The model in the contract decides who eats the loss when consent fails, the lead doesn’t bind, or the buyer’s sales process collapses.

How Lead Pricing Models Actually Settle in 2026

Revenue share and fixed price lead agreements distribute three things: conversion risk, attribution complexity, and TCPA exposure. The dominant model in any given vertical follows from the underlying unit economics – average deal size, sales-cycle length, and the commission structure of the buyer’s downstream relationship – not from preference. Personal lines insurance settles on fixed CPL because the agent commission ceiling on a bound auto policy will not pay for revenue-share tracking infrastructure. Wealth management settles on revenue share because a 25 basis-point cut of $400,000 in assets under management produces a year-one payment that fixed CPL cannot match. The choice rarely turns on philosophy; it turns on whether the buyer has the systems and runway to administer either model honestly.

This analysis covers vertical-by-vertical splits with named buyers and source-attributed benchmarks, the contract provisions that determine who absorbs conversion failures and TCPA clawbacks, the role of ping-post auctions in mediating rev-share economics through affiliate networks, and the Most Favored Nation clauses that have become standard in marketplace contracts. The framework matters because most disputes between lead generators and buyers – quality returns, consent failures, attribution shortfalls – resolve under contract terms that the negotiating parties did not read carefully on day one.

Vertical-by-Vertical Revenue Share Norms

The clearest way to understand pricing models is to look at what actually clears in each vertical, who the named buyers are, and what data sources back the splits.

Insurance: Fixed CPL Dominates Personal Lines

Personal lines insurance leads – auto, home, renters, basic life – clear almost entirely on fixed CPL through ping-post marketplaces. MediaAlpha reported $1.2 billion in 2024 transaction value across its Property and Casualty exchange according to its 2024 10-K filing, and EverQuote reported $499 million in 2024 revenue per its annual report. Both run real-time ping-post auctions with fixed CPL as the settlement unit. QuoteWizard, the LendingTree-owned insurance lead generator, and Insurify, the comparison-shopping platform, monetize on the same fixed-CPL basis.

Typical 2025 personal-lines fixed CPL ranges, drawn from MediaAlpha investor disclosures and the site’s own buyer-side research:

| Vertical sub-segment | Fixed CPL range | Lead type | Notes |

|---|---|---|---|

| Auto insurance, real-time exclusive | $35–$65 | Live transfer or web lead | Higher band for high-state-minimum geographies |

| Auto insurance, shared (3-way) | $12–$22 | Web lead | Per-buyer price; aggregate revenue per lead $36–$66 |

| Home insurance, real-time exclusive | $28–$48 | Web lead | Lower volume than auto |

| Renters insurance | $4–$12 | Web lead | Volume play |

| Final expense (whole life) | $18–$45 | Web or call | Driven by Medicare cohort |

| Medicare Advantage (AEP) | $35–$120 | Inbound call | CMS Section 422.2274 third-party marketing rules apply |

Source attribution: MediaAlpha 2024 10-K filing, EverQuote 2024 10-K filing, and the site’s research catalog cross-checked against Insurance Information Institute average premium data.

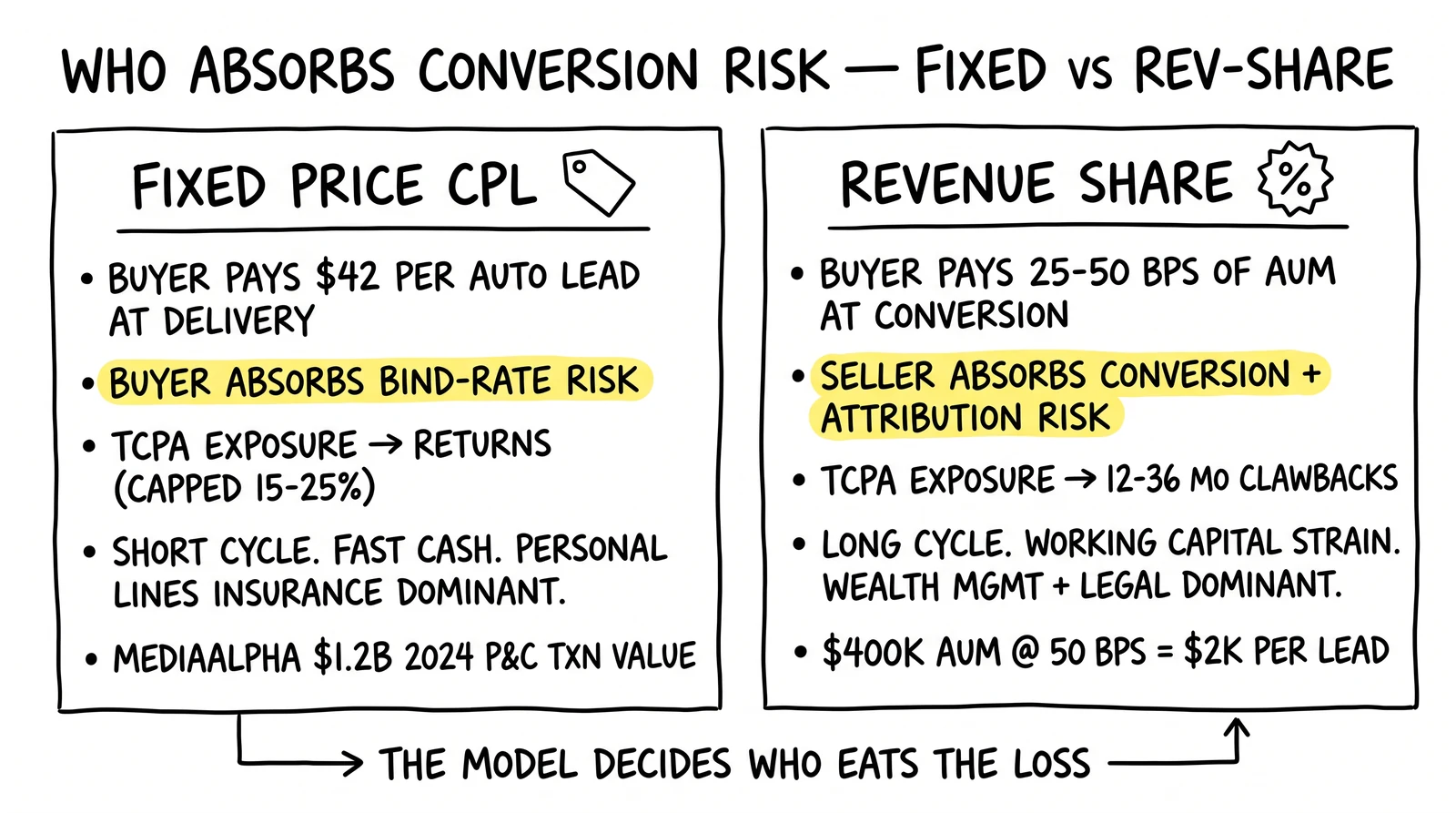

Why fixed CPL dominates personal lines: agent first-year commission on auto runs 10 to 15 percent of premium per Insurance Information Institute data, with average annual auto premiums of roughly $1,500 to $2,200. The commission ceiling – roughly $150 to $330 per bound policy – does not justify the tracking infrastructure that revenue share requires. Carriers can produce $20 to $60 fixed CPL economics that work against expected bind rates of 8 to 15 percent without absorbing the working-capital strain of multi-month rev-share float. The vertical also runs short sales cycles where rev-share delay would simply delay payment without changing total value.

Where revenue share appears in personal lines is at the network-to-affiliate boundary. Networks such as Phonexa and boberdoo administer hybrid contracts where the network takes a percentage of bound premium from carriers, then pays affiliates fixed CPL out of the resulting revenue. The affiliate sees fixed pricing; the network captures the rev-share economics. This structure is documented in the Phonexa Lynx Pulse platform documentation and is standard practice across larger lead networks.

Mortgage: Basis Points of Loan Amount

Mortgage lead pricing has shifted from pure fixed CPL toward hybrid and revenue share structures as conversion volatility increased through the 2022-2025 rate environment. The Mortgage Bankers Association Quarterly Performance Report tracks lender per-loan production cost rising from $6,983 in 2020 to $13,171 in Q4 2023, with marketing and lead acquisition representing 8 to 12 percent of total. That cost pressure pushed lenders toward arrangements that share conversion risk with originators.

Typical mortgage rev-share patterns:

- Refinance leads: 15 to 25 basis points of funded loan amount, paid at funding. On a $400,000 loan, the share is $600 to $1,000 per funded application.

- Purchase leads: 20 to 30 bps, occasionally rising to 35 bps for jumbo. Purchase leads command higher splits because cycle length and quality variance are greater.

- Non-QM and bank-statement loans: 30 to 50 bps reflecting both the higher commission to the originator and the higher quality variance.

- Reverse mortgage and HECM: 25 to 40 bps, often combined with a fixed lead-delivery fee given long cycles.

LendingTree’s lender marketplace and Zillow’s Premier Agent program both publish frameworks consistent with these ranges, and the Mortgage Bankers Association tracks lender acquisition spend disclosures that triangulate them. Fixed CPL still appears in mortgage at the top of the funnel – interest-rate quote leads at $25 to $90 per submission – but the funded-loan economics typically include a backend share component.

Per HousingWire reporting on lender pipeline data through the 2024-2025 environment, mortgage refinance leads averaged 18 to 28 percent return rates as rates moved against locked applications. Return rates this volatile push lenders toward rev-share where a returned lead simply produces no payment, eliminating the dispute friction that clogs fixed-CPL contracts.

Solar: 1 to 4 Percent of System Price

Solar lead generation has converged on a percentage-of-system-price model for residential rooftop installations. Wood Mackenzie’s US Solar Market Insight Q4 2024 reports average residential system pricing of $3.10 to $3.50 per watt and median system size of 8 kW, putting average installed cost at roughly $25,000 to $28,000 before incentives. Revenue share splits cluster as follows:

- Residential rooftop, fresh leads: 2 to 3 percent of system price, paid at install completion. On a $26,000 system, the share is $520 to $780.

- Aged or shared solar leads: 1 to 1.5 percent reflecting lower bind probability.

- Commercial solar referrals: 1 to 2 percent on systems of $100,000 to several million, with caps applied per project.

- Battery storage attachment: Often a separate percentage component on the storage subsystem or a fixed kicker of $200 to $500 per attached battery.

The shift toward rev-share in solar accelerated after 2022 when Wood Mackenzie data showed installer cost-of-acquisition spiking to $0.39 per watt – roughly $3,000 per installation – driven by elevated paid-search competition. Installers responded by pushing acquisition risk back to lead generators willing to absorb it, and the 2 to 3 percent norm emerged as the equilibrium that left both sides with workable margins. Pure fixed CPL in solar persists at $80 to $250 per real-time exclusive lead but is increasingly the structure for new buyer-seller relationships still building trust before transitioning to rev-share.

Wealth Management and Legal: Long-Tail Rev-Share

Wealth management and legal mass-tort referrals run rev-share because the deal sizes and recurring revenues justify multi-year tracking. Wealth management partnerships typically pay 25 to 50 basis points of assets under management in year one with a declining trail, often structured as an introductory referral fee paid quarterly out of advisor management fees. SmartAsset and Zoe Financial both operate under this model with RIA networks. The economics: an introduction that closes on $400,000 of AUM at a 1 percent advisor fee generates $4,000 of year-one revenue, of which 25 to 50 bps to the lead source is $1,000 to $2,000.

Legal mass-tort referral fees – for cases such as roundup litigation, hair-relaxer cases, or rideshare assault claims – run 33 to 40 percent of attorney contingent fee where state bar rules permit fee-sharing. Many state bars require client written consent to fee-sharing arrangements and prohibit referral compensation outside of bar-approved structures, creating a compliance overlay on the rev-share that operators must navigate per state.

B2B SaaS and Enterprise: Hybrid Dominates

B2B lead partnerships with enterprise SaaS buyers have converged on hybrid structures that blend fixed payment for cash flow with backend share for alignment. Forrester research on B2B partnership compensation tracks the prevalence of staged-payment structures in enterprise lead programs, and typical 2025 patterns are:

- $150 to $400 fixed payment per qualified lead, paid at MQL acceptance

- $200 to $500 incremental at sales-accepted lead (SAL) stage

- 5 to 10 percent of first-year ACV at closed-won, capped at 1.5x to 2x the fixed components combined

The hybrid structure addresses the fundamental B2B problem: enterprise sales cycles of 6 to 18 months would create unsustainable cash-flow exposure under pure rev-share, but pure fixed pricing creates quality disputes when buyer conversion rates drop and the buyer has no contractual recourse against marginal leads. The staged structure converts a single binary delivery into multiple verification points where both parties confirm progress before money changes hands.

Most Favored Nation Clauses in Lead Contracts

Most Favored Nation clauses have become standard provisions in carrier-direct insurance contracts and in mortgage marketplace agreements where buyers commit minimum monthly spend in exchange for parity protection. The clause requires that the seller never offer better pricing or terms to any other buyer for comparable lead specifications and volume.

Three forms appear regularly:

Pricing MFN. The buyer receives the lowest CPL the seller charges any other buyer for substantially identical specifications. These typically include a comparability test – exclusive versus shared, real-time versus aged, geography, product type – and audit rights with monthly reporting requirements.

Terms MFN. Beyond price, the buyer receives any preferential commercial terms offered elsewhere – extended return windows, preferred filter access, exclusivity in defined sub-segments. Terms MFN clauses are harder to administer because comparability is fuzzier than price, and disputes commonly center on whether two contracts are actually comparable.

Volume-conditioned MFN. The buyer must maintain minimum monthly spend or volume to keep MFN status. Falling below threshold suspends MFN protection. This structure protects the seller from buyers who claim parity rights without delivering the volume that justified them.

MFN clauses backfire on sellers when they freeze pricing flexibility. A seller bound by broad MFN provisions cannot discount opportunistically without triggering price drops across the entire MFN-bound buyer cohort, and cannot offer promotional pricing to win new buyers without extending those terms to existing relationships. Sophisticated lead generators resist broad MFN provisions in initial term sheets, often offering narrow Pricing MFN limited to identical lead specifications and excluding volume-conditioned and promotional pricing carve-outs. The site has covered the marketplace dynamics of exclusive versus shared lead structures where MFN provisions become consequential.

True-up payments are the standard remedy for retroactive MFN violations. If audit reveals that the seller offered better pricing to another buyer in a prior period, the bound buyer receives a credit equal to the price differential applied retroactively. True-up provisions typically include a 12 to 24 month look-back window matching audit-rights periods.

TCPA, PEWC, and Revenue Share Clawbacks

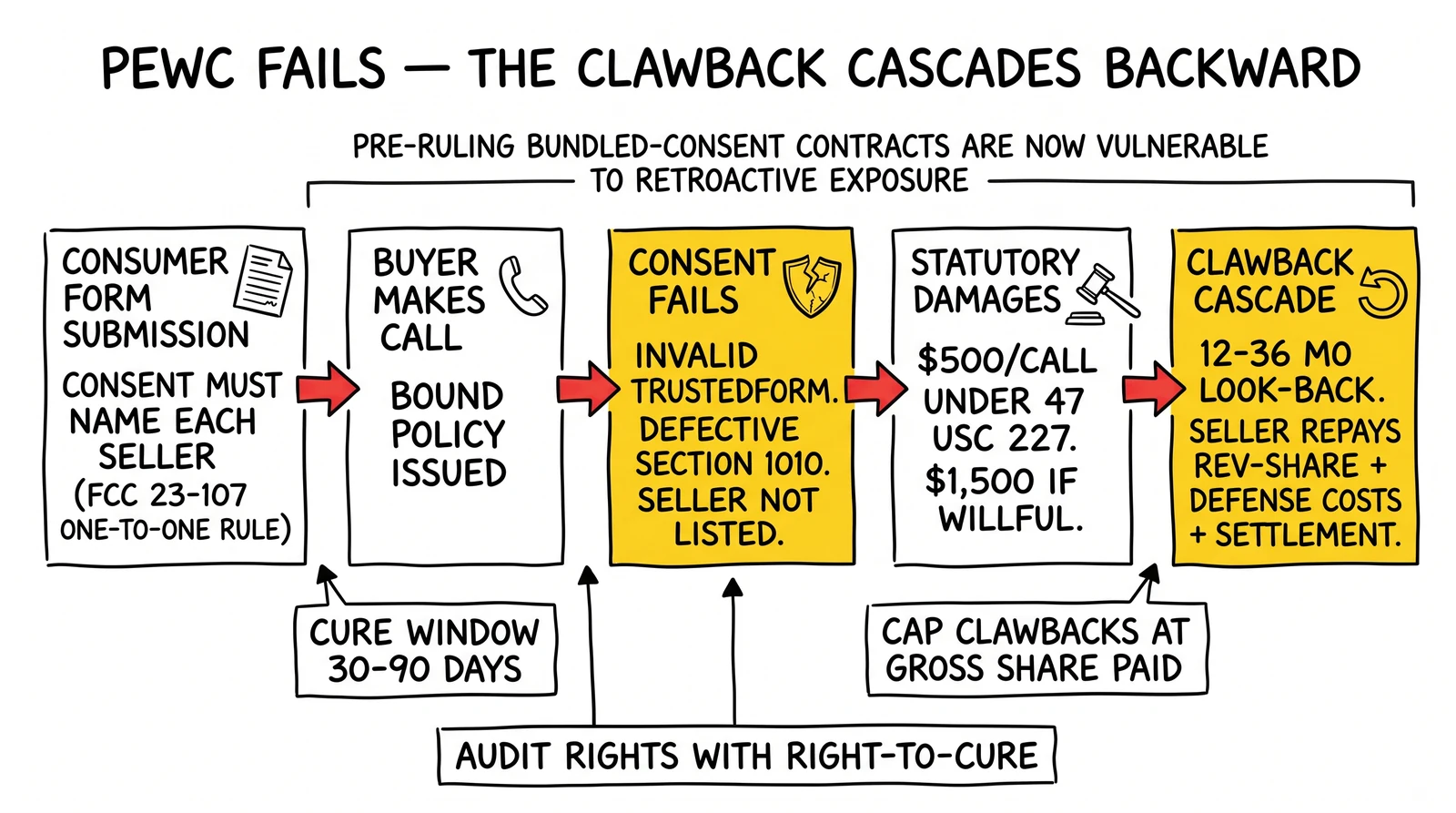

TCPA exposure flows backward through the lead chain because Prior Express Written Consent must be obtained from the consumer for each named seller before any telemarketing call or text. The 2024 FCC Order strengthening consumer revocation rights (FCC 23-107, formally the FCC Order on TCPA One-to-One Consent), which the FCC documented in its rulemaking summary, codified that bundled consent across multiple unspecified sellers is no longer compliant. Each seller must be named at the moment of consent. When that consent record fails – invalid TrustedForm or Jornaya LeadiD certificate, defective Section 1010 disclosure on the consent form, or seller not listed at the time of opt-in – the buyer absorbs statutory damages of $500 per call under 47 USC 227(b)(3), trebling to $1,500 for willful violations.

Revenue share contracts respond to this exposure with clawback provisions that reverse already-paid shares when consent fails post-payment. The mechanics:

Look-back window. Clawback rights typically extend 12 to 36 months matching the TCPA statute of limitations under 28 USC 1658. Some buyer-favorable contracts extend to four years to cover any private right of action that survives the limitations period.

Trigger events. Clawbacks trigger on actual TCPA litigation, regulatory enforcement, or documented consumer revocation that the seller did not honor. Some agreements add credible-threat triggers – demand letters from class-action plaintiff firms – but these are aggressively negotiated.

Calculation basis. Clawback amounts typically equal the full revenue share paid plus a pro-rata share of buyer defense costs and any settlement. Some agreements cap clawbacks at the gross revenue share paid; others extend to direct damages, creating significant tail exposure for sellers.

Cure rights. Sellers typically negotiate a right-to-cure window of 30 to 90 days where they can produce missing consent documentation, remediate consent records, or settle directly with the consumer before clawback enforces.

Fixed price agreements push consent risk toward returns rather than clawbacks. ActiveProspect and LeadsCouncil best-practice guidance recommends that consent failures discovered within standard return windows trigger lead returns at full credit, with returns capped at 15 to 25 percent of monthly volume. This structure isolates the buyer’s TCPA exposure while limiting the seller’s commercial exposure to the return cap. The site covers the full mechanics of consent flow in its Prior Express Written Consent guide.

The 2024 FCC ruling effectively makes one-to-one consent the operating standard, and contracts that pre-date the ruling typically need to be renegotiated to allocate the new exposure. Sellers who continue to operate under bundled consent assumptions face clawback exposure on any policy bound during the post-ruling period. Drips and Gryphon.ai have published TCPA risk allocation guidance documenting the contract-language updates that buyers and sellers have implemented in response.

Ping-Post Auctions and Revenue Share Mediation

Ping-post auctions almost universally settle on fixed CPL at the post stage rather than revenue share. The auction mechanism resolves price discovery in milliseconds through a ping (consumer attributes sent to bidders) followed by a post (lead delivered to the highest-bidder URL endpoint). Carrying revenue share through a real-time auction would require buyers to commit to a percentage of an unknown future outcome at bid time, which is mechanically incompatible with sub-second auction settlement. The site covers the technical architecture in detail in its ping-post systems primer.

Where revenue share appears alongside ping-post is at the layer above the auction. The structure:

- Consumer fills out a form on a publisher property (a comparison site, an SEO-optimized vertical landing page, an aggregator).

- The publisher feeds the lead to a network – Phonexa, boberdoo, LeadsPedia, MediaAlpha – that runs the ping-post auction against its connected buyer pool.

- The network captures the post price as gross revenue and pays the affiliate or publisher a fixed CPL out of it (typically the auction price minus a network margin of 15 to 35 percent).

- The network then runs separate downstream contracts with buyers that may include rev-share treatment – a percentage of bound premium, basis points of funded loan, percentage of system price – flowing back from the buyer to the network on a quarterly reconciliation cycle.

The structure resolves the cash-velocity problem for affiliates while letting the network and the wholesale buyer share conversion risk on the long tail. Affiliates see clean fixed CPL economics that support their media-spend pacing; networks absorb the working-capital float of rev-share reconciliation; buyers get aligned incentives without disrupting the auction-clearing mechanism.

A common variant: the network sells leads under tiered structures based on auction-clearing prices, then applies different rev-share percentages to different buyer cohorts. Premium-tier buyers paying the highest post prices may get smaller rev-share kickbacks (or none); discount-tier buyers paying lower post prices may pay larger rev-share trails to the network. This creates de facto multi-tier pricing that the affiliate never sees.

Attribution Manipulation and Defense Mechanics

Attribution manipulation is the dominant risk to sellers under revenue share. The methods are well documented across operator forums, ActiveProspect compliance materials, and the site’s coverage of multi-touch attribution models. The common manipulations:

Source reassignment. The buyer’s CRM records the lead with the seller’s source code at submission, then reassigns to an organic or direct source code after conversion. Reconciliation reports keyed on the reassigned source show no conversion attributed to the seller.

Attribution window compression. The contract specifies a 30-day attribution window even though the buyer’s actual sales cycle averages 60 days. Leads that convert outside the window produce no rev-share payment, even though they originated with the seller.

Channel-shifted retargeting. The buyer remarkets to the consumer through display, search, or email after submission, then claims the conversion came through the secondary channel rather than the original lead source. Multi-touch attribution rules in the contract decide whether this is a legitimate adjustment or a manipulation.

Off-system conversion. The lead converts through a sales process that runs in a separate CRM that does not feed the reconciliation system – a phone-only inside-sales team, a partner reseller, a sister entity. The conversion does not appear in the report.

Refund and chargeback coding. Conversions are recorded but later reversed as refunds or chargebacks, sometimes legitimately and sometimes to evade rev-share. Contracts typically require that net revenue calculations for share purposes apply only to actual customer-initiated refunds within a defined window.

Defense mechanics fall into four categories:

Unique identifier propagation. Every lead carries a unique ID that propagates through the buyer’s CRM, sales pipeline, billing system, and revenue recognition systems. Reconciliation reports key on the ID, eliminating source reassignment manipulation.

Third-party consent and identity certificates. Jornaya LeadiD or TrustedForm certificates create independent, auditable records of the lead at submission. The certificate token persists in buyer systems and supports forensic reconstruction when reports are challenged.

Audit rights with right-to-cure. The contract specifies access to buyer CRM and reconciliation data on at least an annual basis, with a 30 to 60 day right-to-cure when audit reveals discrepancies. Sellers typically condition full revenue share enforcement on audit-rights compliance, with payment terms reverting to a fallback fixed price during periods when audit access is denied.

Independent verification through closed-loop reporting. Some buyer-seller relationships use a third-party verification service that independently confirms conversions through carrier APIs, lender funding records, or installer closeout reports. The site covers feedback-loop architecture in its sales team lead quality feedback loops guide.

The Forrester Research analysis of B2B sales and marketing alignment identifies attribution disputes as the leading cause of rev-share partnership dissolution, more frequent than pricing disagreements or volume shortfalls. The contract-mechanics layer is what determines whether disputes resolve through cure provisions or through litigation.

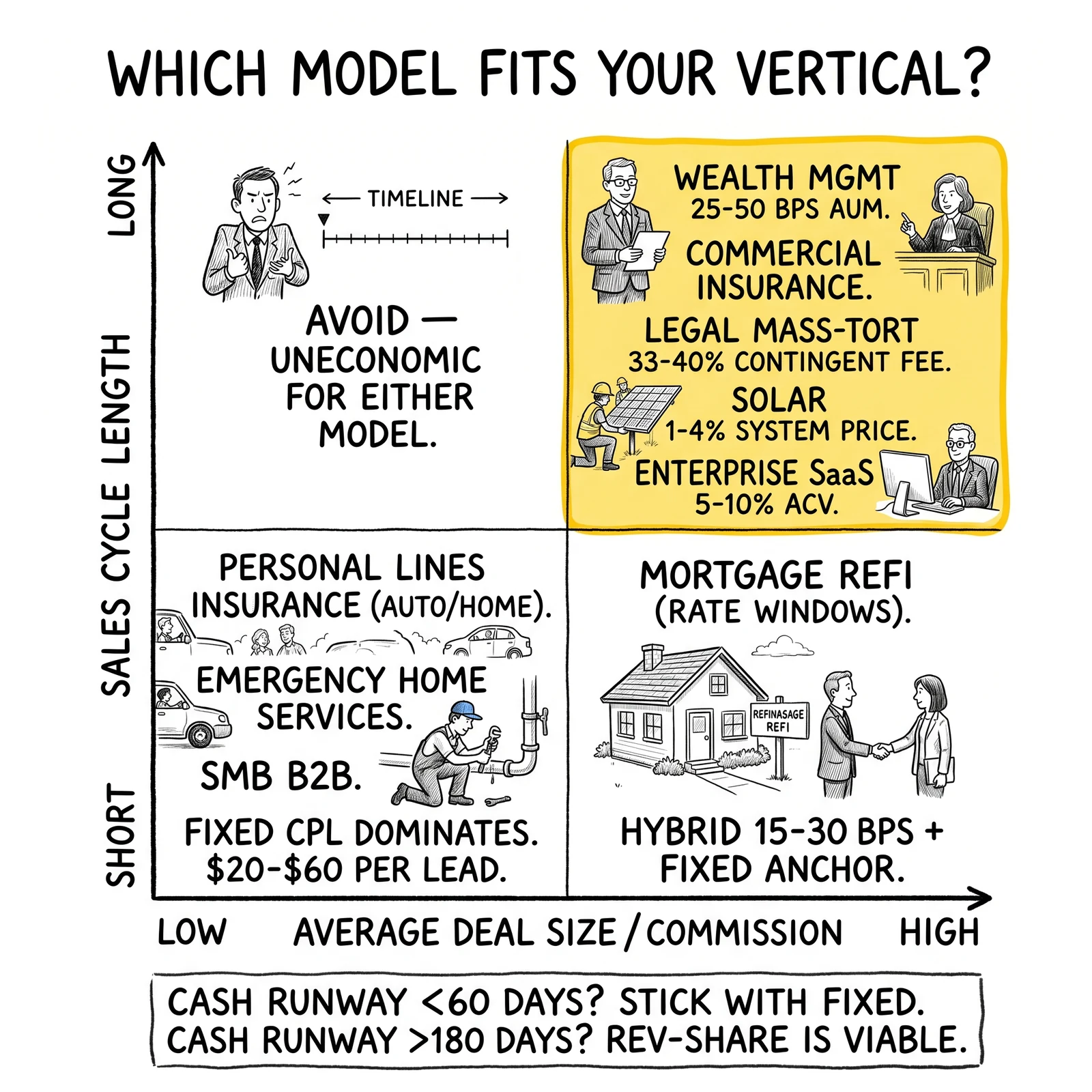

Vertical Conditions That Favor Each Model

Pulling the vertical patterns together produces a decision framework:

| Condition | Favors Fixed Price | Favors Revenue Share | Favors Hybrid |

|---|---|---|---|

| Sales cycle | Days to weeks | Months to years | 30 to 180 days |

| Average deal size | Low to medium ($500 to $5,000 commission) | High ($5,000+ commission or recurring) | Variable |

| Quality variance | Low (commoditized) | High (unverified buyers) | Medium |

| Buyer sales process maturity | Mature, predictable | Variable or unproven | Mixed |

| Cash flow runway | Tight (weeks) | Long (6+ months) | Medium |

| Attribution infrastructure | Not required | Critical | Required for performance leg |

| TCPA exposure | Push to returns | Push to clawbacks | Allocated by component |

| Vertical examples | Auto/home insurance, emergency home services, SMB B2B | Wealth management, commercial insurance, mass-tort legal | Mortgage purchase, enterprise SaaS, life insurance, solar |

The framework reflects the actual settlement patterns described above. Personal lines insurance, emergency home services, and SMB B2B run fixed price because deal sizes and cycle lengths do not justify the alternative. Wealth management, commercial insurance, and legal mass-tort run revenue share because the deal economics and tracking systems make it the only structure that captures fair value. Mortgage purchase, enterprise SaaS, life insurance, and solar run hybrid because the unit economics support some rev-share upside but cash-flow cycles require fixed-component anchoring.

Case Study: MediaAlpha Personal Lines (Public Filings)

MediaAlpha’s 2024 10-K filing provides the cleanest public window into a fixed-CPL marketplace at scale. The company reported $1.2 billion in 2024 P&C transaction value with 28.4 million transactions, implying average transaction value of roughly $42 per transaction. The marketplace operates a pure ping-post auction where buyer carriers and agents bid on consumer attributes in real time, and the winning bid produces a posted lead at fixed CPL. There is no rev-share component flowing back to MediaAlpha from carriers – the auction price clears the transaction.

The 10-K describes the take-rate dynamic where MediaAlpha pays publishers and affiliates a portion of the transaction value as cost of revenue. The implicit publisher share is in the 70 to 80 percent range based on the gross profit margin disclosed, leaving MediaAlpha a network margin of 20 to 30 percent before operating costs. This structure mirrors the broader personal lines pattern: affiliates get fixed CPL, the network captures auction-clearing margin, and carriers absorb downstream conversion outcomes through their own bind-rate management.

The relevant takeaway for operators: at scale, the fixed-CPL ping-post model produces a working economic equilibrium where each layer optimizes its own incentive without requiring contractual rev-share alignment. The carriers’ bidding algorithms incorporate expected bind rates and lifetime value into the bid; the network optimizes auction efficiency; affiliates optimize traffic acquisition against fixed CPL clearing prices. No party requires visibility into the others’ downstream economics to make decisions.

Case Study: SmartAsset Wealth Management Referrals

SmartAsset’s referral program for fee-only RIAs operates on a hybrid structure that the company has documented publicly through its advisor marketing materials and that aligns with the wealth-management norms described above. RIAs pay SmartAsset a fee per qualified introduction (the fixed component) plus a percentage of advisor first-year revenue from converted clients (the performance component), with the structure tuned to the typical AUM and fee economics of the advisor segment.

Public reporting on the program structure indicates fixed introduction fees in the $400 to $1,500 range depending on advisor tier and consumer asset size, with backend revenue share running in the 25 to 50 basis point range of AUM. The hybrid is necessary because SmartAsset must finance ongoing media spend on financial-keyword paid search at average CPCs of $40+ per Wordstream benchmark data, while RIAs cannot absorb fixed CPL high enough to fund those acquisition costs without conversion alignment. The performance component lets SmartAsset recover its actual cost-per-converted-client over the 12 to 18 month conversion arc that wealth management requires.

The case illustrates why long-cycle, high-LTV verticals consistently produce hybrid structures rather than pure rev-share. The fixed component is what makes the working capital workable for the lead-side operator; the performance component is what makes the cost structure workable for the buyer.

Case Study: Phonexa Hybrid Distribution

Phonexa’s Lynx Pulse platform documentation describes hybrid contract administration for buyer-seller relationships running on its distribution infrastructure. The platform supports configurable structures that combine per-lead fixed pricing, stage-based payments triggered by buyer-side events (lead acceptance, sales acceptance, qualified opportunity), and percentage-based shares of downstream revenue tied to buyer-reported conversion outcomes. The platform handles the reconciliation accounting that hybrid contracts require – calculating share payments across reporting periods, applying clawbacks when conversions reverse, and producing audit-trail reports keyed on unique lead identifiers.

The relevance: hybrid structures are administratively expensive enough that most buyer-seller relationships running them do so on shared infrastructure rather than building bespoke reconciliation systems. The Phonexa documentation effectively codifies the hybrid contract patterns that have emerged across mortgage, insurance, and B2B verticals into configurable workflows. Operators evaluating whether to enter hybrid arrangements should understand that the contract terms presume infrastructure capability – both parties need systems that can ingest, reconcile, and audit the multi-component payments, or the structure collapses into payment disputes regardless of how well the underlying terms are negotiated.

Risk Allocation Across Models

Each pricing model creates specific risks that thoughtful contract design mitigates. The structure of the risks differs enough by model that conflating them produces missed exposure.

Fixed Price Risks

Seller-side: Buyer default risk – buyers fail to pay for delivered leads – mitigated through credit checks, prepayment terms, security deposits, and volume limits on new buyer relationships. Return abuse risk arises when buyers return excessive volume inappropriately; mitigation is return caps at 15 to 25 percent of monthly volume per LeadsCouncil guidance, reason-code requirements, and pattern-based dispute escalation. Market price compression risk emerges when competitive pressure drives prices below sustainable levels; sellers diversify across buyers and verticals to protect against single-marketplace deterioration.

Buyer-side: Quality degradation risk occurs when sellers sacrifice quality for volume against threshold-only specifications. Source undisclosure risk exists when sellers obscure traffic sources that create compliance or downstream-quality concerns; FCC enforcement under the 2024 one-to-one consent rule has made source disclosure non-negotiable for personal lines insurance and mortgage. Dependency risk develops when concentration with a single seller creates vulnerability to seller-side disruption.

Revenue Share Risks

Seller-side: Buyer underperformance risk materializes when poor sales execution fails to convert quality leads. Mitigation is minimum guarantees per lead or per period, performance benchmarking against industry-typical bind rates, and termination rights when buyer-side conversion falls outside contracted ranges. Attribution manipulation risk – covered in the previous section – is the dominant exposure. Payment timing risk affects cash flow when revenue recognition delays payment significantly; mitigations include advance or draw provisions, accelerated payment for aged leads, and explicit working-capital planning. The 60 to 180 day float between lead delivery and revenue share payment is the primary reason small lead generators avoid rev-share entirely.

Buyer-side: Overpayment-for-marginal-quality risk occurs when revenue share creates obligation for leads that would have converted anyway through other channels. Mitigation is incrementality testing, holdout analysis on randomized lead cohorts, and attribution methodology that excludes obviously-non-incremental traffic. Unlimited exposure risk exists when lead volume times share percentage exceeds budget capacity; volume caps, monthly spend ceilings, and per-lead share caps protect against runaway exposure. Adverse selection risk emerges if sellers route high-quality leads to fixed-price buyers while routing marginal leads to rev-share arrangements; exclusivity provisions or source-equivalence audit rights address selection bias.

Hybrid Structure Risks

Hybrid agreements compound risks across both components. The fixed component carries seller-side default risk and return abuse; the performance component carries attribution manipulation and buyer underperformance. Component allocation problems emerge when one party views the fixed component as a floor and the other views it as offsetting the performance component. Contract language must specify whether components are independent or whether the performance component net of fixed payment is what changes hands. Cap and floor provisions become particularly consequential – performance payments capped at 1.5x to 2x the fixed component prevent runaway buyer exposure, and fixed-component minimums protect sellers when conversion fails entirely.

Implementation Mechanics: What Contracts Must Specify

Agreement structure significantly impacts outcomes beyond model choice. Implementation details determine whether contracts function or whether they generate continuous disputes.

Lead Qualification Definition

Under either model, explicit specifications prevent post-delivery disputes. Required field validation should specify exact verification standards – phone validity through real-time carrier database lookup with line-type identification excluding VOIP, email deliverability through MX-record check plus syntactic validation, address standardization to USPS Coding Accuracy Support System format. Intent qualification for revenue share contracts should extend beyond contact validity to capture purchase intent at the form level: explicit consent to specific product interest, asset or income thresholds, geographic eligibility. Exclusion criteria – prior customers, competitor employees, test submissions, duplicates within defined windows – must be enumerated rather than assumed. Verification and acceptance processes should specify whether returns require real-time API rejection with reason codes or batch review with defined SLAs.

Compensation Mechanics

For fixed price agreements, payment timing balances seller cash-flow needs against buyer protection. Payment on delivery maximizes seller velocity but eliminates buyer recourse; payment after a 24 to 72 hour review window enables verification before funds transfer. Return policies should specify return windows (typically 7 to 14 days for personal lines, longer for mortgage and B2B), valid return reasons, documentation requirements, and credit-application mechanics.

For revenue share agreements, revenue definition must be precise – gross premium versus net of cancellations, gross loan amount versus net of buyback risk, gross system price versus net of warranty reserves. Attribution methodology – first-touch, last-touch, position-based, time-decay multi-touch – should reflect actual contribution. The site covers attribution model selection in detail in its multi-touch attribution guide. Reporting requirements should specify frequency (monthly minimum, weekly preferred), format (reconciliation file with unique lead identifiers), and detail level sufficient for seller-side verification.

For hybrid models, component separation must be explicit. Triggers for the fixed component (delivery, MQL acceptance, SAL stage) must not overlap with triggers for the performance component (closed-won, funded, bound). Cap and floor provisions should reflect actual risk tolerance rather than templated defaults.

Term, Termination, and Dispute Resolution

Term and termination provisions establish relationship duration and exit mechanics. Auto-renewal language with 30 to 90 day notice requirements is standard. Post-termination obligations matter for rev-share – whether the seller continues to receive share payments on leads delivered before termination that convert post-termination, and over what tail period. Dispute resolution mechanisms – mediation, arbitration venue, prevailing-party fee provisions – become consequential when audit rights are invoked or when TCPA clawbacks trigger. Most operator-level lead contracts specify arbitration in the seller’s home jurisdiction, though buyer-favorable contracts increasingly specify the buyer’s jurisdiction with a fee-shifting clause.

Key Takeaways

-

Fixed CPL dominates personal lines insurance and short-cycle verticals because the agent commission ceiling does not justify rev-share tracking infrastructure. MediaAlpha and EverQuote 10-K filings confirm the structure at marketplace scale, with the ping-post auction settling on fixed CPL while networks capture margin between affiliate-side fixed pricing and carrier-side spend.

-

Mortgage rev-share runs 15 to 30 basis points of funded loan amount, with non-QM and jumbo extending to 35 to 50 bps. The shift from pure fixed CPL accelerated through the 2022-2025 rate environment as MBA-tracked lender per-loan production cost rose past $13,000, pushing lenders toward arrangements that share conversion risk.

-

Solar rev-share converged on 1 to 4 percent of system price after Wood Mackenzie data showed installer cost-of-acquisition spiking to $0.39 per watt in 2022. The 2 to 3 percent residential rooftop norm emerged as the equilibrium that absorbs acquisition risk while leaving installer margins workable.

-

Wealth management runs 25 to 50 bps of AUM in year one with declining trail; legal mass-tort runs 33 to 40 percent of attorney contingent fee subject to state bar fee-sharing rules. Both are long-cycle, high-LTV verticals where deal economics make any other structure uncompetitive.

-

MFN clauses freeze pricing flexibility and should be resisted in initial term sheets. Sellers who sign broad MFN provisions cannot offer promotional pricing or new-buyer discounts without triggering retroactive parity adjustments across the entire MFN-bound cohort. Narrow Pricing MFN limited to identical specifications and excluding promotional carve-outs is the negotiated equilibrium.

-

TCPA Prior Express Written Consent failures trigger clawbacks that flow backward through the rev-share chain for 12 to 36 months matching the statute of limitations. The 2024 FCC one-to-one consent ruling makes pre-existing bundled-consent contracts vulnerable to retroactive clawback exposure on any policy bound during the post-ruling period.

-

Ping-post auctions settle on fixed CPL at the post stage; revenue share appears only at the network-to-buyer layer above the auction. Networks like Phonexa and boberdoo capture rev-share economics from wholesale buyers while paying affiliates clean fixed CPL that supports media-spend pacing.

-

Attribution manipulation is the dominant rev-share dispute driver. Defense mechanics – unique identifier propagation, third-party consent certificates, audit rights with right-to-cure, closed-loop verification – must be specified in contract language before disputes arise. Forrester research identifies attribution disputes as the leading cause of rev-share partnership dissolution.

Sources

- MediaAlpha 2024 Annual Report on Form 10-K – U.S. Securities and Exchange Commission filing, March 2025; transaction value, P&C exchange volumes, and publisher-take economics

- EverQuote 2024 Annual Report on Form 10-K – U.S. Securities and Exchange Commission filing, February 2025; insurance lead marketplace revenue and operating metrics

- FCC Order on TCPA Consumer Consent Revocation and One-to-One Rule (FCC 23-107) – Federal Communications Commission rulemaking, December 2023 with 2024 amendments; basis for one-to-one consent and clawback exposure

- Insurance Information Institute, Facts + Statistics: Auto Insurance – III Research, 2024–2025; average annual auto premium and agent commission ranges

- Mortgage Bankers Association Quarterly Performance Report – MBA Research and Economics, Q4 2023 through Q3 2024; lender per-loan production cost and acquisition spend trend

- Wood Mackenzie US Solar Market Insight Q4 2024 – Wood Mackenzie Power and Renewables Research, December 2024; residential system pricing and installer cost-of-acquisition data

- ActiveProspect TrustedForm Product Documentation and TCPA Consent Best Practices – ActiveProspect Compliance Library, 2024; consent certificate mechanics and return policy guidance

- LeadsCouncil Industry Standards – LeadsCouncil Guidance, 2024; return rate caps, dispute resolution practice, and marketplace conduct standards

- Phonexa Lynx Pulse Pricing, Distribution, and Reconciliation Documentation – Phonexa Platform Reference, 2024; hybrid contract administration and reconciliation accounting

- Forrester Research, B2B Sales and Marketing Alignment Starts With the Customer (RES58165) – Forrester Research Report; B2B partnership compensation and attribution dispute prevalence

- HousingWire industry coverage on lender pipelines – HousingWire Industry Coverage, 2024–2025; refinance return rates and pipeline reporting

- Drips and Gryphon.ai TCPA risk allocation guidance – Industry Compliance Bulletins, 2024; TCPA risk allocation and contract-language updates for buyers and sellers

Conclusion

The pricing model in a lead agreement decides who absorbs the loss when consent fails, when conversion drops, and when the buyer’s sales process collapses. Personal lines insurance has settled on fixed CPL because the underlying unit economics make any other structure uncompetitive at scale. Wealth management, commercial insurance, and legal mass-tort run rev-share because the deal sizes justify multi-year tracking. Mortgage, enterprise SaaS, life insurance, and solar run hybrid structures because cash-flow cycles require fixed anchoring while deal economics support backend share alignment. The 2024 FCC one-to-one consent ruling, the migration of MFN clauses into marketplace contracts, and the maturation of ping-post infrastructure have raised the operational sophistication required to administer either model honestly. Operators who treat pricing-model selection as a templated choice – defaulting to industry convention rather than analyzing the specific exposure their contracts create – discover the cost when a clawback hits, an audit fails, or a buyer reconciliation report does not match the seller’s CRM. The contracts that survive the next five years will be the ones written by parties who read the clawback language, the MFN comparability test, and the attribution methodology before they signed.