Counterparty risk became the dominant cost line in residential solar lead generation the moment Freedom Forever’s bankruptcy petition hit the Delaware docket.

The April 15 Filing in One Page

Freedom Forever LLC filed a voluntary Chapter 11 petition in the U.S. Bankruptcy Court for the District of Delaware on April 15, 2026, case number 26-10522. The petition listed estimated assets of $100 million to $500 million against estimated liabilities of $500 million to $1 billion, with 50,000 to 100,000 creditors. The Temecula, California company, founded in 2011, was the second-largest U.S. residential solar installer in 2025 by Wood Mackenzie’s measure, holding 6.1 percent national share against Sunrun’s 12 percent. The filing came nine business days after the Texas Attorney General named the company in a Civil Investigative Demand targeting deceptive sales practices in residential solar.

The largest single creditor is Mosaic Funding at approximately $114 million. Other top trade creditors include PT. IDN Solar Tech, JA Solar, Trina Solar, Silfab Solar, Unirac, and GoodLeap. The company was represented by Morris Nichols Arsht & Tunnell. Pre-petition, Freedom Forever had operated in 35 states plus Puerto Rico and the District of Columbia, claimed more than 3,600 employees in August 2025, and had installed approximately 2 GW of residential capacity over its history. By early 2026, the company had exited 10 state markets and reduced headcount by approximately 20 percent. Lead aggregators with open invoices to Freedom Forever as of the petition date became unsecured creditors with claims subject to the automatic stay.

For solar lead aggregators, the filing is not a one-off headline. It is the tenth meaningful residential solar bankruptcy in 24 months, and it changes the counterparty-risk math underneath every aggregator’s accounts receivable schedule, contract template, and buyer-diversification policy. The operators who absorb the loss without margin damage are the ones who priced this scenario into their AR aging triggers, contract terms, and TPO buyer roster before the petition hit. The operators who did not are now writing down receivables, rewriting credit policy under stress, and explaining the loss to their lender or their owner. This article is the policy document the second group needs.

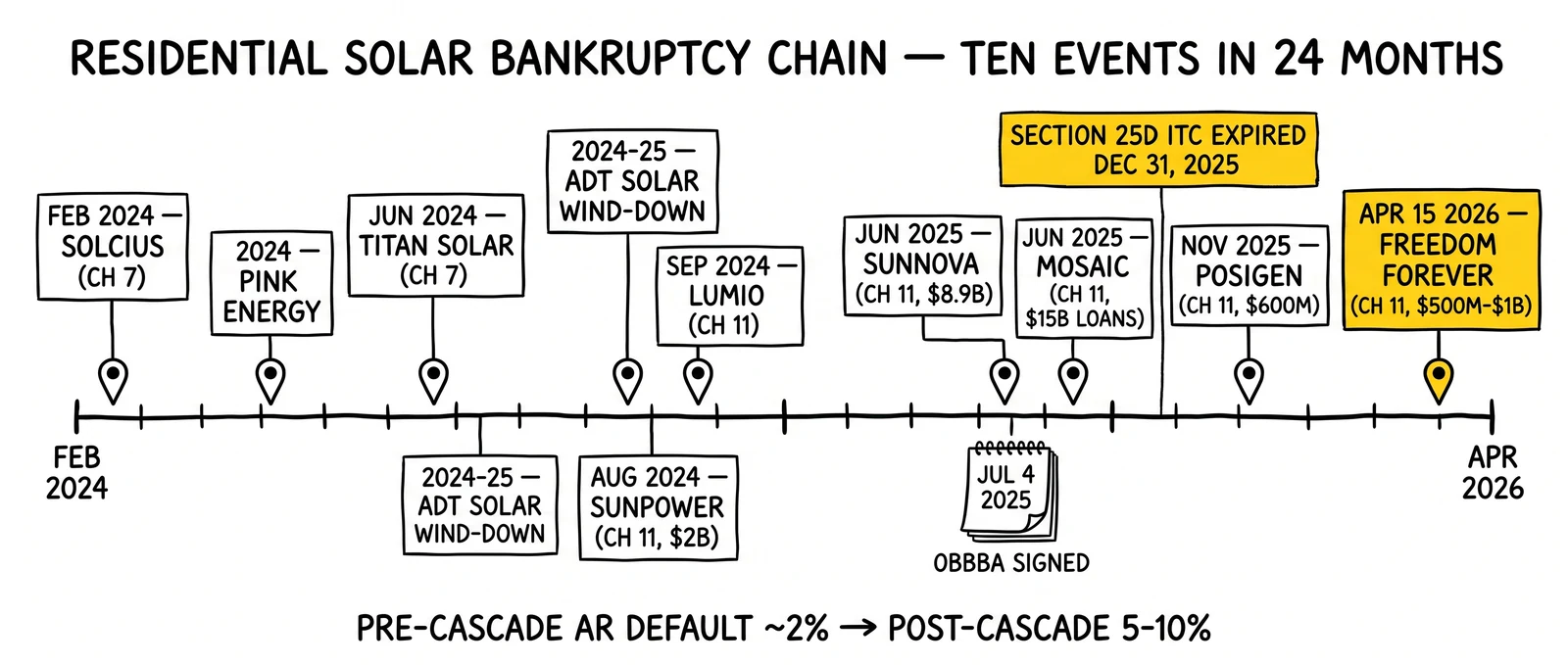

The 24-Month Residential Solar Bankruptcy Chain

The Freedom Forever filing is the closing entry in a sequence that began in early 2024 and produced ten major Chapter 11 or Chapter 7 events plus several wind-downs. The pattern matters because it is not random distress – it is a structural reset of an industry whose unit economics depended on a tax credit (Section 25D) that expired December 31, 2025 under the One Big Beautiful Bill Act, signed July 4, 2025. The cumulative loss of installer and finance counterparty capacity has been concentrated and, for aggregators, traceable.

| Month | Company | Event | Headline financial fact |

|---|---|---|---|

| Feb 2024 | Solcius | Chapter 7 liquidation | Subsidiary of NRG-acquired holding company |

| 2024 | Pink Energy (formerly Powerhome Solar) | Bankruptcy / wind-down | Multi-state consumer fraud actions preceded filing |

| Jun 2024 | Titan Solar Power | Chapter 7 (Arizona) | 22-state operation, ~150,000 affected homeowners |

| 2024-2025 | ADT Solar | Wind-down | Exit announced Jan 2024 after 22-state expansion |

| Aug 2024 | SunPower | Chapter 11 (Delaware) | ~$2.0B in outstanding debt; $45M sale to Complete Solaria |

| Sep 2024 | Lumio | Chapter 11 | $4M cash + 6.2M shares to Zeo Energy |

| Jun 2025 | Sunnova Energy | Chapter 11 | ~$8.9B long-term debt; assets to Solaris Assets for ~$118M |

| Jun 2025 | Solar Mosaic | Chapter 11 (S.D. Texas) | $15B in originated loans; servicing to Solar Servicing (Forbright Bank) |

| Nov 2025 | PosiGen | Chapter 11 | $600M Brookfield exposure; plan confirmed Feb 24, 2026 |

| Apr 2026 | Freedom Forever | Chapter 11 (Delaware, 26-10522) | $500M-$1B liabilities; Mosaic Funding ~$114M top creditor |

Sources: PV Magazine USA, Solar Power World, Law360, Utility Dive, Bloomberg Law, court dockets.

Three observations follow from the table. First, the cascade affected every layer of the value chain – direct-sale installers (Titan, Lumio, Freedom Forever), TPO operators (Sunnova, PosiGen), and finance platforms (Mosaic). An aggregator who diversified across “installer types” but stayed within residential solar diversified across nothing material. Second, the geographic footprint of failed installers covered every major solar state. There is no regional safe harbor in residential solar receivables. Third, the timing is compressed: ten events in 24 months is roughly one event per quarter, and the tail risk that one of them is a top-five customer of any given aggregator is non-trivial.

The driver was identifiable in advance. Section 25D, the residential portion of the federal solar Investment Tax Credit, expired in full on December 31, 2025 with no phase-down. Section 48E, the business-side credit applicable to TPO leases and PPAs, remains in effect through 2027. The OBBBA’s combined effect was to compress customer-owned demand into a 2025 pull-forward, leave installers with overbuilt sales capacity entering a structurally smaller 2026 market, and concentrate surviving demand in TPO. Wood Mackenzie and SEIA’s Q4 2025 Solar Market Insight projected residential installations falling 18 percent year-over-year in 2026. Wood Mackenzie’s separate analysis projected residential customer acquisition costs rising approximately 40 percent in 2026 before gradual decline. An installer business model dependent on customer-owned loan economics in that environment had a survival problem, and Freedom Forever was the largest installer to confirm it through a petition.

Why This Is a Counterparty-Risk Problem, Not a Solar Problem

The framing matters because aggregators who treat the cascade as “solar industry trouble” address it with marketing or vertical decisions – exit solar, raise prices, find new verticals. The framing that produces correct policy is counterparty-risk: aggregators sell a perishable inventory product (a contacted lead) on credit, typically net-30 or net-45, and the buyer’s ability to pay is the second-largest variable in operator unit economics after lead-acquisition cost. When the buyer’s industry produces ten bankruptcies in 24 months, the counterparty-risk component of CPL is structurally higher than what 2023-vintage contracts and pricing assumed.

Consider the math on a hypothetical $20 million annual solar lead aggregator. Average outstanding AR at any given time runs roughly $1.5 million on net-30 terms. If the largest buyer represents 18 percent of revenue (a common concentration in solar lead operations) and that buyer files Chapter 11, immediate exposure is approximately $270,000 of pre-petition receivables, plus whatever inventory was in transit. Recovery on unsecured pre-petition claims in 2024-2025 residential solar Chapter 11s has clustered in the 1 to 20 percent range, with most cases at the low end. Modeling a 5 percent recovery, the operator absorbs a $256,000 charge on a single counterparty event. On a 20 percent EBITDA margin business, that is approximately $1.3 million of revenue equivalent – six weeks of operating output erased by one buyer’s filing.

The exposure compounds when the same operator runs concentrated finance-tier exposure. An aggregator selling to three direct-sale installers all funded by the same loan platform, for example, faces correlated default risk because the platform’s collapse takes all three buyers’ liquidity at once. Mosaic’s June 2025 Chapter 11 was exactly this scenario: installers dependent on Mosaic loan funding lost capacity to close deals during the case, which compressed lead conversion rates across the dependent installer set. Counterparty risk in residential solar has both direct (the buyer files) and indirect (the buyer’s financier files) exposure paths.

What makes solar distinct from other lead-gen verticals is the absence of the regulatory and capital-structure protections that limit default rates elsewhere. Auto and home insurance buyers are state-regulated carriers carrying AM Best ratings and statutory reserves, producing aggregator-AR default rates below 0.5 percent in normal cycles. Medicare advantage buyers face CMS marketing-rule risk but are well-capitalized health plans. Mortgage buyers cycle but are bank-regulated. Residential solar installers and TPO providers, by contrast, are unrated private companies operating with thin equity, large operating-lease and ABS exposure, and dependence on a tax-credit structure Congress just sunset. The vertical’s counterparty profile is the most adverse in U.S. lead generation as of April 2026.

Distress Signal Proxies – What Was Visible Before the Filing

The Freedom Forever filing was preceded by three observable signals on a 90-to-120 day window. Aggregators monitoring counterparty health systematically would have caught all three before the petition.

Workforce and market-footprint contraction. Freedom Forever announced approximately 20 percent workforce reductions in early 2026 and exited 10 of its state markets, down from a claimed 3,000-plus employees and 35-state footprint announced in August 2025. State exits are a stronger signal than headcount because they reflect a board-level decision that a market’s unit economics no longer support fixed cost. The signal is publicly traceable through state contractor-license withdrawal filings, BBB office closures, LinkedIn employee location data, and trade-press coverage.

Regulatory enforcement. The Texas Attorney General named Freedom Forever in a Civil Investigative Demand on April 3, 2026, twelve calendar days before the Chapter 11 petition. State AG enforcement in residential solar has accelerated through 2024 and 2025, and the relationship between AG action and bankruptcy is mechanical: a CID or assurance of voluntary compliance triggers legal-cost increases and customer-acquisition friction precisely when liquidity is thinnest. State AG dockets are public; aggregators can monitor them on a weekly cadence at near-zero cost. Buyers on the receiving end of an active AG matter should trigger immediate credit review.

Trade-payable concentration with a finance partner. Freedom Forever owed approximately $114 million to Mosaic Funding, an unusually large balance to a single finance partner. Trade-payable balances of that scale signal that the installer is using vendor financing as working capital, which is a leading indicator of liquidity stress. Aggregators with access to D&B PAYDEX scores or Experian Business Credit Reports can observe trade-payable trends quarterly, and the cost of those reports is trivial against the size of the AR being protected.

A complete distress-signal monitoring stack for solar buyers includes: D&B PAYDEX or Experian Business credit pulls quarterly for buyers above 5 percent revenue concentration; LinkedIn workforce-trend monitoring monthly; state AG and FTC enforcement docket scans weekly; trade-press scrape (PV Magazine, Solar Power World, PV-Tech, Utility Dive, Law360 bankruptcy alerts) daily; financial-statement review (audited or compiled) annually for buyers above 10 percent revenue concentration. Total annual cost of this stack runs $15,000 to $40,000 for an operator at the $20 million revenue tier – an order of magnitude smaller than a single uncovered counterparty loss. The discipline is mechanical, not heroic.

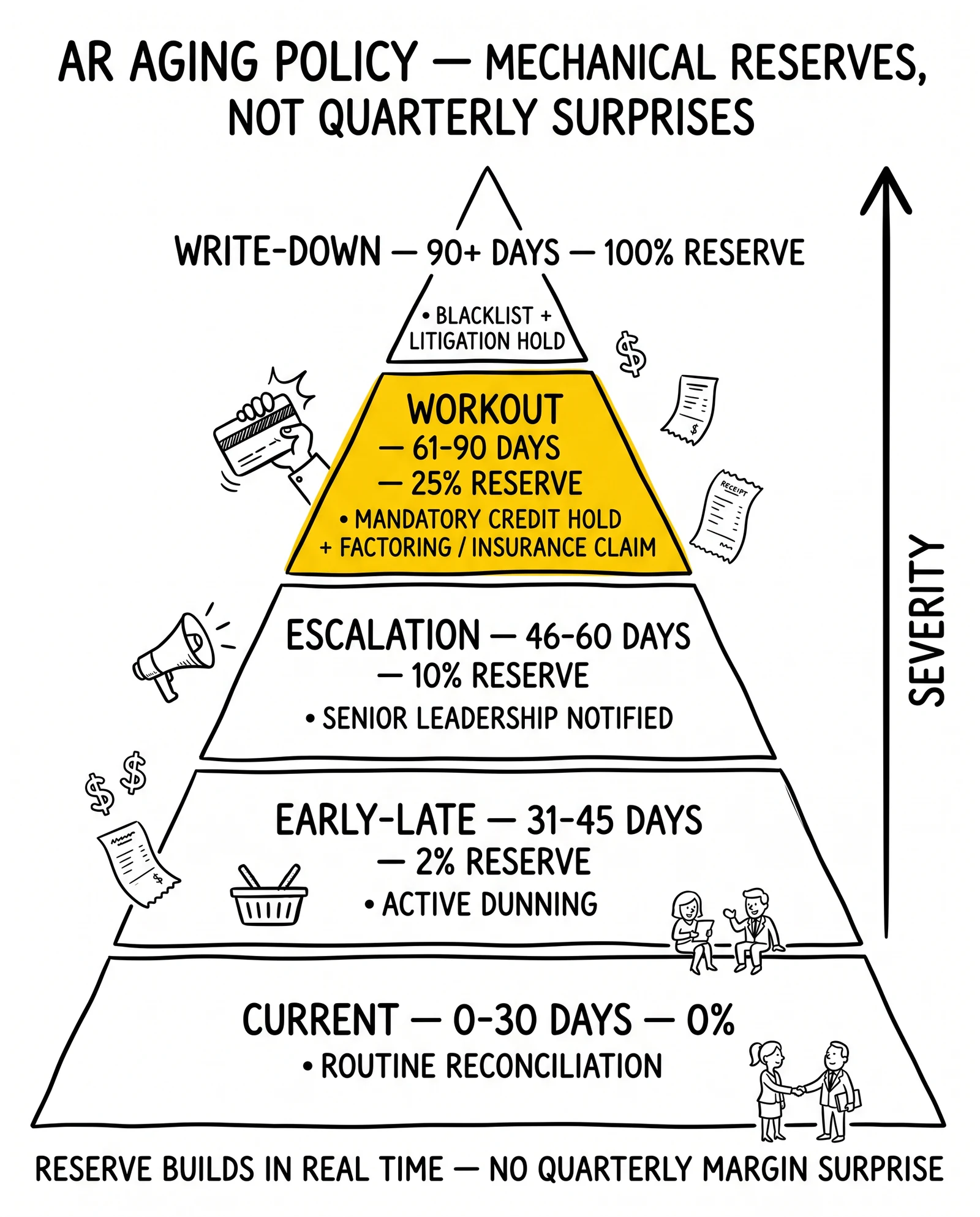

Rewriting AR Aging Policy for the Post-Cascade Market

Standard 2023-vintage AR aging policy in lead generation runs a single 60-day clock and treats anything past 60 as “collections.” That policy was tolerable when solar buyers carried 1-2 percent default rates. With the post-cascade environment likely producing default rates of 5 to 10 percent on residential solar installer AR, aging policy needs a tighter set of triggers and a written escalation path. The five-tier policy below is now operator-standard among solar aggregators that have rebuilt credit policy since the SunPower filing.

| Bucket | Days outstanding | Status | Required action |

|---|---|---|---|

| Current | 0-30 | Standard | No action; routine reconciliation |

| Early-late | 31-45 | Dunning | Automated reminder day 31; AR phone outreach day 38; written notice day 45 |

| Escalation | 46-60 | Active | Sales/AR joint call to controller-level contact; credit hold considered; senior leadership notified |

| Workout | 61-90 | Hold/factor | Mandatory credit hold on new shipments; promissory note or payment plan negotiation; non-recourse factoring or trade credit insurance claim filed |

| Write-down | 90+ | Charge | Full write-down on the books; legal collection or litigation hold; counterparty placed on internal blacklist |

The tightening over 2023 policy is in two places. First, the 31-45 bucket is treated as active dunning, not “still current,” because in a stressed-buyer environment the difference between an invoice paid on day 32 and one paid on day 44 is meaningful information. Second, the 61-90 bucket triggers mandatory credit hold and either factoring or insurance claim activity, not collections-by-quarter-end. The principle is that a residential solar installer paying 75 days on an invoice in 2026 has a non-trivial probability of being in or near restructuring, and continued unsecured shipment is a discretionary decision requiring senior approval, not a default behavior.

The aging policy connects to general-ledger discipline. Operators carrying solar installer AR should book a counterparty reserve on every invoice over 30 days outstanding – a mechanical reserve at, say, 2 percent of balance for the 31-45 bucket, 10 percent for 46-60, 25 percent for 61-90, and 100 percent for 90-plus. The reserve is non-cash but produces accurate margin reporting in real time and avoids the all-at-once charge that follows a buyer’s petition. Lender covenants based on EBITDA respond better to a steady reserve build than to a quarterly surprise, and ownership distributions should reflect reserved-out economics, not gross AR.

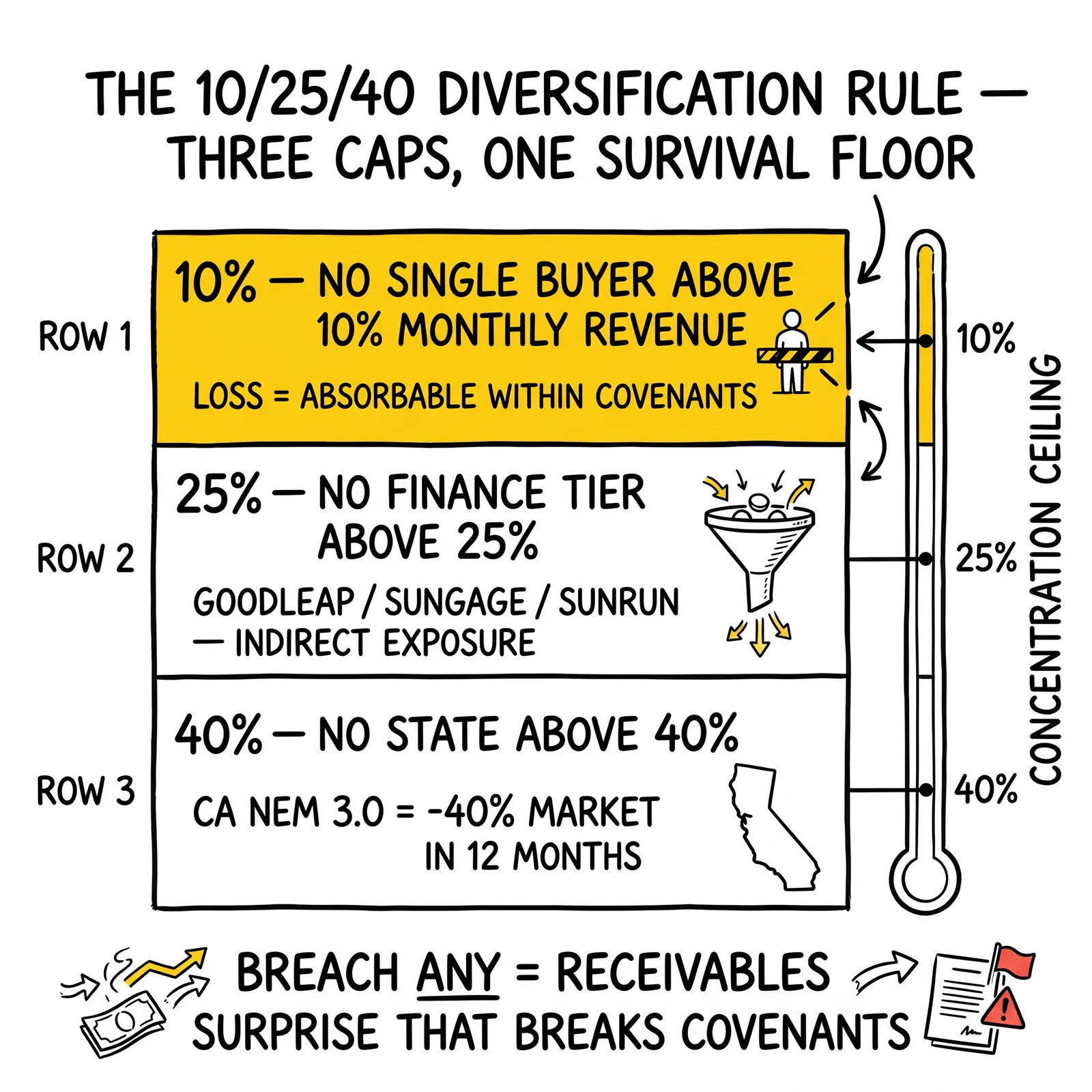

The 10/25/40 Diversification Rule

Three concentration limits frame buyer-roster construction in solar lead operations after April 15, 2026. The numbers are not arbitrary – they reflect the observed correlation structure in residential solar counterparty failures.

No buyer above 10 percent of monthly revenue. The 10 percent cap is calibrated to the largest single-counterparty loss the business can absorb without violating typical bank covenants, missing payroll, or triggering owner cash-call. A 10 percent buyer who files and recovers 5 cents on the dollar produces approximately a 9.5 percent revenue charge; the same buyer at 18 percent concentration produces a 17 percent charge that crosses most covenant thresholds. Operators should run a quarterly concentration report and have a written plan to either grow the denominator or reduce the numerator when any buyer crosses 8 percent on a trailing-three-month basis.

No finance tier above 25 percent. Finance-tier concentration is the indirect-exposure version of the rule and is more often missed. An aggregator selling leads to four installers, three of whom fund through GoodLeap and the fourth through Sungage, has 75 percent finance-tier concentration on GoodLeap. If GoodLeap pulls back funding for any reason – and the precedents now exist – those three installers’ close rates collapse simultaneously. The 25 percent cap forces explicit roster diversification across at least four finance platforms.

No state above 40 percent. Geographic concentration is calibrated to single-state policy shock risk. California’s NEM 3.0 transition in April 2023 compressed the state’s residential market by approximately 40 percent within twelve months. State-by-state net metering rule changes, contractor-licensing reforms, and AG enforcement priorities can produce demand contractions of similar magnitude. Holding any single state below 40 percent of revenue means a single-state policy shock damages margin without taking the operator below cash-flow breakeven. California, Texas, Florida, Arizona, the Northeast PJM cluster, and the Mid-Atlantic each represent natural concentration points and should be monitored individually.

The three caps are floor numbers, not aspirations.

Contract Hardening – ACH, Escrow, Bonds, Personal Guarantees

The contract template residential solar aggregators were running in 2023 – net-30 terms, 30-day termination right, no security, no covenant – was acceptable when the worst-case counterparty was a 2-percent annual default rate. It is not acceptable in the post-cascade environment. Five contract changes apply, and operators should renegotiate every active solar buyer contract on its next renewal cycle.

Shorten payment terms by credit tier. ACH-on-delivery is the new default for any buyer below an internal credit threshold (D&B PAYDEX below 70, no audited financials, less than two years of operating history, or revenue concentration above 8 percent). Weekly settlement is the default above the threshold, with net-30 reserved for buyers carrying audited financials, investment-grade-equivalent metrics, or trade credit insurance pre-coverage. The friction cost of weekly settlement is roughly 10 to 15 minutes of additional AR labor per buyer per week – trivial against single-buyer loss exposure.

Require security from sub-investment-grade buyers. Three security forms are appropriate: a personal guarantee from the controlling owner, an escrow deposit equal to 30 days of historical purchases, or a performance bond from a rated surety. The choice depends on buyer balance sheet and aggregator leverage. Personal guarantees from owners of closely-held installers were standard practice in the 1990s lead-gen market and should be standard again. The owner who refuses to personally guarantee a relationship is signaling a counterparty-risk read that the aggregator should respect.

Five-day suspension right on missed payment. The 30-day cure period customary in 2020-vintage contracts is calibrated to a normal-cycle counterparty and produces unacceptable exposure when the counterparty is in liquidity stress. A five-business-day suspension right with written notice gives the seller the operational ability to stop shipping into a deteriorating counterparty before the loss compounds. Buyers will negotiate for ten or fifteen days; the seller’s floor should be five.

Most-favored-nation pricing clause. Lead pricing in residential solar is fragmenting as TPO providers absorb market share from direct-sale installers and as the shrinking 2026 market produces new pricing pressure. An MFN clause guarantees the seller the best price offered to any other buyer for an equivalent lead spec, which prevents margin compression on existing buyers when the seller acquires a new buyer at a higher rate.

Financial-covenant trigger. A liquidity-based covenant – for example, a representation that the buyer maintains unrestricted cash plus available credit equal to or greater than 30 days of operating expense, with breach producing automatic conversion to ACH-on-delivery – gives the seller a contractual hook into the buyer’s deterioration well before formal default. Buyers will resist this clause; the aggregator’s negotiating position is that the alternative is no credit, period. Many will accept the covenant in exchange for the credit terms.

These contract changes also align with the broader operator discipline covered in credit and payment terms in lead transactions and the working-capital framework in cash flow management for lead generation businesses. The post-cascade environment converts these from optional best practices to baseline policy.

Trade Credit Insurance and Non-Recourse Factoring

Two financial products convert installer counterparty risk from a residual operator exposure into a priced and transferred risk. The choice between them depends on capital structure, working capital appetite, and the operator’s view on whether premium cost or factor’s discount is the more efficient way to pay for credit protection.

Trade credit insurance. Carriers including Allianz Trade, Coface, Atradius, AIG Trade Credit, and Chubb underwrite policies that pay out on commercial buyer insolvency or protracted default. Pricing for diversified portfolios runs 0.10 to 0.50 percent of insured turnover, with concentrated solar-installer portfolios likely priced toward the upper end given 2024-2025 loss history. For a $20 million annual solar lead operation with $1.5 million in average outstanding AR, full coverage runs roughly $30,000 to $75,000 per year. The carrier underwrites each named buyer to a credit limit, and coverage is contingent on the seller continuing to ship within the limit and within the carrier’s payment-terms requirements. Claims are typically settled at 80 to 90 percent of the insured loss after a defined waiting period (often 90 to 180 days from default).

The decision logic is mechanical. Operators running on lines of credit with debt-to-EBITDA covenants generally find the premium economically rational because the policy converts a binary loss event into a smoothed cost line that does not break covenant. Bootstrapped operators with large equity cushions sometimes self-insure on the calculation that the premium exceeds expected loss times claim probability. The post-cascade default-rate environment shifts the math toward purchasing the policy: a 5 percent expected default rate on $1.5 million of AR is $75,000 of expected loss before recovery, which is higher than the upper bound of premium cost.

Non-recourse factoring. Factors purchase the receivable outright at a discount and assume the credit risk. Pricing in solar installer AR runs roughly 1 percent per month on the advance plus a factor’s guarantee fee for the credit assumption, totaling effective costs of 14 to 22 percent annualized depending on tenor and buyer credit. The factoring decision is more attractive than insurance when the operator also needs working capital – factoring delivers liquidity and credit protection in a single instrument, where insurance delivers only credit protection. Operators with strong cash positions and lender lines should generally prefer insurance; operators with constrained cash should evaluate factoring on a buyer-by-buyer basis.

A hybrid approach is increasingly common: insurance on the top three to five buyers (covering 60-70 percent of AR), and factoring on individual buyers below that threshold or those declined by the insurer. The insurer’s underwriting decision is itself information – a carrier that declines coverage or sets a tight limit on a buyer is signaling a credit view the operator should incorporate into its own concentration policy.

The TPO Pivot and the New Buyer Roster

The Section 25D expiration and the installer cascade have together produced a structural shift in who can profitably buy residential solar leads in 2026. Direct-sale installers operating on customer-owned loan economics are the most exposed cohort and contain most of the cascade casualties. Third-party-owned (TPO) providers operating on Section 48E credit economics through 2027 are the surviving capacity. Aggregators who do not rebuild buyer rosters around TPO providers will see acceptance rates and margins decline through 2026.

The post-Freedom Forever buyer roster centers on six TPO providers. Sunrun is the market leader at approximately 12 percent national share, primarily lease and PPA. GoodLeap combines TPO provision with origination platform services and has expanded its direct lease product. Palmetto LightReach provides subscription-style TPO to the Palmetto installer network and third-party installers. EverBright is the NextEra Energy TPO platform serving installer partners. Sungage Financial has historically focused on loan but has expanded TPO capacity post-25D. Solar Servicing, the Forbright Bank subsidiary that acquired Mosaic’s loan platform in September 2025, services the legacy Mosaic loan book and is positioning for ongoing originations. The second tier includes regional TPO providers and the surviving direct-sale installers.

The TPO pivot also requires a lead-spec rewrite. TPO underwriting boxes are tighter than the direct-sale loan boxes that dominated 2022-2024 lead specs. The operator-standard TPO spec now reads roughly: FICO 650-plus for lease (some carriers 660), 680-plus for PPA, homeowner of record (not a deeded-for-value transfer), property in a TPO-eligible state, current utility provider that allows third-party generation, and minimum monthly utility bill of $80. Aggregators filtering to direct-sale loan boxes (FICO 640, $60 utility bill, broader homeowner definitions) will see TPO acceptance rates collapse without rewrites, and the lead-quality cost of filtering tighter at the top of funnel is a 15 to 25 percent reduction in marketable lead volume from the same media spend.

The competitive dynamics for the operator overlap with the strategic playbook in Tesla, Sunrun, and customer acquisition strategies and the financing-product framework in solar financing loan options and lead qualification. The principle that holds across both is that the TPO buyer’s lifetime customer economics support a higher CPL than the loan buyer’s, but only at the higher quality threshold – paying TPO CPL on loan-spec leads is the fastest way to lose the buyer relationship.

Lead-Spec Rewrite, Pricing, and Geographic Reallocation

The combined effect of the bankruptcy chain, the Section 25D expiration, and the TPO pivot is that the lead spec, the price-per-lead, and the state-mix that worked in 2024 are all wrong for 2026. Aggregators rebuilding their solar operation should rewrite each input on the basis of post-cascade reality, not residual assumptions from the customer-owned-loan era.

Spec rewrite. TPO-grade specs (FICO 650-plus lease / 680-plus PPA, $80-plus utility, homeowner of record in TPO-eligible state) become the default. The aggregator should publish a tiered rate card: TPO-grade at the top tier, “loan-grade” (FICO 640-plus, $60-plus utility) at a discount, and “general inquiry” leads sold at a deep discount or returned. The tiering creates pricing power because TPO-grade leads command 30 to 50 percent premiums over loan-grade in the post-cascade market.

Pricing recalibration. Post-cascade CPLs in residential solar reflect Wood Mackenzie’s projected 40 percent customer-acquisition cost spike for 2026. Aggregators should recalibrate their CPL targets upward proportionally and resist the temptation to buy share with below-market pricing – the downstream margin compression is structural, and competing on price into a contracting market produces volume without profitability. State-by-state CPL benchmarks are covered in solar lead CPL by state for 2025 pricing, with the post-25D corrections applying as a roughly uniform 30 to 40 percent uplift across the table.

Geographic reallocation. The 40 percent state cap from the 10/25/40 rule forces explicit geographic diversification. Operators heavily concentrated in California should rebuild Texas, Florida, Arizona, and Northeast PJM exposure. Operators concentrated in the Northeast should rebuild Sun Belt exposure. The purpose is not to chase the highest-CPL state but to limit single-state policy-shock exposure. The state-level analysis in solar incentive changes and lead generation 2025 provides a starting framework for which state markets carry which residual incentive structures.

The lead-quality dispute frequency rises in a stressed-buyer environment because installers under liquidity pressure use disputes to delay payment. Aggregators should review the contractual return-rate caps and dispute-window terms covered in managing lead quality disputes with vendors, and should treat any sustained spike in dispute rate from a specific buyer as a counterparty-distress signal in addition to a quality-control issue. Distressed buyers consistently increase dispute volumes 60 to 90 days before payment failure.

Operating Discipline Through the Reset

The bankruptcy chain that ends (provisionally) with Freedom Forever’s Chapter 11 was driven by structural forces – tax credit expiration, capital-cost reset, regulatory enforcement intensity – that will not reverse in 2026 or 2027. Section 25D is not coming back. Section 48E expires at the end of 2027 and has its own cliff risk. State-level NEM and net-metering reform continues. The residential solar lead market that emerges from the reset will be smaller, more TPO-concentrated, more credit-disciplined, and more demanding of operator counterparty-risk management. Aggregators who treat that environment as the new baseline rather than a temporary disruption will operate profitably through it.

The pre-cascade operator playbook had three points of leverage: media efficiency, conversion optimization, and buyer-roster scale. The post-cascade playbook adds a fourth that is now equal in weight: counterparty-risk policy. The operator who ranks counterparty discipline below the other three will eventually deliver a quarter where a single buyer’s filing erases two months of media-efficiency gains. The operator who builds the policy stack described above – distress monitoring, AR aging tiers with mechanical reserves, the 10/25/40 diversification rule, hardened contracts with security and covenants, trade credit insurance or non-recourse factoring on the largest exposures, and a TPO-pivoted buyer roster with rewritten specs – converts counterparty risk from an unmanaged residual into a priced and bounded line item.

That conversion is the difference between operating through the next residential solar cycle and being the next case study.

Key Takeaways

-

Freedom Forever’s April 15, 2026 Chapter 11 closes a 24-month residential solar bankruptcy chain spanning ten major events, including SunPower, Sunnova, Mosaic, Lumio, PosiGen, and Titan. Operators should treat the cascade as a permanent reset of vertical counterparty risk, not a temporary disruption, and rebuild policy on that basis.

-

The Section 25D expiration on December 31, 2025 is the structural driver of the cascade, and Section 48E’s 2027 cliff is the next visible risk on the horizon. Buyer rosters built around customer-owned loan economics are now structurally exposed; rosters built around TPO providers (Sunrun, GoodLeap, Palmetto LightReach, EverBright, Sungage, Solar Servicing) align with the surviving capital structure through 2027.

-

The 10/25/40 rule (10 percent buyer cap, 25 percent finance-tier cap, 40 percent state cap) is the new operator-standard diversification floor, not an aspiration. Aggregators above any threshold should write a quarterly concentration report and escalation plan, and tightening above the floor (8 percent buyer, 20 percent finance tier) is appropriate for operators with leverage to negotiate it.

-

AR aging policy needs five tiers, not two: current (0-30), early-late (31-45 with active dunning), escalation (46-60 with senior involvement), workout (61-90 with mandatory hold and factoring or insurance claim), and write-down (90-plus, full charge). The mechanical reserve build at 2/10/25/100 percent across the late buckets keeps margin reporting accurate in real time and preserves lender-covenant headroom.

-

Distress signals are observable on a 90-to-120 day window before filing. Workforce contraction, state-market exits, AG enforcement actions, and trade-payable concentration with a finance partner all preceded Freedom Forever’s filing. A $15,000 to $40,000 annual monitoring stack covers this for an operator at the $20 million revenue tier – an order of magnitude smaller than a single uncovered counterparty loss.

-

Contracts must be rewritten with five changes: ACH-on-delivery for sub-investment-grade buyers, security in the form of personal guarantee or escrow or bond, five-business-day suspension right on missed payment, MFN pricing clause, and a financial-covenant trigger that converts to ACH on liquidity breach. The 30-day cure periods customary in 2020-vintage contracts produce unacceptable exposure under post-cascade default rates.

-

Trade credit insurance at 0.10 to 0.50 percent of insured turnover and non-recourse factoring at roughly 1 percent per month plus guarantee fee are the two financial products that convert counterparty risk into a priced and transferred line item. The hybrid pattern – insurance on top buyers, factoring on smaller exposures – is operator-standard; the insurance carrier’s underwriting decision is itself credit-view information.

-

Lead-spec rewrites are non-negotiable in the TPO pivot. The operator-standard TPO spec is FICO 650-plus lease / 680-plus PPA, homeowner of record, $80-plus utility bill, in a TPO-eligible state. Aggregators continuing to filter to direct-sale loan-grade specs will see acceptance rates collapse without realizing why.

-

Recovery on unsecured pre-petition AR in residential solar Chapter 11s has clustered at 1 to 20 percent, with most cases at the low end. The accounting decision is to write down 100 percent of pre-petition exposure on the petition date and reverse the charge if and when a distribution occurs. Treating recovery as zero in operating cash forecasts produces accurate planning.

-

Counterparty-risk policy is now equal in operator weight to media efficiency, conversion optimization, and buyer-roster scale. The pre-cascade three-point playbook is incomplete in 2026. The four-point playbook – adding counterparty discipline – converts solar lead operations from a vertical with episodic balance-sheet damage to one with a priced and bounded risk line.

Sources

- PV Magazine USA, “Residential solar company Freedom Forever files chapter 11 bankruptcy,” April 15, 2026 – pv-magazine-usa.com

- Solar Power World, “Residential solar installer Freedom Forever files bankruptcy,” April 2026 – solarpowerworldonline.com

- PV-Tech, “Freedom Forever files for Chapter 11 bankruptcy with $500 million debts,” April 2026 – pv-tech.org

- Law360, “Solar Co. Freedom Forever Hits Ch. 11 With Over $500M Debt,” April 2026 – law360.com

- PV Magazine, “Sunnova files for bankruptcy,” June 10, 2025 – pv-magazine.com

- PV Magazine USA, “Bankrupt residential solar loan provider Mosaic to be acquired,” September 25, 2025 – pv-magazine-usa.com

- PV Magazine USA, “Residential solar installer Posigen files for bankruptcy,” December 8, 2025 – pv-magazine-usa.com

- Utility Dive, “SunPower files for bankruptcy, plans to sell or wind down remaining operations,” August 2024 – utilitydive.com

- SEIA / Wood Mackenzie, “Solar Market Insight Report Q4 2025,” December 2025 – seia.org

- Wood Mackenzie, “Outlook for US solar worsens under the OBBBA,” 2025 – woodmac.com

- Internal Revenue Service, “FAQs for modification of sections 25C, 25D, 25E, 30C, 30D, 45L, 45W, AND 179D under Public Law 119-21 (OBBB),” 2025 – irs.gov

The next residential solar cycle will be smaller, TPO-concentrated, and unforgiving of operators who carry 2023-vintage counterparty policy into a 2026 default-rate environment. The policy stack is mechanical, the costs are bounded, and the alternative is being the case study in someone else’s article.