Pilots that promised to replace a sixty-thousand-dollar SDR are dying at the bulk-sender threshold and the brand-safety screenshot - usually before the third invoice clears.

The 11x exposé that broke the category open

On March 24, 2025, TechCrunch reporter Marina Temkin published an investigation that did more damage to the AI SDR category in a single afternoon than any analyst report had managed in the prior eighteen months. The headline was direct: a16z and Benchmark-backed 11x had been claiming customers it did not have. The story named ZoomInfo and Airtable explicitly as non-customers whose logos appeared on 11x.ai’s marketing materials. ZoomInfo’s spokesperson said the company had spent four months demanding 11x stop using its logo and that a one-month trial had “performed significantly worse than our SDR employees.” Airtable confirmed it was never a customer and had never given 11x permission to use its logo. Nearly two dozen sources - investors and current and former employees - told the publication that gross retention was tracking below 50 percent, that the company was burning cash faster than its annual recurring revenue line implied, and that early customers were reporting deliverability collapse and brand-safety incidents from the Alice and Jordan agents.

The exposé hit a category that had been priced and funded on a single narrative: AI replaces a $60,000 SDR. 11x.ai had raised at unicorn-adjacent valuations on that pitch. So had Artisan, whose Ava agent ran prime-time billboard campaigns in San Francisco with the line stop hiring humans. Reggie, AiSDR, and a long tail of seed-stage challengers built the same wedge. By Q1 2025 the category looked like a winner-takes-most race; by Q2 2025 the procurement teams that had signed those pilots were calculating how to escape contracts, and the operator-facing publications - ProductGrowth, OnlyCFO, UserGems, Coldreach, Michael Saruggia’s newsletter - were running post-mortems instead of buyer guides.

Twelve months later the cancellation rate triangulates to roughly 50 to 70 percent inside 90 days for managed AI SDR contracts. UserGems publicly reports AI SDR tool churn at 50 to 70 percent annually - roughly double the turnover rate of the human SDRs the tools were pitched to replace - and the operator-side post-mortems on G2, Trustradius, and Reddit suggest the bulk of that churn lands inside the first contract cycle rather than spread across the year. Operator-reported tenure on managed AI SDR programs varies widely; many pilots fail before reaching six months, and very few progress to expanded seat counts. The category is not slowly stabilizing - it is failing at scale, and the failures share three structural fingerprints that the buyer guides published in 2024 and early 2025 systematically underweighted.

This is the post-mortem. The site already runs an AI SDR tools buyer guide covering the leading platforms and their stated capabilities. What follows is the failure forensics: why pilots die, which vendors are driving the cancellation rate, what the surviving 30 percent of programs do differently, and the hybrid playbook that survives contact with sender reputation, hallucination risk, and the actual math of an AE’s calendar.

Three structural failure modes

Every AI SDR cancellation report on G2 and Trustradius, every postmortem on Reddit’s r/sales and r/sales_engineering, and every operator interview that surfaced through 2025 and 2026 lands on some combination of three failure modes. The categories are not exotic. They show up in older email-marketing failures and in the offshore-SDR collapse of the late 2010s. What is new is that AI scales each of them faster than human teams could, and that the cancellation surface area is larger because the vendor pitched autonomy.

Bad data infrastructure

The first failure mode is data. Managed AI SDR vendors typically train their persona models and outreach copy on a combination of scraped LinkedIn profiles, third-party intent data, and the customer’s own CRM exports. None of those sources are clean. LinkedIn profiles overstate seniority by roughly 20 percent and are stale on title changes by a median of seven months. Intent data from Bombora, G2 Buyer Intent, and similar sources runs at 30 to 40 percent precision when measured against actual buyer behavior. CRM exports from Salesforce and HubSpot inherit every bad row the customer’s inside-sales team has logged for the prior five years. When a vendor pipes that compound mess into an LLM and generates outreach copy at scale, the result is what operators have started calling confidently irrelevant - the AI writes a fluent, well-structured email to the wrong person about a product they do not buy, citing a company fact that is no longer true.

Operators on G2 describe receiving outreach from their own AI SDR agents addressed to former employees, naming product lines that had been sunset two quarters earlier, or referencing fundraising rounds that had not happened. The Coldreach 2026 AiSDR review reported a hallucination rate of 12 to 18 percent of generated emails containing at least one factually incorrect company-specific claim. The Michael Saruggia post-mortem cited a hallucination rate above 20 percent on a controlled test set against 11x.ai’s Alice agent. None of these numbers survive contact with a brand-conscious enterprise procurement team. A 12 percent hallucination rate against 5,000 daily sends is 600 confidently wrong emails per day, each carrying brand-safety risk, each one a potential screenshot.

Deliverability collapse

The second failure mode is deliverability. AI SDR vendors typically pitch volume as a primary value driver - one customer recently cited a vendor proposing 1,500 unique outbound emails per day per agent across 5 to 10 mailbox aliases. That volume profile maps directly onto the bulk-sender thresholds Google and Yahoo introduced in February 2024 and tightened in 2025. Senders pushing more than 5,000 messages per day to Gmail addresses must keep spam complaint rates below 0.3 percent, maintain valid SPF, DKIM, and DMARC authentication with strict alignment, support one-click unsubscribe, and avoid the volume-spike patterns the providers’ machine-learning systems flag as bulk. AI SDR programs that ramp from zero to several thousand sends per day inside a 30-day pilot break that pattern almost immediately.

The Google postmaster tools dashboard tells the story across hundreds of cancellation cases reported on Reddit and operator forums. A new sender domain ramps cleanly through the first week. Spam complaint rate ticks past 0.3 percent in week two as recipients flag the AI-generated copy as low-quality bulk. The IP reputation indicator drops from high to medium, then medium to low, by week three. By week four the inbox placement rate has fallen below 60 percent and the cost-per-meeting has tripled because reply rate scales with deliverability. The operator either kills the program or bleeds another six weeks before killing it. The same arc plays out on Yahoo, Microsoft, and Apple’s iCloud filters. The full set of provider rules sits in the Gmail and Yahoo bulk-sender requirements and the 2026 update to email deliverability best practices, which together codify the 0.2 to 0.3 percent complaint thresholds, the authentication alignment requirements, and the volume-ramp curves that human-led sequencing programs build around and AI SDR vendors routinely break.

The deliverability math is what kills the pricing argument. The economic claim - that AI replaces a $60,000 SDR at $5,000 per month or $60,000 per year - assumed inbox placement at 90 percent or better and reply rates around 4 to 6 percent. With inbox placement at 60 percent and reply rates collapsing to 0.5 to 1.5 percent, the cost per meeting moves from roughly $35 to roughly $200, and the program no longer pencils against a human SDR running tighter volume from a warmed sender domain. The vendor cannot fix this with better copy or a different LLM. The constraint is the sender reputation curve, which is a function of recipient behavior, not of model quality.

Brand-risk hallucinations

The third failure mode is brand risk. Hallucinated outreach generates screenshots, and screenshots travel. The most-cited 2025 case was the Alice agent’s outreach to a CTO at a mid-market SaaS company that opened with a fake compliment about a fundraising announcement that had never happened. The recipient posted the screenshot to LinkedIn. The post got 4,000 reactions and 600 comments. Two of the comments came from active 11x.ai customers, one of whom canceled the contract within 48 hours. Artisan’s Ava agent generated a similar pattern through 2025: invented shared connections, fabricated company facts, and wrong-persona outreach where the AI matched a buyer profile to an obviously irrelevant target account. By Q1 2026, LinkedIn’s pattern detection systems had begun rate-limiting Ava-driven activity, and Artisan reportedly faced enforcement actions on automated outreach volume that further compressed the platform’s economic case.

The brand-risk fingerprint is harder to quantify than deliverability because the cost is reputational rather than directly attributable. But every general counsel and CMO who has reviewed a hallucinated-outreach screenshot has applied the same calculus: the upside of an AI SDR program is incremental pipeline, the downside is a viral brand-safety incident, and incremental pipeline does not justify viral downside. The FTC’s settlement with Air AI - complaint filed August 2025, settlement announced March 24, 2026 - hardened that calculus into procurement law. The agency banned Air AI Technologies and its owners from selling or marketing any business opportunity, secured an $18 million monetary judgment (largely suspended on inability to pay, with $50,000 actually paid for consumer relief), and required substantiation of any future AI capability claims, applying to AI sales tooling the same playbook it has used against income-claim violators in network marketing for two decades. General counsels now have a concrete reference point for evaluating vendor marketing claims before signing managed-program contracts.

| Failure mode | Leading indicator | Mitigation |

|---|---|---|

| Bad data infrastructure | Hallucination rate above 5% on validation set | Pre-purchase hallucination audit on held-out targets; refuse vendors above 5% |

| Deliverability collapse | Spam complaint rate above 0.2% in week 2 | Cap volume at 200/day per mailbox; warm domains 30 days before send |

| Brand-risk hallucination | Any wrong-persona send in pilot | Manual review queue on first 1,000 sends; kill switch on hallucinated content |

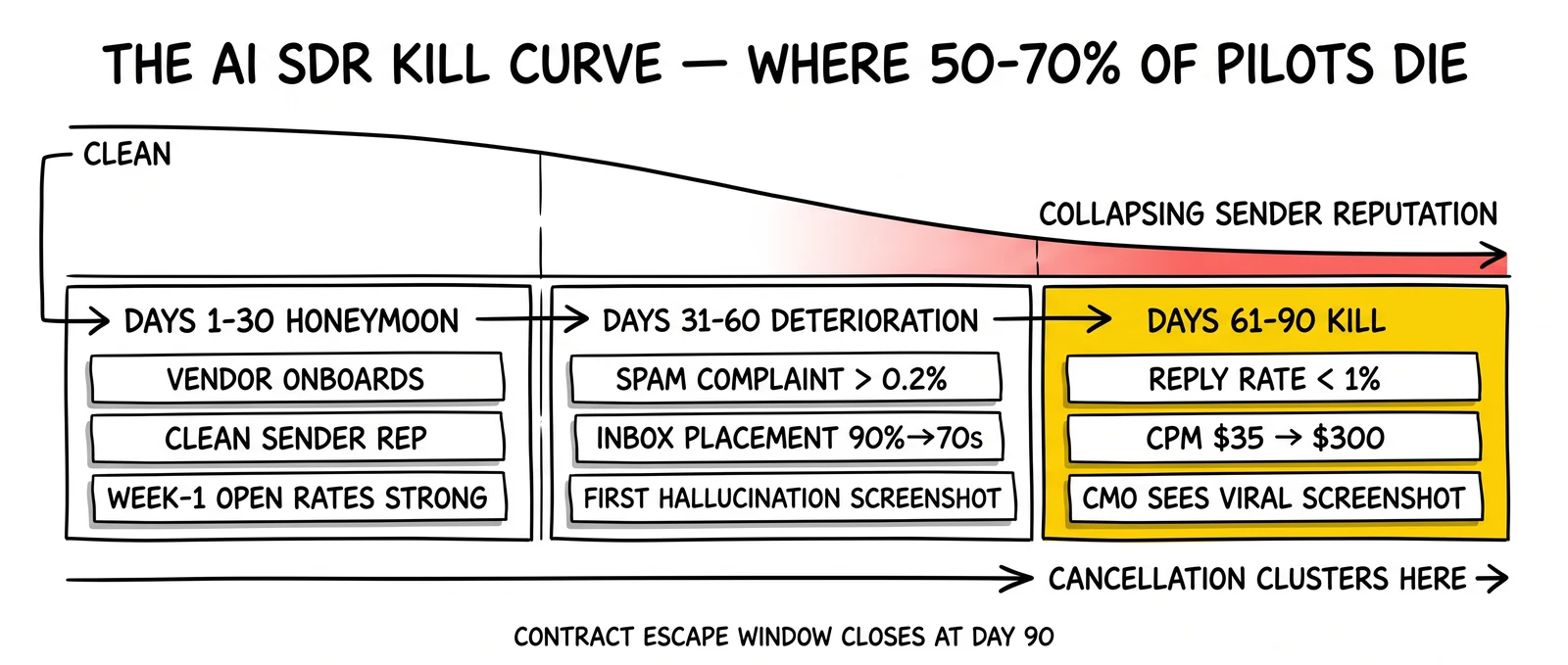

The 90-day kill curve

The cancellation pattern has a shape. Operators rarely kill an AI SDR pilot in the first 30 days because the contract is paid, the procurement team has political capital invested, and the vendor’s customer success motion is at peak engagement. Cancellations cluster between days 60 and 90, the period when the deliverability data has fully developed, the AE team has rejected enough AI-set meetings to surface the conversion gap, and the brand-safety incidents have accumulated past the threshold a CMO will tolerate.

The kill curve breaks into three phases. Days 1 through 30 are the honeymoon. The vendor onboards the customer, builds the persona definitions, generates the first batch of copy, ramps the sending infrastructure, and reports a strong week-one open rate. The customer’s procurement team forwards the dashboard to leadership. The vendor’s customer success manager is on a weekly cadence. Reply rates look acceptable because the underlying domain reputation is still clean and the volume has not yet pushed past the bulk-sender threshold.

Days 31 through 60 are the deterioration. Deliverability metrics begin to soften. Spam complaint rate ticks above 0.2 percent. Inbox placement drops from above 90 percent to the mid-70s. Reply rates fall by half. The AE team starts pushing back on the quality of AI-set meetings - the prospect on the call does not match the qualification criteria, the meeting was scheduled with a mid-market individual contributor instead of a director, the prospect mentions they got the meeting request because the calendar slot was easy to grab. The first hallucinated-outreach screenshot lands in the customer’s slack channel.

Days 61 through 90 are the kill. The deliverability collapse has fully developed. Reply rates are below 1 percent. Cost per meeting has moved from $35 to $150 to $300. The CMO has seen at least one viral screenshot, the general counsel has a question about indemnity, and the head of revenue is calculating whether the AE team’s time spent on AI-set meetings is producing more pipeline than the same hours spent on inbound or marketing-sourced opportunities. The procurement team triggers the cancellation clause if one exists. If the contract has no escape clause, the customer waits out the term and refuses renewal. Operator-reported cancellations cluster tightly inside the late-second-month-to-third-month window, which is the latest point at which a customer can cancel without giving the vendor an additional renewal cycle to argue for retention.

The 30 percent of programs that survive past 90 days do so for three reasons. They run at human-level volume - 100 to 200 sends per day per mailbox rather than 1,000 to 2,000. They keep a manual review queue between AI generation and send. And they have already migrated AI ownership away from initial outreach into research, enrichment, and scheduling. The hybrid playbook section below covers what that operating model looks like in practice.

Vendor-by-vendor reality check

Five vendors account for the bulk of the public cancellation reports through 2025 and 2026. Each has a distinct failure pattern, and the differences matter for procurement teams trying to read between the lines of vendor pitches.

11x.ai (Alice and Jordan)

11x.ai is the category’s reference case for what cancellation looks like. The company raised from a16z and Benchmark on the SDR-replacement pitch, scaled to claimed eight-figure ARR by mid-2024, and entered 2025 facing the TechCrunch investigation into customer-list inflation and the OnlyCFO follow-up titled AI Company Accused of Fraud. Pricing reportedly sat around $5,000 per month for managed coverage of a single AI SDR program. Gross retention has been reported below 50 percent. The Alice agent handles outbound prospecting; Jordan handles inbound qualification and meeting setting. Operator reviews on G2 and Reddit cluster around three complaints: hallucination rate above the customer’s tolerance threshold, deliverability collapse at the volume the vendor recommended, and customer success teams pushing renewals before the customer had clean data on whether the program was working. The MarketBetter 11x review from 2026 documents a pattern of negotiation tactics around the renewal point that suggest the vendor is fighting hard to retain customers who have already decided to leave. The TechCrunch story remains the most-cited primary source on the company’s actual operating condition.

Artisan AI (Ava)

Artisan ran the most aggressive marketing campaign in the category - billboards in San Francisco with the line stop hiring humans paired with an AI-generated face for the Ava agent. The company raised at strong valuations through 2024 and entered 2025 with brand recognition outsized relative to its operating scale. Through 2025 and into Q1 2026, operator complaints converged on three patterns: hallucinated shared-connection claims (Ava would reference a nonexistent prior conversation or mutual contact), volume that triggered LinkedIn’s pattern-detection systems and led to platform restrictions on Ava-driven outreach, and a customer success motion that pushed contract value rather than program tuning. By Q1 2026 the company reportedly faced enforcement on automated LinkedIn activity that compressed the platform’s economic case further. G2 reviews from 2026 show a sustained negative trajectory.

AiSDR

AiSDR sells a per-message pricing model that initially looks attractive against the flat-rate managed model 11x and Artisan use. The economic structure shifts the deliverability and hallucination risk to the customer rather than the vendor - because the customer pays per send, the vendor has every incentive to encourage volume. The Coldreach 2026 review documented a 12 to 18 percent hallucination rate on a controlled test set and noted that customer complaints about deliverability collapse cluster in the second month of program activity, consistent with the broader 90-day kill curve. AiSDR’s per-message model survives slightly better than the managed-flat-rate model because customers can throttle spend, but the underlying quality issues are the same.

Reggie

Reggie’s autopilot positioning - the AI runs the program with minimal human oversight - draws operator complaints disproportionate to its market share. The autopilot framing accelerates each of the three failure modes because the customer is explicitly told to step back from the program. By the time the customer steps back in to evaluate, the deliverability damage is done, the hallucination patterns have accumulated, and the brand-risk incidents have already happened. G2 review velocity through 2025 and 2026 has been negative, and operator-side coverage has been near-uniformly critical.

Reply.io

Reply.io is the partial counterexample. The company sells AI features as components of a broader sequencing platform rather than as a managed SDR replacement. Customers buy the platform and assemble their own programs, which means the customer owns the volume decisions, the persona definitions, and the brand-safety controls. The vendor’s economic incentive is to keep the customer’s programs working at human-led volume rather than to push for the autonomy claim. Reply.io’s review trajectory through 2025 and 2026 has been more positive than the managed-pure-play vendors, and the customer base has been more stable. The lesson is that the vendor’s pricing and product structure determines which failure modes the customer absorbs, and that platform vendors who sell components rather than autonomy tend to weather the cancellation wave better than managed pure-plays.

| Vendor | Pricing model | Reported gross retention | Primary failure mode | Status |

|---|---|---|---|---|

| 11x.ai (Alice/Jordan) | ~$5,000/mo flat | < 50% | Hallucinations + deliverability + customer-list inflation | Distressed; investor pressure |

| Artisan (Ava) | Flat/seat hybrid | < 60% (est.) | LinkedIn restrictions + brand-risk hallucinations | Distressed; enforcement risk |

| AiSDR | Per-message | < 60% (est.) | Deliverability + hallucinations | Operator complaints sustained |

| Reggie | Flat | Not disclosed | Autopilot framing accelerates all three failure modes | Operator complaints sustained |

| Reply.io | Per-seat platform | Industry-standard SaaS | Customer error (component model shifts ownership) | Stable |

Source: TechCrunch (Mar 24, 2025), OnlyCFO (2025), MarketBetter (2026), Coldreach (2026), G2 review velocity analysis (2025-26), ProductGrowth tenure data (2026).

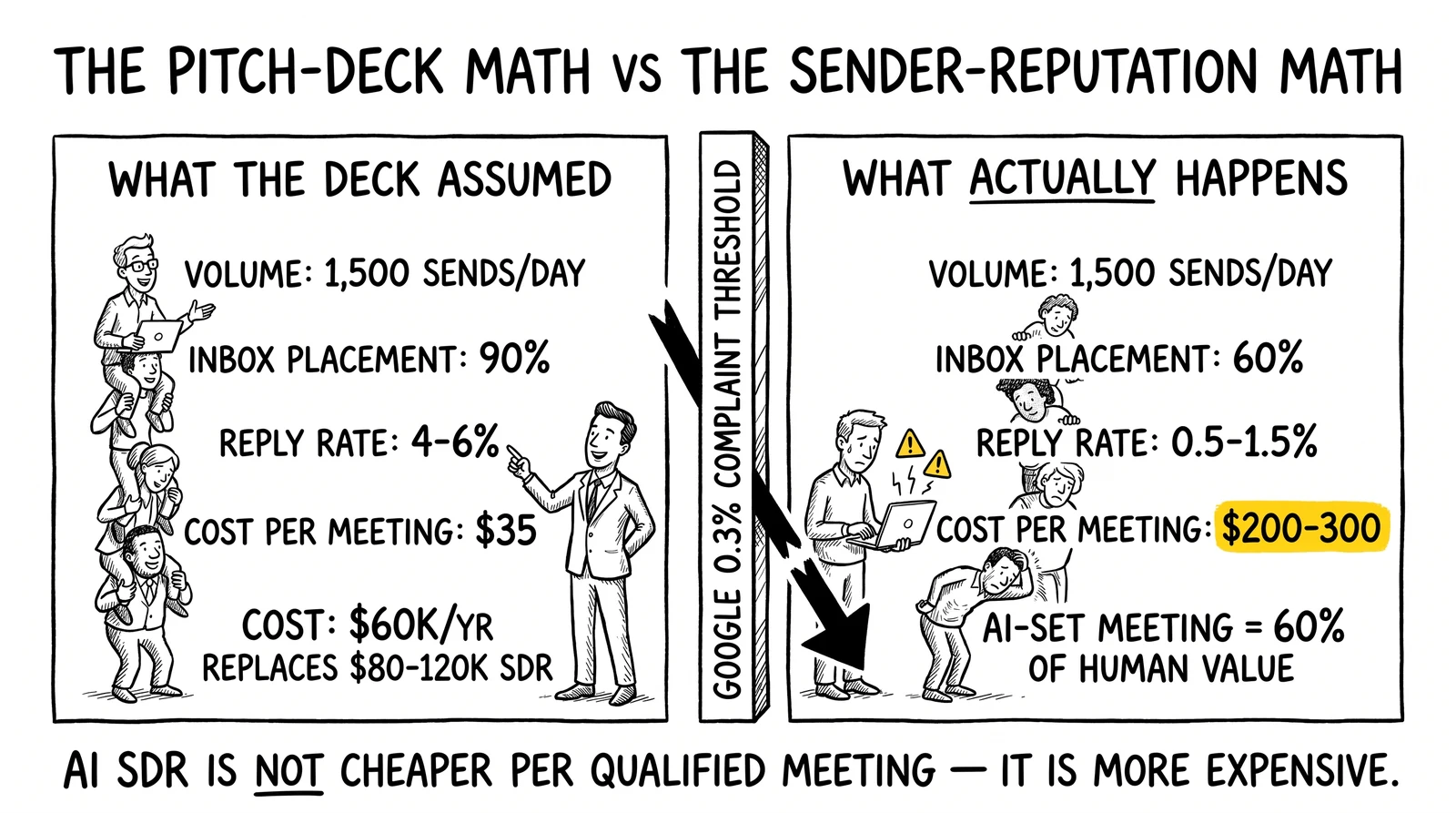

The math: why the SDR-replacement story does not survive contact with sender reputation

The economic claim that built the AI SDR category went like this. A US-based human SDR fully loaded - salary, benefits, management, floor space, dialer, CRM seat - costs roughly $80,000 to $120,000 per year. A managed AI SDR vendor charges roughly $60,000 per year. Therefore the AI SDR pays for itself before producing the first meeting, and any pipeline it generates is upside. The pitch deck uniformly assumed comparable volume and reply rates between the two operating models.

The pitch deck math breaks at the volume comparison. A human SDR runs 50 to 100 high-quality emails per day from a single warmed sender domain, plus call activity, plus LinkedIn touches. The AI SDR runs 1,000 to 2,000 emails per day across 5 to 10 mailbox aliases. The human’s reply rate sits at 4 to 6 percent against a warm domain at 90+ percent inbox placement. The AI’s reply rate at scale lands at 0.5 to 1.5 percent because deliverability collapses past the bulk-sender threshold. The resulting cost-per-meeting numbers diverge sharply. A human SDR costs roughly $35 to $50 per meeting. An AI SDR pilot, run at the volume the vendor recommends, costs $150 to $300 per meeting once deliverability has fully degraded by week six.

The conversion math compounds the cost gap. Operator analyses through 2025 and 2026 generally place AI-set meetings converting to opportunity in the mid-teens versus the low-to-mid 20s for human-set meetings, a roughly ten-point gap reflecting three drivers: weaker qualification at the meeting-set step, lower buyer commitment to a meeting set by an automated agent, and higher AE skepticism heading into AI-sourced calls. Programs that report parity numbers usually run a human SDR review loop between AI booking and AE handoff, which removes the cost advantage AI was supposed to deliver.

Honest unit economics through 2026 should price an AI-set meeting at 60 percent of a human-set meeting’s value and price the cost per meeting at $150 to $300 once deliverability has degraded. That math turns a $60,000 per year managed AI SDR contract into roughly 200 net-equivalent meetings per year, against a human SDR producing 300 to 500 net-equivalent meetings per year for $80,000 to $120,000 fully loaded. The AI SDR is not cheaper per qualified meeting; it is more expensive once the deliverability and conversion penalties are applied.

The cost stack ties back to the LLM rate cards as well. As covered in the GPT-5.5 pricing analysis, OpenAI’s April 2026 price reset doubled output-side rates, which compressed managed AI SDR vendor margins by another 3 to 5 percentage points unless they passed the cost through. Vendors who already sit on sub-50 percent gross retention cannot easily raise prices without losing more customers, which constrains their ability to fund the investment that would actually fix the data and deliverability problems. The economic position of the managed pure-plays through 2026 is a margin trap, not a growth story.

What the 30 percent who succeed do differently

The 30 percent of AI SDR programs that survive past 90 days share a tight set of operational patterns. None of them rely on the autonomy claim. All of them treat AI as infrastructure feeding a human-led sequencing motion rather than as a replacement for the human-led motion. Two reference cases illustrate the survival pattern: Clay’s enrichment-first model and Apollo’s seat-based scaling model.

Clay: enrichment-first

Clay does not sell an AI SDR. The company sells a workflow platform that combines data enrichment, account research, and copy drafting as components that customers wire together inside their existing sequencing motion. Clay’s pricing - $149 per month plus credit-based usage - reflects the component model. The customer owns the persona definitions, the volume decisions, and the brand-safety controls. The platform handles the parts of the workflow where AI demonstrably outperforms humans: pulling structured data from unstructured sources, running enrichment workflows against multiple data providers, and drafting copy that a human reviews before send. Clay’s customer base through 2025 and 2026 has grown faster than the managed pure-plays and retained better. The reason is structural: the customer absorbs the failure modes only at human-led volume, which is a survivable level of exposure.

Apollo: seat-based scaling

Apollo’s seat-based pricing - $49 to $59 per seat per month - sells a database-first sales platform with AI features as accelerators rather than the product. Customers buy seats for human SDRs and AEs and use Apollo’s data, sequencing, and AI assistance to make those humans more productive. The platform’s economic model is aligned with customer retention because seat counts grow when human productivity grows, not when AI volume grows. Apollo has weathered the cancellation wave with retention metrics that look like normal SaaS rather than the sub-50 percent gross retention managed pure-plays have reported. The lesson is that aligning the pricing model with the customer’s actual operating constraint - human productivity - produces a more durable economic relationship than aligning the pricing model with a volume number that breaks against sender reputation.

The pattern across both reference cases is that AI is sold as a capability that compounds with humans, not as a replacement for humans. The customers that buy on that premise run programs that survive 90 days because the failure modes - hallucination, deliverability collapse, brand risk - are bounded by the human-led volume profile. The customers that bought the SDR-replacement pitch are the ones canceling.

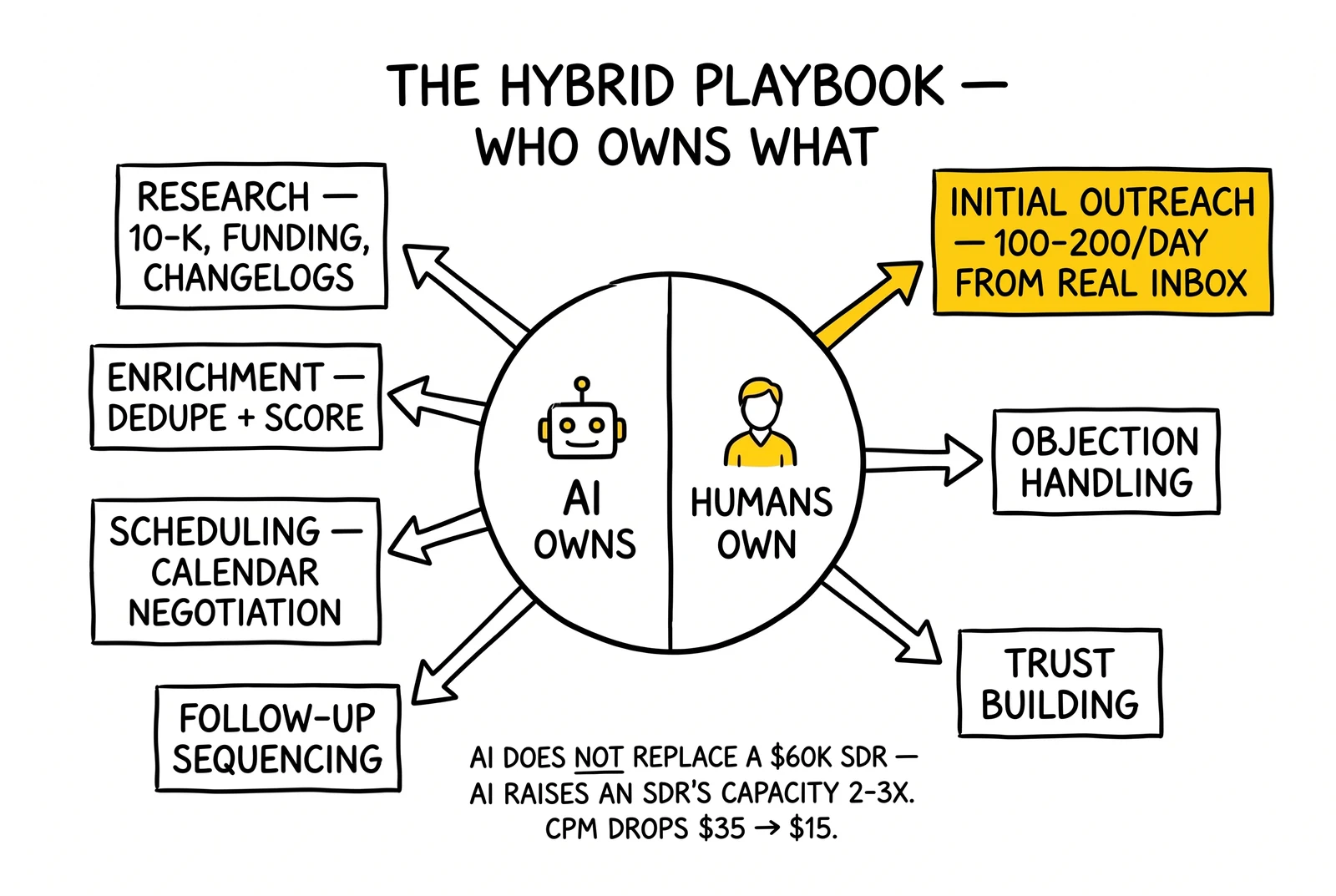

The hybrid playbook: what AI should actually own

The hybrid playbook splits the SDR workflow into research, enrichment, scheduling, sequencing follow-up, initial outreach, objection handling, and trust building. AI owns the first four. Humans own the last three. The split matches each task to the technology’s actual capability profile.

AI handles research because the LLM can read unstructured sources - company websites, 10-Ks, press releases, recent fundraising announcements, product changelogs - faster and more thoroughly than a human SDR. AI generates a structured account brief that a human can review in 30 seconds rather than research from scratch in 30 minutes. AI handles enrichment because the workflow is mechanical: pull a list, run it against three or four data providers, deduplicate, score, and output a clean list. The same workflow that takes a human SDR an hour takes AI 30 seconds. AI handles scheduling because calendar negotiation is bounded, structured, and high-volume - exactly the workload pattern AI executes well. AI handles sequencing follow-up because the work is asynchronous, repetitive, and follows defined rules.

Humans handle initial outreach because the first touch sets the relationship and the brand impression. A first email from a real human, sent from a real inbox, tied to a real LinkedIn profile, with a real signature, lands at higher reply rates than any AI-generated send and carries no brand-risk tail. The volume is lower - 100 to 200 sends per day per human - but the per-send economics are higher, and the deliverability profile holds. Humans handle objection handling because the conversation surface is unbounded and the cost of a wrong answer is high. Humans handle trust building because relationships are the product, and prospects do not build trust with agents.

The integration pattern is sequential. AI runs overnight to build the next day’s account list, generate the research brief, draft the copy. The human SDR reviews the AI’s output in the first 30 minutes of the day, edits the copy, sends from a personal mailbox. AI takes the reply, classifies the intent, drafts the follow-up. The human reviews, sends. AI books the meeting, hands off to the AE. The AE owns the call, the qualification, the handoff to opportunity. The split lets the human SDR cover 2 to 3x the account volume of an unaided SDR while keeping the brand-safety profile intact.

The economic claim shifts. AI does not replace a $60,000 SDR; AI raises an SDR’s effective capacity from one to two or three SDRs’ worth of volume. The math works because the human SDR’s $80,000 to $120,000 fully-loaded cost produces 2 to 3x the meeting count, which lowers cost per meeting from $35 to $15 to $20 without breaking deliverability or brand safety. That is the math procurement teams should run when evaluating AI SDR investment, and it is the math the 30 percent of surviving programs are running.

The handoff to lead scoring also matters. AI-set meetings convert below human-set meetings, but the gap closes when the AI-set qualification is layered with machine-learning lead scoring that prioritizes the AI-sourced opportunities the AE actually engages first. The scoring layer recovers some of the conversion gap by routing AE attention to the right AI-set meetings rather than treating all AI-set meetings as equivalent.

Pre-purchase evaluation rubric

The procurement loop for AI SDR vendors should run a ten-point rubric before signing. Vendors that decline any single line should not survive the loop.

-

Deliverability metrics with named bulk-sender thresholds. Demand the vendor’s data on inbox placement, spam complaint rate, and IP reputation across customer programs over the prior 90 days. Refuse vendors who cannot provide named-threshold compliance against Google, Yahoo, and Microsoft bulk-sender rules.

-

Hallucination rate measured against a held-out validation set. Build a 100-target validation set from the customer’s own market. Have the vendor run the AI against the set and audit the outputs for factual errors. Refuse vendors above 5 percent hallucination rate.

-

List quality and source provenance. Demand documentation of which data providers the vendor uses, what the refresh cadence is, and what the customer’s right is to inspect the list before send. Refuse vendors who run on opaque data sources.

-

Opt-out plumbing tied to suppression lists. Demand a documented opt-out workflow that ties one-click unsubscribe to a global suppression list across all the vendor’s customers. Refuse vendors without cross-customer suppression.

-

Brand-safety controls including kill switch and manual review queue. Demand a documented kill switch the customer can trigger in under 60 seconds and a manual review queue option for the first 1,000 sends of any new persona. Refuse vendors without both.

-

Customer reference calls outside the case-study list. Demand the right to interview at least three named operators not on the vendor’s case-study page. Refuse vendors who restrict references to the marketing list.

-

Gross retention disclosure under NDA. Demand the vendor’s gross retention metric over the prior four quarters under NDA. Refuse vendors below 70 percent gross retention.

-

Contract escape clauses pegged to deliverability and reply-rate SLAs. Demand cancellation rights triggered by spam complaint rate above 0.3 percent, inbox placement below 90 percent, or reply rate below an agreed floor. Refuse vendors without SLA-tied escape clauses.

-

Mid-contract termination rights at 30-day notice. Demand a 30-day no-cause termination right. Refuse vendors who require cause or who set notice periods longer than 30 days.

-

Pass-through pricing transparency on LLM and data provider stack. Demand visibility into the underlying LLM cost, data provider cost, and platform margin. Refuse vendors who refuse the disclosure.

The rubric is not exotic. It applies the same procurement discipline general counsels apply to any vendor with brand-safety exposure. The vendors who fail the rubric are the vendors who built their economic model on the autonomy pitch, and the rubric is designed to surface that failure mode before the contract is signed rather than during the cancellation cluster between days 60 and 90.

Contract terms to demand

If the vendor passes the rubric, the contract terms still need to do real work. Five clauses matter most.

The deliverability SLA should set a maximum 0.2 percent spam complaint rate and a minimum 95 percent inbox placement, with cure rights of 30 days and termination rights if cure fails. The list-quality guarantee should refund the customer if bounce rate exceeds 3 percent across any 30-day window. The brand-safety clause should cover hallucinated content with vendor indemnity for any reputational damage tied to AI-generated copy that the customer can document. The pass-through pricing clause should true up quarterly on LLM and data provider costs, so the vendor cannot expand margin invisibly while service quality degrades. The IP indemnity clause should cover scraped data sources, including LinkedIn, with vendor responsibility for any platform enforcement actions tied to the vendor’s volume profile.

Vendors that resist these terms cannot make the math work in production. The resistance is informative: it surfaces the vendor’s actual confidence in their deliverability, hallucination rate, and brand-safety controls. A vendor confident in their operating discipline will negotiate the cure windows and the indemnity caps but will accept the structure. A vendor selling autonomy without operating discipline will refuse the structure outright and pivot to commercial terms. The procurement team should treat the latter as a no-signal.

The contract terms also work as a forcing function on the vendor’s product roadmap. Vendors who sign deliverability SLAs and brand-safety indemnity have a product-side reason to fix the underlying problems rather than to scale the autonomy pitch. The customers who demand the terms are the ones helping reset the category’s operating norms. The customers who sign the standard managed-program contract without the terms are the ones underwriting the cancellation wave.

The 2027 outlook: agentic distribution and where the category goes

Through 2027 the AI SDR category bifurcates. Managed pure-plays who keep selling the human-replacement narrative will continue to lose contracts at high rates and will consolidate, pivot, or fail. The investor capital that funded the 2023-2024 round is mostly written down by mid-2026, and the next round’s pricing assumes recovery rather than growth. The vendors who survive will reposition as either premium managed services for specific verticals where the autonomy claim can be defended (high-volume transactional B2B with bounded qualification surfaces) or as infrastructure components plugged into customer-led workflows.

The infrastructure layer is where the growth lives through 2027. Clay-style enrichment platforms, sequencing platforms with AI components, scheduling assistants tied to CRM, and reply-triage AI all fit the pattern of selling capability into a human-led workflow rather than autonomy as a product. Apollo, Outreach, Salesloft, and Drift sit in the same category - companies whose pricing model is tied to human productivity rather than AI volume. The aggregate market for these tools through 2027 grows at 30 to 40 percent annually because the customer’s actual problem - making human SDRs and AEs more productive - is real and unsolved.

Above the infrastructure layer sits the agentic commerce overlay. AI agents transacting with AI agents through MCP (Model Context Protocol) and A2A (agent-to-agent) protocols bypass the inbox entirely. When a buyer’s procurement agent talks to a seller’s pricing agent through a protocol-level handshake, no SDR is involved. The economic question shifts from how do we automate the SDR motion to which entities even need an SDR equivalent. The pattern is described in the agentic commerce analysis and the M2M lead transactions analysis, both of which trace the protocol-level transition that makes the inbox a legacy distribution channel for a meaningful share of B2B transactions through 2027 and 2028.

Operators planning 2027 budgets should fund the hybrid stack now and treat the next-generation managed AI SDR pitch with the same skepticism they would apply to any vendor selling a $60,000 headcount replacement. The 50 to 70 percent cancellation rate in the 2025-2026 vintage of managed AI SDR contracts is not noise. It is the signal that the autonomy pitch does not survive contact with sender reputation, hallucination risk, and the actual conversion math of an AE’s calendar. The hybrid playbook is not a fallback; it is the operating model the surviving 30 percent already run.

Key Takeaways

-

The cancellation rate is structural, not cyclical. AI SDR pilots are dying at 50 to 70 percent inside 90 days because the autonomy pitch breaks against sender reputation, hallucination risk, and AE-conversion math - not because a particular vendor cohort got unlucky. Treat the rate as a category constant when modeling 2026 budgets.

-

The TechCrunch 11x exposé reset the category, and the FTC Air AI settlement codified the reset. General counsels now have concrete reference points for evaluating vendor marketing claims before signing managed-program contracts. Procurement loops should incorporate both the customer-list inflation pattern and the FTC substantiation standard.

-

Deliverability collapse is the dominant kill mechanism, not hallucination quality. AI-generated copy can be excellent and the program still dies because volume past the bulk-sender threshold blows up the sender domain reputation. Cap volume at human-led levels (100 to 200 sends per mailbox per day) regardless of what the vendor recommends.

-

AI-set meetings convert at 60 percent of human-set meeting value. Honest unit economics should price the gap into the cost-per-meeting calculation, which moves managed AI SDR programs from cheaper to more expensive than human SDRs once deliverability and conversion penalties are applied.

-

The hybrid playbook is the survival pattern. Give AI ownership of research, enrichment, scheduling, and sequencing follow-up. Keep humans on initial outreach, objection handling, and trust building. The economic claim shifts from AI replaces an SDR to AI raises an SDR’s capacity 2 to 3x, which is a math that survives production.

-

Pricing model determines failure mode absorption. Component vendors (Clay, Apollo, Reply.io) shift volume decisions and brand-safety controls to the customer, which bounds the failure modes at human-led volume. Managed pure-plays (11x, Artisan, Reggie) absorb the customer’s volume decisions and surface every failure mode at scale.

-

Pre-purchase rubric matters more than vendor pitch quality. Run the ten-point rubric on every vendor and refuse vendors who decline any line. Demand deliverability SLAs, gross retention disclosure under NDA, mid-contract termination rights at 30 days, and pass-through pricing transparency on the LLM stack.

-

The 2027 category bifurcates. Managed pure-plays consolidate, pivot, or fail. Infrastructure components grow at 30 to 40 percent annually. Agentic commerce overlays bypass the inbox for a meaningful share of B2B transactions. Plan budgets accordingly.

-

AI is infrastructure for human productivity, not a replacement for human relationships. The vendors and customers who internalize that framing build durable programs. The ones who keep selling or buying the autonomy pitch keep showing up in the cancellation cluster between days 60 and 90.

Sources

- Marina Temkin, “a16z and Benchmark-backed 11x has been claiming customers it doesn’t have,” TechCrunch, March 24, 2025

- OnlyCFO, “AI Company Accused of Fraud,” OnlyCFO Newsletter, 2025

- Aakash Gupta, “The AI SDR Reality Check,” ProductGrowth Newsletter, 2026

- UserGems, “Are AI SDRs Worth It in 2026,” UserGems Research, 2026

- United States Federal Trade Commission, “Air AI and its Owners will be Banned from Marketing Business Opportunities to Settle FTC Charges the Company Misled Many Entrepreneurs and Small Businesses,” FTC Press Release, March 24, 2026 (complaint filed August 2025)

- Google Postmaster Tools, “Email Sender Guidelines,” Google Support, 2024-2026

- Yahoo Inc., “Sender Best Practices and Bulk Requirements,” Yahoo Senders Hub, 2024-2026

- Coldreach, “AiSDR Honest Review 2026,” Coldreach Blog, 2026

- MarketBetter, “11x.ai Honest Review 2026,” MarketBetter Blog, 2026

- G2, “11x.ai User Reviews,” G2 Crowd, 2024-2026

- G2, “Artisan AI User Reviews,” G2 Crowd, 2024-2026

- Michael Saruggia, “AI SDRs Don’t Work,” Saruggia Newsletter, 2026

Closing

The AI SDR cancellation wave is not a vendor-quality problem and not an LLM-capability problem. It is a category-design problem. The pitch that AI replaces a $60,000 SDR was always going to break against the sender reputation curve and the AE conversion gap, and the 50 to 70 percent cancellation rate in the 2025-2026 vintage of managed contracts is the market collecting on the implicit bet. The vendors who survive will be the ones who repositioned early - selling capability into human-led workflows rather than autonomy as a product - and the operators who run successful programs in 2027 will be the ones who internalized the hybrid playbook before procurement forced them to. The opportunity in the category is real. The shape of the opportunity is not what the 2024 pitch decks claimed.