The Agent Payments Protocol Mandate, translated into Mastercard Verifiable Intent and accepted across Visa Intelligent Commerce Connect by mid-2026, is a cryptographically signed authorization that scopes an AI agent’s authority to a specific seller, intent, and outcome. It can support evidence across several distinct compliance categories that should not be conflated – payment authorization (card-network cardholder authorization for the transaction), user-delegation evidence (proof that the user delegated specific authority to a specific agent), marketing consent under TCPA prior express written consent, GDPR Article 6 lawful basis and Article 5(1)(b) purpose limitation, state privacy law, and buyer-specific lead contract acceptance – without by itself satisfying any of those regimes as a matter of law. The Mandate handles the user-delegation-and-scope question (what the agent may do, signed by the user); the parallel agent-identity question (who the agent is and who delegated authority) is treated separately in the companion piece on Know Your Agent frameworks. If the FCC, FTC, and federal courts treat the Mandate as one evidentiary input alongside existing consent capture, the legacy daisy-chained consent architecture gets a stronger evidence layer rather than an immediate replacement.

A Translation Layer That Quietly Re-Wrote the Consent Architecture

In the first three weeks of April 2026, three things happened in payments infrastructure that, taken together, did something the lead-generation industry has been arguing about for half a decade. They created a single, cryptographically signed artifact that captures consumer authorization to do a specific thing with a specific seller, in a form that is portable, tamper-evident, machine-verifiable, and – critically – already accepted by the largest card networks on the planet.

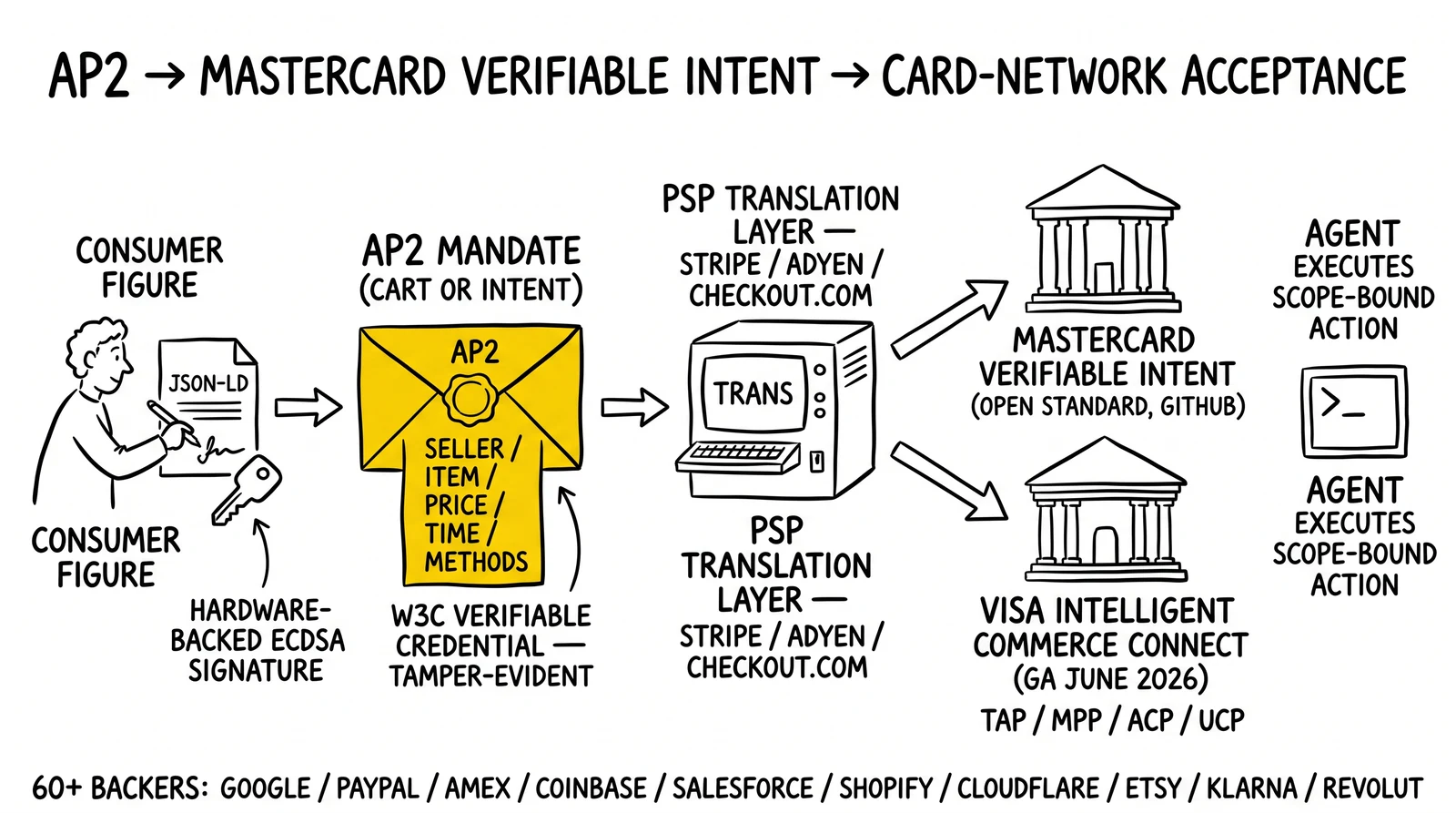

On April 8, 2026, Visa announced Intelligent Commerce Connect, a single-integration on-ramp to agentic commerce that explicitly supports Visa’s own Trusted Agent Protocol alongside the Machine Payments Protocol, the Agentic Commerce Protocol, and the Universal Commerce Protocol. General availability is targeted for June 2026. By mid-April, Stripe, Adyen, and Checkout.com – the three payment service providers who handle a non-trivial share of card-not-present transaction volume across U.S. and European e-commerce – were shipping integrations that take an AP2 Mandate emitted by an AI agent and translate it, on the wire, into a Mastercard Verifiable Intent artifact for clearing on the Mastercard rails. On April 22, 2026, MetaComp, a Singapore-licensed financial institution, formalized a Know Your Agent framework that extends Travel Rule-style identity exchange to agent-to-agent transactions in regulated finance.

For most readers, this looked like payments-stack plumbing. For the lead-generation compliance community, it is something else. It is the first time in the post-Duguid era that a regulated, cryptographically verifiable, cross-network consent artifact has shipped into production, and it is the first time that the artifact has been designed at the protocol layer to be portable across sellers, intent, and downstream parties. The Mastercard Verifiable Intent specification is open-sourced on GitHub. The AP2 Mandate is an open standard with more than sixty backers including Mastercard, PayPal, American Express, Coinbase, Salesforce, Shopify, Cloudflare, Etsy, Klarna, and Revolut. The Visa Trusted Agent Protocol was developed in collaboration with Cloudflare. None of these are proprietary trust frameworks; all of them are betting on the same primitive.

The primitive is the Mandate, and the Mandate is the news. It can support evidence across TCPA prior express written consent, GDPR Article 6 lawful basis and Article 5(1)(b) purpose limitation, state privacy law, card-network cardholder authorization, user-delegation, and buyer contract acceptance – but each of those regimes remains its own legal analysis. The Mandate is an evidence layer, not a replacement for consent analysis, and it is being deployed at the speed and scale that the card networks deploy at – which is to say, faster than regulators tend to keep up with. This analysis examines why Mandate evidence matters for lead-gen compliance more than the people building it realize, what the translation layer between AP2 and the card networks actually does, why the now-vacated FCC one-to-one consent rule looks in retrospect like an attempted manual implementation of an evidence problem that cryptographic delegation can partially address, and what compliance officers and lead buyers should be doing in Q3 2026 to be Mandate-ready.

What Actually Shipped in March and April 2026

The headline events were several, and the order matters.

In September 2025, Google introduced the Agent Payments Protocol with more than sixty initial backers and an open specification. The protocol’s core trust primitive is the Mandate – a JSON-LD Verifiable Credential, signed using ECDSA cryptography, that captures a user’s authorization for an AI agent to perform a specific action. AP2 defines two variants. The Cart Mandate is generated by a merchant when a human is present at purchase time and is signed by the user via a hardware-backed key on their device with in-session authentication. The Intent Mandate is generated by a Shopping Agent when the human is not present at transaction time and serves as the non-repudiable authorization for the agent to execute purchases under defined constraints. Both are tamper-evident: any modification to the credential invalidates the entire signature chain.

Mastercard moved next. The company’s Agent Pay program had completed its first authenticated agentic transaction in Q3 2025, with U.S. Bank and Citibank cardholders as the first issuer participants. By November 2025, Agent Pay was enabled for the rest of Mastercard’s U.S. issuers, with a global rollout planned for early 2026. In March 2026, Mastercard announced Verifiable Intent as an open standard, designed to be protocol-agnostic across AP2 and the Universal Commerce Protocol and open-sourced on GitHub. The launch commitment list included Google, Fiserv, IBM, Checkout.com, Basis Theory, and Getnet. Verifiable Intent uses Selective Disclosure – a cryptographic technique that shares only the minimum information needed with each party in a transaction – to create a tamper-resistant record of what a user authorized when an AI agent acted on their behalf.

On April 8, 2026, Visa announced Intelligent Commerce Connect. The platform is a network-agnostic, protocol-agnostic, token-vault-agnostic on-ramp to agentic commerce, available through a single integration with the Visa Acceptance Platform. Pilot partners include Aldar, AWS, Diddo, Highnote, Mesh, Payabli, and Sumvin. Crucially, Intelligent Commerce Connect supports payment initiation via Trusted Agent Protocol, the Machine Payments Protocol, the Agentic Commerce Protocol, and the Universal Commerce Protocol – meaning the same merchant integration accepts agentic transactions from agents speaking any of the four protocols, with translation handled at the platform layer. General availability is targeted for June 2026.

Three PSPs – Stripe, Adyen, and Checkout.com – moved into the gap between the agent layer and the card-network layer. By mid-April 2026, each of the three was shipping integrations that take an AP2 Mandate emitted by an AI agent and translate it, transparently to the agent, into a Mastercard Verifiable Intent artifact for clearing on the Mastercard rails. The same translation pattern works in the reverse direction for Visa-routed transactions: the agent expresses intent in AP2, the PSP translates into the appropriate Visa-side artifact, Intelligent Commerce Connect routes it. Adyen is publicly listed among the AP2 launch backers; Checkout.com is named among the Mastercard Verifiable Intent commitment partners; Stripe’s broader agentic-commerce stack supports the Agentic Commerce Protocol natively and exposes translation paths into adjacent frameworks.

Then on April 22, 2026, MetaComp launched the StableX Know Your Agent framework at Money20/20 Asia. KYA is the first agent-governance framework authored by a regulated financial institution. It assigns each agent a verified identity linked to a real-world individual or legal entity, defines authority and permission control, monitors behavior, and – most importantly for lead-gen – applies the FATF Travel Rule’s identity-exchange logic to agent-to-agent transactions. The implication is that an agent acting on behalf of a consumer in a regulated financial-services workflow now has, in at least one major jurisdiction, an identity-and-permissions artifact that is itself cryptographically tied to the consumer’s authorization.

What you have at the end of April 2026 is a stack: a Mandate primitive at the top, a translation layer through PSPs and card-network platforms in the middle, and a governance layer at the bottom for regulated jurisdictions. Each layer was designed by a different organization. Each layer was shipped on a different timeline. Together, they constitute a consent infrastructure that did not exist on January 1, 2026.

The Mandate Can Support Evidence Across Every Element of TCPA Prior Express Written Consent

To understand why this matters for lead-gen, hold the AP2 Mandate up against the TCPA’s prior express written consent standard and look at what each one captures.

Prior express written consent under the TCPA, as the regulatory architecture stood after the Eleventh Circuit vacated the FCC’s one-to-one consent rule on January 24, 2025 in Insurance Marketing Coalition v. FCC, requires that a consumer “clearly and unmistakably” authorize the receipt of regulated communications before they happen. The Eleventh Circuit ruled that the FCC exceeded its statutory authority by adding requirements beyond the plain meaning of the statute – specifically the one-seller-at-a-time requirement and the “logically and topically” associated requirement. The FCC eventually issued a final rule in September 2025 that formally killed the one-to-one consent requirement following the Eleventh Circuit decision. What remains is the statutory standard: clear, unambiguous, prior, express, written authorization to receive marketing calls or texts using regulated technologies.

What the TCPA does not require – and what the regulators have been struggling to specify in a defensible way – is a portable, machine-verifiable, tamper-evident artifact that captures the consent. The industry has spent the past decade building approximations: clickwrap timestamps, TrustedForm certificates and Jornaya LeadiD tokens, session-recording playbacks, IP-and-user-agent fingerprints. All of these are evidentiary aids for a consent event that is otherwise difficult to reconstruct after the fact. None of them is cryptographically signed by the consumer.

The AP2 Mandate is. A Cart Mandate is generated by the merchant, signed by the user via a hardware-backed key on their device, and bound to the user’s identity and authorization at the moment of in-session authentication. An Intent Mandate is generated by the Shopping Agent, signed by the user using the same hardware-backed-key path, and scoped to specific constraints – seller, item categories, price ceilings, time windows, downstream sharing rules. Both Mandates are tamper-evident: modifying any element invalidates the cryptographic signature. Both are W3C Verifiable Credentials, which means they are designed for portability across systems.

Compare that, item by item, against the elements of prior express written consent that TCPA litigation typically turns on: did the consumer consent (signature: yes, cryptographic); was the consent express (Mandate is explicit about scope); was it written (the JSON-LD object is the writing); was it prior (the signed timestamp is present in the credential); did it cover the seller in question (the seller is named in the Mandate scope); did it cover the technology used (the technology is named in the Mandate scope). Every element of the TCPA standard maps to an element of the Mandate, and the Mandate carries cryptographic proof for each.

The Mandate goes further than the TCPA standard requires. It carries purpose limitation in a form GDPR Article 5(1)(b) directly recognizes – the Intent Mandate scopes the agent to specific actions, beyond which the agent has no authority. It carries cardholder authorization in the form Mastercard and Visa now accept at the network level. It carries downstream-sharing constraints that map cleanly onto the FTC’s Telemarketing Sales Rule do-not-call and consent-transfer requirements. A single artifact, in other words, captures consent for purposes that until April 2026 required separate documentation streams.

This is not a coincidence. The protocol designers – Google, Mastercard, Visa, the AP2 backer consortium – explicitly studied the failure modes of legacy consent architectures and designed against them. The result is a primitive that solves a problem the FCC could not solve through rulemaking, because the problem turned out to be the wrong shape for a notice-and-comment fix.

Why the FCC’s One-to-One Rule Was the Wrong Tool for the Right Problem

The Eleventh Circuit decision on January 24, 2025 was, on the surface, a legal-doctrine ruling about the limits of FCC authority under the TCPA. It was also, structurally, a signal that the daisy-chain attribution problem the FCC was trying to solve cannot be solved through a one-to-one rule, because the rule treats consent as a binary attribute of a transaction rather than as a signed artifact that travels with the transaction.

The original FCC rule would have required, first, that a consumer give consent to receive TCPA-regulated communications from one identified seller at a time, and second, that the consent be “logically and topically” associated with the interaction that gave rise to it. The motivation was clear. Lead aggregators had built business models around comparison-shopping forms that captured a single consumer consent and then used that consent to authorize calls and texts from dozens or hundreds of downstream sellers. The FCC saw consumers being inundated with calls from sellers they did not recognize and concluded that the consent had been stretched beyond what consumers reasonably understood themselves to have authorized.

The legal vehicle the FCC chose – restricting the per-transaction breadth of consent – failed at the Eleventh Circuit because the underlying TCPA statute does not authorize the restriction. The plain meaning of “prior express consent” is, per the court, that the consumer “clearly and unmistakably” authorize the call. Whether the authorization names one seller or many is a contractual and disclosure question, not a statutory consent question. The FCC tried to push a rule that the statute did not support, and the court vacated the rule.

What is interesting in retrospect is what the FCC was actually trying to solve. The daisy-chain problem is fundamentally an attribution problem: when a consumer consents and the consent is then transferred through a chain of intermediaries, who is responsible for ensuring the scope of the consent is preserved at each transfer? The FCC’s answer was to require explicit per-seller consent at the original consent event, which would force the disclosure of the entire downstream chain to the consumer up front. The court’s view was that the statute does not authorize that requirement.

The AP2 Mandate solves the attribution problem differently. The Mandate is itself the unit of consent. It travels with the transaction. It is cryptographically signed by the consumer. Its scope is specified at the moment of signing and cannot be modified without invalidating the signature. If a downstream party tries to act outside the scope, the Mandate will not validate, and the action will fail at the protocol layer. The consumer does not need to enumerate downstream sellers in advance, because the consumer’s authorization is bounded by what the Mandate specifies – and the Mandate’s specification is enforceable by every party in the chain who validates it.

In other words, the FCC tried to solve a downstream-attribution problem with an upstream-disclosure rule. The cryptographic Mandate solves the same problem by making the consent itself the carrier of the scope. The court was right that the rule was the wrong tool. The protocol designers built the right tool, in a different layer of the stack, on a different timeline, with different incentives. The question now is whether the regulators and the courts will accept the right tool when it shows up.

The Daisy-Chain Problem and What Mandate-Based Routing Looks Like in Practice

To make this concrete, consider how a mortgage-rate-comparison lead generator operates today and how the same operation would work in a Mandate-based architecture.

Today. A consumer fills out a form on a comparison site. The form captures the consumer’s name, contact information, and a click-to-consent checkbox that authorizes the publisher and “marketing partners” to contact the consumer. A TrustedForm certificate is generated. A Jornaya LeadiD token is generated. The lead is sold simultaneously or sequentially to several mortgage lenders – sometimes through an exclusive contract, more often through a shared-lead distribution model that sends the lead to multiple buyers within seconds. Each buyer receives the lead with the consent artifact. Each buyer is supposed to validate the consent before placing a call. Most do. Some do not. In any given month, several thousand TCPA cases are filed challenging whether the consent in question was valid for the specific call that triggered the complaint. Insurance Marketing Coalition v. FCC was, in part, a defense of this distribution model against the FCC’s attempt to constrain it.

Tomorrow, with Mandates. The consumer authenticates into a comparison agent. The agent generates an Intent Mandate scoped to “obtain mortgage-rate quotes from up to N lenders matching profile X, contact via methods Y, within time window Z.” The consumer signs the Mandate using a hardware-backed key on their device. The Mandate is published to the agent ecosystem. Lenders’ agents query for matching Mandates, and each lender receives a copy of the Mandate scoped specifically to its participation. When a lender’s agent contacts the consumer, the Mandate is the authorization. The contact is bounded by what the Mandate specifies – including the methods, the time window, and the maximum number of contacts. Any contact outside the Mandate’s scope is, by construction, unauthorized.

The shift is not subtle. In the legacy model, consent is captured once and then attempted to be preserved through evidentiary trails. In the Mandate model, consent is the routing instruction. A lender’s agent cannot place a call outside the scope of the Mandate, because the Mandate is the only authorization that will validate at the protocol layer. The agent does not need to ask whether it has consent; the agent has either a valid Mandate scoped to the action it is about to take, or it does not.

For a class action plaintiff’s bar that has driven 2,400-plus TCPA filings annually, this changes the underlying litigation theory. The current theory is that the consent the lead generator captured was either invalid in form, not transferred properly, or stretched beyond its original scope. In a Mandate world, the relevant question becomes whether the agent that placed the call had a valid Mandate scoped to that call. The answer is binary and cryptographically verifiable. The fuzzy middle that drives most TCPA litigation collapses.

For a lead buyer, this changes the inventory. A Mandate-scoped lead is not a “lead” in the legacy sense; it is a routing instruction with a built-in authorization scope. Buying that inventory means accepting the scope of the Mandate. If the buyer’s intended use does not fit within the scope, the buyer cannot validly act on the lead. This is closer to what the FCC’s one-to-one rule was trying to enforce, but it is implemented at the protocol layer rather than at the rulemaking layer.

The Three-Way Compliance Convergence: TCPA, GDPR, and Card-Network Authorization

The thesis of this article – that the AP2 Mandate is the first compliance primitive that can support evidence across TCPA-style marketing consent, GDPR Article 6 lawful basis and Article 5(1)(b) purpose limitation, state privacy law, card-network cardholder authorization, user-delegation, and buyer contract acceptance simultaneously – is not theoretical at this point. The convergence is happening in production, on the wire, in April 2026. The compliance officer’s question is not whether to engage with it but how to layer Mandate evidence beside the existing consent-capture stack without conflating the regimes.

Take each of the three regulatory regimes and look at what the Mandate offers.

The TCPA regime requires prior express written consent for regulated marketing communications. The Mandate is signed, in writing (a cryptographically tamper-evident JSON-LD object), prior to the action it authorizes, and explicit about its scope. The signature is verifiable. The scope is enforceable at the protocol layer. The Eleventh Circuit’s reading of the statute – that consent need only be clear and unambiguous – is satisfied trivially by a Mandate, because the Mandate’s scope is enumerated in the credential itself. There is no question about whether the consumer “really” consented to the specific action the agent took; the action is either within the Mandate’s scope or it is not.

The GDPR regime requires that personal data be processed for specified, explicit, and legitimate purposes (Article 5(1)(b)) and not further processed in a manner incompatible with those purposes. The Mandate scopes the agent’s authority to specific purposes – purchase a specific item, query specific sellers, share specific data fields with specific parties. Article 5(1)(b)‘s purpose-limitation requirement is the essence of what an Intent Mandate captures. The cryptographic enforcement is stronger than the GDPR contemplates; the regulation imagines purpose limitation as a contractual and procedural constraint. The Mandate makes it a protocol-layer constraint.

The card-network regime requires cardholder authorization for transactions on the network. Mastercard’s Verifiable Intent and Visa’s Trusted Agent Protocol, both supported in the AP2-translated form, are the network-level acceptance of the Mandate as authorization. A transaction that carries a valid Mandate is authorized; a transaction without a Mandate, or with a Mandate whose scope does not cover the transaction, fails network validation. This is a stronger form of cardholder authorization than the legacy CVV-and-3DS flow, because the authorization is bound to the specific action rather than to the card.

Three regulatory regimes, three sets of requirements, one artifact that can support evidence in each – without by itself satisfying any of them as a matter of law. The architecture is not perfect – there are jurisdictional questions about what counts as a “writing” under TCPA when the writing is a cryptographic object, GDPR questions about how the Mandate’s scope interacts with data-subject rights of access and erasure, state privacy law questions about whether Mandate evidence supports buyer-specific consent transfer, and consumer-protection questions about how clearly the consumer understood the scope they signed. None of these questions is unanswerable. All of them remain open until regulators and courts speak. The Mandate strengthens the evidence record in each regime; it does not collapse the regimes into a single compliance primitive.

The compliance officer who engages with this architecture in Q3 2026 has a different job than the compliance officer who engaged with TCPA-and-GDPR consent architectures in 2024. The legacy job was to build evidentiary trails and litigate over their adequacy. The new job is to validate that Mandate-based flows are correctly scoped, correctly signed, and correctly bounded – and to push back on agent and merchant counterparties whose Mandate flows are loose enough to create downstream liability. It is a more technical job, and a more decisive one.

What Lead Buyers Should Be Doing in Q3 2026 to Be Mandate-Ready

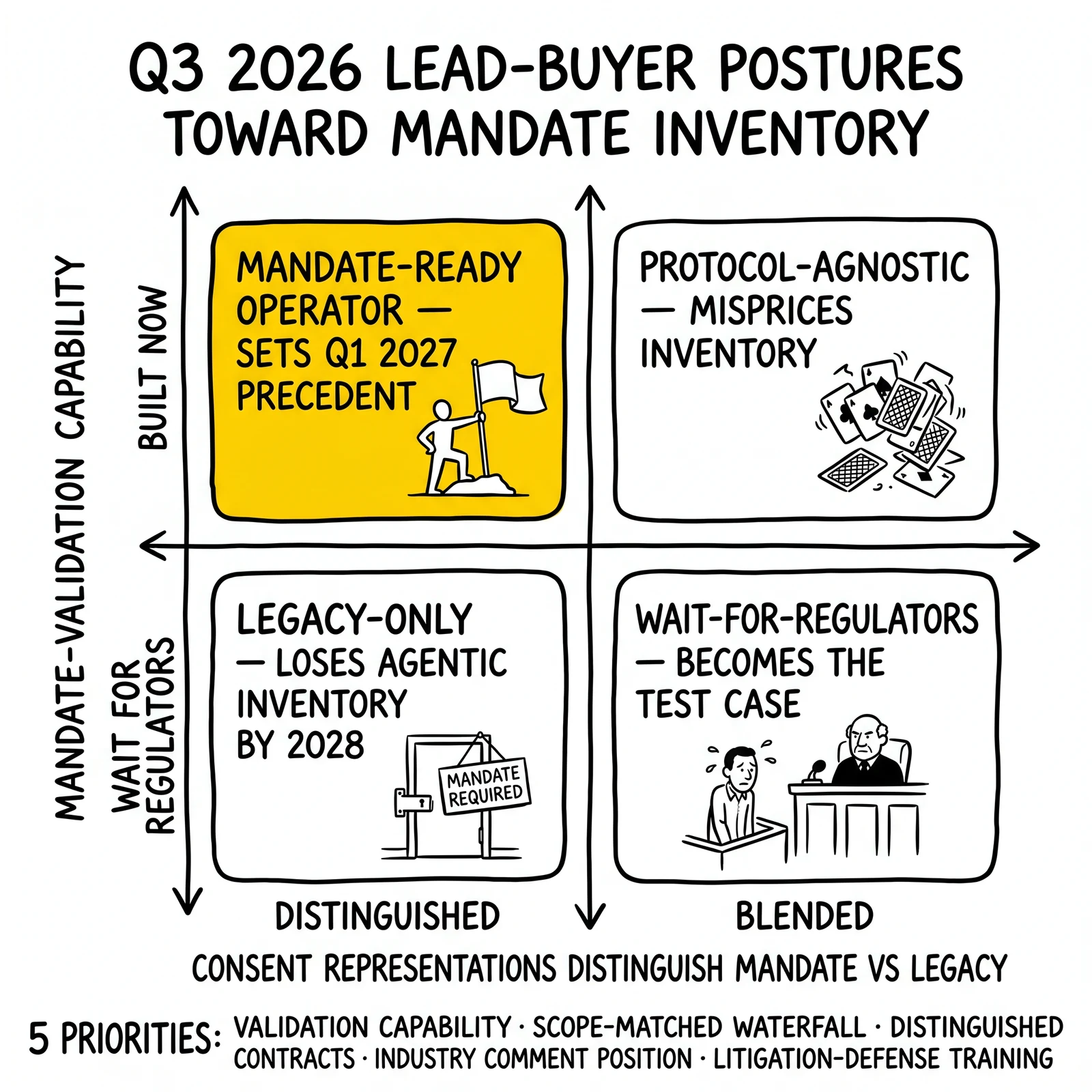

The translation layer is shipping now. The card-network platforms are going to general availability in mid-2026. The PSP integrations are live in production at three major providers. The MetaComp KYA framework is the regulated-financial-services parallel. The window for lead buyers to position for Mandate-based inventory is the next two to three quarters; by Q1 2027, the operators who have built Mandate-aware buying logic will be transacting on a different cost basis than the operators who have not.

Five priorities for compliance and lead-buyer leadership through Q3 2026:

First, build Mandate-validation capability. A buyer who cannot validate an incoming Mandate at the protocol layer is buying an artifact they cannot enforce. The validation is technical: parse the JSON-LD credential, verify the cryptographic signature against the consumer’s public key, check the scope against the intended action, confirm the issuer’s chain of trust. AP2 reference implementations are available. Most lead-distribution platforms will need to add the validation as a first-class feature; few have it today. The engineering investment is moderate – comparable to integrating a new identity-verification provider – and the cost of not having it is the inability to participate in Mandate-based inventory streams.

Second, redesign the buyer waterfall around Mandate-scope matching. Today’s waterfall sorts inventory by buyer pricing tier and exclusivity. Tomorrow’s waterfall needs to sort by Mandate scope: which buyers have intended actions that fit inside which Mandates’ scopes? A Mandate scoped to “mortgage rate quotes from up to three lenders” cannot be sold to four lenders. A Mandate scoped to “follow-up contact within 72 hours” cannot be sold to a buyer whose follow-up cycle runs longer. The matching is not optional; the Mandate’s scope is the binding constraint, and routing inventory outside the scope produces an unauthorized action.

Third, renegotiate consent representations and warranties with publisher counterparties. Most lead-buyer contracts contain consent representations that assume the publisher’s TCPA-compliant consent capture is valid. As Mandate-based inventory enters the mix, the contracts need to specify which inventory is Mandate-backed and which is legacy-consent-backed, and the consent representations need to differ across the two. Mandate-backed inventory should warrant the cryptographic validity of the Mandate; legacy-consent inventory should continue to warrant the form and substance of the captured consent. Mixing them under a single representation creates ambiguity that benefits neither party.

Fourth, prepare regulatory-engagement positions on Mandate acceptance. The FCC, the FTC, and state attorneys general are going to face questions about whether Mandates count as “prior express written consent” under TCPA, whether they satisfy the Telemarketing Sales Rule’s consent transfer requirements, and whether they create a defense or a strict-liability path for downstream callers. The industry’s position will be more credible if it is articulated before the first enforcement action than after. Coordinated industry comment letters, supported by engineering documentation of the Mandate’s properties, are the right vehicle. The lead-gen trade associations should be drafting now.

Fifth, train the operations team on Mandate-aware arbitration and litigation defense. When the first TCPA case is filed against a buyer who acted on a Mandate, the defense will turn on the Mandate’s cryptographic properties. The operations team – including external counsel, the litigation support function, and the compliance engineering team – needs to be able to produce the Mandate, demonstrate its validity, prove the action taken was within scope, and show the chain of custody from the consumer’s signing event to the agent’s action. This is a different evidentiary record than the legacy TrustedForm-and-call-recording stack, and the team that has not practiced producing it will struggle when the first case lands.

These five priorities are all Q3 2026 work. None of them requires waiting for the FCC, the FTC, or any court to validate the architecture. All of them position the buyer for the architecture as it ships.

What Will Underperform: The Three Postures That Lose Margin in 2026

Three responses to the AP2-and-Verifiable-Intent translation layer are visible in the early industry chatter. Each will produce worse outcomes than its proponents expect.

The first is the wait-for-regulators posture. The argument runs that until the FCC, the FTC, or a federal court explicitly accepts Mandates as evidence of consent, lead buyers should continue operating on the legacy consent stack and treat Mandate-based inventory as experimental. The problem is that the card networks are not waiting for U.S. communications regulators. Mastercard Verifiable Intent and Visa Intelligent Commerce Connect are going live regardless of TCPA jurisprudence, because the card-network use case (cardholder authorization for agent-initiated transactions) does not depend on TCPA. By the time the U.S. communications regulators take a position, the Mandate-based inventory streams will have established their own market clearing prices, and the buyers who waited will be entering at a structural cost disadvantage.

The second is the legacy-consent-only posture. Some buyers will conclude that the safe path is to continue requiring TrustedForm certificates and Jornaya LeadiD tokens for every lead, treating Mandates as supplementary rather than substitutive. The argument is that the legacy consent stack has known litigation risks but well-developed defense playbooks, while Mandates are untested in court. The argument is sound for the next twelve months and wrong by 2028. The legacy consent stack is built on evidentiary aids that approximate consent; the Mandate stack carries cryptographic proof of consent. As courts and regulators encounter both, the Mandate’s evidentiary superiority will become apparent, and the legacy stack will be increasingly treated as the inferior default. Buyers who insist on legacy-only will lose access to the agentic commerce inventory streams that constitute most of the new lead supply by 2027.

The third is the protocol-agnostic posture. Some buyers will accept Mandates without distinguishing among AP2, Trusted Agent Protocol, Machine Payments Protocol, Agentic Commerce Protocol, and Universal Commerce Protocol – treating any agent-signed consent artifact as equivalent. The architectures are different. The cryptographic guarantees are different. The downstream-sharing semantics are different. A buyer who treats a Universal Commerce Protocol token as functionally equivalent to an AP2 Cart Mandate will have inventory that does not validate cleanly when audited and will discover the mismatch the first time a regulator or a plaintiff’s expert examines the artifact. Protocol-aware buyers will price inventory accordingly; protocol-agnostic buyers will misprice it.

The common error across all three postures is treating the Mandate as a documentation question rather than as a routing primitive. Documentation can wait. Routing cannot.

The Regulatory Acceptance Path: When and How

The Mandate’s architectural superiority does not automatically translate into regulatory acceptance. The path from “the protocol designers built a primitive that solves the consent problem” to “the FCC, the FTC, and federal courts treat the Mandate as dispositive evidence of TCPA-compliant consent” runs through specific decisions by specific entities, on specific timelines.

The first entity is the FCC. The Commission’s September 2025 final rule formally killed the one-to-one consent requirement following the Eleventh Circuit’s January 2025 vacatur. The Commission has not yet taken a position on Mandate-based consent. The most likely vehicle for that position is a declaratory ruling in response to an industry petition, or a guidance document under the Telemarketing Sales Rule overlap. The trade associations are well-positioned to file the petition; the technical documentation supporting Mandate validity is publicly available in the AP2 specification. A declaratory ruling could land in Q4 2026 or H1 2027.

The second entity is the FTC. The Commission’s enforcement of the Telemarketing Sales Rule and Section 5 deception authority overlaps with TCPA-compliant lead-generation practices. The FTC has historically been more sympathetic to technology-based consent infrastructure than the FCC, and the cross-network adoption of Verifiable Intent by Mastercard and Visa creates a strong record that the Mandate is industry-recognized rather than a novelty. An FTC workshop or staff report on agentic-commerce consent could land in 2026, with formal guidance in 2027.

The third entity is the federal courts. The first TCPA case in which a defendant produces a Mandate as the consent artifact will be a leading indicator. The relevant judicial questions are whether the Mandate satisfies the statutory definition of “prior express consent” under the Eleventh Circuit’s plain-meaning reading, whether the Mandate’s cryptographic signature counts as a writing for purposes of the TCPA’s signed-consent requirements (though those requirements were partly relaxed by the FCC’s 2025 rulemaking), and whether the Mandate’s scope-bound enforcement supports a defense that the contact was within the scope of the consumer’s authorization. The first case is likely in 2027; the first appellate decision could land in 2028 or 2029.

The fourth set of entities is the state attorneys general and state-level TCPA-equivalent statutes. Florida, Oklahoma, and Washington in particular have enacted state-level “mini-TCPAs” with private rights of action. State courts and state AGs may move faster than federal entities, and state enforcement creates leading indicators on what scope of Mandate language is treated as adequate. State-level guidance is likely in 2026-2027.

The cumulative timeline: Mandate-based inventory ships in 2026; first regulatory engagements in late 2026 and 2027; first appellate guidance in 2028-2029; clear regulatory consensus probably not before 2029. During the gap between protocol shipment and regulatory consensus, the lead-buyer community will operate on its own internal interpretations of Mandate adequacy. The buyers who have built Mandate-validation capability and Mandate-aware contracts will be at an evidentiary advantage if the first cases against the new architecture come in early. The buyers who have not will be the test cases.

Frequently Asked Questions

What is an AP2 Mandate?

An AP2 Mandate is a cryptographically signed Verifiable Credential under the Agent Payments Protocol introduced by Google in September 2025. It captures a user’s authorization for an AI agent to perform a specific action – purchase a specific item, query specific sellers, contact specific parties, share specific data – and binds the authorization to the user’s identity through a hardware-backed cryptographic signature. AP2 defines two variants: the Cart Mandate, generated by a merchant when a human is present at purchase time, and the Intent Mandate, generated by a Shopping Agent when the human is not present at transaction time. Both are JSON-LD objects signed using ECDSA cryptography and structured according to the W3C Verifiable Credentials standard. Any modification to the Mandate invalidates its signature, making it tamper-evident.

How does Mastercard Verifiable Intent relate to AP2?

Mastercard Verifiable Intent is an open standard, launched in March 2026 and open-sourced on GitHub, that creates a tamper-resistant record of what a user authorized when an AI agent acts on the user’s behalf. It is designed to be protocol-agnostic across AP2 and the Universal Commerce Protocol. The translation layer that PSPs including Stripe, Adyen, and Checkout.com began shipping in early 2026 takes an AP2 Mandate emitted by an AI agent and translates it on the wire into a Mastercard Verifiable Intent artifact for clearing on the Mastercard rails. The agent expresses authorization in AP2; Mastercard accepts it as Verifiable Intent. Launch commitment partners include Google, Fiserv, IBM, Checkout.com, Basis Theory, and Getnet.

What is Visa Intelligent Commerce Connect and how does it differ from Mastercard’s approach?

Visa Intelligent Commerce Connect, announced April 8, 2026 with general availability targeted for June 2026, is a network-agnostic, protocol-agnostic, token-vault-agnostic on-ramp to agentic commerce available through a single integration with the Visa Acceptance Platform. Unlike Mastercard Verifiable Intent, which is itself an open standard, Intelligent Commerce Connect is a platform service that accepts payment initiation via multiple agent protocols – Visa’s own Trusted Agent Protocol, the Machine Payments Protocol, the Agentic Commerce Protocol, and the Universal Commerce Protocol. The practical effect for merchants is similar: a single integration that accepts agentic transactions from agents speaking any major protocol. Pilot partners include Aldar, AWS, Diddo, Highnote, Mesh, Payabli, and Sumvin. Trusted Agent Protocol was developed in collaboration with Cloudflare.

Why do compliance officers care about an agentic-payments protocol?

The Mandate at the heart of AP2 – and the Verifiable Intent and Trusted Agent Protocol artifacts that translate from it – is a cryptographically signed authorization that captures user delegation and intent in a form that is portable, tamper-evident, and machine-verifiable. The Mandate can support evidence of every element of TCPA prior express written consent: it is signed, written, prior, express, and explicit about its scope. It can also support evidence under GDPR Article 5(1)(b) purpose limitation and card-network cardholder authorization. AP2-style mandates can create stronger evidence of user scope and intent, but they do not by themselves satisfy TCPA, GDPR, state privacy law, or buyer-specific lead consent requirements; each regime remains its own legal analysis. For compliance officers, this is an evidence layer that strengthens – not a replacement that retires – the multi-stream documentation architecture that TCPA, GDPR, state privacy law, and card-network compliance currently require, and the layer is shipping in production at three major PSPs as of April 2026.

What happened to the FCC’s one-to-one consent rule?

The Eleventh Circuit Court of Appeals vacated the FCC’s one-to-one consent rule on January 24, 2025 in Insurance Marketing Coalition v. FCC, ruling that the FCC exceeded its statutory authority under the TCPA. The rule would have required consumers to give consent to receive TCPA-regulated communications from one identified seller at a time, with the consent “logically and topically” associated with the interaction that produced it. The Court held that “prior express consent” under the TCPA requires only that the consumer “clearly and unmistakably” authorize the call, with no statutory basis for the FCC’s per-seller restriction. Following the decision, the FCC issued a final rule in September 2025 that formally killed the one-to-one consent requirement. The underlying TCPA prior-express-written-consent standard remains in force.

Does an AP2 Mandate count as TCPA prior express written consent?

This is the open question that will determine the regulatory trajectory of the Mandate architecture in U.S. lead-generation. The Mandate can support evidence of every element of the statutory standard as the Eleventh Circuit articulated it: it is prior (the timestamp is in the credential), express (the scope is enumerated), written (the JSON-LD object is the writing), and signed by the consumer (cryptographically, using a hardware-backed key). Whether that evidence is treated as sufficient under TCPA, alongside or instead of legacy clickwrap-and-certificate evidence, is a question for the FCC, the FTC, and federal courts. The FCC has not yet taken a position. The first federal court to encounter a Mandate as the proffered consent artifact will set a leading indicator. Until then, lead buyers operating on Mandate-based inventory are making their own interpretations of evidentiary adequacy and should layer Mandate evidence beside existing consent capture rather than substitute it.

How does the Mandate solve the daisy-chain attribution problem?

In the legacy lead-generation model, a single consumer consent is captured at one point and then transferred through a chain of intermediaries – comparison sites, lead aggregators, lead buyers, downstream callers. The attribution problem is that each transfer creates an opportunity for the scope of the consent to drift, and the consumer’s original authorization may not match what the final downstream party actually does. The FCC’s vacated one-to-one rule tried to solve this by requiring per-seller disclosure at the original consent event. The Mandate solves it differently: the Mandate is itself the unit of consent, it travels with the transaction, its scope is specified at signing time and is enforceable by every party in the chain who validates it cryptographically. A downstream party cannot act outside the Mandate’s scope, because the protocol layer rejects unauthorized actions. The attribution problem becomes a routing problem, and routing is solved.

Which payment service providers support AP2-to-Verifiable-Intent translation today?

As of April 2026, Stripe, Adyen, and Checkout.com are shipping payment-service-provider implementations that emit AP2 Mandates as Mastercard Verifiable Intent artifacts. Adyen is publicly listed among the AP2 launch backers; Checkout.com is named among Mastercard Verifiable Intent commitment partners; Stripe’s broader agentic-commerce stack supports the Agentic Commerce Protocol natively and exposes translation paths into adjacent frameworks. The translation pattern is that the agent expresses intent in AP2, the PSP performs the protocol translation, and the resulting artifact is accepted at the card-network level. Worldpay and Revolut are also listed among AP2 backers and are expected to ship analogous translation capabilities through 2026.

What is the Know Your Agent framework that MetaComp launched on April 22, 2026?

The StableX Know Your Agent framework, launched by MetaComp at Money20/20 Asia in Bangkok on April 22, 2026, is the first AI agent governance framework authored by a regulated financial institution. It assigns each AI agent a verified identity linked to a real-world individual or legal entity, defines authority and permission control, monitors agent behavior, and applies the FATF Travel Rule’s identity-exchange logic to agent-to-agent transactions. The framework is organized around four pillars: agent identity and registration, authority and permission control, behavior monitoring and risk intelligence, and ecosystem and interaction governance. For regulated financial-services lead generators, KYA is the parallel architecture to AP2’s Mandate primitive – it provides the agent-side identity and permissions infrastructure that complements the Mandate’s consent infrastructure.

What should lead buyers be doing in Q3 2026 to be Mandate-ready?

Five priorities. First, build Mandate-validation capability – parse the JSON-LD credential, verify the cryptographic signature, check the scope against the intended action. Second, redesign the buyer waterfall around Mandate-scope matching, so inventory routes only to buyers whose intended actions fit within the Mandate’s authorized scope. Third, renegotiate consent representations and warranties with publisher counterparties to distinguish Mandate-backed inventory from legacy-consent-backed inventory. Fourth, prepare regulatory-engagement positions on Mandate acceptance, including coordinated industry comment letters supported by engineering documentation. Fifth, train the operations team on Mandate-aware litigation defense, including Mandate production, signature validation, and scope-of-use proofs. None of these requires waiting for the FCC, FTC, or any court to validate the architecture; all of them position the buyer for the architecture as it ships.

Will AP2 Mandates eliminate TCPA litigation?

Not in the short run. TCPA litigation will continue at high volumes through at least 2027 because most inventory in the market remains on the legacy consent stack, and the plaintiff’s bar has well-developed playbooks for challenging legacy consent artifacts. Over the medium term, as Mandate-based inventory grows and the courts and regulators issue guidance on Mandate adequacy, litigation theory will shift. The fuzzy-middle questions that drive most current cases – was the consent valid, was it transferred properly, was the call within scope – collapse in a Mandate world into a binary cryptographic question. Litigation will not disappear, but the unit-economics of TCPA cases will change. Cases against Mandate-backed inventory will need to attack the cryptographic chain or the scope interpretation, both of which are harder than attacking a TrustedForm certificate. Cases against legacy-consent inventory will continue under existing theories, but the inventory pool will shrink as the market migrates.

How does this interact with state-level mini-TCPA statutes?

State-level mini-TCPAs in Florida, Oklahoma, Washington, and other jurisdictions create private rights of action and statutory damages for telephone-marketing violations, often under broader definitions of automatic telephone dialing systems than the federal TCPA’s definition under Facebook v. Duguid. The Mandate architecture works at the consent layer rather than the dialing-technology layer, so it is largely independent of how a state defines an ATDS. A Mandate scoped to “contact via methods Y” with Y including any phone or SMS technology authorizes contact under both state and federal regimes, regardless of how the dialing technology is classified. State courts and state AGs will need to take a position on whether a Mandate satisfies the state’s consent requirement; the analysis is similar to the federal-TCPA analysis but may move on a different timeline. Operators with multi-state exposure should prepare state-specific Mandate scope language in addition to the core federal-TCPA-and-card-network scope.

Sources

Tier 1: Primary Protocol and Standards Documentation

-

Google Cloud, “Announcing Agent Payments Protocol (AP2),” Google Cloud Blog, September 2025 – https://cloud.google.com/blog/products/ai-machine-learning/announcing-agents-to-payments-ap2-protocol

-

AP2 Protocol Documentation, “AP2 specification,” accessed April 28, 2026 – https://ap2-protocol.org/specification/

-

AP2 Protocol Documentation, “Partners,” accessed April 28, 2026 – https://ap2-protocol.org/partners/

-

GitHub, “google-agentic-commerce/AP2 Partners,” accessed April 28, 2026 – https://github.com/google-agentic-commerce/AP2/blob/main/docs/partners.md

-

Mastercard, “How Verifiable Intent builds trust in agentic AI commerce,” Mastercard Stories, 2026 – https://www.mastercard.com/us/en/news-and-trends/stories/2026/verifiable-intent.html

-

Mastercard, “Mastercard Agent Pay: secure, scalable and trusted agentic AI,” accessed April 28, 2026 – https://www.mastercard.com/global/en/business/artificial-intelligence/mastercard-agent-pay.html

-

Visa, “Visa Opens the Door to AI-Driven Shopping for Businesses Worldwide,” Visa Investor News, April 8, 2026 – https://investor.visa.com/news/news-details/2026/Visa-Opens-the-Door-to-AI-Driven-Shopping-for-Businesses-Worldwide/default.aspx

-

Visa Developer, “Trusted Agent Protocol,” accessed April 28, 2026 – https://developer.visa.com/capabilities/trusted-agent-protocol

-

Visa, “Visa Introduces Trusted Agent Protocol: An Ecosystem-Led Framework for AI Commerce,” Visa Investor News – https://investor.visa.com/news/news-details/2025/Visa-Introduces-Trusted-Agent-Protocol-An-Ecosystem-Led-Framework-for-AI-Commerce/default.aspx

Tier 2: Established Industry Press and Analysis

-

PYMNTS, “Mastercard Unveils Open Standard to Verify AI Agent Transactions,” 2026 – https://www.pymnts.com/mastercard/2026/mastercard-unveils-open-standard-to-verify-ai-agent-transactions/

-

PYMNTS, “Visa Says Millions of Consumers Will Use Agentic Commerce by Late 2026,” 2025 – https://www.pymnts.com/artificial-intelligence-2/2025/visa-says-millions-of-consumers-will-use-agentic-commerce-by-late-2026/

-

Digital Commerce 360, “Google launches payments protocol for AI commerce, names dozens of partners,” September 19, 2025 – https://www.digitalcommerce360.com/2025/09/19/google-ai-payments-protocol-ap2/

-

Digital Commerce 360, “Mastercard launches ‘agent suite’ for deploying agentic AI,” January 27, 2026 – https://www.digitalcommerce360.com/2026/01/27/mastercard-launches-agent-suite-agentic-ai/

-

FinTech Magazine, “Santander and Mastercard Complete First AI Agent Payment” – https://fintechmagazine.com/news/santander-and-mastercard-complete-first-ai-payment

-

TechAfrica News, “Visa Inc. Launches Intelligent Commerce Connect to Power AI-Driven Payments,” April 22, 2026 – https://techafricanews.com/2026/04/22/visa-inc-launches-intelligent-commerce-connect-to-power-ai-driven-payments/

-

Mastercard Newsroom, “Mastercard accelerates AI-powered commerce with Australia’s first authenticated agentic transactions using Agent Pay,” 2026 – https://www.mastercard.com/news/ap/en/newsroom/press-releases/en/2026/mastercard-accelerates-ai-powered-commerce-with-australia-s-first-authenticated-agentic-transactions-using-agent-pay/

-

PayPal Newsroom, “Mastercard and PayPal Join Forces To Accelerate Secure Global Agentic Commerce,” October 27, 2025 – https://newsroom.paypal-corp.com/2025-10-27-Mastercard-and-PayPal-Join-Forces-To-Accelerate-Secure-Global-Agentic-Commerce

Tier 3: Regulatory and Legal Sources

-

Wiley Rein, “UPDATE: 11th Circuit Vacates FCC’s One-to-One TCPA Consent Rule,” 2025 – https://www.wiley.law/alert-UPDATE-11th-Circuit-Vacates-FCCs-One-to-One-TCPA-Consent-Rule

-

Goodwin, “Eleventh Circuit Deals Fatal Blow to the TCPA’s One-to-One Consent Rule,” January 2025 – https://www.goodwinlaw.com/en/insights/publications/2025/01/alerts-otherindustries-eleventh-circuit-deals-fatal-blow

-

Womble Bond Dickinson, “FCC Repeals One-to-One Consent Rule Following Eleventh Circuit Decision” – https://www.womblebonddickinson.com/us/insights/blogs/fcc-repeals-one-one-consent-rule-following-eleventh-circuit-decision

-

Consumer Financial Services Law Monitor, “FCC’s Final Rule on Consent Kills One-to-One Consent Requirement,” September 2025 – https://www.consumerfinancialserviceslawmonitor.com/2025/09/fccs-final-rule-on-consent-kills-one-to-one-consent-requirement/

-

Debevoise & Plimpton, “The Eleventh Circuit Invalidates TCPA Rules: Lessons for Companies Subject to the TCPA and Administrative Law,” 2025 – https://www.debevoise.com/insights/publications/2025/01/the-eleventh-circuit-invalidates-tcpa-rules

Tier 4: Industry Commentary, Implementation Guides, and Adjacent Coverage

-

Cloud Security Alliance, “Secure Use of the Agent Payments Protocol (AP2): A Framework for Trustworthy AI-Driven Transactions,” October 6, 2025 – https://cloudsecurityalliance.org/blog/2025/10/06/secure-use-of-the-agent-payments-protocol-ap2-a-framework-for-trustworthy-ai-driven-transactions

-

Descope, “What is the Agent Payments Protocol (AP2) and How Does It Work?” – https://www.descope.com/learn/post/ap2

-

Stellagent, “Mastercard Agent Pay Explained: Agentic Tokens and Verifiable Intent for AI Agent Payments (2026)” – https://stellagent.ai/insights/mastercard-agent-pay-agentic-tokens

-

Stellagent, “Visa Intelligent Commerce (VIC) and Trusted Agent Protocol Explained” – https://stellagent.ai/insights/visa-intelligent-commerce-vic-explained

-

Crossmint, “Agentic payments protocols compared: Which is best for your AI agents? (MPP, ACP, AP2, x402)” – https://www.crossmint.com/learn/agentic-payments-protocols-compared

-

PR Newswire, “MetaComp launches the world’s first AI agent governance framework for regulated financial services,” April 22, 2026 – https://www.prnewswire.com/apac/news-releases/metacomp-launches-the-worlds-first-ai-agent-governance-framework-for-regulated-financial-services-302749713.html

-

Blockhead, “Singapore’s MetaComp Rolls Out AI Agent Governance Framework for Financial Institutions, Regulators,” April 21, 2026 – https://www.blockhead.co/2026/04/21/singapores-metacomp-rolls-out-ai-agent-governance-framework-for-financial-institutions-regulators/

-

Visa, “Visa and Partners Complete Secure AI Transactions, Setting the Stage for Mainstream Adoption in 2026” – https://usa.visa.com/about-visa/newsroom/press-releases.releaseId.21961.html

Closing

The story of April 2026 will be told several ways. The payments industry will tell it as the moment agentic commerce went from pilot to production across both major U.S. card networks. The protocol-design community will tell it as the moment AP2 won the de facto standard war for AI agent authorization. The regulated-finance community will tell it as the moment Know Your Agent became a real compliance requirement. None of those framings is wrong. None of them captures the most consequential thing that happened. The Mandate – the cryptographically signed Verifiable Credential at the heart of AP2, accepted on Mastercard rails as Verifiable Intent and on Visa rails through Intelligent Commerce Connect – became, in the space of three weeks, the first artifact that can support evidence simultaneously across the user-delegation, payment-authorization, marketing-consent, GDPR-purpose-limitation, state-privacy-law, and buyer-contract-acceptance categories that lead-generation compliance officers have been documenting separately for a decade. It is signed, written, prior, express, scoped, portable, tamper-evident, and machine-verifiable. It can support evidence consistent with the Eleventh Circuit’s plain-meaning reading of TCPA prior express written consent, alongside (not instead of) existing TrustedForm and Jornaya-style certificates. It can support evidence consistent with GDPR Article 5(1)(b) purpose limitation. It can support evidence consistent with card-network cardholder authorization. The regulators have not yet caught up. The courts have not yet ruled. The first cases are coming. The buyers who arrive at those cases with Mandate-validation capability, scope-aware waterfalls, and a coordinated industry-engagement position will set the precedent. The buyers who arrive without will be the precedent. The decision is whether to preserve evidence now or defend missing evidence later.

Protocol specifications, payment service provider integrations, and regulatory developments reflect publicly reported conditions through April 28, 2026. AP2, Mastercard Verifiable Intent, Visa Intelligent Commerce Connect, and related agentic-commerce frameworks are evolving rapidly; verify current specifications and acceptance status through primary sources before making compliance or operational decisions. This article provides general industry analysis and does not constitute legal, financial, or compliance advice. Consult qualified counsel for specific compliance questions related to TCPA prior express written consent, GDPR purpose limitation, card-network cardholder authorization, or the interaction among these regimes.