Progressive’s mid-April 2026 print is the cleanest read on auto direct-acquisition unit economics in years. Revenue of $22.2 billion, net income of $2.8 billion, EPS of $4.80, net premiums written up 6% to $23.6 billion, net premiums earned up 8% to $21.0 billion, a combined ratio of 86.4, and 39.6 million policies in force – up 9% year over year from 36.3 million. The same week, the MBA’s April refinance wave delivered a parallel signal on the mortgage side, framing the Q2 2026 carrier-direct-plus-refi window as a coordinated rerate moment for both auto and home lead-buyer operations. The auto-lead aggregator question that print just answered is no longer whether 2026 pricing compresses. It is by how much, and on what timeline.

Progressive’s Q1 2026 Print Sets the Auto-Acquisition Floor

On the morning of its mid-April 2026 release, Progressive Corporation reported a quarter that, on the income statement, looked like a continuation of the cycle the company had been running since late 2023. Revenue grew to $22.2 billion. Net income reached $2.8 billion, with diluted earnings per share of $4.80, up roughly ten percent year over year. Net premiums written rose six percent to $23.6 billion. Net premiums earned rose eight percent to $21.0 billion. The combined ratio printed at 86.4, a forty-basis-point uptick from the 86.0 a year earlier but still firmly in territory that most personal-lines underwriters would call structurally profitable.

The line that mattered for the lead-generation industry was lower in the release. Policies in force reached 39.6 million, up nine percent year over year from 36.3 million. That is roughly 3.3 million net new active auto and property policies on the books in twelve months at a single carrier – a unit count larger than the entire policyholder base of several mid-sized national insurers and acquired against a backdrop in which most of Progressive’s direct competitors were still recovering from the 2022-2023 loss-cost shock that had pushed combined ratios into triple digits across the personal auto line.

For most readers, this read as a strong-quarter story. For auto-insurance lead aggregators, brokers running carrier panels, and the performance-marketing teams sitting on the carrier side of the table, it read as something else: confirmation that the carrier-direct bid is no longer cyclically depressed, no longer waiting for loss-cost normalization, no longer constrained by the underwriting losses that had kept Progressive, GEICO, and Allstate out of the most aggressive Google and Meta auctions through 2023. Progressive is now growing policy count at nine percent annually while running an underwriting margin north of thirteen points. It has both the cash and the strategic mandate to outbid third-party aggregators in the same auctions every aggregator competes in. Allstate’s Q1 2026 earnings call on April 30 will provide the second carrier read; the disclosure expected from Berkshire Hathaway’s 10-Q a week later will provide the third. None is likely to look meaningfully different in shape, even if the magnitude varies.

This analysis covers what the print signals about the carrier-direct acquisition floor, why aggregator margin compression in 2026 is structural rather than cyclical, how the bid pressure flows through the auto-insurance lead generation funnel, and what aggregators, agents, and lead operators should be doing in the next sixty days to reprice contracts before the carrier-direct floor sets.

What the Q1 2026 Numbers Actually Say About Carrier Acquisition Capacity

The headline numbers are the income-statement summary. The acquisition-capacity story is in the way those numbers fit together.

A combined ratio of 86.4 means that for every dollar of premium Progressive earned in the quarter, it paid roughly 64 cents in claims and loss-adjustment expense and 22 cents in underwriting expense, leaving 13.6 cents of underwriting profit. Applied to net premiums earned of $21.0 billion, that produces approximately $2.86 billion in pre-tax underwriting profit for the quarter – enough by itself to fund the entire $2.8 billion of consolidated net income, with investment income providing additional cushion. For a personal-lines insurer, this is the structural profile that allows acquisition spend to be funded out of operating cash flow rather than out of capital reserves. It is also the profile that allows a board to authorize incremental marketing spend without triggering rating-agency questions about underwriting discipline.

Compare that to the early-2023 baseline. In 2022 and into 2023, Progressive ran combined ratios in the 95-to-99 range as loss costs spiked on used-vehicle parts and labor inflation. Through that period, the company explicitly throttled marketing spend to preserve underwriting margin. The most-cited operational tactic was to reduce paid-search bids on prospect cohorts that did not meet a tightened risk threshold and to shift acquisition focus toward existing-customer cross-sell. The result was a slowdown in policy-count growth and a temporary opening for non-carrier auto-lead aggregators to capture share at the top of the funnel.

That window has closed. The Q1 2026 print confirms it. With combined ratios back below 87, Progressive is running the inverse playbook: aggressive acquisition spend funded by underwriting profitability, with the explicit goal of compounding the policy-in-force base while loss costs remain stable. The nine percent year-over-year policy growth rate is not an accident or a one-quarter pull-forward. It is the visible output of a multi-quarter acquisition program that has been ramping since late 2024 and is now hitting full operational scale.

The marketing spend disclosure that matters

Progressive’s exact Q1 2026 marketing spend will appear in the 10-Q filed within forty-five days of the earnings release. Historical quarterly disclosures have placed the company’s advertising and marketing expense in the range of $700 million to $900 million per quarter during periods of aggressive acquisition, dropping to $500 million or below during throttle periods. A return to the $800 million-plus quarterly tier – which the Q1 2026 policy growth rate strongly implies – would represent annualized marketing spend approaching $3.5 billion at a single carrier.

For context, the entire publicly traded auto-lead aggregator segment – including the auto-insurance components of LendingTree’s marketplace, MediaAlpha’s property-and-casualty business, EverQuote’s auto vertical, and QuinStreet’s insurance segment – runs at a combined revenue base of approximately $1.5 to $2.0 billion annually, of which a portion flows through to carrier customers as media spend on behalf of agent buyers rather than directly into the open paid-search auctions. The single-carrier marketing budget Progressive is operationalizing in 2026 is materially larger than the entire aggregator-channel revenue base it competes against.

That asymmetry can make the carrier-direct bid a structural floor on aggregator pricing – if Progressive’s incremental direct-acquisition capacity is redeployed into the same Google, Meta, and broadcast auction pools that aggregators bid into. The conditional matters: if Progressive routes its incremental marketing spend into channels where aggregators do not compete (broadcast, owned-property funnels, partner programs), the auction-floor effect is muted. Where the budgets do overlap, aggregators bidding into the same pools face a counterparty whose bid clears at a higher CPC than the aggregator can profitably pay given downstream per-lead pricing constraints, and the aggregator either accepts thinner margin, retreats to lower-funnel inventory, or exits the auction. None of those options expand aggregator margin. The size of the compression depends on how much of Progressive’s spend lands in the shared pools.

Why the carrier-direct bid sets a floor, not a fluctuation

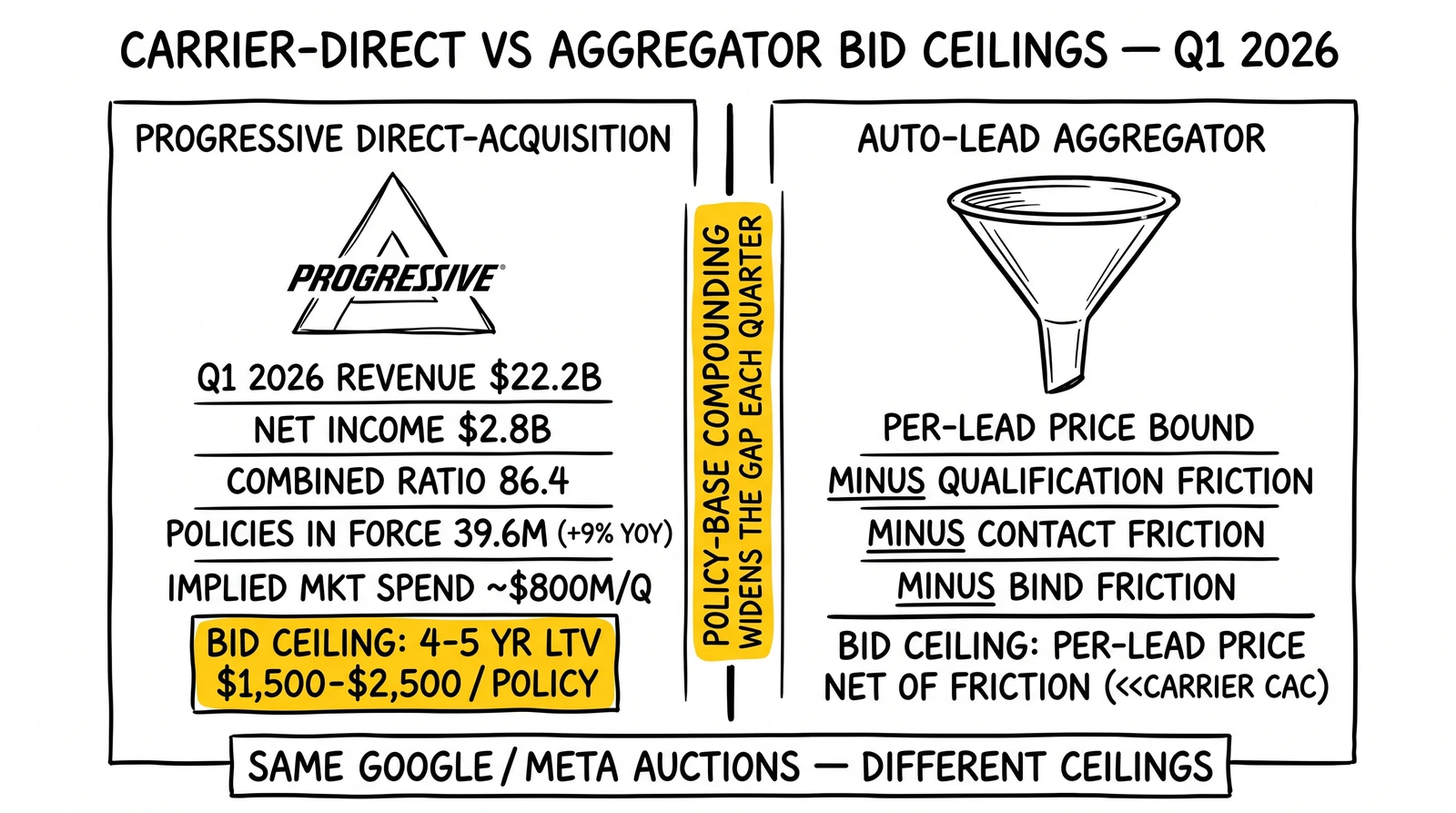

A useful way to think about the bid dynamic: Progressive’s per-policy customer acquisition cost is bounded above by the present value of underwriting margin on a multi-year retained policyholder. At a current six-month average premium in the high four-figures and a multi-year retention curve, a typical Progressive auto policy generates roughly $1,500 to $2,500 in lifetime underwriting margin over a four-to-five-year retention horizon. That ceiling on acquisition cost is what the carrier-direct bid is anchored to.

An auto-lead aggregator’s per-policy economics work in the opposite direction. The aggregator captures a prospect at a paid-media cost, qualifies and routes that prospect to a carrier or agent buyer, and earns a per-lead, per-call, or per-click fee. The aggregator’s bid into the same paid-media auction is bounded above by the per-lead price the carrier will pay, minus the conversion friction (qualification rate, contact rate, bind rate) that compounds along the way. When carrier-direct teams are themselves the dominant bidder in the auction, the per-lead price the aggregator can charge is competing against the carrier’s own internal cost-per-policy benchmark – and the aggregator carries the conversion friction the carrier does not.

The arithmetic is unforgiving. If a carrier can acquire a policyholder directly at $400 in marketing cost, the carrier will pay an aggregator only what the aggregator can deliver below that internal benchmark net of conversion friction. As the carrier’s direct-acquisition efficiency improves – and Q1 2026 says it is improving – the per-lead price the aggregator can sustainably charge falls. This is the structural compression that the Progressive print formalizes.

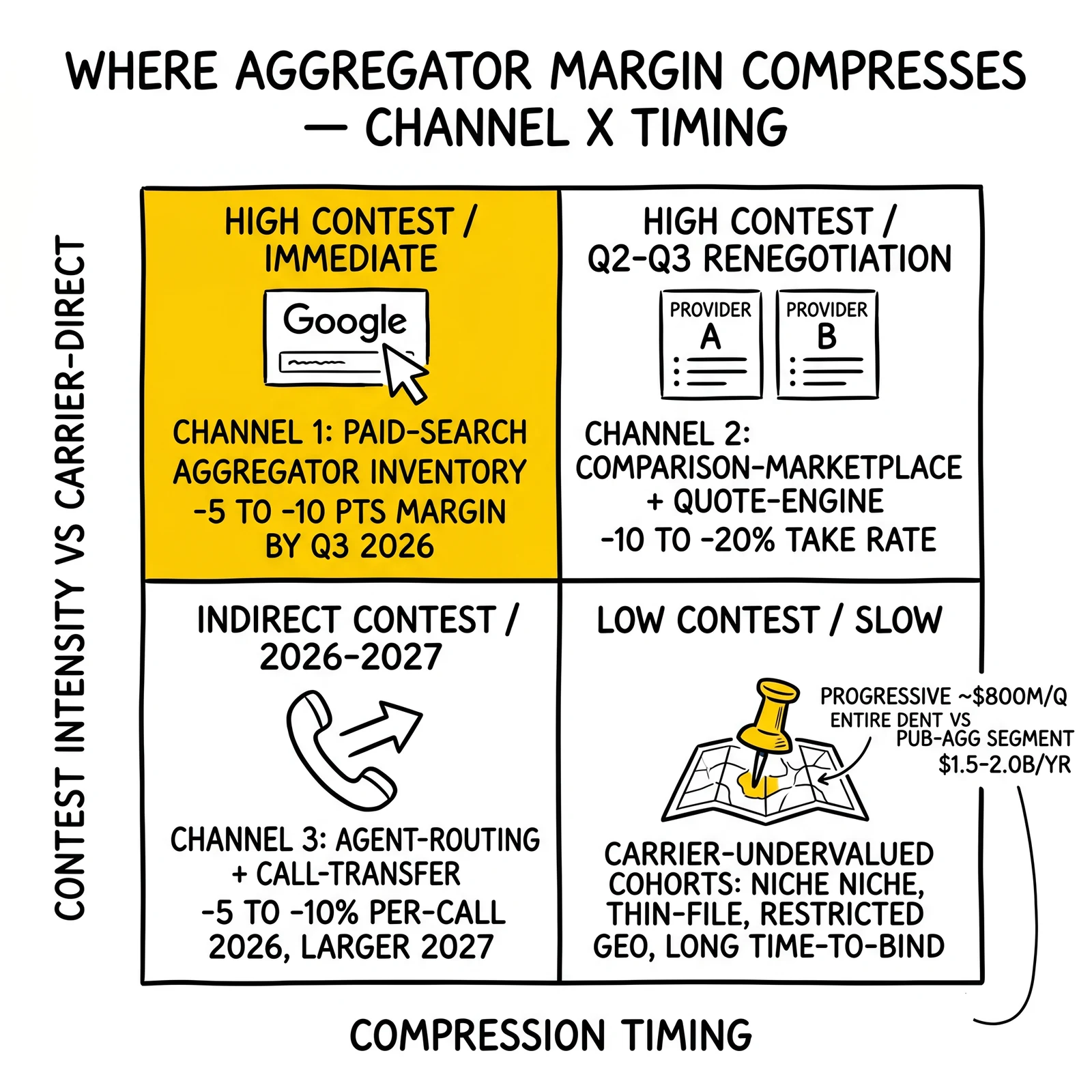

The Three Channels Where Aggregator Margin Will Compress First

The compression will not arrive evenly across the auto-lead-aggregator stack. Three distinct channels carry different exposure profiles, and the operators paying attention to which channel they are most concentrated in will weather the next six quarters with very different P&L outcomes.

Channel one: paid-search and paid-social aggregator inventory

The most directly exposed channel is the keyword-driven, paid-search-funded aggregator inventory that competes head-to-head with carrier-direct bids in the Google and Meta auctions. Aggregators in this segment typically capture prospects at $25 to $60 in paid-media cost, qualify the prospect through an online form or short flow, and sell the resulting lead at $12 to $25 for shared inventory or $30 to $80 for exclusive inventory. The margin between media cost and lead price is the operator’s contribution.

When Progressive’s direct-acquisition team raises its CPC bids on the same keyword set – “auto insurance quote,” “cheap car insurance,” “car insurance comparison,” and the long tail around them – the aggregator either pays more for the same prospect (compressing margin) or accepts a lower position (compressing volume). Both outcomes hit P&L. The compression is most acute on high-intent commercial keywords where the carrier’s expected lifetime value justifies a CPC the aggregator cannot match.

The defensive move available to aggregators in this channel is to shift inventory mix toward keywords and audiences where the carrier-direct ROI is structurally lower – typically high-funnel content keywords, demographic-targeted social audiences without strong commercial intent signals, and aged-search-arbitrage cohorts that carriers prefer to avoid. The trade-off is lower contact rates and lower bind rates on the resulting leads, which pushes per-lead pricing down on the buyer side. The math works for some operators; the math does not work for many. By Q3 2026, the operators who have not made the inventory-mix shift will be running margin profiles that are five to ten points thinner than they entered the year with.

Channel two: comparison-marketplace and quote-engine inventory

The second exposure profile sits in the comparison-marketplace tier – the LendingTree-style quote-comparison flows where consumers enter information once and receive offers from multiple carriers. The structural question for these operators is whether carriers continue to participate as panel members or pull bids in favor of direct-acquisition channels.

Progressive’s relationship with comparison marketplaces has historically been selective. The company has participated in some quote-comparison flows when the marketplace economics produced a per-policy acquisition cost competitive with Progressive’s own direct channels and has pulled out when they did not. The Q1 2026 print does not change Progressive’s policy in either direction; it changes the marketplace’s negotiating leverage. With Progressive’s direct-acquisition machine running at full scale, the marketplace cannot credibly threaten to send Progressive’s panel slot to a competitor – the competitor’s own direct-acquisition economics are likely improving in parallel, and no carrier wants to pay marketplace economics if the direct channel is converting at parity.

The result is that comparison marketplaces are likely to face a Q2-Q3 2026 round of bid renegotiation in which carrier panel participation is contingent on lower marketplace take rates or higher carrier-favorable filter routing. Aggregators who run comparison-marketplace inventory should expect the take rate per converted policy to compress by ten to twenty percent through the back half of the year, with the steepest compression on prospect cohorts the carrier values most.

Channel three: agent-routing and call-transfer inventory

The third exposure profile is the agent-routing and call-transfer tier – the inventory that flows to independent agents and captive-agent organizations rather than to carrier-direct teams. This channel is the most structurally insulated from the Progressive print, because the carrier-direct bid does not directly contest the agent-channel inventory in the same way it contests the carrier-direct keyword set. Agents pay for leads and calls that produce policies they are licensed to place across multiple carriers, and the agent’s per-policy economics are different from a carrier’s because they include carrier appointments, commission residuals, and renewal-book value.

That said, the agent channel is not immune. The pressure arrives indirectly: when carrier-direct acquisition efficiency improves, carriers pull volume away from the agent channel by increasing direct quote conversion, which depresses agent volume and the per-call pricing agents are willing to support. The compression is slower and milder than in the paid-search-aggregator channel, but it is real. Operators concentrated in call-transfer inventory routed to insurance call centers should expect per-call pricing to compress by five to ten percent through 2026, with the larger impact arriving in 2027 as carrier-direct programs mature.

The pattern across all three channels: the compression is not a single event but a multi-quarter slope, and the slope steepens through the back half of 2026 as the carrier-direct programs that the Q1 print confirms are now hitting full operational scale.

Why This Compression Is Structural, Not Cyclical

The temptation, when reading a single carrier’s quarterly print, is to interpret the underlying pressure as cyclical – a feature of the current loss-cost environment that will reverse when the next loss-cost shock hits and combined ratios climb again. That framing is wrong, and the wrongness matters operationally.

The 2026 environment is not the 2022-2023 environment

Through 2022 and 2023, the auto-insurance industry ran combined ratios in the 95-to-105 range as parts inflation, labor cost growth, and severity escalation outran the rate-filing cycle. Carriers responded by tightening underwriting, throttling acquisition spend, and absorbing share loss in the agent and aggregator channels. The cycle reversed when rate filings caught up and loss costs stabilized; by mid-2024, combined ratios had returned to profitable territory at most major carriers. The Q1 2026 print confirms that the recovery has compounded into a sustained period of underwriting profitability.

What is different about the current cycle versus prior recoveries is that the post-2024 carrier acquisition infrastructure is materially more sophisticated than the infrastructure that exited the 2008-2010 recovery or the 2017-2019 recovery. Progressive’s bidding stack, in particular, has been described in industry coverage as integrating real-time underwriting risk signals with paid-media bid logic at a granularity that allows the company to bid asymmetrically on high-quality prospect cohorts and bid down on cohorts that fail underwriting filters. GEICO has reportedly built comparable infrastructure, and Allstate has been investing heavily in direct-channel build since its 2022 strategic review.

The implication: when the next loss-cost shock arrives – whether driven by parts inflation, severity, fraud, or a regulatory event – carriers will throttle acquisition more selectively than they did in 2022-2023. They will continue bidding aggressively on the cohorts the underwriting model favors and pull bids only on the cohorts that fail the filter. Aggregators competing against this behavior will not get the same broad reprieve they got during prior cycles. The competitive floor has been raised structurally, and prior cycles understated the floor because the carrier infrastructure was less capable.

The policyholder-base compounding effect

A second structural factor is the compounding mechanic of policy-in-force growth. Progressive added approximately 3.3 million net policies in twelve months. At a multi-year retention curve, that 3.3 million-policy increment generates two adjacent benefits the carrier can plow back into acquisition: incremental renewal premium that funds further marketing spend, and a larger denominator against which to spread fixed acquisition technology costs. Both benefits compound. By Q1 2027, the policy-in-force base will be larger again, and the per-policy fixed-cost denominator will be larger again, which will make Progressive’s per-policy acquisition economics more favorable than they are today.

The compounding mechanic is asymmetric. Aggregators do not share in the renewal-premium tailwind – they earn revenue on the initial lead transaction, not on the multi-year retention curve. The aggregator’s per-lead economics are static. The carrier’s per-policy economics are dynamic and improving. Over a multi-quarter horizon, the gap between the carrier’s bid ceiling and the aggregator’s bid ceiling widens.

This is the structural pattern behind the framing that 2026 aggregator margin compression is not a cyclical feature. It is a multi-quarter compounding of carrier-direct economic advantages that the prior cycle masked.

What would actually reverse the compression

A genuinely cyclical reversal would require one of three conditions: a loss-cost shock large enough to push combined ratios above 100 across the major carriers, a regulatory action that constrains carrier-direct paid-media activity (improbable in the U.S. regulatory environment), or a shift in consumer search behavior away from carrier-branded queries toward comparison-shopping queries that aggregators are better positioned to capture. None of these conditions is the central case for 2026 or 2027. The first is possible but unlikely given the current rate-filing environment. The second is unlikely. The third is a possibility but operates on a multi-year timeline.

The operational conclusion: aggregators planning around the assumption that 2026 compression reverses in 2027 are planning around the wrong base case. The realistic base case is that compression continues through 2027 and stabilizes only when carrier-direct acquisition programs have reached saturation in the highest-value prospect cohorts – which industry analysts generally place in 2028 or later.

The Approaches That Will Underperform This Cycle

Three responses to the Progressive print are visible in early industry commentary. Each will produce worse outcomes than its proponents expect, and the reasons are worth being explicit about.

The first is the wait-and-watch posture. The argument runs that Progressive is one carrier, that Allstate’s print on April 30 may show a different shape, that GEICO’s Berkshire-disclosed numbers may show throttle, and that the broader industry signal will not be clear until the full Q1 cycle reports out. Until then, the wait-and-watch operator continues running existing pricing, existing buyer panels, and existing inventory mix. The problem is that the carrier-direct bid pressure is already in market. The Google and Meta auctions reflect carrier bid activity in real time, not on quarterly-earnings cadence. By the time the full Q1 cycle has reported and the shape is unambiguous, the operators who waited will have absorbed two months of compressed-margin transactions at unchanged contractual pricing – which is the worst possible asymmetry, because the operator carries the cost change without having repriced the buyer side.

The second is the volume-recovery posture. The argument is that the right defensive response to per-lead margin compression is to push volume higher to maintain absolute contribution dollars. This logic is intuitive but operationally wrong. Pushing volume into the same auctions where carrier-direct bids are tightening means the operator’s average paid-media cost per prospect rises faster than per-lead price holds, which compresses margin per lead at exactly the moment the operator is taking on more leads. The result is more revenue, less profit, and a working-capital problem if buyer payment terms lag media-spend payment terms – which they almost always do. The operators who tried this playbook in 2018-2019 during an earlier carrier-direct ramp ended the cycle with worse P&L than the operators who held volume flat and shifted mix.

The third is the carrier-pivot posture. The argument is that if carrier-direct is squeezing the aggregator channel, the right response is to pivot toward selling directly to carriers as a managed-service media partner rather than as a per-lead vendor. This is sometimes a legitimate strategic move for an operator with the right relationships and infrastructure, but it is a category change rather than a tactical fix. The operators executing this pivot in 2026 are the same operators who started building carrier-direct partnerships in 2023-2024, when the relationships could be established at lower competitive intensity. Operators starting the pivot now will find that the carrier-direct teams they are pitching are the same teams they have spent the past three years competing against, which makes the partnership conversation structurally harder.

The common pattern: each posture underestimates the speed of the compression and overestimates the operator’s options for absorbing or deflecting it. The realistic posture is to assume the compression is real, immediate, and structural – and to design contractual and operational responses accordingly.

The Strategic Reframe: Three Principles for Aggregators in the Compressed Environment

The right response to the Q1 print starts from a different premise. The carrier-direct bid is now the dominant force in the auto-acquisition auction stack, and aggregator strategy should be designed around that reality rather than around the prior assumption that aggregators set the per-lead price and carriers paid it. Three principles flow from that premise.

Principle one: reprice contracts on a quarterly rather than annual cadence

The legacy auto-lead aggregator contract typically runs on an annual pricing schedule with quarterly volume true-ups. That cadence was viable when carrier-direct bid pressure moved on a multi-year cycle. It is no longer viable when the underlying pressure shifts quarter-to-quarter as carrier-direct programs scale.

The repricing move available to aggregators is to renegotiate buyer contracts on a quarterly cadence with carrier-bid-indexed pricing – that is, contracts in which the per-lead price moves with a published index of carrier-direct CPC activity in the relevant geo-product segment. The carrier customer accepts indexed pricing because it aligns the aggregator’s per-lead price with the carrier’s own internal benchmark; the aggregator accepts indexed pricing because it transfers the bid-pressure risk back to the buyer rather than absorbing it on the supply side.

The build is non-trivial. It requires an indexing methodology that both sides will accept, a data source the index can reference (third-party CPC data, the aggregator’s own auction-loss reporting, or a hybrid), and contractual language that handles edge cases. Aggregators who completed this contractual rework in late 2024 or early 2025 are running 2026 with substantially better margin protection than aggregators who are still on annual pricing schedules. Aggregators who start the work now will have completed contracts in place for Q3 2026 – in time to absorb the second-half compression rather than pay it.

Principle two: shift inventory mix toward conversion-quality dimensions carriers undervalue

The carrier-direct bid is most aggressive on prospect cohorts where the carrier’s lifetime-value model produces a high expected return. The bid is less aggressive on cohorts where the lifetime-value model produces lower returns – typically thin-file consumers, prospects in geographies where the carrier’s underwriting filter is restrictive, prospects with vehicle profiles outside the carrier’s preferred mix, and prospects whose conversion-velocity profile suggests longer time-to-bind.

For aggregators, the corresponding shift is to capture and qualify prospects on dimensions the carrier-direct channel undervalues. The most effective dimensions are conversion-velocity-related: prospects who shop multiple carriers, prospects who request callbacks at specific times, prospects whose data signals indicate proximity-to-renewal rather than spontaneous shopping, and prospects in aged-lead segments that carry lower acquisition cost on the supply side and have specific conversion patterns that direct-acquisition models do not optimize for.

The trade-off is that aggregators shifting toward these segments take on more complex qualification logic and longer prospect-to-bind cycles, which requires investment in funnel infrastructure. The investment is justifiable when the alternative is competing head-to-head on the carrier-favored cohorts at compressed margins. Operators who complete the inventory-mix shift in 2026 enter 2027 running a fundamentally different competitive position than operators who do not.

Principle three: monetize the data layer, not just the lead transaction

The legacy aggregator business model monetizes a single transaction – the per-lead, per-call, or per-click sale to a buyer. The data the aggregator captures during qualification (prospect demographics, vehicle profile, current carrier, shopping behavior, conversion-velocity signals) is treated as input to the lead transaction, not as an independent revenue stream. In the compressed environment, this monetization model leaves significant value on the table.

The reframe is to treat the data layer as a parallel revenue stream. Carriers building direct-acquisition models are constantly investing in data inputs that improve their bid logic – third-party demographic data, vehicle-history data, telematics signals, retention-model inputs. Aggregators sitting on years of prospect-shopping data have an asset that some carriers will pay for as a model input even when they decline to buy the underlying leads. The monetization is typically structured as a data-licensing or model-services arrangement rather than a per-lead transaction.

The build requires a data-governance posture (consent, retention, deidentification) that most aggregators have not formalized at the level a carrier data-procurement function will require. The build requires investment in data-product packaging – specifically, packaging the data in a form a carrier’s analytics team can ingest into existing modeling infrastructure. And the build requires sales-and-relationship work with carrier data-procurement teams, which is a different sales motion than the per-lead-buyer relationship most aggregators are organized around. Operators completing this pivot are constructing a revenue stream that compresses less than the per-lead stream because it competes on data quality rather than on auction-bid economics.

The combined effect of the three principles is to reposition the aggregator from a per-lead seller competing on auction economics to a hybrid model in which contracts are bid-indexed, inventory is differentiated against the carrier-favored cohorts, and a data-licensing layer captures value the per-lead transaction cannot. The repositioning is structurally more durable than the current model, and the operators completing it in 2026 will be the operators with the strongest 2027 P&L.

Evidence from the Carrier Comparables: Allstate, GEICO, State Farm

Progressive is the cleanest read on the Q1 2026 acquisition environment because its earnings cadence and disclosure practice produce the timeliest, most granular data. The other three top-five U.S. auto carriers each tell a piece of the same story with different emphasis.

Allstate’s April 30 print and the property-casualty rebalance

Allstate’s Q1 2026 earnings call is scheduled for April 30, 2026 per the company’s newsroom announcement. The market will be reading the print for two specific signals: combined-ratio trajectory in the auto segment, and the marketing-spend disclosure that shapes the implied direct-acquisition velocity. Allstate has been more transparent than Progressive about its direct-channel ramp through 2024-2025, having explicitly described the strategic shift from a captive-agent-dominant model toward a more balanced direct-and-agent model in successive 10-K disclosures.

The implication for aggregators is that the Allstate print is likely to confirm the same direction Progressive has shown – accelerating direct-acquisition spend funded by an underwriting-margin recovery – even if the magnitude differs. Aggregators routing leads to Allstate’s agent channel will face the cross-pressure described above: a carrier increasing its direct-channel investment while continuing to receive agent-channel volume, with the per-lead and per-call pricing tier on the agent side compressing as the direct channel proves out.

The reading exercise is to pair the April 30 print with Progressive’s Q1 print and look at the combined acquisition-spend signal at the two carriers, which together account for a large share of the personal auto direct-channel competitive intensity. If both carriers are increasing direct-spend at double-digit year-over-year rates, the auction pressure on aggregators is materially stronger than if either alone were doing so. Early indicators suggest both are.

GEICO and the Berkshire disclosure timing

GEICO’s underwriting and marketing-spend data appears in Berkshire Hathaway’s quarterly 10-Q rather than as a standalone earnings call. The Q1 2026 10-Q is expected within forty-five days of quarter-end, placing the GEICO disclosure in mid-May. GEICO’s direct-channel posture through the 2022-2023 cycle was the most disciplined of the major direct carriers – the company explicitly throttled marketing spend to defend underwriting margin and accepted multi-year share loss as the trade-off. The recovery posture has been more measured than Progressive’s; GEICO has been ramping marketing spend gradually rather than aggressively.

For aggregators, GEICO’s gradual ramp is a partial offset to the Progressive acceleration. GEICO does not contest the Google and Meta auction inventory at the same intensity Progressive does, which leaves more inventory at clearable CPCs for non-Progressive bidders. The offset is partial because GEICO’s gradual ramp is still upward-sloping and because Progressive’s acceleration is large enough on its own to set the auction floor in many segments. But the GEICO posture is the reason the compression is steep rather than catastrophic – a fully aggressive ramp at GEICO matched to Progressive would produce materially worse aggregator P&L outcomes than the current configuration.

State Farm and the captive-agent insulation

State Farm remains the largest U.S. personal-lines auto insurer by direct premiums written, but its acquisition activity is concentrated in the captive-agent channel rather than in the direct-channel auctions Progressive and GEICO contest. State Farm’s marketing spend disclosed in NAIC filings supports brand and agent-channel acquisition rather than direct paid-search activity. The company’s underwriting recovery has tracked the broader cycle, and State Farm’s combined ratios have returned to profitable territory along with the rest of the industry.

The implication is that State Farm contributes less direct auction pressure than Progressive or GEICO, but the company’s captive-agent presence shapes the agent-channel-pricing environment in ways that affect aggregators routing leads to independent agents who compete against State Farm captives in local markets. The pressure flows through the buyer side rather than the supply side: agents competing against State Farm captives have less pricing flexibility on the buyer side of the aggregator transaction, which compresses the per-lead price aggregators can charge agent buyers.

The carrier-comparable picture, taken together: Progressive is the auction-pressure leader, Allstate is the close-second confirming the directional signal, GEICO is the moderating presence whose gradual ramp keeps compression from being catastrophic, and State Farm contributes pressure through the captive-channel-versus-independent-agent dynamic rather than direct auctions. Aggregator strategy that accounts for all four signals is more resilient than strategy that reads only the headline Progressive number.

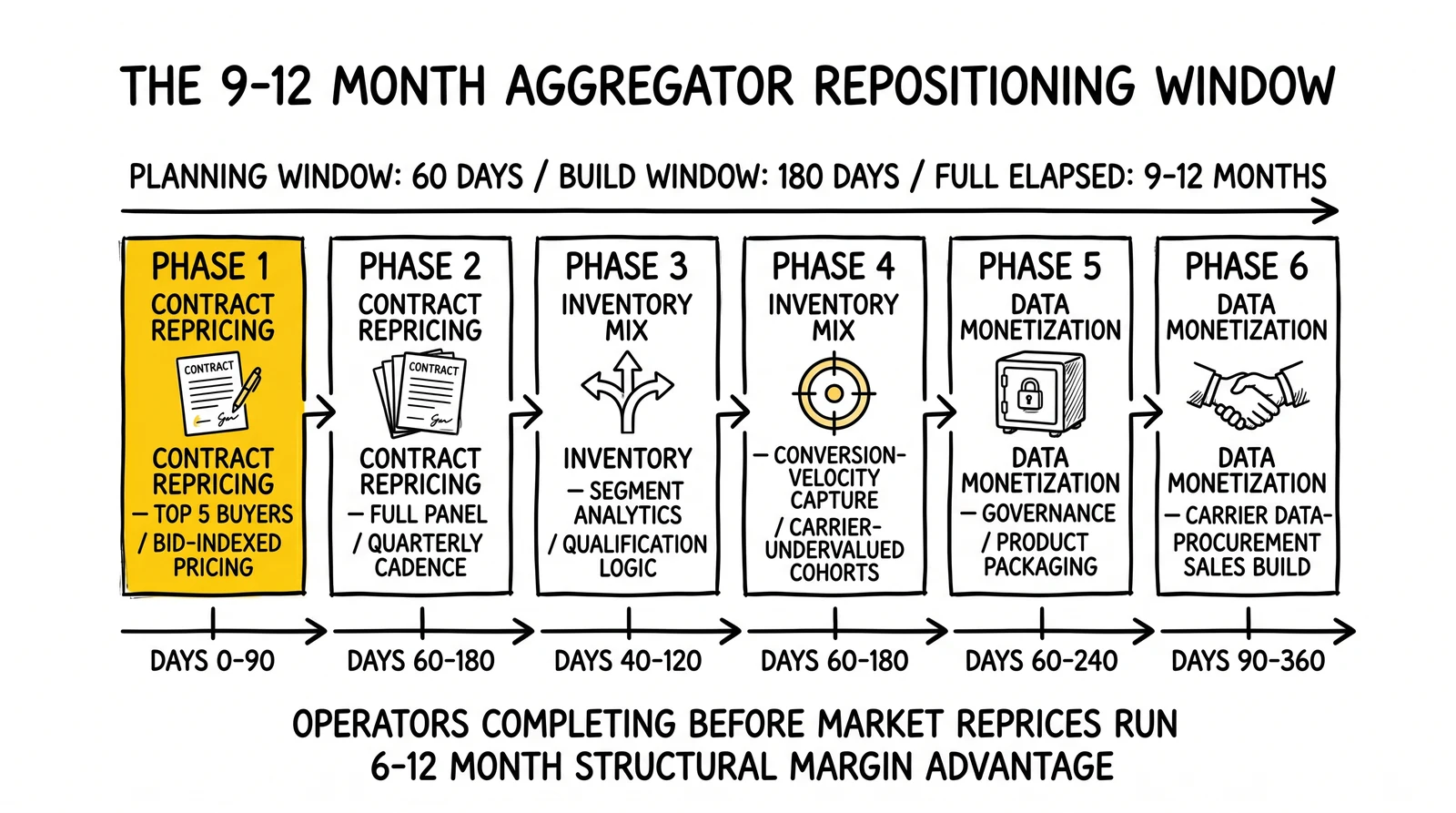

Implementation Reality: What It Actually Takes to Reprice

The strategic reframe is straightforward. The implementation is not.

Resource requirements

The contractual repricing work is primarily legal-and-business-development effort rather than engineering effort, but it is non-trivial. Renegotiating buyer contracts to bid-indexed pricing typically requires sixty to one hundred and twenty days per buyer relationship, depending on the buyer’s contracting cycle and procurement process. Aggregators with twenty to fifty buyer relationships should plan a six-to-nine-month total renegotiation cycle, with the largest buyers prioritized first. The legal work – drafting indexing language, defining the index data source, defining edge-case handling – is typically thirty to sixty days of outside counsel time on the aggregator side and a comparable cycle on the buyer side. Aggregators who try to renegotiate without specialized contracting counsel typically end up with weaker indexing language than the comparable aggregator who invests in the legal work.

The inventory-mix-shift work is engineering and analytics effort. Building the qualification logic that captures conversion-velocity dimensions and routes prospects toward buyer profiles that value those dimensions is a sixty-to-one-hundred-twenty engineering-day project for an aggregator on a modern lead-distribution stack and longer for an aggregator on legacy infrastructure. The analytics work – building the reporting that lets the operator see which inventory segments are compressing fastest and adjust mix in response – is a parallel forty-to-eighty-day project. The combined effort is typically a four-to-six-month build with phased rollout.

The data-monetization build is the largest of the three projects. It requires a data-governance pass (consent, retention, deidentification), a data-product packaging effort (defining the data products carriers will buy, building the delivery infrastructure), and a sales-team build (hiring or repurposing sales staff to call on carrier data-procurement teams rather than carrier or agent media-buyer teams). The full build is typically a nine-to-twelve-month project with substantial up-front investment before the first revenue contract closes.

Timeline expectations

A realistic implementation timeline for a mid-sized auto-lead aggregator working on all three principles in parallel:

| Phase | Duration | Key Activities |

|---|---|---|

| Contract repricing – top buyers | 60–90 days | Renegotiate top 5 buyer contracts to quarterly cadence with bid-indexed pricing |

| Contract repricing – full panel | 120–180 days | Roll bid-indexed pricing across remaining 15-45 buyer relationships |

| Inventory-mix shift – analytics | 40–80 days | Build segment-level reporting that exposes compression by inventory type |

| Inventory-mix shift – qualification logic | 60–120 days | Implement conversion-velocity capture and routing to carrier-undervalued cohorts |

| Data-monetization – governance | 60–90 days | Consent, retention, deidentification framework |

| Data-monetization – product packaging | 90–150 days | Define data products, build delivery infrastructure |

| Data-monetization – sales build | 90–180 days | Hire data-procurement-facing sales; first carrier conversations |

| Total elapsed time | 9–12 months | Conservative for an aggregator without prior data-licensing motion |

Source: Composite of industry implementation patterns and analysis of carrier-direct competitive timeline

Common obstacles

Three obstacles consistently slow these implementations beyond the nominal timeline. The first is buyer resistance to indexed pricing. Buyers – especially carrier-direct customers – prefer fixed pricing because it simplifies their internal forecasting and budget allocation. The aggregator’s leverage to push indexed pricing depends on the strength of the buyer relationship and the buyer’s perception of the aggregator’s alternative options. Aggregators with strong buyer concentration (top three buyers more than fifty percent of revenue) typically have weaker leverage and complete the renegotiation more slowly than aggregators with diversified buyer panels.

The second is the carrier-direct internal politics around data partnerships. Carrier data-procurement teams are typically separate from media-buying teams, and the aggregator’s relationship with the carrier may be entirely on the media-buying side – which means the data partnership conversation requires opening a new internal door at the carrier. The opening sometimes goes well; sometimes the data team is reluctant to engage with a vendor whose primary product is leads the carrier may not be buying at the moment. Aggregators typically need three-to-five carrier data conversations to close one contract.

The third is the engineering-resource competition. The qualification-logic and analytics build for inventory-mix shift competes with other engineering priorities, and aggregators running on stretched engineering teams typically extend the build timeline by twenty-five to fifty percent. Operators who allocate dedicated headcount to the project complete it faster than operators who try to run it as side work alongside other roadmap items.

The implementation is hard. The operators who complete it before the rest of the market reprices will run a six-to-twelve-month structural margin advantage as the carrier-direct compression continues.

Future Implications: The Multi-Year Trajectory of Auto-Lead Pricing

The Q1 2026 print is the first event in a multi-quarter sequence. The shape of the sequence is reasonably predictable from the structure of the market.

In the next twelve months, expect the carrier-direct compression to continue at roughly the slope established in Q1 2026, with quarterly variability tracking each carrier’s earnings cadence and marketing-spend disclosures. Aggregators on annual pricing schedules will absorb the compression at unchanged contractual prices through year-end. Aggregators on quarterly indexed pricing will pass the compression through to buyers at a lag of one to two quarters. Aggregators completing the inventory-mix shift and data-monetization work through 2026 will end the year with structurally better margin profiles than aggregators who do not.

In the next twenty-four months, the compression slope is likely to flatten as carrier-direct programs approach saturation in the highest-value cohorts and the marginal acquisition cost at the carrier-direct channel rises. By mid-2027, carrier-direct CPCs in the most competitive segments are likely to plateau as the cohort of high-LTV prospects accessible at acceptable acquisition cost narrows. Aggregators who have shifted toward the carrier-undervalued cohorts will see margin recovery as the competitive intensity in their inventory mix is lower.

In the next thirty-six months, the structural picture stabilizes. Aggregator margin compression that began in Q1 2026 reaches its trough in 2027-2028, with the operators who completed the strategic repositioning running at compressed-but-stable margins and the operators who did not running at lower-volume, lower-margin profiles that may not be sustainable at scale. Industry consolidation is the typical outcome of this kind of multi-year compression: smaller operators sell to larger operators, the largest operators acquire the data assets they could not build organically, and the operator population narrows.

The longer-term picture is shaped by the next wave of data and AI infrastructure. Carriers building direct-acquisition models are increasingly integrating AI-driven bid logic and prospect-scoring infrastructure that improves direct-channel efficiency further. Aggregators with comparable infrastructure investments can compete for the data-services revenue stream described above; aggregators without those investments compete on a steadily shrinking surface area. The operators who will be largest in 2030 are the operators who are making the infrastructure investments now.

For auto-insurance lead generators currently running annual contracts with carrier-favored inventory mix and no data-licensing revenue stream, the next sixty days are the planning window. The next one hundred and eighty days are the build window. The structural trajectory will not wait for slower operators to catch up.

What Would Falsify This Thesis

The carrier-direct floor argument is conditional on observable behavior. Operators tracking the next two earnings cycles should look for signals that would falsify the thesis rather than confirm it. The argument should be reweighted or abandoned if the following evidence appears:

- Stable bid density on shared paid-search and paid-social pools. If clearing CPCs in the largest Google auto-insurance keyword clusters and Meta auto-quote audiences hold flat or fall through Q2 and Q3 2026 – measured through MediaAlpha, EverQuote, and aggregator-side bid-loss telemetry – the carrier-direct redeployment hypothesis is not playing out in the auctions where aggregators compete.

- Flat or falling aggregator CPL on like-for-like inventory. If the auto-insurance CPL benchmark range is flat or compressing on comparable inventory mix and consent posture across H2 2026, the aggregator margin compression mechanism is not operative regardless of carrier earnings strength.

- Unchanged carrier mix in aggregator buyer waterfalls. If Progressive, GEICO, and Allstate maintain or reduce their share of aggregator-routed lead and click volume – measured by aggregator disclosed buyer-mix or carrier-side broker-channel reporting – the carriers are absorbing capacity through direct channels that do not displace aggregator inventory.

- No incremental Progressive marketing-spend disclosure in the 10-Q. If the Q1 2026 10-Q shows quarterly advertising and marketing expense at or below the throttle-period range ($500M or less), the policy-count growth is being delivered through retention and cross-sell rather than incremental acquisition spend, and the auction-floor argument weakens.

- Allstate or Berkshire Hathaway prints showing materially weaker direct-acquisition posture. If Allstate’s April 30 release and Berkshire’s subsequent 10-Q indicate materially weaker direct-acquisition activity than Progressive’s, the carrier-direct floor is a single-carrier story rather than a market-wide rerate.

If two or more of those signals appear by the end of Q3 2026, operators should treat the floor argument as overstated and reprice their planning assumptions accordingly.

Key Takeaways

Progressive’s Q1 2026 print – $22.2 billion in revenue, $2.8 billion in net income, 39.6 million policies in force at +9% year over year, and a combined ratio of 86.4 – confirms that the carrier-direct acquisition channel is now both well-funded and operationally scaled, and can raise the floor on auto-lead aggregator pricing through the back half of 2026 if direct-acquisition capacity is redeployed into the same auction pools. The falsification signals above are the ones to monitor.

Carrier-direct CACs are bounded above by multi-year policyholder lifetime value, while aggregator per-lead pricing is bounded above by carrier-direct CACs net of conversion friction; as carrier-direct efficiency improves with policy-base compounding, the gap between the two bounds widens, producing structural rather than cyclical compression in aggregator margin.

The compression hits three channels with different timing and severity: paid-search-and-paid-social aggregator inventory faces the steepest immediate compression, comparison-marketplace inventory faces a Q2-Q3 take-rate renegotiation, and agent-routing-and-call-transfer inventory faces a milder, slower compression that arrives indirectly through carrier volume shifts.

The 2026 environment differs structurally from prior recoveries because carrier acquisition infrastructure – granular bid logic integrated with underwriting filters, real-time direct-channel optimization, and policy-base compounding effects – is materially more capable than in prior cycles, which raises the structural floor and dampens the historical cyclical reprieve aggregators received during loss-cost-shock periods.

Three responses will underperform: the wait-and-watch posture (loses margin every month it persists), the volume-recovery posture (worsens contribution by pushing into compressed auctions), and the carrier-pivot posture as a tactical fix (works only as a multi-year strategic move started years earlier).

Three principles define the realistic operator response: reprice buyer contracts on a quarterly cadence with carrier-bid-indexed pricing, shift inventory mix toward conversion-quality dimensions carrier-direct models undervalue, and monetize the data layer alongside the per-lead transaction stream.

Implementation is non-trivial: the contractual rework, inventory-mix shift, and data-monetization build together represent a nine-to-twelve-month effort across legal, engineering, analytics, and sales functions; aggregators who complete the work before the rest of the market reprices run a six-to-twelve-month structural margin advantage.

The multi-year trajectory points to continued compression through 2026, slope flattening in 2027 as carrier-direct saturation begins, structural stabilization in 2028, and industry consolidation as smaller operators sell to larger operators that have completed the data-and-infrastructure repositioning. The operators largest in 2030 are the operators making the infrastructure investments in 2026.

For auto-insurance lead operators, the planning window is sixty days. The build window is one hundred and eighty days. The decision about whether to be in the structurally repositioned cohort or the compressed-margin cohort is being made now, and the carrier-direct print confirms there is no comfortable third option.

Frequently Asked Questions

What did Progressive actually report in Q1 2026?

Progressive’s mid-April 2026 release reported revenue of $22.2 billion, net income of $2.8 billion, diluted EPS of $4.80 (up roughly ten percent year over year), net premiums written of $23.6 billion (up six percent), net premiums earned of $21.0 billion (up eight percent), a combined ratio of 86.4 (versus 86.0 a year earlier), and 39.6 million policies in force as of quarter-end (up nine percent from 36.3 million a year earlier). The combined ratio of 86.4 implies approximately $2.86 billion of pre-tax underwriting profit on the quarter, sufficient by itself to fund the entire $2.8 billion of consolidated net income with investment income providing additional cushion. The net 3.3 million policy-in-force increase over twelve months is the unit count that anchors the carrier-direct acquisition story.

Why does Progressive’s earnings print matter for auto-insurance lead aggregators?

Auto-insurance lead aggregators bid into the same paid-search and paid-social auctions that Progressive’s direct-acquisition team bids into. When Progressive’s combined ratio is profitable and policy growth is strong, the company has both the cash and the strategic mandate to bid aggressively in those auctions, which raises the clearing price and compresses aggregator margin. The Q1 2026 print confirms that Progressive is funding incremental acquisition spend out of underwriting profit and growing its policy-in-force base at nine percent year over year – a configuration that puts persistent upward pressure on auction CPCs through the back half of 2026 and continues compressing aggregator per-lead margins.

How is the carrier-direct bid different from the aggregator bid?

A carrier’s per-policy customer acquisition cost is bounded above by the present value of underwriting margin on a multi-year retained policyholder, which for a typical auto policy is in the range of $1,500 to $2,500 over a four-to-five-year retention horizon. An aggregator’s per-prospect bid is bounded above by the per-lead price the carrier or agent buyer will pay, minus the conversion friction (qualification rate, contact rate, bind rate) that compounds along the way. Because the aggregator carries conversion friction the carrier does not, the aggregator’s bid ceiling is structurally lower than the carrier’s bid ceiling on the same prospect. As the carrier’s direct-acquisition efficiency improves through the policy-base compounding effect, the gap between the two ceilings widens and aggregator margin compresses.

Is the 2026 compression cyclical or structural?

It is primarily structural. The 2026 environment differs from prior auto-insurance recovery cycles because carrier acquisition infrastructure is materially more sophisticated than in prior cycles. Carriers now integrate real-time underwriting risk signals with paid-media bid logic at granularity that allows asymmetric bidding on high-quality cohorts and bid-down on cohorts that fail underwriting filters. The compounding mechanic of policy-in-force growth – incremental renewal premium funding further marketing spend, larger denominator spreading fixed acquisition technology costs – also reinforces carrier-side advantages over time. The combination raises the structural floor on aggregator margin and dampens the historical cyclical reprieve aggregators received during loss-cost-shock periods.

When do Allstate, GEICO, and State Farm report?

Allstate’s Q1 2026 earnings call is scheduled for April 30, 2026 per the company’s newsroom announcement. GEICO’s Q1 2026 underwriting and marketing-spend data appears in Berkshire Hathaway’s Q1 2026 10-Q, expected within forty-five days of quarter-end (roughly mid-May 2026). State Farm reports auto-line direct premiums written through periodic NAIC and state-level filings rather than through public quarterly earnings calls, so the State Farm read on Q1 2026 typically becomes available later in the quarter through aggregated NAIC market-share reports.

Which aggregator channels face the steepest compression first?

The paid-search-and-paid-social aggregator inventory faces the steepest immediate compression because it competes head-to-head with carrier-direct bids in the same Google and Meta auctions. Comparison-marketplace inventory faces a slower but real Q2-Q3 2026 round of take-rate renegotiation as carrier panel participation becomes contingent on lower marketplace economics. Agent-routing and call-transfer inventory faces the mildest compression, arriving indirectly through carrier volume shifts away from the agent channel as direct-channel conversion proves out – typically a five-to-ten-percent compression in 2026 with the larger impact arriving in 2027.

What is bid-indexed pricing and why should aggregators move to it?

Bid-indexed pricing is a contractual structure in which the per-lead price between an aggregator and a buyer moves with a published index of carrier-direct CPC activity in the relevant geo-product segment. The carrier customer accepts indexed pricing because it aligns the aggregator’s per-lead price with the carrier’s own internal benchmark. The aggregator accepts indexed pricing because it transfers the bid-pressure risk back to the buyer rather than absorbing it on the supply side. Aggregators on legacy annual fixed-price contracts absorb the full carrier-direct compression at unchanged contractual prices; aggregators on indexed pricing pass the compression through to buyers at a one-to-two-quarter lag, which preserves margin during the multi-quarter compression cycle.

What inventory dimensions do carrier-direct models undervalue?

Carrier-direct models are most aggressive on prospect cohorts where the lifetime-value model produces a high expected return – typically full-file consumers in carrier-preferred geographies with vehicle profiles inside the preferred mix and short conversion-velocity profiles. Models are less aggressive on thin-file consumers, prospects in geographies where the carrier’s underwriting filter is restrictive, prospects with vehicle profiles outside the preferred mix, and prospects whose conversion-velocity profile suggests longer time-to-bind. Aggregators shifting inventory mix toward these dimensions take on more complex qualification logic and longer prospect-to-bind cycles in exchange for less direct competition with carrier-direct bids.

How does the data-monetization play actually work?

The reframe is to treat the prospect-shopping data the aggregator captures as a parallel revenue stream alongside the per-lead transaction. Carriers building direct-acquisition models invest continuously in data inputs that improve their bid logic – third-party demographic data, vehicle-history data, telematics signals, retention-model inputs. Aggregators sitting on years of prospect-shopping data have an asset that some carriers will pay for as a model input even when they decline to buy the underlying leads. The arrangement is typically structured as data-licensing or model-services revenue rather than a per-lead transaction, and it requires a data-governance posture (consent, retention, deidentification), data-product packaging, and a sales motion oriented toward carrier data-procurement teams rather than carrier media-buyer teams.

What is the realistic timeline for an aggregator to reposition?

A mid-sized auto-lead aggregator pursuing all three principles – contract repricing, inventory-mix shift, and data monetization – should plan a nine-to-twelve-month total elapsed timeline. Contract repricing on the top five buyers typically runs sixty to ninety days; rolling indexed pricing across the full buyer panel takes one hundred and twenty to one hundred and eighty days. Inventory-mix shift requires sixty to one hundred and twenty engineering-days of qualification-logic work plus forty to eighty days of segment-level analytics. Data-monetization is the largest project at nine to twelve months covering governance, product packaging, and sales-team build. Aggregators who allocate dedicated headcount complete the work faster than aggregators who run it as side work alongside other roadmap items.

How should aggregators think about volume in this environment?

Pushing volume higher to maintain absolute contribution dollars is a common but counterproductive response. Pushing volume into the same auctions where carrier-direct bids are tightening means the operator’s average paid-media cost per prospect rises faster than per-lead price holds, which compresses margin per lead at exactly the moment the operator is taking on more leads. The result is more revenue, less profit, and a working-capital problem if buyer payment terms lag media-spend payment terms. The operators who tried this playbook in 2018-2019 during an earlier carrier-direct ramp ended the cycle with worse P&L than the operators who held volume flat and shifted mix. The realistic posture is to hold or modestly reduce volume, shift mix toward less-contested inventory, and reprice contracts before continuing to chase volume at compressed margins.

What does the multi-year trajectory look like for aggregator pricing?

In the next twelve months, expect carrier-direct compression to continue at roughly the slope established in Q1 2026, with quarterly variability tracking each carrier’s earnings cadence. In the next twenty-four months, the slope is likely to flatten as carrier-direct programs approach saturation in the highest-value cohorts and the marginal acquisition cost at the carrier-direct channel rises. In the next thirty-six months, the structural picture stabilizes with the trough of compression in 2027-2028. Industry consolidation is the typical outcome – smaller operators sell to larger operators, the largest operators acquire data assets they could not build organically, and the operator population narrows. The operators largest in 2030 are the operators making the infrastructure investments now.

Sources

Tier 1: Primary Issuer and Regulatory Disclosures

-

Progressive Corporation, Q1 2026 Earnings Release, mid-April 2026 – corporate filings as referenced in trade-press coverage.

-

Allstate Corporation, “Allstate to Hold Q1 2026 Earnings Call April 30, 2026,” Allstate Newsroom, April 2026 – https://www.allstatenewsroom.com/news/allstate-to-hold-q1-2026-earnings-call-april-30-2026/

-

Berkshire Hathaway, Q1 2026 Form 10-Q, expected mid-May 2026 – to be filed at SEC EDGAR.

-

National Association of Insurance Commissioners, Quarterly Market Share Reports, Personal Auto Line, accessed April 2026 – https://content.naic.org/

Tier 2: Established Industry Research and Trade Press

-

Insurance Business Magazine, “Progressive reports solid premium and earnings growth for Q1,” April 2026 – https://www.insurancebusinessmag.com/us/news/auto-motor/progressive-reports-solid-premium-and-earnings-growth-for-q1-571925.aspx

-

Simply Wall Street, “Will Strong Q1 2026 Earnings Acceleration Change Progressive,” April 2026 – https://simplywall.st/stocks/us/insurance/nyse-pgr/progressive/news/will-strong-q1-2026-earnings-acceleration-change-progressive

-

PitchBook, “Progressive Corporation Profile,” accessed April 2026 – https://pitchbook.com/profiles/company/41169-52

-

S&P Global Market Intelligence, U.S. Personal Auto Insurance Market Share and Combined Ratio Data, accessed April 2026.

-

AM Best, Quarterly Industry Performance Updates – Personal Auto, accessed April 2026.

-

Moody’s Investor Service, U.S. Personal Auto Insurance Sector Reports, accessed April 2026.

Tier 3: Industry Statements and Practitioner Coverage

-

Insurance Information Institute, Auto Insurance Market Overview, accessed April 2026 – https://www.iii.org/

-

American Property Casualty Insurance Association, Personal Auto Insurance Reports, accessed April 2026 – https://www.apci.org/

-

Insurance Journal, Carrier Earnings Coverage, April 2026 – https://www.insurancejournal.com/

-

Business Insurance, Q1 2026 Earnings Roundup, April 2026 – https://www.businessinsurance.com/

-

National Underwriter Property & Casualty, Earnings Coverage, April 2026 – https://www.propertycasualty360.com/

Tier 4: Supporting Industry Commentary

-

LendingTree Investor Relations, Quarterly Performance Disclosures, accessed April 2026 – https://investors.lendingtree.com/

-

MediaAlpha Investor Relations, Quarterly Performance Disclosures, accessed April 2026 – https://investors.mediaalpha.com/

-

EverQuote Investor Relations, Quarterly Performance Disclosures, accessed April 2026 – https://investors.everquote.com/

-

QuinStreet Investor Relations, Quarterly Performance Disclosures, accessed April 2026 – https://investors.quinstreet.com/

-

MoneyLion Investor Relations, Engine Business Disclosures, accessed April 2026 – https://investors.moneylion.com/

Closing

The Q1 2026 Progressive print will be remembered for the wrong reason. The headlines treated it as a strong-quarter story – a continuation of the cycle the company had been running since late 2023. That framing misses what actually happened. The structural event was the confirmation that carrier-direct acquisition is now both profitably funded and operationally scaled at a level that resets the floor on every auction auto-lead aggregators compete in, and the operational event was the visible nine-percent year-over-year policy-in-force growth that establishes the compounding mechanic carriers will run against the aggregator channel for the next multi-quarter cycle. The auto-lead operators who treat the Q1 print as a one-quarter signal will spend 2026 absorbing margin compression at unchanged contractual prices. The operators who treat it as the formal start of a structural repricing will run the next nine to twelve months on contract repricing, inventory-mix shift, and data-monetization work that repositions the business for the compressed environment. The decision about which group to be in is being made now, in the next sixty days of planning and the next one hundred and eighty days of build. The carrier-direct print confirms there is no comfortable third option.

Carrier earnings data, marketing-spend disclosures, and auction-pricing dynamics reflect publicly reported conditions through April 28, 2026. Carrier strategy, paid-media auction dynamics, and aggregator buyer-side pricing change continuously; verify current terms through primary issuer filings and direct buyer relationships before making operational decisions. This article provides general industry analysis and does not constitute legal, financial, investment, or compliance advice. Consult qualified counsel for specific questions related to contract repricing, data-licensing arrangements, and consent frameworks.