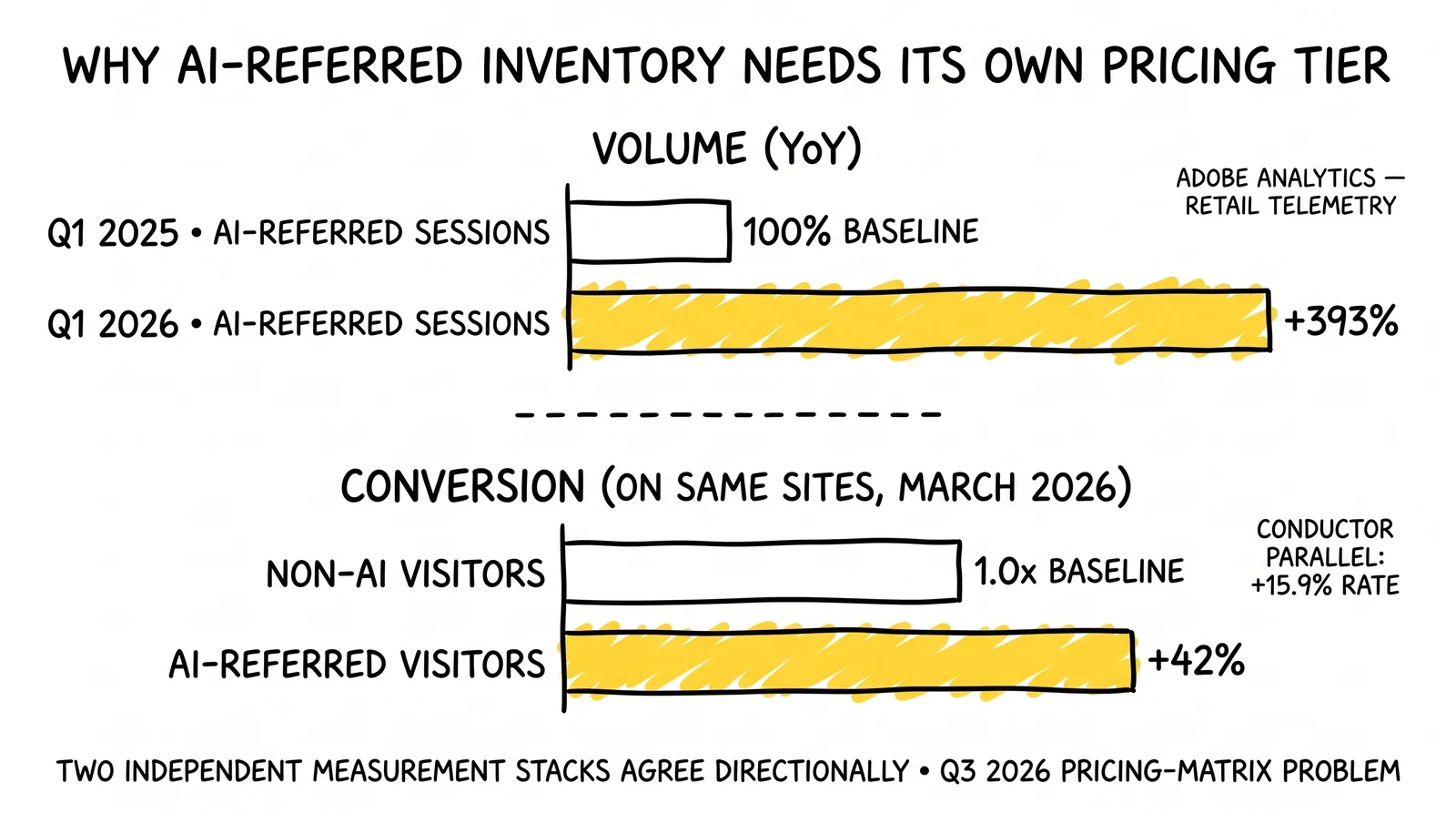

Adobe Analytics reported in mid-April 2026 that AI-source traffic to U.S. retail sites rose 393% year over year in the first quarter, with AI-referred visitors in March converting 42% better than non-AI traffic. Conductor’s AgentStack announcement the same week reframed AI engine visibility as orchestration infrastructure. The combined signal is structural, not seasonal: AI-referred sessions are a different inventory class, and the lead economy’s CPL and EPL pricing matrices need a third dimension to handle them. This piece focuses on the per-session conversion premium and how to price for it; the parallel question of fewer total sessions reaching the funnel – the denominator-contraction side – is treated in the Forrester GTM Singularity pre-funnel demand analysis.

A 393% Volume Jump and a 42% Conversion Premium Walk Into the Same Quarter

Adobe Analytics’ Q1 2026 retail update, covered through trade press on April 14 to 20, 2026, contains two numbers that sit uneasily next to each other. The first is a volume number: AI-source traffic to U.S. retail sites was up 393% year over year in the first quarter of 2026, with ChatGPT-User crawler activity alone up 201% from February to March. The second is a quality number: in March, AI-referred visitors converted 42% better than non-AI visitors, with deeper engagement on the sessions that did not convert immediately. Conductor’s reporting in the same window added a concentration figure – approximately 87.4% of measurable AI referral traffic flowing through ChatGPT – and a conversion-rate figure of about 15.9% on AI-referred sessions in the cohorts Conductor tracks.

Volume and conversion both growing at this pace is what makes the data structural rather than incremental. Most new traffic sources arrive cheap and convert poorly, then stabilize as the channel matures. AI referral traffic is arriving in compounding volume and converting at a measurable premium against the same site’s organic and paid baselines. That combination violates the assumption embedded in most lead pricing matrices, which treat conversion rate as a property of vertical and intent stage rather than of source.

For the lead economy, the practical consequence is that the existing two-axis pricing grid – vertical on one axis, intent stage or exclusive-versus-shared on the other – does not have a place for AI-referred inventory. A buyer paying $30 to $50 for a vertical-benchmark CPL on auto-exclusive inventory is paying for an average conversion rate that no longer represents the inventory they receive when ten percent of it carries a 42% conversion lift. Either the average drifts up over the next two quarters and the buyer captures the premium, or the publisher segments the inventory and prices the AI-referred subset separately. This analysis covers the Adobe and Conductor data, the structural reason a third pricing axis is needed, the design of that axis for insurance, mortgage, and solar verticals, and the implementation work that has to happen in 2026 to capture the premium before buyers price it back into baseline.

What Adobe and Conductor Reported and Why the Combined Signal Matters

The Adobe and Conductor data points were announced separately, sit in different surfaces, and are doing different analytical jobs. Read together, they describe one phenomenon.

Adobe Analytics’ Q1 2026 retail report is built on aggregated commerce telemetry from a large sample of U.S. retail sites – the same dataset Adobe uses for its holiday-season Digital Economy Index and quarterly retail benchmarks. The 393% year-over-year growth in AI-source traffic measures sessions arriving from identifiable AI assistants – ChatGPT, Claude, Copilot, Perplexity, and Google AI Mode – based on referrer headers, user-agent strings, and Adobe’s own classification logic. The 42% conversion premium compares the conversion rate of those AI-referred sessions in March 2026 against the conversion rate of all other sessions on the same sites in the same window. The “deeper engagement” qualifier reflects time-on-site, pages-per-session, and assisted-conversion metrics that Adobe reported alongside the headline number.

Conductor’s reporting on AgentStack, announced in the same April 14 to 20 window, treats AI engine visibility as a managed orchestration problem rather than a measurement problem. The 87.4% ChatGPT concentration figure describes the share of AI referral traffic that flows through ChatGPT specifically – a meaningful share even after accounting for Claude, Copilot, Perplexity, and Google AI Mode growth. The 15.9% conversion rate on AI-referred sessions is a Conductor-tracked benchmark that sits well above typical organic-search conversion rates in the same verticals, supporting the directional claim Adobe made with different data and different methodology.

Why two independent datasets agreeing matters

Both publishers are credible. Both measurement approaches are published. The agreement between Adobe’s commerce-telemetry view and Conductor’s content-platform view reduces the probability that the conversion premium is an artifact of one vendor’s classification rules. Two independent measurement stacks looking at different cuts of the same phenomenon and producing the same directional signal – AI-referred traffic converts materially better than non-AI traffic on the same sites – is a stronger evidence base than either dataset alone.

The remaining uncertainty is mostly about the size and durability of the premium. Adobe’s 42% lift could narrow as AI engines push more head-of-funnel discovery traffic and the AI-referred pool dilutes. Conductor’s 15.9% rate could be specific to the e-commerce-heavy cuts that Conductor’s platform tracks most heavily. Neither caveat is large enough to discard the structural conclusion: AI-referred inventory is converting at a premium today, the premium is measurable on at least two independent measurement stacks, and the volume growth means the inventory class is no longer too small to price separately.

For lead operators, the practical translation is straightforward. A site that had ten thousand monthly sessions in Q1 2025 and three hundred AI-referred sessions has, on Adobe’s growth rate, roughly fifteen hundred AI-referred sessions in Q1 2026 – fifteen percent of inventory. That inventory is converting forty-two percent better than the rest. The blended conversion rate moves up; the publisher captures most of the lift; and the buyer eventually catches up by paying more across the board. Or the publisher segments and prices the fifteen percent separately, captures the segmentation premium directly, and the buyer pays a different price for a different inventory class.

The choice between those two paths is the pricing-architecture decision the next two quarters of lead operations will be made on.

The Two-Axis Pricing Grid That Cannot Hold the New Data

Before designing a third axis, it is worth being explicit about how the current two-axis grid actually works in lead distribution markets. Most publishers and aggregators run something close to the following structure.

The first axis is vertical and intent stage. An auto-insurance lead with current-coverage information, vehicle data, and ZIP code is priced differently from an auto-insurance click that has only ZIP and email. A mortgage lead with credit-band self-report and loan amount is priced differently from a mortgage lead with only loan-purpose intent. A solar lead with utility bill range and roof type is priced differently from a solar lead with only ZIP and homeowner status. Inside each vertical, intent-stage tiers are established through years of buyer-side conversion data and reflect the realized economic value of each stage.

The second axis is exclusivity and shared count. An exclusive auto lead – sold once, to one buyer – typically commands $30 to $50, depending on intent stage and vertical. The same lead sold under a shared model at three or four ping-post recipients will sell through at $50 to $85 in aggregate, with each recipient paying $15 to $25 individually but a higher number of recipients lifting the publisher’s blended yield. The exclusivity dimension is priced because conversion rate falls as buyers compete for the same prospect; the publisher captures more total revenue at the cost of lower per-buyer conversion.

What both axes assume about source

Both axes are silent on source. A lead originating from paid search, organic search, display retargeting, social ads, content syndication, or affiliate networks is priced inside the same vertical-and-exclusivity grid. The implicit assumption is that the conversion rate distribution across sources is roughly uniform once vertical and intent stage are controlled for, with deviations small enough to be absorbed in buyer-side optimization rather than priced into the publisher’s quoted CPL.

That assumption was approximately true through 2024. Source variations existed – paid-search leads in some verticals converted slightly better than display-retargeted leads, for instance – but the deviations were small enough that pricing them separately introduced more operational complexity than margin uplift. Buyers ran source-aware bid logic on their own side; publishers quoted source-agnostic prices; and the market settled at a price that reflected a blended average.

The Adobe 42% conversion lift is too large for that assumption to survive. A 42% lift in conversion rate is the difference between a profitable buyer relationship and an unprofitable one in many verticals. It is the difference between an auto-insurance buyer paying $40 per exclusive lead and the same buyer paying $30 because the average conversion rate on the inventory does not justify the higher price. When fifteen percent of the inventory carries a structurally higher conversion rate than the other eighty-five percent, the source-agnostic price either underprices the AI-referred subset (and the buyer captures the lift) or overprices the non-AI majority (and the buyer pulls back on volume).

Both outcomes degrade the publisher’s margin position over time. The publisher who recognizes this in 2026 and segments the inventory captures the segmentation premium. The publisher who does not is, in effect, subsidizing the buyer’s source-aware optimization.

Why this is a Q3 2026 problem, not a 2027 problem

Buyers are not waiting for publishers to segment. Sophisticated lead-buying operations on the lender and carrier side are already running conversion-rate analysis by source attribution, building source-aware bid logic in their distribution platforms, and shifting budget toward sources that historically over-perform. The 42% Adobe lift will appear in their dashboards within a quarter or two of the Q1 2026 data wave. By Q3 2026, mid-market and large buyers will have run the numbers and arrived at one of two conclusions: bid up uniformly because the average conversion rate is rising, or pay differential prices for source-tagged inventory.

The publishers who are ready to sell source-tagged inventory at the moment buyers arrive at that conclusion will set the new market price. The publishers who arrive late will sell into the same source-tagged demand at the buyers’ chosen prices, with less negotiating leverage and a smaller share of the realized premium.

Designing the Third Axis: Source AI Engine as a Pricing Dimension

A pricing matrix that incorporates source AI engine as a third axis has to handle four operational realities at once: the volume distribution across engines, the conversion premium that varies by engine, the engine-specific cost-to-acquire profile, and the buyer-side bid behavior that the third axis surfaces. None of these is symmetric across engines. A useful third axis is engine-aware, not just source-aware.

Volume distribution: ChatGPT dominates, but the tail matters

Conductor’s 87.4% ChatGPT concentration is the load-bearing data point. Roughly seven of every eight measurable AI-referred sessions arrive through ChatGPT today, with the remaining share distributed across Claude, Copilot, Perplexity, and Google AI Mode in proportions that vary materially by vertical. In e-commerce-heavy cuts, Perplexity tends to over-index because its product-comparison surfaces drive purchase-intent traffic. In B2B and research-heavy cuts, Claude and Copilot tend to over-index because their use-case mix skews toward longer-form work tasks. In informational queries that flow through traditional Google interfaces, AI Mode is taking share that previously belonged to featured snippets and zero-click answers.

For a publisher pricing inventory, the practical implication is that a single “AI-referred” tag is too coarse. A ChatGPT-referred auto-insurance session and a Perplexity-referred auto-insurance session are different inventory items with different downstream conversion behavior, and the buyer that values one will not necessarily value the other at the same level. A useful tag layer carries the engine identity at minimum and ideally carries the engine-plus-surface information (ChatGPT browsing versus ChatGPT search, Claude artifact versus Claude chat, etc.) where referrer data permits.

Conversion premium: not uniform across engines

Adobe’s 42% headline number is an average across engines. The underlying distribution is not uniform. ChatGPT-referred sessions, given their volume share, dominate the average; Perplexity-referred sessions appear to convert at materially higher rates in commerce-intent cuts where the assistant surfaces specific product recommendations; Claude-referred sessions tend to be smaller in volume but high in engagement quality in research-intent cuts. The publishers who segment inventory by engine and report engine-level conversion rates to buyers create a richer pricing signal than publishers who report a single AI-referred conversion rate.

This is the same lesson that emerged from vertical-by-vertical CPA benchmarks over the past five years. Aggregated-average pricing systematically underprices the high-conversion subset and overprices the low-conversion subset. Engine-level segmentation surfaces the underlying distribution and lets buyers bid against the actual inventory rather than a blended average.

Cost-to-acquire profile: engine visibility is not free

The third operational reality is that AI engine visibility carries a cost. A publisher who shows up consistently in ChatGPT citations did so because the publisher’s content was structured for AI ingestion, the site’s technical infrastructure handled AI crawlers correctly, and the publisher’s editorial strategy aligned with the kinds of queries that AI engines route through cited sources. Conductor’s AgentStack framing makes the cost explicit: managing AI engine visibility is a system-level orchestration project with engineering, content, and analytics components. The total annual cost for a mid-sized publisher to build and run AI-engine visibility infrastructure is meaningful – comparable in scale to a mid-sized SEO program – and that cost has to be allocated against AI-referred inventory in any honest CPL calculation.

The practical implication is that AI-referred inventory has both a conversion premium and a cost premium, and the net economic value depends on the ratio. Publishers who calculate the gross conversion lift without accounting for the visibility-program cost will overstate the inventory’s value. Publishers who calculate the net lift after allocating visibility costs will arrive at a tighter but more honest pricing signal.

Buyer-side bid behavior: the surface is not the same

Buyers do not yet bid uniformly on engine-tagged inventory because most lead-buying platforms do not yet ingest engine tags. Engine-aware bid logic is a build that lender and carrier operations teams have on their roadmaps but have not, in most cases, completed. Through the second half of 2026, the buyers most likely to bid on engine-tagged inventory will be the ones who have done their own internal source-attribution work and noticed the lift. Through 2027, engine-aware bidding will spread across the buyer set as platform vendors add the capability and as the conversion premium becomes harder to ignore.

The window during which publishers can extract a premium from engine-tagged inventory is the gap between the moment publishers can supply tagged inventory and the moment buyers can bid intelligently on it. That window is narrow – six to twelve months – but it is the window in which the largest pricing-power gains are available.

Pricing Scenarios: Insurance, Mortgage, and Solar Publishers Under the Third Axis

Concrete scenarios make the third axis tractable. The three verticals below use existing published benchmarks for current pricing tiers and apply the Adobe 42% conversion lift, the Conductor 15.9% AI-referred conversion rate, and reasonable allocation assumptions to arrive at a defensible re-pricing range for AI-referred inventory.

Auto insurance: the $30 to $50 exclusive becomes a $45 to $75 AI-tagged exclusive

The current reference range for an auto-exclusive lead is $30 to $50, depending on intent stage and quality tier, with shared inventory selling through at $50 to $85 in aggregate. Buyer-side conversion rates on auto-exclusive inventory typically run in the high single digits to low teens, with exclusive-versus-shared spreads reflecting the contact-rate differences between exclusive and shared distribution.

Apply Adobe’s 42% conversion lift to the exclusive base. A 12% baseline conversion rate becomes approximately 17% on AI-referred inventory, holding all other variables constant. Buyer LTV math at that conversion rate supports a meaningfully higher CPL, and the resulting pricing range for AI-tagged auto-exclusive inventory lands somewhere between $45 and $75 – a 50% to 60% premium over source-agnostic pricing. The width of the range reflects the engine-mix uncertainty: an inventory pool that is 90% ChatGPT-referred prices differently from one that is 60% ChatGPT and 40% distributed across the other four engines.

For a mid-sized auto publisher running 100,000 monthly leads, with AI-referred share moving from low single digits in 2025 to 12% to 18% by Q3 2026, the realized revenue uplift from segmented pricing on the AI-tagged subset is meaningful – in the seven-figure annual range at the higher end of the volume-and-premium combination. That is the gross uplift, before allocating the visibility-program cost.

Mortgage: the soft-pull pre-qual lead and AI-tagged ChatGPT inventory

Mortgage lead pricing runs higher per unit than auto, with exclusive pre-qualified leads in the $80 to $200 range depending on credit band, loan purpose, and state, and shared inventory at lower per-recipient prices but higher publisher yield. Conversion rates from lead to funded loan run in the low single digits to mid-single digits, with substantial variation by buyer underwriting profile.

Apply the same 42% lift. A 4% baseline conversion rate becomes approximately 5.7% on AI-referred inventory. Lender LTV per funded loan supports a CPL premium in the $40 to $80 range over source-agnostic pricing, depending on the credit band and loan amount distribution of the AI-tagged inventory specifically. Mortgage buyers running their own source attribution will arrive at this number with or without publisher segmentation; the question is whether the publisher captures the premium directly through tagged pricing or indirectly through gradual lift in blended pricing.

The mortgage vertical also has a speed-to-contact dimension that interacts with the source axis. AI-referred prospects who have already had a research conversation with an AI assistant before reaching the publisher’s funnel arrive with stronger intent signal but a tighter time window for buyer follow-up. Publishers who can deliver AI-tagged mortgage leads to buyers within sixty seconds of capture preserve the conversion lift; publishers who hand off through batch or hourly cadences erode it.

Solar: the $200+ exclusive in a vertical where AI search has structural fit

Solar lead pricing sits at the high end of consumer-finance and home-services leads, with exclusive solar leads ranging from $150 to $300 or more depending on geography, household income tier, and credit prequalification status. Conversion rates from lead to installed system run in the low single digits, but the per-customer LTV is high enough to support the front-loaded CPL.

Solar is also a vertical where AI assistants have structural fit. Consumers researching solar adoption ask multi-turn questions about panel options, financing, tax incentives, and installer comparisons – exactly the kind of extended, information-rich conversation that AI assistants surface well. Anecdotally and in early publisher data, solar AI-referred conversion lift sits at the higher end of the cross-vertical distribution, plausibly above the 42% Adobe average.

Apply a conservative 50% lift on solar exclusive baselines. A $200 source-agnostic exclusive becomes a $300 AI-tagged exclusive at the lower end and could justify $400 at the higher end for ChatGPT-referred inventory in high-intent geographies. The premium captures both the conversion-rate lift and the reduced installer-side qualification time on prospects who arrive pre-educated by the AI assistant. For a solar publisher, the third-axis pricing decision is not optional in 2026; it is the difference between continuing to sell at 2024 reference prices in a market where the actual buyer LTV math has moved.

What links all three scenarios

The common pattern is that the third axis surfaces a real conversion premium that exists today and will be priced into the market over the next twelve months one way or another. Publishers who price it directly capture more of it. Publishers who do not price it directly cede it to buyers, who will eventually surface it through their own bid logic. The size of the captured premium depends on three things: how cleanly the publisher can segment AI-referred inventory, how granularly the publisher can tag by engine, and how quickly the publisher can establish tagged pricing with the buyer set before buyers build their own engine-aware bid infrastructure.

Cohort Architecture and Measurement: Making the Premium Provable

Pricing AI-referred inventory at a premium requires the publisher to prove, repeatedly and quantitatively, that the conversion premium is real for the specific inventory the buyer is purchasing. The proof is not a one-time benchmark; it is a continuous reporting infrastructure that surfaces engine-level conversion data alongside the standard lead delivery payload.

What the cohort architecture has to capture

A useful AI-referred cohort architecture captures, at minimum, six fields per session: the AI engine that referred the session, the surface type within the engine (browse versus chat versus search), the entry path (cited link, direct URL, agentic browse), the time-on-site and pages-per-session for the session, the conversion event (form fill, qualified lead, billable lead, downstream conversion), and the buyer destination (which buyer received the lead, in which tier, at what price). Each field is a join key that lets the publisher run cohort analysis at the level the third pricing axis demands.

The architecture has to handle attribution edge cases that traditional UTM-based source tagging does not. AI assistants frequently route users through intermediate links, summarization layers, and client-side redirects that strip referrer data. Publishers who rely solely on referrer headers will systematically undercount AI-referred inventory; publishers who supplement with user-agent classification, session-pattern analysis, and entry-path heuristics will capture a more complete picture. The cost of getting this right is meaningful – measurable engineering work plus analytics-team time – but the publishers who do it run a more credible third-axis pricing claim than those who do not.

Reporting cadence and buyer-side trust

Buyers will only pay tagged-inventory premiums if the tagging is verifiable. A publisher who delivers AI-tagged leads with a black-box “trust us” label will compress the premium against a publisher who delivers AI-tagged leads with engine-level reporting that buyers can validate against their own conversion telemetry. The validation cycle – publisher reports tagged inventory mix, buyer measures realized conversion rate, reconciliation cycle confirms or disputes the tagging – is the trust-building mechanism that lets tagged pricing stick.

Reporting cadence matters as much as reporting accuracy. Buyers operating their own attribution infrastructure want weekly or daily tagged-inventory reports, not monthly. The publishers who build real-time or near-real-time tagged-inventory reporting create a buyer-side experience that supports premium pricing; the publishers who report monthly create an experience that supports a discount.

Measurement maturity and the LLMO dimension

The reporting infrastructure overlaps with LLMO measurement, but it is not the same thing. LLMO measurement focuses on the publisher’s visibility within AI engines – citation share, position, and trajectory across the major assistants. AI-referred inventory measurement focuses on the downstream conversion behavior of users who arrived from those engines. Both feed into pricing decisions, but they answer different questions: LLMO answers whether the publisher is visible in the engines that matter, and AI-referred inventory measurement answers whether the traffic from those engines converts at the premium the publisher has priced into the inventory.

A publisher who runs both measurement programs together has a complete picture: the visibility program tells them which engines are surfacing their content and at what rate, and the inventory program tells them which engines are producing the conversion lift that justifies tagged pricing. The two programs share telemetry and analytics infrastructure but produce different outputs and serve different operational decisions.

Approaches That Will Underperform This Cycle

Three responses to the Adobe and Conductor data are visible in early industry chatter. Each will produce worse outcomes than its proponents expect.

The first is the wait-and-see posture. The argument is that AI referral traffic is still a small share of total inventory, that the conversion premium might narrow as the channel matures, and that pricing infrastructure changes are expensive enough to defer until the data is more settled. The problem is that the data is settled enough now that buyers are already running source-attribution analysis and arriving at conclusions. By Q3 2026, sophisticated buyers will be paying differential prices for source-tagged inventory in their own internal accounting, even if their external bids remain source-agnostic. Publishers who delay will find that the buyers’ internal differential pricing does not flow back to the publishers as higher quoted CPLs; instead, it flows to the buyers’ margin lines as captured surplus on under-segmented publisher inventory.

The second is the AI-referred-as-organic posture. Some publishers are treating AI referral traffic as a higher-converting subset of organic search and pricing it inside the existing organic-search bucket. The problem is that AI referral traffic does not behave like organic search traffic in two important ways. AI referral traffic carries a conversation-history signal that organic search traffic does not – the user has already had a multi-turn discussion with the assistant about the topic before clicking through – and that signal correlates with the conversion premium. Treating AI traffic as organic erases the signal and prices the inventory at organic levels, which understates value by something close to the 42% Adobe lift. Buyers who recognize this will optimize their bids for the publisher’s organic mix, capturing the AI-traffic premium without paying for it.

The third is the all-engines-equal posture. Publishers in this group recognize that AI referral traffic is structurally different but treat ChatGPT, Claude, Copilot, Perplexity, and Google AI Mode as a single bucket with a uniform conversion premium. The problem is that the engines do not perform identically. A buyer whose downstream conversion telemetry shows that ChatGPT-referred prospects convert at 17% and Perplexity-referred prospects convert at 14% will pay more for ChatGPT-tagged inventory specifically and less for the bucket. Publishers who supply only bucket-level tagging price into the average and miss the engine-level premium that more granular tagging would capture.

The unifying pattern is that each posture leaves margin on the table by failing to match the granularity of the publisher’s tagging to the granularity of the buyer’s bid logic. The buyer’s bid logic is moving faster than most publishers expect; the granularity gap will be a 2027 problem for any publisher whose third-axis architecture is not in place by the end of 2026.

The Strategic Reframe: Three Principles for the Re-Priced Funnel

The right response starts from a different premise. AI-referred inventory is a structurally distinct inventory class, the conversion premium is real and measurable, and the pricing infrastructure to capture it is a 2026 build, not a 2027 plan. Three principles flow from that premise.

Principle one: tag inventory at the engine level from the moment of capture

The first principle is that source tagging has to happen at the moment of capture, not as an afterthought during reporting. A lead that enters the publisher’s system without an engine tag cannot be re-tagged later without forensic referrer reconstruction that is expensive and lossy. The publisher’s tracking infrastructure needs to capture and persist the engine identity, surface type, and entry path as fields on the lead record itself, alongside the standard vertical, intent-stage, and exclusivity fields. Once captured, those fields flow through the lead’s lifecycle: pricing, routing, scoring, buyer reporting, and conversion-rate reconciliation.

The build is non-trivial but not enormous. For most lead-distribution platforms, adding engine-level tagging is a sixty-to-one-hundred-twenty-day engineering project plus analytics-team time to update reporting layers and operations-team time to brief buyers on the new fields. The platforms that have already done this work for granular source attribution in other contexts – paid-search keyword tagging, affiliate sub-ID tracking, content-syndication source codes – have most of the architecture in place; the engine-tagging layer is an extension rather than a rebuild.

Principle two: price tagged inventory in tiers, not as a single premium

The second principle is that the premium on AI-referred inventory is not uniform across engines, intent stages, or verticals, and the pricing structure should not pretend otherwise. A useful tiered structure prices ChatGPT-referred high-intent inventory at one premium tier, Perplexity-referred high-intent inventory at a different tier, and bucket AI-referred low-intent inventory at a base premium. The tiering is informed by the cohort-analysis output from principle one and updates as the conversion-rate distribution changes.

Tiered pricing is harder to communicate to buyers than flat-premium pricing, but it produces a higher realized average price across the tagged inventory pool. Buyers in early 2026 are sophisticated enough to handle tier-based pricing; the constraint is the publisher’s confidence in the tiering, which depends on the data infrastructure described in principle one. Publishers who have the data infrastructure can tier; publishers who do not are stuck with flat-premium pricing or no tagging at all.

Principle three: rebuild the buyer waterfall against engine-tagged inventory

The third principle is that the existing buyer waterfall – the routing logic that sends each lead to the highest-bidding buyer – has to absorb the engine-tagged inventory dimension. A waterfall that routes purely on vertical and exclusivity will miss the engine-level price differentials that sophisticated buyers will surface. A waterfall that incorporates engine tags as a routing input can match each lead to the buyer whose engine-aware bid logic values it most highly.

The waterfall update is operationally similar to the model-tagged routing changes that mortgage publishers built in response to the FHFA VantageScore decision in spring 2026: a schema change in the lead-record store, a bid-interface update in the routing platform, an analytics-layer extension to surface engine-tagged margin by buyer, and a buyer-onboarding cycle to communicate the new routing fields. The engineering scope is comparable; the buyer-relationship work is the larger lift, because buyers who have not yet built engine-aware bid logic need time to do so before they can pay for engine-tagged inventory at the prices the data justifies.

Implementation Reality: What It Actually Takes to Run the Third Axis

The strategic reframe is straightforward. The implementation is the work.

Resource requirements

Building engine-tagged pricing infrastructure requires three types of investment. The first is capture-layer engineering: the integration work that detects the AI engine, surface, and entry path of each session and persists those signals on the lead record. The capture layer has to handle the messy reality of AI referrer data, including referrer-header gaps, user-agent ambiguity, and intermediate-redirect attribution. For most lead operators, this is sixty to one hundred and twenty engineering days, depending on the existing tracking infrastructure and the quality of the analytics tooling already in place.

The second is pricing and routing infrastructure. The lead-record schema needs to carry the new fields, the pricing logic needs to apply tiered premiums based on engine and surface, the routing logic needs to incorporate engine tags as bid inputs, and the reporting layer needs to surface engine-tagged conversion data to internal operations and to buyer-facing dashboards. This is forty to eighty engineering days plus product-management time to design the pricing tier structure, validate it against the early data, and update operations playbooks.

The third is analytics maturity. The conversion-rate analysis that proves the engine-tagged premium has to run continuously, with statistical-significance testing on cohort-level data, A/B comparisons against source-agnostic baselines, and reconciliation cycles with buyers. Most lead operators have analytics infrastructure for vertical and intent-stage analysis; extending to engine and surface dimensions is an additional project of forty to sixty days of analytics-engineering plus an ongoing operations cost.

Timeline expectations

A realistic implementation timeline for a mid-sized publisher or aggregator:

| Phase | Duration | Key Activities |

|---|---|---|

| Capture-layer engineering | 60–120 days | AI engine detection; surface and entry-path tagging; referrer reconstruction logic |

| Pricing and routing build | 40–80 days | Schema updates; tier-based premium logic; engine-aware routing; buyer dashboard updates |

| Analytics-layer extension | 40–60 days | Cohort tracking; statistical-significance testing; reconciliation reporting infrastructure |

| Buyer onboarding | 45–60 days | Communicate engine tagging; renegotiate pricing tiers; update buyer integration documentation |

| Total elapsed time | 5–7 months | Conservative estimate for a platform without prior engine-level source tagging |

Source: Composite of publisher implementation patterns across analogous source-attribution upgrades

Common obstacles

Three obstacles consistently slow these implementations. The first is referrer-data quality. AI assistants vary in how they pass referrer information to destination sites; some pass clean referrer headers, some strip them, and some pass intermediate-redirect URLs that obscure the originating engine. Publishers who underestimate the data-quality problem will produce engine tagging that does not match buyer telemetry, which compresses the trust premium that tagged pricing depends on. Investing in high-quality detection upfront – including user-agent classification, session-pattern heuristics, and where possible cooperative tagging arrangements with the engines themselves – pays back in tagging accuracy.

The second is buyer-side readiness. The premium that engine-tagged inventory commands depends on buyers having the bid infrastructure to pay for it. Buyers who have not yet built engine-aware bid logic will pay flat premiums on tagged inventory at best and will treat the tagging as informational at worst. Publisher operations teams who brief buyers ahead of capability rollout, share early conversion data, and offer joint-pilot structures get the buyer infrastructure built faster than publishers who simply ship the new fields and wait.

The third is internal organizational alignment. Engine-tagged pricing requires changes in pricing operations, account management, analytics, and engineering. Publishers whose pricing and analytics teams are siloed from product and engineering will run into coordination friction that adds months to the timeline. The publishers who treat the third-axis project as a cross-functional initiative with executive sponsorship complete the rollout in the five-to-seven-month window; those who treat it as a single-team project tend to slip into the eight-to-twelve-month range.

The implementation is hard. The publishers who complete it before competitors will run a six-to-twelve-month structural margin advantage in the markets where AI-referred inventory share is highest.

Future Implications: The Multi-Year Trajectory of AI-Referred Pricing

The Adobe and Conductor data is a starting point, not an end state. The next twenty-four to thirty-six months will move through several predictable phases.

In the next twelve months, the conversion-rate spread between AI-referred and non-AI inventory will likely remain wide enough to support tagged pricing at meaningful premiums. The volume share of AI-referred inventory will continue to climb; Adobe’s 393% growth rate is too large to sustain indefinitely, but the trajectory remains steep enough that fifteen to twenty-five percent inventory share by late 2026 is a reasonable expectation in commerce-adjacent verticals. ChatGPT will likely retain dominant share but lose some ground to Perplexity in commerce-intent cuts and to Claude in research-intent cuts as those engines mature and gain consumer-facing surfaces.

In the next twenty-four months, the conversion-rate premium will face two competing pressures. On one hand, AI engines will route more head-of-funnel discovery traffic as their consumer adoption deepens, which will dilute the average intent of AI-referred sessions and narrow the conversion premium. On the other hand, AI engines will route more high-intent commerce and decision traffic as users learn to use them for those purposes, which will sustain the premium. The net effect is uncertain, but the premium is unlikely to disappear in the twenty-four-month window; the more likely path is that the headline 42% number compresses to something like 20% to 30% while remaining a structurally significant pricing signal.

In the next thirty-six months, the third pricing axis will become standard infrastructure rather than competitive advantage. By 2029, lead-distribution platforms will treat engine tags as native fields in the same way they treat vertical and intent-stage tags today. Buyers will run engine-aware bid logic by default; publishers will quote engine-tagged prices by default; and the margin opportunity that 2026 first movers captured will be priced into the baseline. The strategic window is the 2026-2028 stretch in which the architecture is scarce and the buyers who can pay for it are concentrated in the more sophisticated end of the market.

The longer-term shift is more interesting. The third axis is not the final state. As AI assistants build commerce surfaces that route purchases directly from the chat interface, the publisher’s role in the funnel changes. A publisher whose inventory is referred from an AI assistant for a final-step research read is one inventory class; a publisher whose inventory is referred from an AI assistant during an in-progress assistant-mediated transaction is a different inventory class. The fourth axis – assistant-mediated versus user-driven session flow – is plausibly a 2027-2028 pricing dimension, as the agentic-browse and assistant-checkout patterns mature.

For lead operators planning beyond the immediate window, the strategic implication is to design the pricing infrastructure for a multi-axis future, not just for the third axis. A pricing architecture that abstracts source attribution into a flexible tag layer – where engine, surface, session-flow type, and other dimensions can be added as native fields without re-platforming – is more durable than one that hard-codes engine tags into the schema as a bolt-on.

Key Takeaways

Adobe’s Q1 2026 retail data and Conductor’s AgentStack reporting describe a structural shift in the lead economy that the existing two-axis pricing grid cannot hold. AI-referred inventory is a distinct inventory class with measurable conversion premium, and the publishers who price it as such will capture margin that publishers who treat it as undifferentiated organic traffic will cede to buyers.

The 393% year-over-year volume growth and the 42% conversion premium are corroborated across two independent measurement stacks (Adobe and Conductor), making the directional claim solid enough to act on without waiting for additional data waves.

The current vertical-by-exclusivity pricing matrix systematically misprices AI-referred inventory, either underpricing the high-converting subset or overpricing the non-AI majority depending on the publisher’s blending choice. A third axis – source AI engine – is the architectural fix.

The third axis has to capture engine identity, surface type, and entry path at the moment of session capture, persist those fields on the lead record, and propagate them through pricing, routing, and reporting. Forensic re-tagging after capture is expensive and lossy; the architecture has to be built into the capture layer.

ChatGPT dominates AI referral volume at approximately 87.4% concentration today, but the engine-mix distribution varies by vertical and by intent stage. Bucket-level “AI-referred” tagging is too coarse to capture the engine-level conversion-rate distribution; useful tagging is engine-specific.

Pricing scenarios in auto insurance, mortgage, and solar suggest the AI-tagged premium runs 50% to 60% above source-agnostic baselines today, with vertical-specific variation. Auto-exclusive moves from $30 to $50 baseline to $45 to $75 AI-tagged; mortgage exclusive moves up by $40 to $80; solar exclusive moves up by $100 or more depending on engine mix and geography.

Three approaches will underperform the cycle: the wait-and-see posture (loses margin every month it persists as buyers run their own attribution), the AI-as-organic posture (erases the conversion-history signal and underprices inventory), and the all-engines-equal posture (misses the engine-level price differentials sophisticated buyers will surface).

Implementation runs five to seven months end-to-end for a mid-sized publisher, with capture-layer engineering, pricing-and-routing build, analytics-layer extension, and buyer onboarding as the four parallel work streams. The buyer-onboarding work is the longest path because it depends on each buyer’s internal cycle.

The 2026-2028 window is the strategic opportunity. Publishers who complete the third-axis build in 2026 capture engine-tagged premiums while buyer infrastructure is uneven; by 2029, the architecture standardizes, the premiums compress to the new baseline, and the early-mover margin advantage closes.

For publishers and aggregators currently running source-agnostic pricing, the next ninety days are the planning window. The next one hundred and eighty days are the build window. The first buyers to bid intelligently on engine-tagged inventory are doing so in the second half of 2026; the publishers who arrive at that conversation with tagged inventory and tiered pricing capture the margin opportunity. The publishers who arrive later compete for what is left.

Frequently Asked Questions

What did Adobe and Conductor actually report in April 2026?

Adobe Analytics, in its Q1 2026 retail report covered through trade press on April 14 to 20, 2026, reported that AI-source traffic to U.S. retail sites was up 393% year over year in the first quarter, that ChatGPT-User crawler traffic specifically rose 201% from February to March, and that AI-referred March visitors converted 42% better than non-AI traffic on the same sites with deeper engagement. Conductor, in its AgentStack launch communications during the same window, reported approximately 87.4% AI referral concentration in ChatGPT and a 15.9% conversion rate on AI-referred sessions in the cohorts Conductor tracks. Both data points sit within the same week of trade-press coverage and describe complementary cuts of the same underlying phenomenon: AI-referred web inventory is growing in volume and converting at a measurable premium against non-AI sources.

Why does this matter for CPL and EPL pricing rather than just for SEO?

The CPL and EPL pricing matrices that govern most lead-distribution markets price inventory along two axes – vertical and intent stage on one, exclusive versus shared on the other – and treat source as a relatively neutral variable inside those buckets. The Adobe 42% conversion lift is too large for that neutrality to hold. When a meaningful share of inventory carries a structurally higher conversion rate than the rest, pricing the inventory at a single average underprices the high-conversion subset and overprices the rest, which degrades publisher margin over time as buyers run their own source-attribution analysis and adjust bids accordingly. The implication is a pricing-architecture decision, not a measurement adjustment: source AI engine becomes a third pricing axis, with tagged-inventory tiers that match the underlying conversion-rate distribution.

Is AI referral traffic large enough to bother segmenting?

The volume question is the most common objection and the most quickly outdated one. In Q1 2025, AI-referred traffic was a low-single-digit share of inventory in most verticals; by Q1 2026, on Adobe’s growth rate, it sits at roughly 12% to 18% in commerce-heavy verticals, with continued growth through the year. By Q3 2026, the share will plausibly cross 20% in commerce-intent cuts. Twenty percent of inventory carrying a 42% conversion premium is large enough to move blended conversion rates by several percentage points, which is far above the threshold at which buyer bid logic should respond. The “too small to bother” framing was correct in 2024 and incorrect in 2026.

How concentrated is AI referral traffic in ChatGPT versus the other engines?

Conductor’s reporting puts ChatGPT at approximately 87.4% of measurable AI referral traffic in early 2026. Adobe’s data does not publish an engine-level breakdown but describes a mix that includes ChatGPT, Claude, Copilot, Perplexity, and Google AI Mode. The concentration is heavily ChatGPT-skewed today but is expected to flatten as Claude, Copilot, Perplexity, and AI Mode mature their consumer-facing surfaces and gain share. The engine mix also varies by vertical: Perplexity over-indexes in commerce-intent cuts, Claude and Copilot over-index in B2B and research-intent cuts, and AI Mode takes share from traditional Google interfaces in informational queries. Single-engine “AI-referred” tagging misses the vertical-specific engine distribution and the engine-level conversion-rate differences.

What does engine-level tagging require that source-agnostic tracking does not?

Engine-level tagging captures the AI engine identity, the surface type within the engine (browse versus chat versus search), and the entry path (cited link, direct URL, agentic browse) at the moment of session capture, then persists those fields on the lead record through pricing, routing, and reporting. The capture infrastructure has to handle messy referrer data – header gaps, user-agent ambiguity, intermediate-redirect attribution – using a combination of referrer parsing, user-agent classification, and session-pattern heuristics. Source-agnostic tracking captures none of this, which means lead records cannot be retroactively tagged without forensic referrer reconstruction that is expensive and produces uncertain results. The capture-layer build is the foundational requirement and is typically a sixty-to-one-hundred-twenty-day engineering project.

How should AI-tagged inventory be priced relative to source-agnostic baselines?

The pricing scenarios in this analysis suggest a 50% to 60% premium on AI-tagged exclusive inventory across the auto-insurance, mortgage, and solar verticals, with engine-mix variation inside that range. Auto-exclusive moves from $30 to $50 baseline to $45 to $75 AI-tagged; mortgage exclusive moves up by $40 to $80; solar exclusive moves up by $100 or more for ChatGPT-referred inventory in high-intent geographies. The premium reflects the conversion-rate lift implied by Adobe’s 42% headline number, applied conservatively to vertical-specific baseline conversion rates and validated against the cohort-level data that engine tagging produces. The right number for a specific publisher depends on the engine mix of their AI-referred inventory, the vertical-specific conversion-rate distribution, and the buyer set’s readiness to pay for tagged inventory; the 50% to 60% range is a starting point, not a final answer.

How long is the window during which engine-tagged premiums will hold?

The premium window is bounded by buyer-side bid infrastructure. As long as buyers cannot bid intelligently on engine-tagged inventory, publishers who can supply tagged inventory capture more of the premium. As buyers build engine-aware bid logic – which is in progress at sophisticated buyers in 2026 and will spread across the market through 2027 and 2028 – the premium compresses to the level at which buyer LTV math supports it. By 2029, engine tags will be baseline infrastructure on both sides of the market, and the early-mover margin advantage will close. The 2026 to 2028 window is the strategic opportunity; within that window, the largest pricing-power gains are available in the first twelve months because that is when the supply-and-demand asymmetry is widest.

What about smaller publishers who cannot build the full third-axis infrastructure?

Smaller publishers who cannot build the full capture-layer and analytics-layer infrastructure can still capture some of the premium through partial measures. The most useful partial measures are: distinct landing pages or campaign trackers for traffic from sources known to send AI-referred sessions; basic referrer-header parsing to identify and tag AI-referred sessions even at lower accuracy; and selective buyer relationships in which the publisher and buyer cooperatively measure conversion rates on the tagged subset. The realized premium will be smaller than what a full third-axis build captures, but the cost is also smaller, and the directional benefit is real. Publishers who skip the conversation entirely will see the largest margin erosion as buyers reprice the publisher’s blended inventory.

How does the third axis interact with existing exclusivity and ping-post pricing?

The third axis sits alongside the existing exclusivity and ping-post dimensions rather than replacing them. An AI-tagged auto-insurance lead can still be sold exclusive or shared, with the exclusivity premium applied on top of the engine-tagged premium. The pricing formula becomes multiplicative across axes: vertical-and-intent baseline times engine-tagged multiplier times exclusivity multiplier. Implementing this in the pricing engine is a schema-and-logic update rather than a redesign; the existing pricing infrastructure carries the multiplicative structure, and the engine-tagged multiplier is an additional input. Buyer-side bid logic absorbs the additional dimension the same way it absorbs the existing dimensions, with engine-aware bid models replacing source-agnostic bid models over time.

What are the compliance considerations for engine-level tagging?

Engine-level tagging captures additional fields on the lead record that describe how the lead arrived rather than what the lead disclosed, which sits adjacent to but generally outside the consumer-disclosure regulatory framework that governs CPL operations. The compliance considerations that do apply include: ensuring that engine-tagged data is not used in ways that would constitute prohibited inferred-attribute marketing under state-level rules, maintaining retention policies that align with the broader lead-record retention framework, and ensuring that buyer-facing reports do not expose individually identifying session data inappropriately. A typical compliance review for the third-axis build is a one-week external counsel engagement focused on these specific points; it is meaningful, but it is smaller in scope than the compliance review required for a multi-stage credit-pull funnel or a regulated-vertical disclosure update.

Does this apply to B2B lead generation as well as B2C?

The Adobe data is specifically B2C retail; the Conductor data spans B2B and B2C. Directionally, the same structural pattern appears in B2B lead generation: AI-referred sessions in B2B research and decision queries are converting at a premium against non-AI sources, with engine-mix differences that favor Claude and Copilot in research-intent cuts. The headline conversion-lift number in B2B is harder to pin down because B2B conversion paths are longer and noisier, but early indications suggest the premium is at least as large as the B2C 42% figure on lead-quality measures (qualified-pipeline rate, opportunity-conversion rate) even where the immediate transactional conversion rate is harder to compare. B2B publishers and aggregators face the same pricing-architecture decision, with the additional complication that B2B buyer cycles for adopting engine-aware bid logic are slower than B2C cycles.

How should this article’s conclusions evolve through 2027?

The expected evolution moves through three phases. Through the second half of 2026, the engine-tagged premium will likely sustain at the 50% to 60% range, with publishers who have built the architecture capturing the most. Through 2027, the premium will begin to compress as buyer-side bid infrastructure matures and as AI-referred inventory share continues to climb (diluting average intent at the margin). By the end of 2027, expect the headline premium to be somewhere in the 20% to 30% range with engine-mix-specific variation, and expect the third axis to be standard infrastructure on the most sophisticated lead-distribution platforms. The strategic implication for 2027 planning is that the architecture that captures premium in 2026 will, in 2027 and 2028, be table stakes; publishers who delay the build into 2027 will be running catch-up against a tightening premium window rather than capturing the early-mover advantage.

Sources

Tier 1: Primary Adobe and Conductor Source Material

-

Adobe Newsroom, “AI-Source Traffic to U.S. Retail Sites Up 393% in Q1 2026,” Adobe Analytics Quarterly Retail Report, April 2026 – https://news.adobe.com/news/2026/adobe-analytics-q1-retail-ai-traffic

-

Conductor, “AgentStack Launch Announcement: Managing AI Engine Visibility as Orchestration Infrastructure,” Conductor Press Release, April 2026 – https://www.conductor.com/news/agentstack-launch-2026

-

Adobe Digital Economy Index, “Generative AI Traffic and Commerce Patterns in U.S. Retail,” Q1 2026 Update – https://business.adobe.com/resources/digital-economy-index.html

-

Conductor, “AI Search Visibility Benchmark Report,” 2026 – https://www.conductor.com/research/ai-search-visibility

Tier 2: Established Industry Trade Press Coverage

-

Search Engine Land, “Adobe says AI-referred shoppers convert 42% better than non-AI traffic,” April 2026 – https://searchengineland.com/adobe-ai-referred-shoppers-convert-better-2026

-

Search Engine Journal, “Conductor launches AgentStack to manage AI engine visibility,” April 2026 – https://www.searchenginejournal.com/conductor-agentstack-ai-visibility-2026

-

Marketing Land, “AI Referral Traffic Reaches Inflection Point: What Adobe’s Q1 Numbers Mean for Marketers,” April 2026 – https://martech.org/ai-referral-traffic-inflection-point-2026

-

AdExchanger, “Conductor’s AgentStack and the Reframing of AI Visibility,” April 2026 – https://www.adexchanger.com/data-driven-thinking/conductor-agentstack-2026

-

Digiday, “Why AI-referred shoppers are converting better – and what brands are doing about it,” April 2026 – https://digiday.com/marketing/ai-referred-shoppers-converting-better-2026

-

The Drum, “AI search is the new SEO frontier – and the conversion data is rewriting the playbook,” April 2026 – https://www.thedrum.com/news/2026/04/ai-search-conversion-data

Tier 3: AI Engine and Vendor Technical References

-

OpenAI, “ChatGPT browsing and citation behavior overview,” accessed April 2026 – https://openai.com/research/chatgpt-browsing

-

Anthropic, “Claude web access and source citations,” accessed April 2026 – https://www.anthropic.com/news/claude-web-access

-

Microsoft, “Copilot grounding and source citations technical overview,” accessed April 2026 – https://www.microsoft.com/en-us/microsoft-copilot/learn/grounding

-

Perplexity, “How Perplexity cites sources,” accessed April 2026 – https://www.perplexity.ai/hub/faq/how-does-perplexity-work

-

Google, “AI Mode in Google Search: how generative answers cite sources,” accessed April 2026 – https://blog.google/products/search/google-search-ai-mode

Tier 4: Supporting Industry Commentary and Analysis

-

eMarketer, “Generative AI Reshapes the Path to Purchase: 2026 Outlook,” April 2026 – https://www.emarketer.com/content/generative-ai-path-to-purchase-2026

-

Forrester, “The State of AI Search and Discovery, Q1 2026,” March 2026 – https://www.forrester.com/report/state-of-ai-search-2026

-

Gartner, “Generative AI Disrupts Search Marketing: Implications for Lead Generation,” 2026 – https://www.gartner.com/en/documents/generative-ai-disrupts-search-2026

-

Boston Consulting Group, “AI-Mediated Commerce: The Next Margin Battleground,” April 2026 – https://www.bcg.com/publications/2026/ai-mediated-commerce-margin-battleground

-

McKinsey, “Generative AI and Consumer Decision Journeys: 2026 Update,” March 2026 – https://www.mckinsey.com/capabilities/growth-marketing-and-sales/our-insights/generative-ai-consumer-decision-journeys

-

Pew Research Center, “How Americans Use AI Assistants for Shopping and Research,” April 2026 – https://www.pewresearch.org/internet/2026/04/ai-assistants-shopping

-

Federal Trade Commission, “Statement on AI-Mediated Marketing and Consumer Disclosure,” March 2026 – https://www.ftc.gov/news-events/2026/03/statement-ai-mediated-marketing

-

Interactive Advertising Bureau, “AI Referral Traffic Measurement Working Group: Interim Report,” 2026 – https://www.iab.com/insights/ai-referral-measurement-2026

Closing

The Adobe and Conductor data points published in April 2026 will be remembered by most operators as a one-week story about AI search growing fast. That framing misses what actually happened. The structural event was the appearance of a measurable, replicable, cross-vendor-validated conversion premium on AI-referred inventory at a volume share that crossed the threshold below which segmented pricing is operationally pointless and above which it is operationally necessary. The lead operators who treat the data as a marketing-curiosity headline will spend the next two years competing on a two-axis pricing grid that systematically underprices their best-converting inventory. The operators who treat it as a pricing-architecture reset will run engine-tagged inventory, tiered premiums, and rebuilt buyer waterfalls into a margin window that closes when the rest of the market catches up. The decision about which group to be in is being made now, in the next ninety days of planning and the next one hundred and eighty days of build. The buyers who can pay for engine-tagged inventory at the prices the data justifies are arriving at that conversation in the second half of 2026; the publishers who arrive ready capture the premium, and the publishers who arrive later compete for what is left. There is no comfortable third option.

Market data, AI engine reporting, and conversion benchmarks reflect publicly reported conditions through April 28, 2026. AI engine surface behavior, referrer attribution, and conversion-rate distributions change continuously; verify current performance through primary sources before making operational pricing decisions. This article provides general industry analysis and does not constitute legal, financial, or compliance advice. Consult qualified counsel for specific compliance questions related to AI-referred session tagging, consumer-disclosure framing, and buyer reporting obligations.