Forrester’s April 27, 2026 GTM Singularity research did not invent the demand contraction lead generators are already feeling. It named it. Where the broader demand-generation versus lead-generation strategic distinction frames the long-running discipline divide, this Forrester-specific report angle isolates the pre-funnel demand hole – the share of buyer research that AI surfaces have already absorbed before any classical funnel event registers. The denominator-contraction story this piece tells pairs with the Adobe AI traffic 42% conversion-premium analysis, which addresses what the surviving sessions are worth on a per-visit basis – fewer sessions reach the funnel, but each one converts harder. The harder question, for any operator running a CPL benchmark, a twelve-month traffic forecast, or a buyer-waterfall model built on form-fill volume, is what the pre-funnel haircut actually does to the math. The short answer: it makes CPL inflation structural. This analysis walks through why.

Forrester Named the Era – and What the Naming Reveals

On April 27, 2026, from the main stage at B2B Summit North America in Phoenix, Forrester unveiled research it had been signaling since the prior fall: The GTM Singularity Is Here. A singularity, in the sense Forrester used, is a convergence point at which traditional rules stop applying. Three forces are doing the converging. AI-driven buyer autonomy is collapsing the discovery and evaluation phases of the funnel. Generative search is intercepting buyer questions before they ever produce a click. Agentic procurement, which a year ago was a slide-deck concept, has begun negotiating real quotes against real sellers. Forrester’s prescription is the ARC framework – Augmented, Resilient, Collaborative – and the firm’s argument is that any go-to-market organization still operating on the marketing-qualified-lead playbook is now running on borrowed time.

For most readers in the marketing trade press, the headline was the framework. For lead-gen operators, the headline should have been a single number buried in the supporting research. According to Forrester’s January 2026 State of Business Buying report, drawn from a survey of nearly eighteen thousand global business buyers, ninety-four percent of business buyers now use generative AI somewhere in their purchase process. The typical buying group has expanded to thirteen internal stakeholders and nine external influencers – twenty-two people, materially larger than the seven-to-ten figure that anchored 2018-era B2B sales literature. And nineteen percent of buyers using AI in their decision say they feel less confident in the resulting decision because of inaccurate or unreliable AI output, rising to twenty-eight percent among procurement professionals.

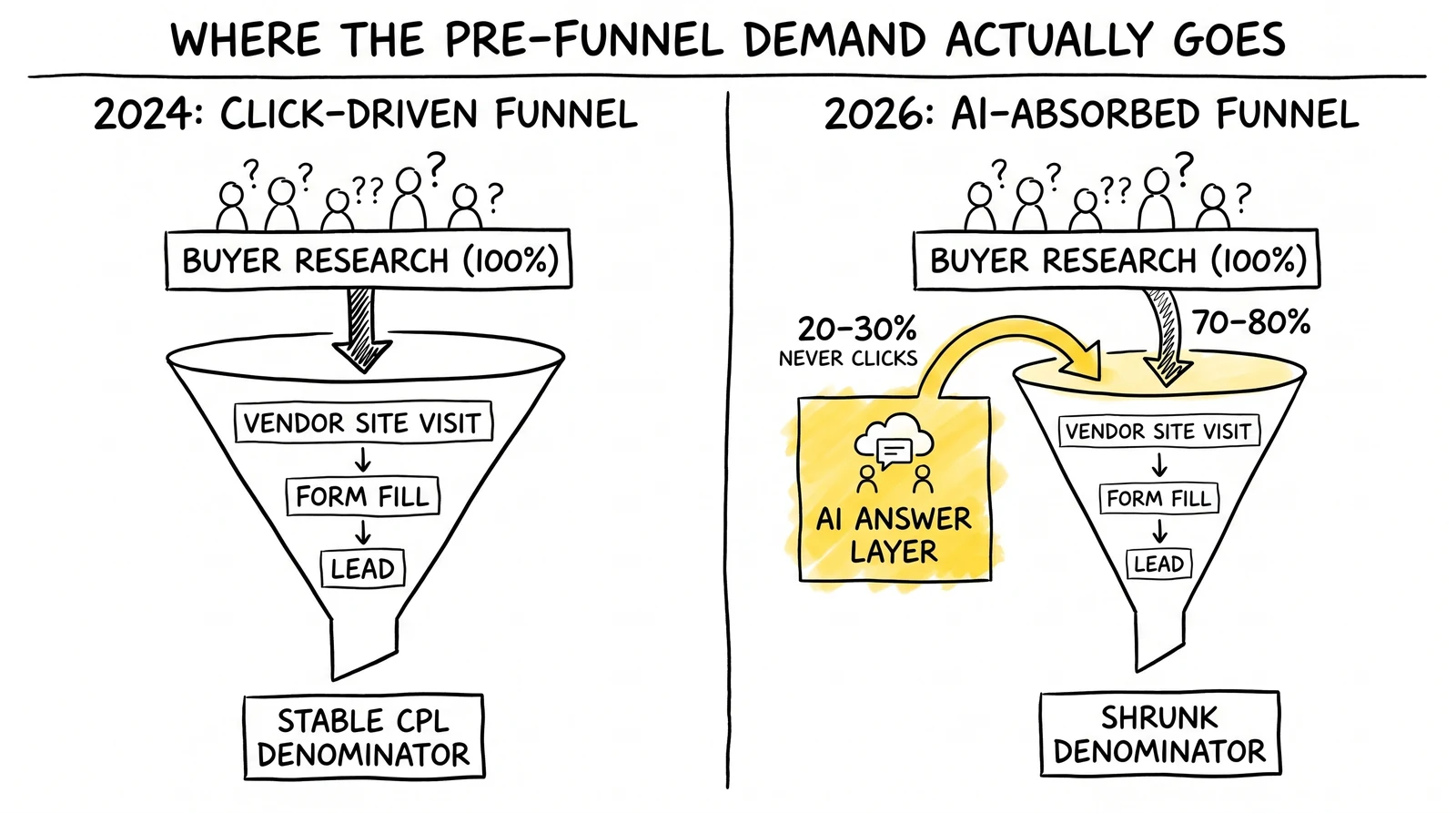

Pair those buyer-side numbers with the Pew Research Center’s July 2025 measurement of click-through behavior on AI-summarized search results – eight percent click rate when an AI summary appears, fifteen percent without one – and pair them further with Bain & Company’s tracked fifteen to twenty-five percent reduction in organic web traffic across categories where AI summaries dominate. Stack the three numbers and the directional implication is unambiguous. Twenty to thirty percent of the pre-purchase research that used to produce a measurable click on a vendor or publisher property no longer produces one. The research happens. It just happens inside the model.

To be precise about provenance: the twenty-to-thirty-percent range is a site composite scenario, not a Forrester-published number. Forrester did not put a single contraction percentage on the GTM Singularity. The composite is built from three independent inputs documented below.

Derivation note – the 20-30% pre-funnel hole as a site model

Input Source Observed behavior Modeled contribution Confidence Click-through halving on AI-summarized SERPs Pew Research Center, July 2025 (n≈900 U.S. adults) 8% click rate with AI summary vs. 15% without A roughly 7-percentage-point absolute click-rate drop on summarized queries Medium-high; specific cohort and survey methodology, not panel-validated against server logs Organic-traffic reduction in AI-summary-dominant categories Bain & Company, 2025-2026 research 15-25% drop in organic web traffic Lower-bound traffic loss across affected categories Medium; consultancy-published, category-mix sensitive Pre-purchase research migrating into AI surfaces Forrester State of Business Buying, January 2026 (n≈18,000 buyers) 94% of B2B buyers using generative AI in purchase process Structural, not cyclical, reduction in vendor-site research events Medium; self-reported buyer behavior, directional Composite (site model) Stacked plausibility range across the three inputs – 20-30% pre-funnel click loss across affected categories Medium; site synthesis, not a Forrester-published figure Operators applying the composite to their own categories should run their own input ranges; the site model is intended as a planning scenario, not a market measurement.

Why the framework matters less than the data underneath it

The ARC framework reads, for a vendor running its own GTM, as a leadership-team agenda. For a lead-generation publisher selling traffic and form-fill events into that vendor’s funnel, the framework reads differently. The Augmented pillar’s directive to “treat buyer agents as members of the buying network and supply them with relevant content” is the load-bearing one. It says, plainly, that the surface area where lead-gen content has to be discoverable, citable, and persuasive is no longer the vendor’s website or the publisher’s article page alone. It is also the answer engine that the buyer agent queries on its way to a shortlist. A publisher whose content is invisible in that query layer is, in Forrester’s framing, supplying nothing to the buying network at the exact moment the buying network is being formed. That is the line that connects the GTM Singularity directly to the existing site thesis on entity-graph and schema infrastructure for AI visibility. The publisher who treated entity tagging and schema markup as a 2025 nice-to-have is now, in 2026, watching the cost of having skipped the work compound.

Conductor’s April 20, 2026 launch of Enterprise AgentStack is the supply-side market response. Native LLM apps inside ChatGPT, Claude, and Microsoft Copilot; developer infrastructure including an MCP server; packaged Answer Engine Optimization agents – Conductor positions the product as “the industry’s only system of record for AEO.” Adoption signals matter more than the product spec. Optimizely, Razorfish, Havas, and IBM are publicly building on the platform. Conductor reported closing FY2026 with fifty-plus new logos and exceeding ARR targets by 147 percent. That is the curve of a category enterprise marketing departments have already concluded they need to staff.

This is not, as some industry commentary has framed it, a top-of-funnel content marketing problem. It is a denominator problem. Every CPL benchmark, every cost-per-acquisition ratio, every conversion-rate calculation, and every paid-media efficiency metric is computed by dividing some cost figure by a count of measurable funnel events. When the count of measurable funnel events shrinks structurally, the same dollar of advertising spend produces a smaller denominator and a larger ratio. That ratio looks, on a dashboard, exactly like CPL inflation. It is not inflation in the cyclical sense. It is a definitional shrink. The number got smaller because the thing being counted got smaller, and no amount of media optimization closes that gap. This analysis covers what changed on April 27, why the twenty-to-thirty-percent pre-funnel haircut breaks the existing CPL measurement stack, what the buyer-agent layer does to lead pricing, and what lead-gen operators should be doing in the next ninety days to capture the replatform window before the operators who move first establish cost positions the rest of the market cannot match.

The Demand-Curve Haircut Lead-Gen Operators Are Walking Into

The clean way to see what the contraction does to lead-gen unit economics is to walk through what happens to a single CPL benchmark when its denominator shrinks by the rates the data describes.

The denominator math

Take a benchmark calculation that should be familiar to any operator. A category-level CPL is the dollar cost of producing one billable lead, computed by dividing total acquisition spend by total billable form fills for the period. The denominator – billable form fills – has historically been a function of three things: the size of the addressable search-driven traffic pool, the click-through rate from search to the publisher’s funnel pages, and the form-fill conversion rate on those pages. For a typical lead-gen vertical, the search-driven traffic pool was the largest of the three by a wide margin. CTR and on-site conversion were measured to two decimal places; the traffic pool was the assumed constant.

Apply Pew’s documented click-rate halving to the share of search behavior that now produces an AI summary, weight it by the eighteen-percent prevalence Pew measured in early 2025 (and which industry data suggests was higher by Q1 2026), and the search-driven traffic pool contracts by something on the order of fifteen to twenty-five percent – exactly the range Bain’s organic-traffic measurement reports. Layer on top of that the share of pre-funnel research that has migrated entirely off classical search engines and into ChatGPT, Claude, Perplexity, and Copilot interactions that produce no Google query at all, and the upper end of the contraction estimate edges toward thirty percent for top-of-funnel queries.

Now run the CPL math. Hold acquisition spend flat. Reduce the form-fill denominator by twenty-five percent. The CPL ratio rises by exactly thirty-three percent – not because any cost layer got more expensive, not because conversion rates changed, but because the count of countable events shrank. That number is roughly aligned with the CPL inflation many lead-gen verticals have reported in 2025-2026 benchmark studies. Operators have been describing the rise as “competitive pressure,” “media-cost inflation,” or “platform algorithm change.” The data suggests a different explanation. A meaningful share of what looks like CPL inflation is denominator collapse misclassified as cost growth.

Why this is structural, not cyclical

The case that the contraction is cyclical – that it will correct as users get tired of AI summaries or as Google reweights its surface – does not survive the buyer-side data. Buyers are not abandoning AI; the State of Business Buying survey shows the opposite. They are using it more. The use is sticky because it is faster and the answers are good enough. The nineteen-percent confidence-erosion finding suggests buyers know the answers are imperfect and are routing around the imperfections through expanded buying groups and external influencer reliance, not by clicking back through to vendor websites.

The case that operators can simply rebuild the lost top-of-funnel volume on social, video, or community channels does not survive the agentic-procurement data. As buyer agents take on more of the discovery and shortlist-construction work, the demand they generate is fundamentally different from the demand a human researcher generates. A human researcher visits five sites, reads three articles, and fills a form. A buyer agent queries an answer engine, ingests citations, evaluates against a structured criteria list, and produces a shortlist that the human reviews. The form-fill, in that workflow, is replaced by an agent-to-vendor handoff that may or may not pass through any publisher’s measurement layer at all. Forrester’s prediction that twenty percent of B2B sellers will face agent-led quote negotiations in 2026 is the early read on how fast that handoff is normalizing.

Both forces – sticky AI usage and rising agentic procurement – push the denominator down rather than letting it recover. The contraction is structural in the same sense the shift from print classifieds to online classifieds was structural twenty years ago. The volume did not come back. The measurement framework had to change.

What it means for the buyer waterfall

Every tier of a traditional buyer waterfall is now sitting on a smaller foundation than its pricing model assumes. If the pool is twenty-five percent smaller, the count of leads available to all tiers is twenty-five percent smaller. The waterfall does not break – it just transmits the contraction unevenly. Lead-gen buyers feel it as smaller monthly delivery against the same retainer. Publishers feel it as compressed margin against a fixed cost base. Both sides eventually recalibrate, but the operators who have not done the denominator math going in absorb the friction asymmetrically.

The Three Dimensions of the Measurement Stack Reset

Beneath the denominator collapse sit three distinct measurement breaks, each of which independently affects lead-gen unit economics. Operators who treat this as a single change miss the compound effect.

Dimension one: attribution models assume a click that no longer happens

Multi-touch attribution, last-click attribution, and even the “data-driven” attribution variants offered by major ad platforms all assume that a buyer’s pre-purchase research generates a sequence of trackable touchpoints, the last of which is a click leading to a measurable session. When the pre-purchase research happens inside an AI summary that the buyer reads in twenty seconds and never clicks out of, none of that sequence exists. The attribution model is computing weights for touchpoints that did not occur. The practical consequence is that attribution outputs in 2026 are increasingly biased toward bottom-of-funnel touchpoints – the branded search, the direct visit, the comparison-page session – because those are the touchpoints the buyer takes after the AI-mediated research has already produced a Day One List. Forrester’s ARC prescription touches this indirectly. The “augmented” pillar’s directive to “treat buyer agents as members of the buying network and supply them with relevant content” is, when read through a measurement lens, a directive to instrument content for consumption by an audience that does not generate clicks. That requires entirely different measurement primitives – citation share, AI-overview presence, model-mention frequency – that most lead-gen analytics stacks do not currently capture. The site’s existing thesis on LLMO measurement and AI-search ROI is the playbook for that build, and it is no longer optional.

Dimension two: cross-year CPL comparisons stop being comparable

Cross-year CPL comparisons are the spine of how lead-gen operators communicate with finance, with buyers, and with their own teams. Q1 2026 versus Q1 2025 CPL is the line on the dashboard that triggers either confidence or alarm. The denominator shift makes that comparison structurally misleading, because the numerator (dollars of acquisition spend) and the denominator (form fills) are still nominally the same but the underlying demand pool the denominator is drawn from is materially smaller. A finance team that reads a thirty-percent year-over-year CPL increase as evidence of media-cost inflation will allocate budget differently than a finance team that reads the same number as evidence of denominator contraction. The first team buys more media. The second team buys the answer-engine infrastructure that makes the publisher findable inside AI summaries. The action implications are nearly opposite. Operators whose internal reporting does not separate the two effects systematically misallocate.

Dimension three: the buyer-agent layer bifurcates lead pricing

The third break is the most consequential and the most operationally underrated. Forrester’s prediction that twenty percent of B2B sellers will be forced into agent-led quote negotiations in 2026 affects pricing on both sides of the marketplace simultaneously. On the buy side, when a procurement function deploys a buyer agent, the agent’s role is to compress what was a multi-week research-and-shortlist process into a multi-hour query-and-evaluate process. The agent ingests procurement criteria, queries answer engines for vendors that match, evaluates against a scoring rubric, and produces a ranked shortlist. For a publisher whose content is cited in the answer-engine query, the agent is a beneficial reader. For a publisher whose content is not cited, the agent is invisible. There is no second-chance click, no remarketing pixel that can re-engage the agent. The agent moves on, and the publisher never knows it was in the running because the agent did not generate a measurable session.

The mirror development is on the seller side. Forrester’s prediction explicitly calls out seller-controlled agents that will deliver “dynamically delivered counteroffers” in response to buyer-agent inquiries. For lead-gen publishers selling form fills into vendor funnels, this changes what a “lead” is. The form fill that used to enter a CRM as a record waiting for a sales rep to engage is now, in the agentic flow, the trigger for an automated counteroffer. Publishers who can deliver structured, agent-readable lead records – with verified intent signals, validated contact data, and routed scoring metadata – become more valuable to vendors with active counteroffer engines. Publishers who deliver legacy form-fill records become less valuable. The result is a bifurcation of the lead-gen market into two pricing tiers: an agent-ready tier of leads sourced from answer-engine-cited publishers and delivered with structured metadata, and a legacy tier of leads sourced from non-cited surfaces and delivered as conventional records. Pricing on the agent-ready tier holds or rises. Pricing on the legacy tier falls. The combined market may show flat aggregate pricing while dispersion between the two tiers widens dramatically – and that bifurcation maps directly to the operator’s existing entity-graph and authority infrastructure, which is the E-E-A-T and author-entity verification question the AI Overviews surface specifically rewards.

The Approaches That Will Underperform This Cycle

Three responses to the GTM Singularity research are visible in early lead-gen industry chatter. Each underperforms the alternative for reasons worth being explicit about.

The first is the “wait for the data to settle” posture. The argument is that the twenty-to-thirty-percent contraction is an early-cycle estimate, that AI summary penetration is still rising, that platform algorithms will reweight, and that prudent operators should hold current spend allocations until the contraction stabilizes. The flaw in the argument is that the contraction is not a one-time shock that stabilizes; it is a structural shift that compounds. Every quarter an operator delays the answer-engine build, the share of pre-funnel research happening through AI gets larger, the cost of catching up to operators who started in 2025 grows, and the citation share that is being claimed by competitors in the answer-engine layer becomes harder to dislodge. Citation share, like organic ranking before it, has a strong incumbency advantage. The operator who arrives in Q4 2026 to a category whose top three answer-engine citations were locked down in Q1-Q2 is in approximately the position of a late-arriving SEO competitor in 2010.

The second is the “double down on paid” posture. The argument is that if organic top-of-funnel is shrinking, the rational response is to compensate with more paid acquisition. The flaw is that paid acquisition is competing for the same shrunken denominator, and the unit economics of paid in a contracting demand pool deteriorate faster than the unit economics of paid in a stable pool. As more operators chase fewer searches, the auction prices rise; as auction prices rise on an already inflated CPL, margin compresses; as margin compresses, the operator has fewer dollars to redirect into the answer-engine build that would have addressed the underlying problem. The doubled-down paid strategy is a deeper hole, not an alternative path out of the original one.

The third is the “build a generic content moat” posture. The argument is that producing more content – more how-to guides, more comparison articles, more vertical-specific blog posts – creates more surface area for AI summaries to cite. The flaw is that volume of content is no longer the binding constraint on citation. Authority, entity verification, schema clarity, and source-of-record positioning are. A well-resourced operator who produces fifty new articles a month and does not invest in the entity-graph layer will, in most categories, be cited less often than a focused operator who produces ten articles a month and has tightly built entity infrastructure and verified author signals. The volume strategy was the right strategy for 2018-era SEO. It is not the strategy that the answer-engine layer rewards.

The pattern across the three responses is the same. Each treats the GTM Singularity as a quantitative shift that can be addressed by doing more of what already exists. The data describes a qualitative shift that requires doing different things. The operators who recognize the difference now run the build window. The operators who do not run, eventually, against the operators who did.

The Strategic Reframe: Three Principles for the Replatformed Lead-Gen Funnel

The right response to April 27 starts from a different premise. The lead-gen funnel is no longer a collection of search-and-form-fill events that can be measured in the classical sense. It is a participation graph in which the operator’s content is either cited inside the AI-mediated research surface or not. Three principles flow from that premise.

Principle one: build the answer-engine layer as a first-class measurement surface, not a content tactic

The instinct most lead-gen operators have when they hear “AI search visibility” is to assign the work to a content marketing team and treat it as a 2026 SEO refresh. The reframe is that the answer-engine layer is not a content tactic; it is a measurement surface that needs first-class instrumentation, dashboards, and ownership. Operators who do this well track citation share by category, by query, and by competitor. They monitor model-mention frequency across ChatGPT, Claude, Perplexity, and Copilot. They run regression analyses linking citation events to downstream form-fill volume to identify which citations actually feed the funnel and which are decorative.

Conductor’s AgentStack is one tool in this category; others exist; more will arrive. The tooling is less important than the operational decision to treat citation share as a top-line metric rather than a content-marketing vanity stat. An operator whose monthly business review includes citation-share trends alongside form-fill volume is operating in 2026’s actual market structure. An operator whose monthly business review still leads with organic traffic and goal completions is operating against a market that no longer exists.

Principle two: re-bench CPL ladders against the haircut denominator, then renegotiate buyer pricing accordingly

The CPL ladder – the set of price tiers an operator charges for different lead types and exclusivity grades – was built against a denominator that no longer holds. The right operational response is to recompute the ladder against the haircut denominator and renegotiate buyer pricing to reflect the new economics. This is uncomfortable work; buyers do not enjoy receiving CPL increase notices. It is also non-optional, because the alternative is to absorb the contraction silently and watch margin disappear over the next two to three quarters.

The pricing conversation goes better when the operator has the data to back the request. A buyer who is shown a denominator-haircut analysis, with citation-share evidence that the operator’s content is intercepting more of the surviving research traffic than before, sees a vendor who is investing in the buyer’s success even as the underlying market contracts. A buyer who is shown only a CPL-increase request without supporting structural evidence sees a vendor passing through inflation. The distinction matters at retention time. The site’s existing thesis on content marketing ROI measurement and lead-quality reporting is the playbook for assembling that evidence.

Principle three: structure inventory for buyer agents, not just human buyers

The third principle is the operationally heaviest. Every lead-gen publisher needs to make a deliberate decision about whether their inventory is structured for delivery to vendors with active buyer-agent and counteroffer-engine workflows, or whether it is structured for delivery to vendors still operating on human-mediated CRM workflows. The right answer for most operators is “both, in clearly differentiated tiers.”

Agent-ready inventory carries structured metadata: verified contact data, intent-signal tags drawn from the originating answer-engine query, scoring metadata that maps to common counteroffer rule sets, and provenance tags identifying the citation chain that produced the lead. Legacy inventory carries the conventional fields. The two tiers are priced separately, sold separately, and reported separately. Buyers self-select into the tier their downstream workflow can actually consume. Both tiers benefit because the legacy inventory stops being penalized for failing to do work it was never instrumented to do, and the agent-ready inventory captures pricing that reflects its higher value to the agentic-procurement cohort.

The build for agent-ready inventory is non-trivial. It requires schema work, identity-resolution upgrades, integration with answer-engine APIs that publish citation provenance, and contractual updates with buyers about what metadata the operator is committing to supply. A realistic implementation runs four to six months for a mid-sized publisher. That timeline is identical to the VantageScore re-pricing build window the mortgage segment is currently navigating; the resource patterns are similar; and operators who can run both builds in parallel during 2026 emerge in 2027 with two structural cost positions competitors cannot easily match.

Evidence and Early Movers: Forrester’s Award List and Conductor’s Adoption Curve

The GTM Singularity research did not arrive with named lead-gen operators as case studies. It did arrive with a cohort of named B2B operators that Forrester recognized as exemplars, and the pattern of names is informative.

Amazon Ads, Rockwell Automation, and ServiceNow took home Forrester’s 2026 B2B Return on Integration Honors at the same B2B Summit that unveiled the GTM Singularity research. Each of the three has, in the public record, made significant 2024-2025 investments in connected GTM infrastructure – shared customer data platforms, AI-augmented content production at scale, and integration of answer-engine and entity-graph work into core marketing operations rather than treating it as an SEO sideline. The pattern that connects them is the one the ARC framework prescribes – investment in collaboration across silos and in augmentation across the GTM tech stack – operationalized before the research formalized the framework.

Conductor’s adoption curve tells a parallel story. Optimizely, Razorfish, Havas, and IBM building on the AgentStack platform represent enterprise marketing services and software companies committing engineering resources to answer-engine optimization at the platform-integration level. The combined adoption signals that the buyer side of the answer-engine tooling market – the marketing organizations that have to make the buy-or-build decision – has decisively chosen buy and now over wait and see. For lead-gen operators, the practical read is that the answer-engine infrastructure layer is being commoditized faster than expected. The build cost was, in 2024, a serious in-house engineering project. By Q2 2026, it is a vendor-tool integration the operator can rent.

The data-quality consideration most operators are missing

The single underrated finding in the supporting research is the nineteen-percent buyer-confidence-erosion number, rising to twenty-eight percent in procurement. The operational read is that buyers know AI output is unreliable and are over-weighting identifiable expert sources to compensate. That over-weighting, paired with the buying-group expansion to twenty-two stakeholders, makes the cohort of trusted, verifiable, named experts a structurally appreciating asset. For lead-gen publishers, this is the case for author-entity verification work. A publication whose articles are written by named experts whose credentials are verifiable in the entity graph – through Wikipedia, through industry-association rosters, through professional licensing databases – is more frequently cited by AI summaries than a publication bylined to “the editorial team.” The premium is widening because the buyer-side trust gap is widening.

The broader pattern: the GTM Singularity is not a single change. It is a layered change. Each layer compounds with the others. Operators who model only one layer will systematically understate both the threat and the opportunity.

Implementation Reality: What It Actually Takes to Replatform

The strategic reframe is straightforward. The implementation is not.

Resource requirements

Building the answer-engine and agent-ready infrastructure requires three investments most lead-gen organizations have not budgeted for. The first is the entity-graph and schema layer – the structured metadata that lets answer engines confidently cite the publisher’s content. For a publisher with a back catalog of two hundred or more articles, this is typically a sixty-to-one-hundred-twenty engineering-day project covering schema-markup updates, author-entity verification, citation-graph linking, and the integration work to keep metadata current.

The second is the citation-share measurement layer – the build that turns answer-engine visibility from intuition into a measured surface. Build-your-own runs forty to eighty engineering days plus ongoing maintenance; rental options like Conductor AgentStack run mid-five-figure to low-six-figure annual license costs and a thirty-to-sixty-day integration window. The third is the agent-ready inventory build: schema work, identity-resolution upgrade, and buyer-side contractual update that allows the publisher to deliver structured metadata-rich leads alongside legacy leads. For a publisher delivering tens of thousands of leads per month, this is a forty-to-eighty engineering-day build plus a buyer-onboarding cycle that depends on each individual buyer’s internal pace.

Timeline expectations

A realistic implementation timeline for a mid-sized lead-gen publisher:

| Phase | Duration | Key Activities |

|---|---|---|

| Entity-graph and schema build | 60-120 days | Author-entity verification; schema markup; citation linking; ongoing-update integration |

| Citation-share measurement | 30-60 days | Tool selection (build vs. rental); integration; dashboard build; baseline measurement |

| Agent-ready inventory schema | 40-80 days | Lead-record metadata expansion; identity-resolution upgrade; buyer-side schema documentation |

| CPL ladder re-bench | 14-21 days | Denominator-haircut modeling; tier re-pricing; buyer-comm preparation |

| Buyer renegotiation | 30-60 days | Communicate haircut analysis; renegotiate tier pricing; onboard agent-ready inventory tier |

| Total elapsed time | 4-6 months | Conservative estimate for a publisher without prior entity-graph or citation-measurement infrastructure |

Source: Composite estimate based on Conductor, Forrester, and analogous re-platform projects; specific timelines vary by publisher scale and prior infrastructure

Common obstacles

Three obstacles consistently slow these implementations. The first is internal data ownership. Entity-graph and schema work touches the editorial team’s authoring workflow, the engineering team’s content-management infrastructure, and the analytics team’s measurement layer. Cross-functional ownership is a precondition for finishing on time, and most lead-gen organizations have not established it. The second is the buyer-renegotiation cycle. CPL ladder updates touch every active buyer relationship; operators who run the buyer conversations in parallel with the engineering work compress the overall timeline by thirty to forty-five days. The third is the measurement-baseline gap. Citation-share measurement requires at least sixty days of historical data to make trend signals interpretable; the right sequence is to start the citation-measurement integration first, so the baseline accumulates while the deeper work is in flight.

The implementation is hard. The operators who complete it before the rest of the market reprices will run a six-to-twelve-month structural advantage in citation share, lead pricing, and buyer-side perception of value.

Future Implications: The Five-Year Trajectory of Lead-Gen Pricing Under the Singularity

The April 27 announcement is the formal beginning of a multi-year sequence. The shape of the sequence is reasonably predictable from the structure of the buyer-side data.

In the next twelve months, expect the contraction to deepen. AI summary prevalence rises from the eighteen-percent share Pew measured in early 2025 toward thirty to forty percent of search behavior by year-end 2026 as Google, Bing, and the dedicated answer engines compete for query share. Bain’s organic-traffic-decline range widens at the upper end. The publishers who have already built citation share capture an outsized share of the surviving traffic; the publishers who have not face accelerating CPL inflation.

In the next twenty-four months, expect agent-led negotiation to expand from the twenty-percent Forrester predicts in 2026 to a materially larger share of B2B sell-side workflows. The publishers who have built agent-ready inventory tiers see those tiers become the dominant share of their book. Legacy inventory tiers persist for buyer cohorts running classical CRM workflows but trade at a discount that widens as the agent-ready cohort scales.

In the next thirty-six months, expect citation share itself to become a tradable asset. The pattern follows the SEO-domain-authority arc of 2010-2015: a metric that was initially a marketing-team intuition becomes a measured surface, then a benchmark, then a basis for valuation. Lead-gen publishers who have established strong citation positions in 2026-2027 categories will be acquisition targets at premiums similar to those high-authority domains commanded in the 2014-2017 SEO consolidation cycle.

The longer-term shift is the more interesting one. The GTM Singularity research is, in Forrester’s framing, the formal end of the traditional B2B marketing playbook. The downstream implication for lead generation is that the discipline’s center of gravity migrates from acquisition-against-search to participation-in-AI-mediated-discovery. The operators who treat the migration as a tactical refresh will be optimizing yesterday’s funnel through 2027 and 2028. The operators who treat it as a discipline-level reset will be running the funnel that exists in 2029 – the funnel built around answer-engine fitness, agent-ready inventory, and entity-graph authority – while their competitors are still trying to recover the click-through rates of 2022.

For lead generators, the strategic implication is to design the operating model for the world after the next two cycles of AI maturation, not just the world after the first one. A publisher architecture that abstracts the surface layer – that treats classical search, AI summaries, agent queries, and whatever comes next as interchangeable acquisition surfaces with consistent measurement primitives – is a more durable architecture than one optimized specifically for the April 2026 conditions.

Key Takeaways

The April 27, 2026 GTM Singularity research formalized a structural shift in B2B buying that lead-gen operators have been feeling but not naming. The naming matters because it gives the shift a vocabulary that finance teams, buyers, and boards can debate; the data underneath it matters because it quantifies the contraction in terms operators can model.

The pre-funnel demand contraction of twenty to thirty percent – supported by Pew Research’s measured click-rate halving on AI-summarized search, Bain’s organic-traffic-decline tracking, and Forrester’s ninety-four-percent buyer AI usage figure – moved from a 2025 industry concern to a 2026 measurable reality. The contraction is structural, not cyclical, and it compounds as AI summary penetration rises.

The denominator haircut breaks the existing CPL benchmark stack. A meaningful share of what lead-gen operators have classified as CPL inflation in 2025-2026 is denominator collapse misclassified as cost growth. Operators whose internal reporting does not separate the two effects systematically misallocate budget toward more media when the load-bearing investment is in answer-engine infrastructure.

The buyer-agent layer creates a bifurcated lead-gen market. Agent-ready inventory – sourced from answer-engine-cited publishers and delivered with structured metadata – holds or appreciates in price. Legacy inventory trades at a widening discount. Publishers who structure inventory for both tiers capture both buyer cohorts; publishers who do not cede pricing power to those who do.

Three responses underperform: waiting for the contraction to stabilize (it compounds), doubling down on paid media (worsens unit economics in a contracting denominator), and producing more generic content (volume is no longer the binding constraint on citation; authority and entity verification are).

The implementation is non-trivial. A mid-sized lead-gen publisher should plan four to six months of engineering, schema, measurement, and buyer-negotiation work to capture the replatform opportunity, with entity-graph build, citation-share measurement, and agent-ready inventory schema as the three critical-path items.

The five-year trajectory points toward AI summary penetration of thirty to forty percent of search by year-end 2026, agent-led negotiation expanding well beyond Forrester’s twenty-percent 2026 prediction, citation share emerging as a tradable asset by 2028, and the discipline’s center of gravity migrating from acquisition-against-search to participation-in-AI-mediated-discovery by 2029.

For lead-gen operators currently running classical search-and-form-fill funnels, the next ninety days are the planning window. The next one hundred and eighty days are the build window. The first lenders, insurers, and home-services advertisers to reprice their bids on agent-ready inventory are doing it in Q3 2026; the publishers who arrive at that conversation with structured metadata, verified author entities, and citation-share evidence capture the margin opportunity. The publishers who arrive later compete for what is left.

Frequently Asked Questions

What did Forrester actually announce on April 27, 2026?

Forrester unveiled research titled The GTM Singularity Is Here at its B2B Summit North America in Phoenix on April 27, 2026. The research argues that AI-driven buyer autonomy, generative search interception of buyer questions, and emerging agentic procurement have converged into a structural break with traditional B2B go-to-market practices. Forrester’s prescriptive response is the ARC framework – Augmented, Resilient, Collaborative – which directs marketing, sales, customer success, and product leaders to connect AI agents to GTM workflows, abandon static playbooks, and dissolve cross-functional silos. The research was paired with Forrester’s January 2026 State of Business Buying report and its October 2025 2026 B2B Marketing, Sales, and Product Predictions, which together provide the buyer-side data underneath the framework.

Why does this matter more for lead-gen operators than for typical B2B vendors?

For a typical B2B vendor, the GTM Singularity is a strategic guidance frame – what their leadership team should think about over the next eighteen months. For a lead-gen operator, the same research is a unit-economic event because every CPL benchmark, every buyer-waterfall pricing model, and every twelve-month traffic forecast is computed against a denominator that the contraction reduces by twenty to thirty percent. Vendors can absorb the shift through marketing-budget reallocation; lead-gen publishers cannot, because their revenue model depends on the form-fill volume that the denominator measures. The operator-side stakes are higher and the action window is shorter.

How was the 20-30% pre-funnel contraction figure derived?

It is a site composite scenario, not a Forrester-published number. The figure is composed from three measurable inputs. Pew Research Center’s July 2025 study of nine hundred U.S. adults documented an eight-percent click rate on traditional search results when an AI summary was present versus fifteen percent when one was not – roughly a halving of click-through. Bain & Company’s complementary 2025-2026 research has tracked a fifteen to twenty-five percent reduction in organic web traffic in categories where AI summaries are prevalent. Forrester’s State of Business Buying survey shows ninety-four-percent buyer AI usage and an expansion of buying groups to twenty-two stakeholders, signaling that pre-purchase research has moved structurally into AI surfaces. Layered together, the inputs imply a top-of-funnel contraction in the twenty to thirty percent range under the site model, with steeper declines on early-stage queries and shallower declines on bottom-of-funnel comparison and pricing queries. Forrester did not publish that exact contraction range – the title and headline framing reflect the site model, not a Forrester forecast.

What is the ARC framework and what does it mean operationally?

ARC is Forrester’s prescriptive response to the GTM Singularity. Augmented directs leaders to connect AI agents to key GTM initiatives and to treat buyer agents as members of the buying network – supplying them with relevant content rather than treating them as friction to be filtered out. Resilient directs leaders to abandon static funnel playbooks and re-anchor decisions in actual customer needs, on the theory that the singularity’s defining feature is unpredictability that defeats static approaches. Collaborative directs marketing, sales, customer success, and product to operate from a shared, transparent view of the prospect and customer. For lead-gen operators specifically, the most operationally consequential pillar is the augmented one, because its directive to supply content to buyer agents is, when read through a measurement lens, a directive to instrument content for an audience that does not generate clicks.

How is “AI demand contraction” different from the Adobe AI traffic conversion uplift narrative?

The two narratives describe different phenomena that are easy to confuse. The Adobe data, which has been widely cited in 2025-2026, documents that traffic that does arrive from AI sources converts at materially higher rates than traffic from classical organic sources – sometimes 393 percent or 42 percent higher depending on the metric and category. That finding is real, and it is consistent with the AI surface intercepting earlier-stage research and routing only late-stage, high-intent buyers through to the publisher. The Forrester GTM Singularity finding describes the inverse problem: the volume of pre-funnel research that produces any click at all has contracted by twenty to thirty percent. Both are true simultaneously. The conversion uplift on the surviving traffic does not, in most categories, fully compensate for the volume loss on the contracted denominator.

Why is the contraction structural rather than cyclical?

Three reasons. First, buyer adoption of AI in B2B research is rising rather than stabilizing – Forrester’s ninety-four percent figure (per Forrester’s 2026 State of Business Buying report; not yet independently corroborated by a federal-statistical-agency series, so directional rather than precise) is up from the prior year and climbing. Second, the click-through behavior changes are sticky because the AI summaries are good enough for most buyer questions; the buyer is not deferring the click, the buyer is no longer needing it. Third, the agentic-procurement layer Forrester predicts will affect twenty percent of B2B sellers in 2026 fundamentally changes what a “lead” is – the buyer agent’s handoff to a vendor agent often does not produce a measurable form-fill at all. Cyclical recovery requires one of those three forces to reverse. None shows signs of reversing in the available data.

What is “answer engine optimization” and how does it differ from SEO?

Answer engine optimization (AEO) is the discipline of structuring content, schema markup, entity references, and authority signals so that large language models – ChatGPT, Claude, Perplexity, Copilot, and Google’s AI Overviews – cite the brand when generating answers to user queries. Classical SEO targets ranking position on a results page. AEO targets citation presence inside a generative response. The two disciplines overlap on technical foundations (schema, structured data, page authority) but diverge on the underlying retrieval mechanics; AI surfaces use retrieval-augmented generation that weights cosine similarity and authority signals differently than classical search algorithms. Conductor’s April 20, 2026 launch of AgentStack is one indication that enterprise-grade AEO tooling has moved from intuition to instrumented practice.

What does Forrester’s prediction about “buyer agents” actually mean for lead-gen pricing?

Forrester predicts that twenty percent of B2B sellers will be forced into agent-led quote negotiations in 2026 – that is, negotiations where the buyer side is represented by an autonomous procurement assistant rather than (or alongside) a human procurement manager. For lead-gen operators, this changes the value of a lead in two ways. First, leads sourced from answer engines that the buyer agent queries become structurally more valuable than leads sourced from surfaces the agent does not query. Second, leads delivered with structured, agent-readable metadata become more valuable to vendors with active counteroffer engines than leads delivered as legacy CRM records. The pricing implication is a bifurcation between agent-ready inventory (holding or appreciating) and legacy inventory (trading at a widening discount).

How should lead-gen operators recompute their CPL benchmarks?

The right recomputation has three steps. Step one: estimate the category-specific share of pre-funnel research that has migrated to AI surfaces, using Pew, Bain, and category-specific traffic data as inputs; this becomes the haircut percentage. Step two: apply the haircut to the historical denominator to produce an adjusted denominator that reflects the contracted demand pool. Step three: recompute the CPL ratio against the adjusted denominator and report it alongside the legacy CPL with explicit footnoting of the haircut assumption. The recomputed CPL is the number that should drive media-allocation and buyer-pricing decisions; the legacy CPL is the number that should be used only for cross-year continuity reporting with explicit caveats. Operators who run both numbers in parallel maintain comparability while making decisions on the right denominator.

What are the compliance considerations for agent-ready lead inventory?

Agent-ready lead inventory typically carries more metadata than legacy inventory – verified contact data, intent-signal tags, citation-provenance markers, and scoring metadata. Each additional data layer creates regulatory artifacts under TCPA, the Telephone Robocall Abuse Criminal Enforcement and Deterrence Act, state privacy frameworks like the California Privacy Rights Act, and emerging AI-specific regulations like the EU AI Act’s transparency requirements for automated decision-making. Operators need to validate that their consent disclosures explicitly cover the metadata they are commiting to deliver, that retention policies handle agent-readable lead records appropriately, and that adverse-action protocols address scenarios where a buyer agent declines a lead based on automated scoring. A typical compliance review of an agent-ready inventory tier is a three-to-four-week external counsel engagement; it is not optional.

How will the GTM Singularity affect demand-generation and lead-generation as distinct disciplines?

The GTM Singularity reinforces the strategic distinction between demand generation and lead generation rather than collapsing it. Demand generation, the discipline of creating awareness and preference in the broad buying audience, becomes increasingly mediated by AI surfaces – the practitioner’s measurement primitive moves from impression and engagement metrics to citation-share and model-mention metrics. Lead generation, the discipline of converting expressed buyer intent into measurable funnel events, becomes increasingly bifurcated between agent-ready and legacy tiers. Both disciplines remain real and necessary; the tooling and measurement infrastructure each requires diverges further. Operators who run both as a single function with a single dashboard will struggle; operators who run them as connected disciplines with separate measurement layers will adapt better.

What is the realistic timeline for a mid-sized lead-gen publisher to capture the replatform opportunity?

A typical implementation runs four to six months end-to-end. Entity-graph and schema build takes sixty to one hundred and twenty days for publishers without prior structured-data infrastructure. Citation-share measurement integration takes thirty to sixty days depending on whether the publisher builds or buys the tooling. Agent-ready inventory schema work takes forty to eighty days, including buyer-side documentation and onboarding. CPL ladder re-bench is a fourteen-to-twenty-one-day analytical exercise. Buyer renegotiation runs thirty to sixty days but typically extends because it depends on each individual buyer’s internal cycle. Operators who run the buyer renegotiation in parallel with the engineering work compress the overall timeline; operators who sequence them serially extend it. The publishers who finish ahead of the four-to-six-month timeline are those who started the citation-measurement integration first to accumulate baseline data while the deeper build was in flight.

Sources

Tier 1: Primary Forrester Research and Press

-

Forrester Research, “The GTM Singularity Is Collapsing Traditional Go-To-Market Approaches,” via Business Wire, April 27, 2026 – https://www.businesswire.com/news/home/20260427151500/en/Forrester-The-GTM-Singularity-Is-Collapsing-Traditional-Go-To-Market-Approaches

-

Forrester Research, “Hello, GTM Singularity: Turn Ideas Into Action At B2B Summit North America,” Forrester Blogs, 2026 – https://www.forrester.com/blogs/hello-gtm-singularity-turn-ideas-into-action-at-b2b-summit-north-america/

-

Forrester Research, “The State Of Business Buying, 2026,” Forrester Press Newsroom, January 2026 – https://www.forrester.com/press-newsroom/forrester-2026-the-state-of-business-buying/

-

Forrester Research, “The State Of Business Buying: Risk-Averse Buyers Demand Proof, Not Promises,” Forrester Blogs, 2026 – https://www.forrester.com/blogs/state-of-business-buying-2026/

-

Forrester Research, “Forrester’s 2026 Buyer Insights: GenAI Is Upending B2B Buying As Leaders Face Mounting Pressure To Justify Every Dollar Spent,” via Business Wire, January 21, 2026 – https://www.businesswire.com/news/home/20260121478240/en/Forresters-2026-Buyer-Insights-GenAI-Is-Upending-B2B-Buying-As-Leaders-Face-Mounting-Pressure-To-Justify-Every-Dollar-Spent

-

Forrester Research, “Forrester’s 2026 B2B Marketing, Sales, And Product Predictions: B2B Companies Will Lose More Than $10 Billion Because Of Ungoverned Use Of Generative AI,” via Business Wire, October 28, 2025 – https://www.businesswire.com/news/home/20251028458309/en/Forresters-2026-B2B-Marketing-Sales-And-Product-Predictions-B2B-Companies-Will-Lose-More-Than-$10-Billion-Because-Of-Ungoverned-Use-Of-Generative-AI

-

Forrester Research, “Forrester Announces The Theme And Agenda For B2B Summit North America 2026,” Forrester Press Newsroom, January 15, 2026 – https://www.forrester.com/press-newsroom/forrester-b2b-summit-north-america-2026-agenda/

-

Forrester Research, “The Future Of B2B GTM Isn’t Human Versus AI,” Forrester Blogs, 2026 – https://www.forrester.com/blogs/the-future-of-b2b-gtm-isnt-human-versus-ai/

-

Forrester Research, “The Connected GTM Approach,” Forrester Blogs, 2026 – https://www.forrester.com/blogs/its-time-to-end-disconnected-gtm-efforts/

-

Forrester Research, “The GTM Illusion Is Cracking – These Three Leaders Aren’t Waiting For The Collapse,” Forrester Blogs, 2026 – https://www.forrester.com/blogs/the-gtm-illusion-is-cracking-these-three-leaders-arent-waiting-for-the-collapse/

Tier 2: Independent Research and Trade Press Coverage

-

Pew Research Center, “Google users are less likely to click on links when an AI summary appears in the results,” July 22, 2025 – https://www.pewresearch.org/short-reads/2025/07/22/google-users-are-less-likely-to-click-on-links-when-an-ai-summary-appears-in-the-results/

-

Pew Research Center, “How Americans feel about AI summaries in search results,” October 1, 2025 – https://www.pewresearch.org/short-reads/2025/10/01/americans-have-mixed-feelings-about-ai-summaries-in-search-results/

-

Demand Gen Report, “Forrester’s B2B Marketing Predictions for 2026,” 2026 – https://www.demandgenreport.com/industry-news/news-brief/forresters-b2b-marketing-predictions-for-2026/50729/

-

Digital Commerce 360, “Forrester: B2B buying groups expand as they question AI,” January 22, 2026 – https://www.digitalcommerce360.com/2026/01/22/forrester-b2b-buying-ai-2026/

-

TopRank Marketing, “The CMO Guide to Forrester’s B2B Summit North America 2026,” 2026 – https://www.toprankmarketing.com/blog/forrester-b2b-summit-na-26/

-

Search Engine Land, “Google’s AI Overviews are hurting clicks: Pew study,” 2025 – https://searchengineland.com/google-ai-overviews-hurting-clicks-study-459434

-

Marketing Charts, “More Data Finds AI Overviews Leading to Reduced Clicks,” 2025 – https://www.marketingcharts.com/digital-236587

Tier 3: Vendor and Tooling Announcements

-

Conductor, “Conductor Launches Enterprise AgentStack to Power the Next Era of AI Visibility,” via Business Wire, April 20, 2026 – https://www.businesswire.com/news/home/20260420121997/en/Conductor-Launches-Enterprise-AgentStack-to-Power-the-Next-Era-of-AI-Visibility

-

CMSWire, “Conductor Builds an AEO Stack for AI Search Visibility,” 2026 – https://www.cmswire.com/digital-experience/conductor-launches-agentstack-for-aeo/

-

MarTech Vibe, “Conductor Unveils AgentStack to Scale AEO in AI Search,” 2026 – https://martechvibe.com/article/conductor-unveils-agentstack-to-scale-aeo-in-ai-search/

Tier 4: Supporting Industry Commentary and Data

-

Averi AI, “ChatGPT vs. Perplexity vs. Google AI Mode: The B2B SaaS Citation Benchmarks Report (2026),” 2026 – https://www.averi.ai/how-to/chatgpt-vs.-perplexity-vs.-google-ai-mode-the-b2b-saas-citation-benchmarks-report-(2026)

-

Austin Heaton, “50+ B2B SEO Statistics for 2026: Traffic, Conversion, ROI, and AI Search Data Every Marketer Needs,” 2026 – https://www.austinheaton.com/blog/50-b2b-seo-statistics-for-2026-traffic-conversion-roi-and-ai-search-data-every-marketer-needs

-

The Digital Bloom, “Organic Traffic Crisis Report, 2026 Update: Clicks, AI, Case Studies,” 2026 – https://thedigitalbloom.com/learn/organic-traffic-crisis-report-2026-update/

-

ALM Corp, “AI Citation Patterns by Platform, Industry, and Intent: What the 2026 Data Actually Shows Brands,” 2026 – https://almcorp.com/blog/ai-citation-patterns-platform-industry-brand-strategy/

-

Forrester Research, “Forrester Announces 2026 B2B Return On Integration Honorees And Programs Of The Year Awards Winners For North America,” 2026 – https://investor.forrester.com/news-releases/news-release-details/forrester-announces-2026-b2b-return-integration-honorees-and/

Closing

The April 27, 2026 GTM Singularity research will be remembered, in most marketing-trade-press histories, as the moment Forrester gave a name to a shift the industry had been circling around. That framing is correct as far as it goes. It also misses what the research means for the lead-generation discipline specifically. The structural event is the denominator collapse – the twenty-to-thirty-percent contraction of pre-funnel research that produces a measurable click – and the operational event is the launch of agentic procurement workflows that are already reshaping what a lead is worth on the buy side. The lead-gen operators who treat April 27 as a content marketing memo will spend the next two years optimizing yesterday’s funnel against a denominator that no longer exists. The operators who treat it as a discipline-level reset will run answer-engine-fit content libraries, agent-ready inventory tiers, and re-benched CPL ladders into a margin window that closes when the rest of the market catches up. The decision about which group to be in is being made now, in the next ninety days of planning and the next one hundred and eighty days of build. There is no comfortable third option.

Market data, vendor announcements, and Forrester research findings reflect publicly reported conditions through April 28, 2026. AI search behavior, citation-share measurement methodologies, and agentic-procurement adoption rates change continuously; verify current conditions through primary sources before making operational decisions. This article provides general industry analysis and does not constitute legal, financial, or compliance advice. Consult qualified counsel for specific compliance questions related to agent-ready lead inventory, structured-metadata consent disclosures, and adverse-action protocols for automated buyer-agent decisioning.