The 2026 AEP is the first enrollment window where Medicare lead supply is finally decoupled from the carrier panel that buys it – and where county-level supply maps matter more than CPL benchmarks.

The shrinkage event that rewrites Medicare lead-gen geography

The 2026 Medicare Advantage Annual Election Period opens October 15, 2026 against the largest carrier-supply contraction since the program was created. Kaiser Family Foundation’s 2026 Medicare Advantage Spotlight, the canonical Tier 1 source for plan-availability data, counts 3,373 individual Medicare Advantage plans for 2026 – a 9 percent decrease from 3,719 in 2025. The average MA-PD beneficiary has 32 plan options in 2026, down from 34 in 2025 and from a peak of 36 in 2024. Total plans across all types fall from 42 to 39 per beneficiary year over year.

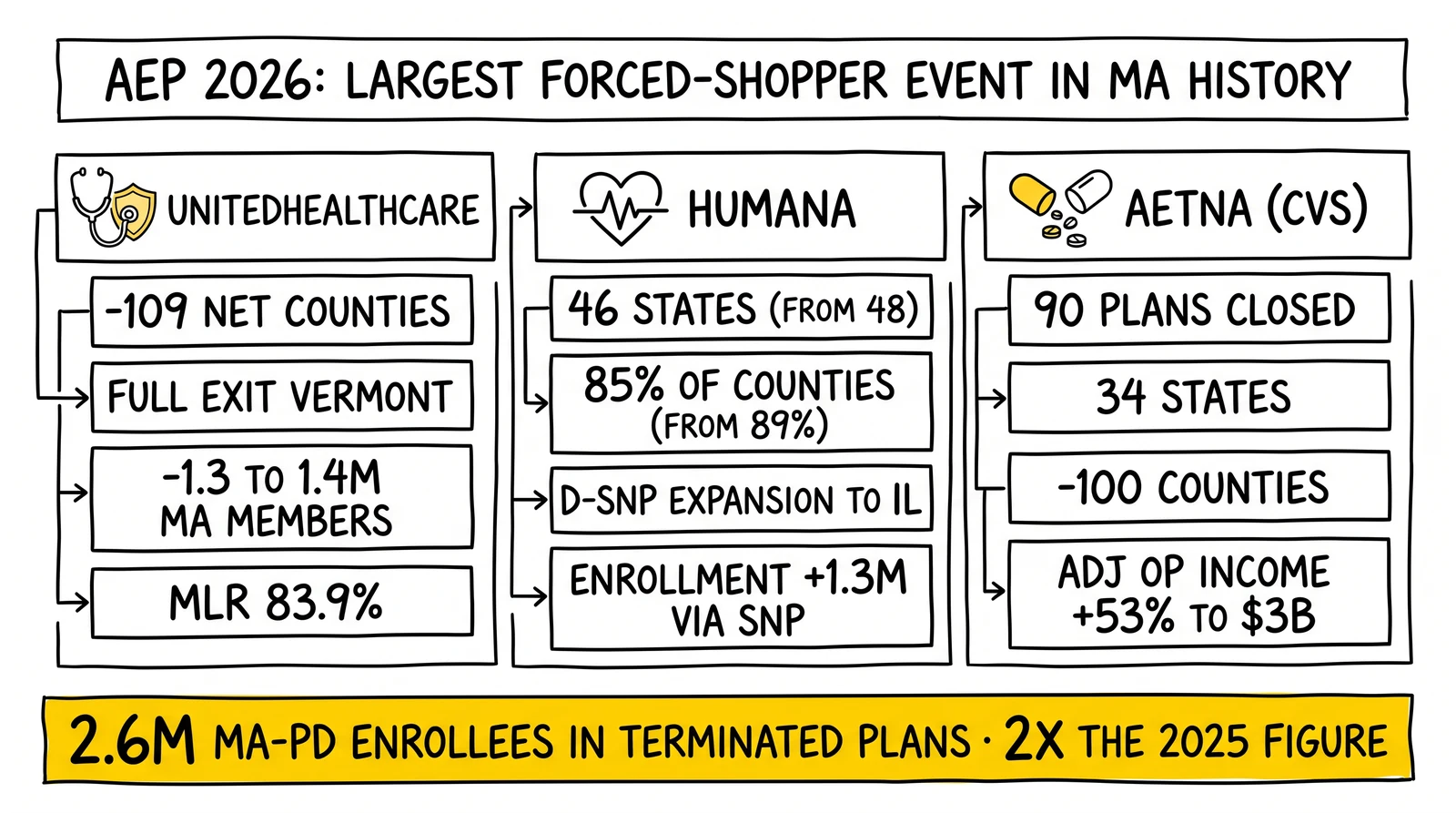

The headline number for forced shoppers: roughly 2.6 million MA-PD enrollees – about 13 percent of total MA-PD enrollment – are in a plan that has been terminated for 2026. That figure is double the 1.3 million enrollees affected in 2025. Layer on plan consolidations and the displaced volume reaches an additional 1.3 million beneficiaries who must reassess coverage even where no termination occurred.

UnitedHealthcare confirmed its individual Medicare Advantage exit from 109 net counties for the 2026 plan year, with a full state exit from Vermont disclosed in non-renewal notices mailed to affected members on October 2, 2025. Humana’s October 1, 2025 press release confirmed the company would offer MA plans in 46 states and Washington DC for 2026 – down from 48 states the year prior – covering 85 percent of US counties versus 89 percent in 2025. Aetna closed nearly 90 individual Medicare Advantage plans across 34 states for 2026, exiting 100 counties on a net basis and one full state.

The lead-gen operator question is not whether carrier exits affect AEP – they always have. The question is whether the 2026 contraction is structural enough to require resetting the panel-mapping assumptions that have governed Medicare lead routing since the program’s market-share equilibrium settled in 2018. The answer this site reaches across the verified data: yes, for rural counties, New England, and the Midwest in particular, and yes for any aggregator pricing a ping-and-post panel without state-by-state buyer availability checks. Operators reading this alongside the companion analysis on the CMS CY2027 Final Rule and the SOA waiting-period kill are looking at the two halves of the same reset: regulation changing how Medicare leads convert, supply changing where they can be sold.

UnitedHealthcare – 109 counties out, 1.3 million members projected loss, margin recovery as the operating thesis

UnitedHealthcare entered 2026 as the largest US Medicare Advantage carrier and exited Q1 as the largest concentrated source of MA membership loss in the program’s history. KFF’s market-share update puts UnitedHealth Group at 9.3 million MA enrollees in 2026 – a decline of 647,000 from 2025 – keeping it at 26 percent share of the MA market. KFF’s plan-offering analysis counts UnitedHealth’s gross county exit at 225 with 14 county entries, for a net reduction of 211 counties; the carrier-reported figure of 109 net county exits reflects only individual MA plan withdrawals and excludes employer-group and dual-eligible movements.

The company’s Q1 2026 earnings call confirmed the strategy is intentional. Seniors served through Medicare Advantage declined by 965,000 in the first quarter alone. UnitedHealth’s full-year 2026 outlook projects 1.3 to 1.4 million MA member losses across the group, individual, and dual special needs segments combined. Medical loss ratio improved to 83.9 percent, down from 84.8 percent a year earlier and well below the analyst estimate of 85.5 percent – confirmation that the membership pruning lifted margins as designed.

The plan-type concentration matters for lead-gen routing. Most discontinued UnitedHealthcare plans were Preferred Provider Organization (PPO) products, which the company stated underperform Health Maintenance Organization (HMO) products on outcomes and affordability. KFF’s plan-mix data tracks the broader market move: HMOs are 57 percent of all 2026 plans and local PPOs are 42 percent, versus a 71-percent HMO and 24-percent PPO split in 2017. The PPO retrenchment is not unique to UnitedHealthcare; it is the structural pattern across the largest carriers.

The county footprint shrank from 87 percent of US counties in 2025 to 80 percent in 2026. For lead-gen operators, that 7-point gap is concentrated geographically – Vermont in full, plus measurable cuts in Minnesota and other primarily rural states. A national MA lead inventory priced against UnitedHealthcare buyer demand in 2025 cannot be sold at 2025 fill rates into the 2026 carrier panel. Operators selling into UnitedHealthcare’s appointment chain through field marketing organizations need a county-by-county map showing where the carrier is still buying and where it is not.

What UnitedHealthcare’s exit changes about lead pricing

Three pricing implications stand out. First, lead aggregators pricing UnitedHealthcare ping bids by zip should re-bid the 2026 panel against the new county footprint; ping-and-post panels that don’t filter against the carrier’s 2026 service-area file will run dead-end pings on inventory the carrier cannot accept. Second, FMOs and IMOs holding UnitedHealthcare appointments in exited counties need to reassign or release agent territories before AEP starts; agents writing inventory through the wrong carrier appointment will lose commissions on plans that do not exist. Third, replacement-plan routing for displaced UnitedHealthcare members should weight Humana D-SNP availability and CVS/Aetna alternatives where they still exist, with Medicare Supplement and stand-alone Part D as the fallback in counties where no MA replacement is available.

Humana – 85 percent of counties, two-state retreat, and the D-SNP growth pivot that masks the contraction

Humana’s 2026 retreat is geographically smaller than UnitedHealthcare’s by absolute count but structurally more revealing about where MA economics work and where they do not. The October 1, 2025 press release confirmed Humana offered Medicare Advantage in 46 states and Washington DC for 2026, down from 48 states in 2025. KFF’s county-level tally put Humana’s gross county exit at 198 with 5 county entries, for a net reduction of 193 counties. The total county-coverage footprint dropped from 89 percent in 2025 to 85 percent in 2026 – Humana’s reported figure – or 82 percent per KFF’s broader methodology.

The paradox in the Humana numbers is the enrollment story. Despite the county exits, KFF’s enrollment update reports Humana grew total MA enrollment to 7.0 million in 2026, a 1.3 million member increase from 2025. The growth concentrates in Special Needs Plans. Humana’s October 2025 announcement confirmed D-SNP expansion to Illinois and C-SNP expansion to Idaho, Maine, and New Jersey. SNP enrollment was the dominant 2026 MA growth lever industry-wide: 8.2 million SNP enrollees represent 23 percent of all MA enrollment, up 900,000 year over year and accounting for 85 percent of net MA growth, with D-SNPs alone at 78 percent of SNP enrollment.

The lead-gen translation: Humana is not pulling out of the MA market, it is concentrating into populations where capitation economics work. Dual-eligible beneficiaries – Medicare-and-Medicaid eligible seniors – generate higher capitation revenue and qualify for SEP enrollment outside the AEP window, which means a year-round inbound lead pipeline rather than a six-week AEP funnel. Humana’s 2026 strategy makes D-SNP intake the higher-value pipeline and general-population MA the deprioritized one.

Humana’s Q1 2026 earnings call reinforced the margin recovery posture. CEO James Rechtin told analysts the company is targeting a return to a sustainable 3-percent individual Medicare Advantage margin by 2028, with a milestone of doubling 2026 margins as a step toward that goal. The 2027 bid cycle is the operational priority. The funding gap relative to medical cost trend is “larger than it was a year ago,” requiring Medicare Advantage benefit adjustments going into 2027. Adjusted EPS guidance for 2026 was reaffirmed at $9.00 with the insurance benefit ratio guided to 92.75 percent plus or minus 25 basis points.

What Humana’s pivot means for FMO commission economics

Industry coverage placed Humana among the carriers that cut or eliminated broker commissions on selected 2026 plans, alongside UnitedHealthcare, Anthem, Centene, and regional insurers including SummaCare. The cuts target plans projected to attract higher-cost enrollees. State insurance departments in Idaho, Delaware, Mississippi, Montana, New Hampshire, North Carolina, Oklahoma, and South Carolina issued warnings that the practice may constitute unfair trade conduct under state law. For Medicare lead-gen operators, the change forces a plan-by-plan commission map: the same Humana inbound lead may convert at full commission, reduced commission, or zero new-enrollment commission depending on the plan the agent writes. Lead routing software that ignores carrier-and-plan commission tiers will mispriced AEP campaigns from the first week.

Aetna – 90 plans down, 34 states affected, and the CVS-driven margin discipline that read across to the panel

Aetna’s 2026 retreat is the cleanest test case of the carrier-margin discipline that has reset Medicare Advantage supply. CVS Health, Aetna’s parent, communicated the strategy explicitly: scale back unprofitable MA inventory and accept the membership loss as the price of margin recovery. Aetna closed nearly 90 individual Medicare Advantage plans across 34 states for 2026, fully exited one state, and reduced county presence by 100. KFF’s enrollment data shows CVS Health at -29,000 MA members year over year on a net basis, a smaller loss than UnitedHealthcare or Elevance because Aetna’s exit volume was concentrated in low-share counties rather than dense markets. KFF’s plan-offering tally puts CVS Health at 160 counties exited with 17 entered, for a net reduction of 143 counties.

The state-level specificity matters for AEP lead routing. Aetna withdrew individual MA plans from most New Hampshire counties – Belknap, Carroll, Cheshire, Grafton, Merrimack, Strafford, and Sullivan – concentrating the New Hampshire MA market for 2026 around the remaining carrier panel. New Hampshire’s 61-percent plan-termination rate for 2026 MA-PD enrollees, per KFF, ranks fifth nationally and is one of five states above 60 percent. Vermont topped the list at 93 percent – the highest plan-termination rate in any state – and South Dakota (64 percent), Idaho (63 percent), and North Dakota (60 percent) round out the five-state group with majority plan termination.

For Medicare lead-gen operators, that geography is the supply-shrinkage map. Vermont, New Hampshire, North Dakota, South Dakota, Idaho, and Wyoming all have plan-termination rates above 60 percent. A lead inventory priced against the 2025 carrier panel in those states will quote 2026 panels at a fraction of historical demand. Aggregators selling AEP inventory into those zips need to reset CPL expectations, reassess panel coverage, and disposition non-MA-eligible inquiries to Medicare Supplement and stand-alone Part D intake rather than burning ping spend on dead pings.

The CVS Q1 2026 earnings report confirmed the strategy hit its margin target. Aetna adjusted operating income rose 53 percent year over year to more than $3 billion. The insurance segment medical benefit ratio dropped to 84.6 percent from 87.3 percent in the year-ago quarter. Full-year 2026 adjusted EPS guidance was raised to $7.30-$7.50 and revenue guidance was lifted to at least $405 billion from at least $400 billion. CVS also exited the Affordable Care Act marketplace entirely across 17 states, displacing roughly 1 million ACA members in addition to the MA membership reductions. The dual exit – ACA and selected MA markets – is the cleanest evidence that the CVS thesis is margin discipline, not market expansion.

Why carriers retreated – V28, RADV, IRA Part D redesign, and utilization

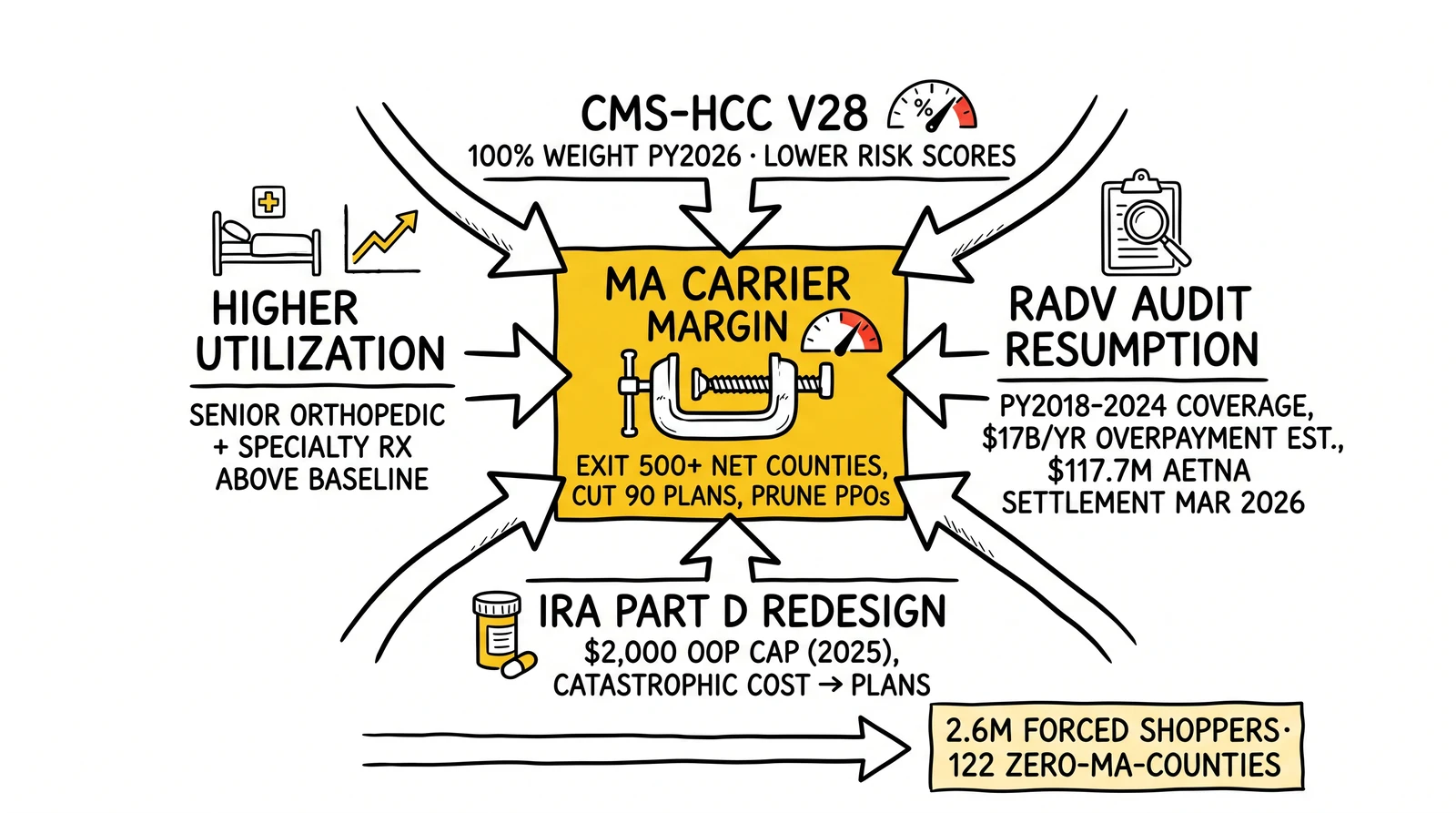

The carrier exits are not a 2026 anomaly. They reflect three structural cost pressures aligning simultaneously with higher-than-projected utilization.

CMS-HCC Model V28. The CMS-HCC V28 risk adjustment model became fully operative for payment year 2026, with 100 percent of MA risk scores calculated under the new model. CMS designed V28 to remove diagnoses that were weak predictors of cost and to require more clinically specific documentation. The downstream effect on plans is lower risk scores per member where V28-removed diagnoses had previously driven payment, which lowers revenue per member. Combined with the phased payment rate updates, V28’s full implementation in 2026 is the single largest revenue-per-member reset since the MA program reached scale.

RADV audit resumption. CMS’s January 2026 RADV memorandum confirmed the agency had resumed active audits covering payment years 2018 through 2024, with sample sizes from 35 to 200 enrollees per contract, a five-month medical record submission window, and new audits initiated approximately every three months. CMS estimates approximately $17 billion in annual MA overpayments from unsupported diagnosis data. The most public enforcement was the Department of Justice settlement with Aetna/CVS for $117.7 million in March 2026, covering PY 2015 retrospective chart review practices where additional diagnosis codes were submitted but unsupported codes were not deleted. RADV exposure is structurally bigger than V28 because the audits are retroactive on coding practices already in the field, and the program covers seven contract years simultaneously.

Inflation Reduction Act Part D redesign. The IRA capped Medicare beneficiary out-of-pocket prescription drug spending at $2,000 for 2025 and shifted catastrophic-phase cost-sharing toward Part D plan sponsors. For carriers that bundle Part D into Medicare Advantage Prescription Drug plans, the redesign shows up as higher per-member Part D liability, particularly for enrollees with high-cost specialty drug utilization. CMS projected a slight decline in average Part D premiums for 2026 – from $38.31 in 2025 to $34.50 – driven in part by the IRA-related premium stabilization demonstration, but the underlying cost pressure on plans remains.

Higher-than-projected utilization. UnitedHealth, Humana, and CVS all flagged higher senior utilization through 2024 and 2025 as a primary cost driver. Senior demand for orthopedic procedures, outpatient services, and specialty pharmaceuticals exceeded actuarial baseline assumptions. Carriers responded with plan-design changes – raised deductibles, raised out-of-pocket maximums, reduced over-the-counter benefits, narrowed networks – and where benefit changes were insufficient, county exits and plan terminations.

The four pressures compound. V28 lowers revenue per member. RADV claws back historical revenue. IRA Part D moves catastrophic cost onto plans. Utilization runs above pricing assumptions. The aggregate is exactly what showed up in 2026 plan filings: fewer plans, fewer counties, leaner benefits, and carriers explicitly stating that the 2026 exit strategy was margin-recovery-first. Medicare lead-gen operators reading those filings should treat them as forward guidance for 2027 supply: if any of the four pressures persists into the 2027 bid cycle, the carrier panel contracts further.

Broker commissions – the second-order shock that hits lead-gen economics directly

The carrier supply contraction is the headline; the broker commission realignment is the lead-gen-direct shock. Industry coverage and state-regulator filings confirm that Humana, UnitedHealthcare, Anthem, Centene, and regional insurers including SummaCare cut or eliminated broker commissions on selected Medicare Advantage plans for the 2026 plan year. The cuts began after the October 15, 2025 AEP opening and concentrated on plans projected to attract higher-cost enrollees.

The Chapter Medicare advisory firm reported through industry coverage that 15 to 20 percent of all MA plans nationally now pay reduced or zero new-enrollment commission, with regional concentrations as high as 25 percent in New York and 35 percent in parts of Georgia. State insurance departments in Idaho, Delaware, Mississippi, Montana, New Hampshire, North Carolina, Oklahoma, and South Carolina have issued formal warnings that the practice may violate state law on agent compensation and beneficiary access. The state-level warnings did not roll back the carrier commission decisions, but they put the carriers in active negotiation with state regulators going into 2026 AEP.

For Medicare lead-gen operators, the commission realignment changes the unit economics of every AEP lead in three ways.

Plan-level routing matters more than carrier-level routing. A lead routed to a Humana D-SNP appointment converts at full commission. The same lead routed to a Humana PPO marked as zero-commission inventory converts the appointment but pays no broker commission for the new enrollment. Lead routing software that priced against carrier-level appointments without plan-level commission overlays will mismatch agent payouts against lead acquisition cost from the first call.

Suitability conversations shift upstream. When a broker’s payout for writing Plan A is $725 and Plan B is $0, the suitability conversation is no longer purely fiduciary – it is also compensation-aware. Lead-gen operators selling exclusive leads to brokers face the question of whether their leads are being written into the plans that pay the broker, the plans that fit the beneficiary, or both. Operators that flag the commission tier at lead handoff give brokers cleaner suitability framing; operators that don’t, ship leads into a payout fog.

The CMS CY2027 commission bump partially backfills. The June 1, 2026 CMS HPMS memo set 2027 national Medicare Advantage initial commissions at $725 per member, up from $694 – a 4.5 percent increase – with regional rates as high as $902 in California and New Jersey. The 2027 maximum allowable commissions reset upward, but Fair Market Value rules let carriers set actual payments below the cap. Carriers cutting 2026 commissions are not legally required to restore them at the new 2027 maximum. The companion analysis on the CMS CY2027 Medicare Final Rule walks through the broker compensation reporting deadline (July 31, 2026) where carriers must disclose actual 2027 rates by plan and channel, the first time that disclosure has been required at the plan level.

For FMOs and IMOs, the commission realignment forces a re-contracting cycle. Agents holding carrier appointments for plans now paying zero new-enrollment commission need to be re-papered against the carriers and plans that do pay. Lead vendors selling into FMO networks need to align their inventory by carrier appointment availability and commission tier, not just by zip. The 2026 AEP is the first AEP where the commission map is plan-by-plan rather than carrier-by-carrier – and the operators that have not built that data layer by October 15 will run AEP without it.

The county-level supply map – where displaced beneficiaries land and where the lead-gen panel cannot follow

The carrier exits are not uniformly distributed. KFF’s county-level analysis shows the 2026 shrinkage concentrated in specific geographies, with replacement-plan availability ranging from robust to non-existent. For Medicare lead-gen operators, the county-level supply map is the operational artifact that determines whether AEP campaigns make economic sense.

The dead zones. KFF identified 122 counties across 13 states with no Medicare Advantage plan availability for 2026, up from 81 counties in 2025. Approximately 391,000 beneficiaries live in those counties. Nearly 65 percent of the 30,000 beneficiaries with no MA-PD options at all live in rural counties across just 8 states. For lead-gen operators, those counties are functionally MA-impossible – any inbound MA lead from those zips routes to Medigap and stand-alone Part D quoting. Lead-gen platforms that don’t pre-tag those zips will spend ping budget on inquiries that cannot monetize as MA enrollments.

The plan-termination hotspots. Vermont topped the list at 93 percent of MA-PD enrollees in a terminated plan. Wyoming, South Dakota, Idaho, New Hampshire, and North Dakota all ran above 60 percent. The hotspot states share two characteristics: rural population concentration and small individual MA market size. Carriers writing scale-driven MA economics cannot make those geographies work; the exits reflect that math. For lead-gen operators, hotspot states are where forced-shopper volume concentrates – but they are also where the carrier panel that buys MA leads has shrunk most aggressively. The disconnect can produce high lead volume that converts at low fill rates if the panel mapping is wrong.

Where 2026 replacement coverage is robust. KFF notes that 98.9 percent of MA enrollees in terminated plans had at least one alternative MA-PD plan available, with the national average of 25 MA-PD options for affected beneficiaries. Most displaced enrollees outside the rural-hotspot states have multiple replacement options – which is where the AEP 2026 lead opportunity exists. The largest controlled-supply lead event in MA history sits inside the AEP October 15 to December 7 window, and operators with carrier appointments and lead inventory aligned to the urban and suburban counties where replacement coverage is dense will harvest most of that volume.

The SNP growth corridor. Special Needs Plans grew 900,000 members in 2026, accounting for 85 percent of net MA growth. D-SNPs reached 78 percent of SNP enrollment, with C-SNPs at 20 percent. SNP enrollment runs year-round under SEP rules rather than only inside AEP, which means SNP-eligible lead pipelines deliver continuous economics rather than seasonal peaks. For Medicare lead-gen operators, the SNP segment is the highest-margin growth corridor in the 2026 MA market – Humana’s D-SNP expansion to Illinois and C-SNP expansion to Idaho, Maine, and New Jersey, and the broader carrier shift toward SNP capitation, point to where the 2027 supply will continue concentrating. Operators building SNP-specific intake funnels (dual-eligibility verification, chronic-condition pre-qualification, low-income subsidy screening) will own the next two-year growth in MA lead-gen while general-population MA panels contract.

The companion analysis on Medicare lead generation AEP and OEP strategies covers the structural seasonality math; the 2026 AEP layer on top of that math is the new county-by-county supply constraint. Operators running the chapter-level review of vertical AI lead disruption in Medicare are looking at what AI does to the funnel; this analysis covers what the carrier panel does to the panel.

Operator playbook – five moves before October 15, 2026

The 2026 AEP runs October 15 through December 7, with the marketing window opening October 1 under the CMS CY2027 Final Rule’s effective date. Five operator actions sit inside the prep window between June and October 2026.

Build the county-level supply map. Pull the CMS Plan Finder 2026 data and the carrier-published 2026 service area files. Overlay against the broker network’s contracted carrier appointments. Identify panel gaps by zip – counties where the lead vendor has inventory the carrier panel cannot accept. Re-price ping bids accordingly. Suppress inventory from the 122 zero-MA-availability counties identified by KFF; route those inquiries to Medigap and stand-alone Part D funnels rather than burning AEP spend on dead pings.

Pre-segment displaced-beneficiary leads by source carrier. Vermont UHC members, New Hampshire Aetna members, Florida Humana members, and other large-block displaced segments have predictable replacement-plan landing patterns. Pre-segmenting the lead pool by current carrier lets the agent lead with replacement-plan options rather than discovery questions, compressing the call-to-enrollment timeline inside the new same-call SOA flow.

Build the plan-by-plan commission map. Carrier-level commission averages no longer represent agent payout reality. Build a plan-level commission overlay against the 2026 carrier panel – flag every zero-commission and reduced-commission plan, surface the flag at lead handoff, and exclude zero-commission plans from FMO appointment recruiting. The CMS HPMS broker compensation submission deadline of July 31, 2026 will surface the carrier-by-carrier and plan-by-plan rates for 2027, which gives operators their first publicly verifiable commission map.

Retrain the call floor on same-call SOA under CY2027. The CMS CY2027 Final Rule’s October 1, 2026 effective date eliminates the 48-hour Scope of Appointment waiting period and the 12-hour gap between educational and marketing events. Inbound and outbound flows can collect a signed SOA and proceed to plan-specific discussion in the same call. The companion analysis on the SOA waiting-period kill walks through the script re-engineering required. The 2026 AEP is the first AEP where the SOA timing constraint is gone – operators that adapt their call flows fastest will compress lead-to-enrollment cycle times against the competition.

Reconcile CRM disposition trees for non-MA-eligible inquiries. Zero-MA-availability counties, beneficiaries holding existing Medigap policies that meet their needs, and beneficiaries who fail dual-eligibility or chronic-condition qualification for SNP enrollment all need disposition codes that route to alternative lines of business rather than AEP MA enrollment workflows. The companion compliance review on the Davis Healthplex emergency-purposes TCPA exception in insurance covers the consent posture for outbound contacts; the disposition tree change covers the inbound side of the same workflow.

Key Takeaways

- Roughly 2.6 million Medicare Advantage Prescription Drug enrollees – 13 percent of total MA-PD enrollment – are in plans terminated for 2026, double the 2025 figure. An additional 1.3 million enrollees face plan consolidations. AEP 2026 is the largest forced-shopper event in MA program history and the prep window closes October 15.

- UnitedHealthcare exited 109 net individual MA counties for 2026, fully exited Vermont, and projects 1.3 to 1.4 million MA member losses across the year. KFF’s broader county tally puts the net change at -211 counties. Most discontinued plans were PPO products. UnitedHealth’s Q1 2026 MLR fell to 83.9 percent, confirming margin recovery as the operating thesis.

- Humana reduced its 2026 footprint to 46 states and Washington DC and 85 percent of US counties, a net reduction of 193 counties per KFF. Total MA enrollment grew 1.3 million members to 7.0 million because D-SNP and C-SNP expansion offset general-population losses – the carrier is concentrating into capitation-economic populations and exiting the rest.

- Aetna closed nearly 90 individual MA plans across 34 states and exited 100 counties. CVS Q1 2026 confirmed Aetna adjusted operating income up 53 percent to over $3 billion and the insurance medical benefit ratio dropped to 84.6 percent. CVS also exited the ACA marketplace across 17 states, displacing roughly 1 million additional ACA members.

- Four structural pressures drove the exits: CMS-HCC V28 at 100 percent weight for PY 2026 reducing revenue per member; RADV audits resumed covering PY 2018-2024 with an estimated $17 billion in annual MA overpayments at stake; IRA Part D redesign shifting catastrophic-phase cost-sharing onto plans; higher-than-projected senior utilization through 2024-2025.

- Broker commissions were cut or eliminated on 15-20 percent of MA plans nationally – exceeding 25 percent in New York and 35 percent in parts of Georgia per Chapter Medicare data – by Humana, UnitedHealthcare, Anthem, Centene, and regional carriers. State insurance departments in eight states have issued warnings on the practice. The commission map is now plan-by-plan, not carrier-by-carrier.

- 122 counties across 13 states have no MA plan availability for 2026, up from 81 counties in 2025. Approximately 391,000 beneficiaries live in those counties. Vermont, Wyoming, South Dakota, Idaho, New Hampshire, and North Dakota all had MA-PD plan-termination rates above 60 percent. Lead-gen operators selling inventory in those zips need disposition trees that route to Medigap and stand-alone Part D rather than AEP MA workflows.

- SNP enrollment grew 900,000 members in 2026 and accounted for 85 percent of net MA growth. D-SNPs reached 78 percent of SNP enrollment. SNP eligibility allows year-round enrollment under SEP rules, making SNP-specific intake the highest-margin growth corridor in 2026 Medicare lead-gen – and the most defensible against the 2027 supply contraction that the same carrier pressures will likely produce.

- The CMS CY2027 Final Rule’s October 1, 2026 effective date eliminates the 48-hour SOA waiting period and the 12-hour educational-to-marketing gap. Combined with the 2026 carrier exits, the AEP 2026 lead-gen environment is the most operationally compressed and supply-constrained AEP in program history. Operators that build county-level supply maps, plan-level commission overlays, and same-call SOA flows before October 15 will compete against operators still running 2025 panel assumptions.

Sources

- Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings (Kaiser Family Foundation, October 2025)

- Medicare Advantage in 2026: Enrollment Update and Key Trends (Kaiser Family Foundation, 2026)

- Most Medicare Beneficiaries Affected by Plan Terminations in 2025 Have Robust Medicare Advantage Options in 2026 (Kaiser Family Foundation, 2025)

- UnitedHealthcare, Humana, Aetna scale back Medicare Advantage plans for 2026 (Healthcare Dive, October 2025)

- Aetna to close nearly 90 Medicare Advantage plans in 2026 (Modern Healthcare, October 2025)

- Humana’s 2026 Medicare Advantage Plans Prioritize Simplicity, Stability and Quality Care for Beneficiaries (Humana Press Release, October 1, 2025)

- Major Insurers Scale Back Medicare Advantage and Part D Plans for 2026 (Kiplinger, 2026)

- UnitedHealth Group Reports First Quarter 2026 Results (Morningstar Business Wire, April 2026)

- Aetna drives CVS earnings in the first quarter (Healthcare Finance News, May 2026)

- CMS Releases Update on Medicare Advantage RADV Audit Plans (AHCA/NCAL, 2026)

- Major health insurers like Humana, UnitedHealth are cutting broker commissions to avoid costly Medicare enrollees (STAT News, November 25, 2025)

- Medicare Advantage Plans Continue Market Overhauls In 2026 (Oliver Wyman, October 2025)

- UnitedHealth Group Q1 2026 Results – Medicare Market Insights

- Humana (HUM) Q1 2026 Earnings Call Transcript (The Motley Fool, April 29, 2026)