toward higher-sophistication attacks.

These numbers are the threat-model justification for the entire KYA effort. Consent-based verification, which proves a human authorized contact at a point in time, does not address the 2025-era attack surface in which the entity submitting the consent claim may itself be an AI agent operating outside the scope of any legitimate human authorization. Sumsub’s AI Agent Verification responds by binding agent activity to verified human identity at runtime. For lead operators in verticals already exposed to identity-fraud attack patterns – credit and lending, healthcare, insurance – buyers will adopt agent-binding verification on a faster timeline than buyers in lower-risk verticals.

Mastercard Verifiable Intent: the audit-trail standard

Mastercard’s March 5 announcement commits a card network to an open standard. Verifiable Intent links three artifacts – cardholder authentication of the AI agent, the cardholder’s specific instructions, and the agent’s interaction with the merchant – into a tamper-resistant record using FIDO Alliance, EMVCo, IETF, and W3C standards, with privacy preserved through Selective Disclosure. Mastercard open-sourced the specification at verifiableintent.dev and on GitHub. Verifiable Intent is integrated directly into Mastercard Agent Pay’s intent APIs, operating in production payments rails as of Q2 2026.

The lead-generation relevance is indirect but determinative. The cryptographic shape of the Verifiable Intent record – identity plus instruction plus action plus signature – is the same shape any agent-mediated commercial transaction will need, including a lead form submission. Lead buyers whose businesses include card payment flows are already building infrastructure to consume Verifiable Intent records; those same buyers will, within a year, expect their lead-side suppliers to deliver records of comparable structural integrity.

NIST AI Agent Standards Initiative: the federal trajectory

NIST’s February 2026 launch confirms that federal direction will adapt rather than displace industry standards. The Center for AI Standards and Innovation’s concept paper, Accelerating the Adoption of Software and AI Agent Identity and Authorization, was open for public comment through April 2 and explicitly evaluates whether existing identity standards – OAuth, SPIFFE, OpenID Connect – can be applied to AI agents. The paper’s conclusion that adaptation is the right path tells industry that the work being done at IETF, at FIDO, at W3C, and at major identity providers is on a trajectory NIST is preparing to ratify rather than replace. For a lead operator weighing whether to invest in agent-identity infrastructure now or wait, the NIST signal cuts toward investing now: OAuth-based, JWT-based, and OpenID-Connect-based agent verification is forward-compatible with federal guidance whenever it issues.

Trulioo Digital Agent Passport and the McKinsey readiness data

Trulioo and PayOS published Know Your Agent: An Identity Framework for Trusted Agentic Commerce on February 4, introducing the Digital Agent Passport with five checkpoints: provenance, user binding, permission scope, real-time behavior telemetry, and continuous risk scoring. Trulioo subsequently partnered with Worldpay to deliver KYA capability to merchants. The white paper proposes establishing Digital Passport Authorities – analogous to certificate authorities in TLS – operated by identity providers, payment networks, or industry consortia. The five-checkpoint structure is the most operationally specific reference architecture in the KYA literature as of April 2026 and maps cleanly onto a lead operator’s required verification stack.

McKinsey’s 2026 AI Trust Maturity Survey, conducted across approximately 500 organizations between December 2025 and January 2026, reported an average responsible AI maturity score of 2.3 out of 4 in 2026, up from 2.0 in 2025. Only about one-third of organizations report maturity levels of three or higher in agentic AI governance specifically. The implication for lead operators is that buyer-side adoption will be uneven through 2026 and 2027, with the most-mature one-third of buyers asking for KYA-verified inventory ahead of the rest, and the remaining buyers catching up over the following twelve to eighteen months. The operator’s planning question is not whether KYA is a real shift; it is which buyer relationships will reach KYA-readiness first.

Implementation Reality: What a KYA-Ready Funnel Costs to Build

The strategic reframe is straightforward. The implementation is non-trivial and most lead operators have not budgeted for it.

Resource requirements

A KYA-ready funnel build has four work streams. Each is independently sized and the total is larger than typical compliance projects.

The first is mandate-token ingestion. The funnel’s form layer needs to ingest signed mandate tokens from multiple agent ecosystems – Mastercard Agent Pay intent APIs, Google AP2, Skyfire KYAPay, MetaComp AgentX via Model Context Protocol, and the additional ecosystems likely to surface across 2026. Each ecosystem exposes a different token format and resolution endpoint; the integration is a per-ecosystem build. Operators should plan for sixty to ninety engineering days per major ecosystem, with the first integration carrying additional foundational architecture cost.

The second is verification-stack integration. The operator runs the agent identity through one or more verification providers (Sumsub, Trulioo, or equivalent), receives a verification response, and incorporates the response into the lead record. The integration is API-level work and is straightforward in isolation; the complexity sits in the response normalization layer that maps each provider’s risk-scoring output into a single internal scoring schema. Plan for forty to sixty engineering days for the first provider and twenty to thirty per additional provider.

The third is the mandate-aware compliance log. The operator’s existing consent retention substrate retains consent text, timestamp, IP, and session – KYA logging adds agent identity tokens, mandate tokens, verification-provider responses, telemetry streams, and continuous risk scores. The data volume is approximately one order of magnitude larger than consent logging at current capture rates. Schema design, retention policy, and access control work is forty to eighty engineering days. Compliance counsel review of the resulting logging architecture is two to three weeks, running in parallel.

The fourth is buyer-side delivery. Lead delivery formats need to extend to carry verification metadata – agent identity reference, mandate identifier, verification status, risk score – alongside the lead’s traditional fields. Each buyer integration is a separate negotiation because the receiving CRM or routing engine needs to accept and act on the new metadata. Plan thirty to forty-five days per major buyer relationship for delivery-format negotiation and testing.

Timeline expectations

A realistic implementation timeline for a mid-sized lead operator covering one major agent ecosystem and one verification provider:

| Phase | Duration | Key Activities |

|---|---|---|

| Mandate-token ingestion | 60–90 days | First-ecosystem integration with multi-format extensibility |

| Verification provider integration | 40–60 days | API-level integration; risk-score normalization; response handling |

| Compliance log build | 40–80 days | Schema; retention; access control; cryptographic chain of custody |

| Compliance counsel review | 14–21 days | External review of logging architecture and mandate retention |

| Buyer-side delivery format | 30–45 days per buyer | Metadata extension; CRM/routing integration; onboarding documentation |

| Total elapsed time | 5–7 months | Conservative estimate for one ecosystem and one verification provider |

Source: Composite based on Mastercard Verifiable Intent reference implementation guidance, Trulioo/PayOS Digital Agent Passport white paper, and Skyfire KYAPay protocol specifications

Operators who plan to support multiple agent ecosystems or multiple verification providers should expect the total elapsed time to extend by approximately three to four months per additional ecosystem and one to two months per additional verification provider, with parallelization compressing the total only modestly because the buyer-side integration work is largely sequential.

Common obstacles

Three obstacles consistently slow KYA implementations beyond the nominal timeline. The first is buyer asymmetry. Different buyers in the operator’s relationship set will reach KYA-readiness at different times, and the operator who tries to deliver verification metadata to a buyer whose CRM cannot ingest it will end up either dropping the metadata in delivery or running parallel delivery formats. McKinsey’s two-thirds-immature finding makes this asymmetry the modal experience rather than the exception.

The second is the standards-fragmentation problem. As of April 2026, MetaComp, Sumsub, Mastercard, Google, Trulioo, Skyfire, and other ecosystem participants have not converged on a single token format, a single verification-provider response schema, or a single risk-score normalization. The convergence will happen over the next eighteen to thirty months, partly under NIST guidance, but operators building today are building against a moving target. The mitigation is to abstract the format-handling layer behind an internal canonical schema, but the abstraction itself is engineering work that single-ecosystem builds tend to skip and regret.

The third is the threat-model evolution. The Sumsub Identity Fraud Report 2025-2026 documented a 180 percent year-on-year increase in sophisticated multi-step attacks; the trajectory is not flat. Verification stacks built against the early-2026 threat model will need ongoing tuning against the late-2026 and 2027 threat models. Operators who build with a “set and forget” mindset and do not budget for verification-stack tuning will see verification quality degrade against drifting attack patterns.

The implementation is hard. The operators who complete the first KYA-ready funnel before the rest of the market catches up will run a six-to-twelve-month structural advantage in agent-originated lead inventory, with margin implications that compound across the buyer waterfall.

Future Implications: The Five-Year Trajectory of the KYA Substrate

The April 2026 announcements are the first events in a multi-year sequence. The shape of the sequence is reasonably predictable from the structure of the standards and the regulatory calendar.

In the next twelve months, the EU AI Act’s August 2, 2026 enforcement of high-risk system requirements will catalyze KYA adoption among any operator with EU-resident lead volume. Compliance reviews triggered by the August 2 date will surface KYA-readiness gaps in operators who had been treating the question as a 2027 concern. Mastercard Verifiable Intent reference implementations will move from early-adopter merchants into broader card-network use, and the resulting documentary expectations will propagate into adjacent lead-generation flows.

In the next twenty-four months, NIST will issue follow-up guidance to the February 2026 concept paper. The guidance is unlikely to displace the OAuth-and-JWT-based architecture industry has built but will likely add federal requirements around audit-trail retention, agent registry coordination, and incident reporting. The agent ecosystems – Mastercard Agent Pay, Google AP2, Skyfire KYAPay, MetaComp AgentX – will begin converging on a smaller set of token formats under industry-and-NIST pressure, reducing but not eliminating the multi-ecosystem integration burden.

In the next thirty-six months, KYA verification metadata will become a routine field on the lead record, comparable to how consent text became routine after TCPA’s prior express written consent rule took hold. Buyer waterfalls will tier inventory by KYA verification depth as a matter of course, and inventory without KYA metadata will price below verified inventory at a structural discount. The shift will not extinguish consent capture – TCPA remains the operating regime for human-originated lead capture – but it will displace consent capture from its position as the singular compliance anchor.

If the Trulioo/PayOS Digital Passport Authority concept matures into operating institutions issuing, signing, and revoking agent passports, the lead generation industry’s compliance infrastructure gains a centralized accountability point that has not existed since the FCC’s TCPA enforcement role was established. Operators who build infrastructure to interface with passport authorities now will be positioned to operate inside that institutional architecture as it forms, rather than being asked to retrofit later. The strategic implication is to design the KYA build for the world after the next standards convergence – abstracting agent ecosystem, verification provider, and logging substrate behind canonical internal schemas – rather than optimizing for the April 2026 component vendors specifically.

Key Takeaways

The Know Your Agent shift is the most consequential compliance development for lead generation since the FCC’s 2013 prior-express-written-consent rule under TCPA, and it arrived in roughly twelve weeks across MetaComp, Sumsub, Mastercard with Google, NIST, and Trulioo-with-PayOS announcements between January 29 and April 22, 2026.

KYA verifies three layers, not one: the agent’s identity and provenance, the agent’s binding to a verified human principal under a delegated mandate, and the agent’s runtime behavioral telemetry. Operators who instrument only one or two of the three will fail buyer-onboarding review under post-August 2, 2026 EU AI Act high-risk requirements.

The Sumsub Identity Fraud Report 2025-2026 documented the threat-model justification: a 180 percent year-on-year increase in sophisticated multi-step coordinated attacks during 2025 and deepfakes accounting for 11 percent of first-party fraud schemes. Synthetic identity document fraud rose 300 percent in the U.S. The aggregate attack surface is shifting from volume to sophistication, and consent-only verification does not address the new surface.

Mastercard’s March 5 Verifiable Intent specification, built on FIDO, EMVCo, IETF, and W3C standards and integrated into Agent Pay’s intent APIs, establishes the cryptographic shape – identity plus instruction plus action plus signature – that any agent-mediated commercial record will need to carry. The shape will propagate from card payments into lead form submissions on a twelve-to-eighteen-month timeline.

Three approaches will underperform: the consent-is-consent posture (technically correct on TCPA, structurally underprepared on EU AI Act), the wait-for-the-regulator posture (NIST has signaled adaptation rather than top-down standards, leaving wait-and-see operators six to twelve months behind), and the require-KYA-from-the-agent posture (treats verification as a credential rather than a runtime stack, fails buyer audit).

A KYA-ready funnel build is roughly a five-to-seven-month engineering and compliance project for a mid-sized operator covering one major agent ecosystem and one verification provider, with mandate-token ingestion, verification-stack integration, mandate-aware compliance logging, and buyer-side delivery format work as the four critical paths.

McKinsey’s 2026 AI Trust Maturity Survey of approximately 500 organizations found that only about one-third report maturity levels of three or higher in agentic AI governance, which means buyer-side KYA absorption will be uneven through 2026 and 2027, with the most-mature one-third leading the demand for KYA-verified inventory.

The five-year trajectory points to KYA verification metadata as a routine lead-record field by 2029, buyer waterfalls tiered by verification depth, the possible emergence of Digital Passport Authorities under the Trulioo/PayOS framework, and continued convergence under NIST guidance toward a smaller set of mandate token formats and verification response schemas.

For lead operators currently running consent-only compliance, the next ninety days are the planning window. The next one hundred and eighty days are the first major-ecosystem integration window. The first lead buyers asking for KYA-verified inventory in onboarding are doing so in Q3 2026; the operators arriving at those conversations with mandate-token ingestion and verification logs will capture the early margin opportunity. The operators arriving later compete for the inventory the early movers passed over.

Frequently Asked Questions

What does Know Your Agent (KYA) actually mean for lead generators?

Know Your Agent is a compliance framework for verifying the identity, authority, and runtime behavior of an AI agent acting on behalf of a human principal. For a lead generator, the practical meaning is that an inbound form submission from an agent should carry three verifiable artifacts: a signed identity token that resolves to a recognized agent registry, a mandate token binding the agent to a verified human and a specific authorized purpose, and a runtime risk signal from a verification provider. The framework was crystallized across roughly twelve weeks in early 2026 through MetaComp’s StableX Framework, Sumsub’s AI Agent Verification, Mastercard’s Verifiable Intent, NIST’s AI Agent Standards Initiative, and the Trulioo/PayOS Digital Agent Passport white paper. KYA does not replace TCPA prior express written consent for human-originated leads. It supplements consent for agent-originated leads, which are a growing share of inbound submissions in agentic-commerce-adjacent verticals.

How is KYA different from KYC, and why does the difference matter?

KYC (Know Your Customer) verifies one entity: the human customer, typically at account opening, with a static documentary check that establishes identity and permits ongoing transactions. KYA verifies three entities: the agent, the human principal under whose mandate the agent acts, and the chain of authority connecting them – and the verification is continuous rather than static. The Trulioo/PayOS Digital Agent Passport names continuous risk scoring as one of its five checkpoints because an agent identity issued in good faith on Monday can be compromised by Wednesday. Treating KYA as KYC-for-bots leads operators to instrument a one-time identity check and skip the mandate-binding and behavioral-telemetry layers, which is the configuration that fails buyer onboarding review. The KYA verification stack is a runtime obligation, not a record-keeping event.

Does KYA replace TCPA prior express written consent?

No. TCPA prior express written consent remains the operating regime for human-originated lead capture under the FCC’s vacated one-to-one consent rule and its predecessor regulations dating to 2013. KYA is a parallel framework for agent-originated lead capture, where the consumer’s authorization runs through a delegated mandate rather than a direct form submission. The two regimes coexist: a lead form should accept either a human-originated submission with TCPA-grade consent, or an agent-originated submission with a verified mandate plus the additional KYA layers. The architectural change is that the lead record schema needs to accommodate both submission paths and retain different artifacts for each. Operators who run consent-only compliance will be technically correct on TCPA grounds but structurally underprepared as agent-originated submission volume grows, particularly in EU markets after August 2, 2026 enforcement of AI Act high-risk system requirements.

What did MetaComp announce on April 22, 2026?

MetaComp Pte. Ltd., a Singapore-licensed financial institution, launched the StableX Know Your Agent Framework at Money20/20 Asia in Bangkok on April 22, 2026, and described it as the first AI agent governance framework from a regulated financial institution. The framework is organized around four pillars: agent identity and registration; authority and permission control; behavior monitoring and risk intelligence; and ecosystem and interaction governance. It was developed in alignment with Singapore’s Infocomm Media Development Authority Model AI Governance Framework for Agentic AI, published in January 2026 as the first cross-sector governance framework for AI agents from a national regulator. MetaComp simultaneously expanded its AgentX agentic financial services Skill ecosystem, accessible across Claude, Claude Code, and other Model Context Protocol-compatible AI platforms, providing a runtime substrate for the framework rather than a paper-only proposal.

What is Mastercard’s Verifiable Intent specification?

Mastercard, in collaboration with Google, announced Verifiable Intent on March 5, 2026 as an open-standard cryptographic audit trail for AI-agent purchases. Verifiable Intent links three artifacts into a tamper-resistant record: the cardholder’s authentication of the AI agent, the cardholder’s specific instructions to the agent, and the agent’s interaction with the merchant. The specification uses Selective Disclosure techniques to share only minimum-necessary transaction information across parties. It is built on widely adopted specifications from the FIDO Alliance, EMVCo, the Internet Engineering Task Force, and the World Wide Web Consortium. Mastercard open-sourced the specification and a reference implementation on GitHub and at verifiableintent.dev, and integrated Verifiable Intent into Mastercard Agent Pay’s intent APIs. The lead-generation relevance is that the cryptographic shape – identity plus instruction plus action plus signature – is the same shape any agent-mediated commercial transaction will need to produce, including agent-originated lead submissions.

What is the Sumsub AI Agent Verification framework?

Sumsub announced AI Agent Verification on January 29, 2026 as a first-of-its-kind binding of AI-driven automation to a verified human identity, sitting inside what the company called its Know Your Agent framework. The framework verifies AI agents across identity, authentication, authorization, and policy enforcement, and establishes who is behind the agent so that only legitimate agents operate within defined guardrails. The verification model centers on agent-to-human binding: linking all activity to a verified human principal and creating a clear line of accountability. The system detects when activity is automated, evaluates risk, and applies additional verification – including targeted liveness checks – when warranted. The framework builds on Sumsub’s full-cycle verification platform, which includes device intelligence, mule-network signal analysis, and liveness detection. The threat-model justification is documented in Sumsub’s Identity Fraud Report 2025-2026, which reported a 180 percent year-on-year increase in sophisticated multi-step coordinated attacks during 2025.

What did NIST publish in February 2026, and how should operators interpret the federal direction?

NIST’s Center for AI Standards and Innovation announced the AI Agent Standards Initiative in February 2026, with the goal that AI agents capable of autonomous actions can function securely on behalf of users and interoperate across the digital ecosystem. On February 5, NIST released a concept paper titled Accelerating the Adoption of Software and AI Agent Identity and Authorization, with public comment open through April 2, 2026. The paper evaluates whether existing identity standards – OAuth, SPIFFE, OpenID Connect – can be applied to AI agents, and concludes that adaptation rather than invention is needed. The federal direction is to ratify and adapt industry-developed standards rather than to issue top-down requirements. For operators deciding whether to invest in agent-identity infrastructure now or wait for federal direction, the NIST signal cuts toward investing now: builds on OAuth-based, JWT-based, and OpenID-Connect-based architectures are forward-compatible with the trajectory NIST has staked out.

When does the EU AI Act high-risk requirement take effect, and how does it interact with KYA?

August 2, 2026 marks the application date for the EU AI Act’s core framework, including comprehensive requirements for high-risk AI systems listed in Annex III – biometrics, critical infrastructure, education, employment, essential private and public services, law enforcement, migration, and administration of justice. By that date, conformity assessments must be completed, technical documentation finalized, CE marking affixed, and EU database registration completed. Article 50 transparency obligations – disclosure of AI interactions, labeling of synthetic content, deepfake identification – also become enforceable. The interaction with KYA is that AI agents acting in commercial transactions on behalf of consumers will, in many configurations, fall within Annex III high-risk categories or trigger Article 50 transparency requirements. KYA-grade verification – agent identity, mandate binding, behavioral telemetry, audit log – provides the documentary infrastructure required under post-market monitoring and incident reporting obligations. Operators with EU-resident lead volume should treat August 2, 2026 as the practical compliance deadline for their first KYA-ready integration.

What is the Digital Agent Passport, and what are its five checkpoints?

Trulioo and PayOS published the white paper Know Your Agent: An Identity Framework for Trusted Agentic Commerce on February 4, 2026, introducing the Digital Agent Passport (DAP) as a lightweight, tamper-proof token for agent-led interactions. The passport framework includes five checkpoints: provenance (which model, developer, and deployment the agent originated from), user binding (the linkage to a verified human principal), permission scope (the boundary of authority within which the agent may act), real-time behavior telemetry (the runtime monitoring stream), and continuous risk scoring (the running aggregate risk signal). The white paper proposes establishing Digital Passport Authorities – operated by identity providers, payment networks, or industry consortia – to issue, sign, and revoke passports analogously to certificate authorities in TLS. Trulioo subsequently partnered with Worldpay to deliver KYA capability to merchants. For lead operators, the five checkpoints map cleanly onto a required verification stack and provide the most operationally specific reference architecture in the KYA literature as of April 2026.

How should a lead operator phase a KYA implementation across the next twelve months?

A realistic phasing for a mid-sized operator runs in three stages. Stage one, months one through three: scope the agent ecosystems most relevant to the operator’s vertical (Mastercard Agent Pay, Google AP2, Skyfire KYAPay, MetaComp AgentX, or others), select a verification provider (Sumsub, Trulioo, or equivalent), and complete compliance counsel review of the proposed logging architecture. Stage two, months three through seven: build first-ecosystem mandate-token ingestion (sixty to ninety engineering days), verification-provider integration (forty to sixty days), mandate-aware compliance logging (forty to eighty days), and parallel buyer-side delivery format negotiations (thirty to forty-five days per buyer). Stage three, months seven through twelve: roll out to additional ecosystems and verification providers, tune the verification stack against drifting threat models documented in Sumsub-style fraud reporting, and extend buyer-side delivery to the remaining buyer relationships as those buyers reach their own KYA-readiness milestones. The phasing front-loads the foundational architecture so that ecosystem-by-ecosystem and buyer-by-buyer extension becomes incremental rather than rebuilding.

What does this mean for lead operators in EU markets specifically?

EU-resident lead volume and EU-jurisdictional buyers face the August 2, 2026 EU AI Act high-risk system enforcement as a hard deadline. The Act’s Article 50 transparency obligations require disclosure of AI interactions, labeling of synthetic content, and deepfake identification. Annex III high-risk categories cover essential private services, employment, and other domains in which agent-mediated lead capture is plausible. Compliance with the Act’s risk management, data governance, technical documentation, transparency, and post-market monitoring obligations is not satisfied by TCPA-grade consent capture; it requires the documentary infrastructure that KYA-grade verification provides. Operators with even a minority share of EU lead volume should plan for KYA-ready operation by August 2, 2026 in their EU-touching workflows, even if their U.S. volume remains on consent-only compliance for longer. The asymmetry – a KYA-ready EU funnel running in parallel with a consent-only U.S. funnel – is operationally feasible and is the path most multi-jurisdiction operators will take during the 2026-2027 transition.

What about lead operators in heavily regulated verticals like healthcare and Medicare?

Verticals with vertical-specific compliance regimes – healthcare under HIPAA, Medicare under CMS marketing rules, credit and lending under FCRA and ECOA, insurance under state-level regimes – face an additional layer. KYA does not displace the vertical regime; it adds a verification dimension on top of it. A Medicare lead originating from an AI agent acting under a beneficiary’s delegated mandate must satisfy CMS marketing rules for Medicare Advantage and Part D plan inquiries and the KYA verification stack. The compound compliance burden is higher than either regime alone, and the mitigation is to design the KYA log so that the vertical-specific compliance artifacts (CMS scope-of-appointment records, FCRA permissible-purpose attestations, state-licensed-producer attributions) are captured alongside the KYA artifacts in a single chain-of-custody log. Operators who built their DNC Registry compliance infrastructure on a vertical-aware schema will find the extension to KYA more tractable than operators on a generic consent-retention substrate.

Sources

Tier 1: Primary and Government Sources

-

National Institute of Standards and Technology, “Announcing the AI Agent Standards Initiative for Interoperable and Secure Innovation,” NIST News, February 2026 – https://www.nist.gov/news-events/news/2026/02/announcing-ai-agent-standards-initiative-interoperable-and-secure

-

NIST Center for AI Standards and Innovation, “AI Agent Standards Initiative,” accessed April 28, 2026 – https://www.nist.gov/caisi/ai-agent-standards-initiative

-

NIST Computer Security Resource Center, “Accelerating the Adoption of Software and Artificial Intelligence Agent Identity and Authorization (Concept Paper),” February 5, 2026 – https://csrc.nist.gov/pubs/other/2026/02/05/accelerating-the-adoption-of-software-and-ai-agent/ipd

-

NIST National Cybersecurity Center of Excellence, “New Concept Paper on Identity and Authority of Software Agents,” 2026 – https://www.nccoe.nist.gov/news-insights/new-concept-paper-identity-and-authority-software-agents

-

NIST NCCoE, “Accelerating the Adoption of Software and AI Agent Identity and Authorization,” PDF concept paper, February 2026 – https://www.nccoe.nist.gov/sites/default/files/2026-02/accelerating-the-adoption-of-software-and-ai-agent-identity-and-authorization-concept-paper.pdf

-

European Commission, “AI Act,” Shaping Europe’s Digital Future, accessed April 28, 2026 – https://digital-strategy.ec.europa.eu/en/policies/regulatory-framework-ai

-

EU Artificial Intelligence Act, “Implementation Timeline,” accessed April 28, 2026 – https://artificialintelligenceact.eu/implementation-timeline/

-

EU Artificial Intelligence Act, “Article 6: Classification Rules for High-Risk AI Systems,” accessed April 28, 2026 – https://artificialintelligenceact.eu/article/6/

Tier 2: Established Industry Research and Trade Press

-

Sumsub, “Identity Fraud Report 2025-2026,” 2026 – https://sumsub.com/fraud-report-2025/

-

Sumsub, “Why KYA Is Critical for Secure Autonomous AI,” Sumsub Blog, 2026 – https://sumsub.com/blog/know-your-agent/

-

Sumsub, “Sumsub’s AI Agent Verification Introduces Agent-to-Human Binding to Establish Human Accountability in AI,” Sumsub Newsroom, January 29, 2026 – https://sumsub.com/newsroom/sumsubs-ai-agent-verification-introduces-agent-to-human-binding-to-establish-human-accountability-in-ai/

-

Sumsub, “Annual Report: Fraud Shifts to Complex Multi-Step Schemes in 2025, Agentic AI Scams Poised to Surge in 2026,” Sumsub Newsroom, November 2025 – https://sumsub.com/newsroom/sumsubs-annual-report-fraud-shifts-to-complex-multi-step-schemes-in-2025-agentic-ai-scams-poised-to-surge-in-2026/

-

Help Net Security, “Sumsub’s AI Agent Verification Binds Automation to Verified Human Identity,” January 29, 2026 – https://www.helpnetsecurity.com/2026/01/29/sumsub-ai-agent-verification/

-

PYMNTS, “Sumsub Adds AI Agent Verification to Know Your Agent Framework,” 2026 – https://www.pymnts.com/news/artificial-intelligence/2026/sumsub-adds-ai-verification-know-your-agent-framework/

-

Mastercard, “How Verifiable Intent Builds Trust in Agentic AI Commerce,” Mastercard News and Trends, March 5, 2026 – https://www.mastercard.com/us/en/news-and-trends/stories/2026/verifiable-intent.html

-

Mastercard, “Agentic Token Framework: Driving Trusted AI Transactions,” Mastercard News and Trends, 2025 – https://www.mastercard.com/global/en/news-and-trends/stories/2025/agentic-commerce-framework.html

-

PYMNTS, “Mastercard Unveils Open Standard to Verify AI Agent Transactions,” March 2026 – https://www.pymnts.com/mastercard/2026/mastercard-unveils-open-standard-to-verify-ai-agent-transactions/

-

McKinsey & Company, “State of AI Trust in 2026: Shifting to the Agentic Era,” McKinsey Tech Forward, 2026 – https://www.mckinsey.com/capabilities/tech-and-ai/our-insights/tech-forward/state-of-ai-trust-in-2026-shifting-to-the-agentic-era

-

McKinsey & Company, “Agentic AI Governance for Autonomous Systems: Trust in the Age of Agents,” McKinsey Risk and Resilience, 2026 – https://www.mckinsey.com/capabilities/risk-and-resilience/our-insights/trust-in-the-age-of-agents

Tier 3: Industry and Vendor Statements

-

MetaComp Pte. Ltd. via PR Newswire, “MetaComp Launches the World’s First AI Agent Governance Framework for Regulated Financial Services,” April 21, 2026 – https://www.prnewswire.com/apac/news-releases/metacomp-launches-the-worlds-first-ai-agent-governance-framework-for-regulated-financial-services-302749713.html

-

Blockhead, “Singapore’s MetaComp Rolls Out AI Agent Governance Framework for Financial Institutions, Regulators,” April 21, 2026 – https://www.blockhead.co/2026/04/21/singapores-metacomp-rolls-out-ai-agent-governance-framework-for-financial-institutions-regulators/

-

Trulioo, “Know Your Agent: An Identity Framework for Trusted Agentic Commerce,” Trulioo White Paper, February 4, 2026 – https://www.trulioo.com/resources/white-papers/know-your-agent-an-identity-framework-for-trusted-agentic-commerce

-

Trulioo, “The Future of Agentic Commerce: Trust With KYA,” Trulioo Blog, 2026 – https://www.trulioo.com/blog/trust-and-safety/future-agentic-commerce-know-your-agent-kya

-

PYMNTS, “Trulioo Bets on a Digital Agent Passport to Keep Bots Honest at Checkout,” 2025 – https://www.pymnts.com/artificial-intelligence-2/2025/trulioo-bets-on-a-digital-agent-passport-to-keep-bots-honest-at-checkout/

-

Skyfire, “Know Your Agent (KYA),” Skyfire Product Page, accessed April 28, 2026 – https://skyfire.xyz/know-your-agent-kya/

-

IETF Datatracker, “draft-skyfire-kyapayprofile-01: KYAPay Profile,” 2026 – https://datatracker.ietf.org/doc/draft-skyfire-kyapayprofile/

-

Skyfire via BusinessWire, “Skyfire Launches Open KYAPay Protocol With Agent Checkout,” June 26, 2025 – https://www.businesswire.com/news/home/20250626772489/en/Skyfire-Launches-Open-KYAPay-Protocol-With-Agent-Checkout

-

Worldpay-Trulioo via Biometric Update, “Trulioo Partners with Worldpay to Offer Know Your Agent to Merchants,” August 2025 – https://www.biometricupdate.com/202508/trulioo-partners-with-payment-platform-worldpay-to-offer-know-your-agent-to-merchants

Tier 4: Supporting Industry Commentary

-

Orrick, “The EU AI Act: 6 Steps to Take Before 2 August 2026,” November 2025 – https://www.orrick.com/en/Insights/2025/11/The-EU-AI-Act-6-Steps-to-Take-Before-2-August-2026

-

WorkOS, “Everything You Should Know About NIST’s AI Agent Standards Initiative,” 2026 – https://workos.com/blog/nist-ai-agent-standards-initiative-explained

-

Jones Walker LLP, “NIST’s AI Agent Standards Initiative: Why Autonomous AI Just Became Washington’s Problem,” AI Law Blog, 2026 – https://www.joneswalker.com/en/insights/blogs/ai-law-blog/nists-ai-agent-standards-initiative-why-autonomous-ai-just-became-washingtons.html

-

Stellagent, “Mastercard Agent Pay Explained: Agentic Tokens and Verifiable Intent for AI Agent Payments,” 2026 – https://stellagent.ai/insights/mastercard-agent-pay-agentic-tokens

-

Stellagent, “KYA (Know Your Agent) Framework – The New Standard for Agent Identity Verification,” 2026 – https://stellagent.ai/insights/kya-know-your-agent-framework

-

Cloud Security Alliance, “NIST AI Agent Standards: Listening Sessions and Emerging Controls,” April 2026 – https://labs.cloudsecurityalliance.org/research/csa-research-note-nist-ai-agent-standards-20260416-csa-style/

-

Akamai, “Bot Management for the Agentic Era,” Akamai Blog, 2026 – https://www.akamai.com/blog/security/bot-management-agentic-era

-

The Paypers, “Mastercard and Google Launch Verifiable Intent,” 2026 – https://thepaypers.com/payments/news/mastercard-introduces-verifiable-intent-co-developed-with-google

Closing

The Telephone Consumer Protection Act of 1991 anchored U.S. lead-generation compliance for thirty-five years on a single premise: a human consumer authorizes contact, and the operator captures and retains that authorization. The premise was sound while the entity filling out the form was a human typing into a browser. In the first four months of 2026, a regulated financial institution in Singapore, an identity-verification provider, a global card network, a federal standards body, and a merchant-side identity stack collectively shipped the architectural components of a parallel framework for an environment in which the entity filling out the form is software acting under a delegated mandate. The framework does not displace TCPA. It supplements it for a class of submissions that did not meaningfully exist when TCPA was written. Operators who begin the mandate-token ingestion, verification-stack integration, mandate-aware logging, and buyer-side delivery work in the next ninety days will run a six-to-twelve-month structural advantage through Q3 2027. The August 2, 2026 EU AI Act enforcement date is a hard deadline for any operator with EU lead volume. The buyer-side adoption curve, with one-third of organizations at McKinsey-measured maturity-level-three on agentic governance, keeps the early-mover window open for about a year and then closes hard. The decision about which side of that window to be on is being made now.

Market data, regulatory developments, and vendor announcements reflect publicly reported conditions through April 28, 2026. Agent-identity standards, verification-provider capabilities, EU AI Act guidance, and NIST direction continue to evolve; verify current terms through primary sources before making operational decisions. This article provides general industry analysis and does not constitute legal, financial, or compliance advice. Consult qualified counsel for specific compliance questions related to mandate retention, agent-identity logging, EU AI Act high-risk system obligations, and TCPA prior express written consent in agent-originated submission flows.