Snap’s April 15, 2026 announcement disclosed 1,000 job cuts, a $500 million-plus annualized savings target, and that more than 65 percent of new code at the company is now written by AI. Those are the publisher-side facts. The lead-gen-side reading – that the cost-base reset may correlate with structurally cheaper Gen Z inventory through Q3 2026, and that the 65 percent AI-code share creates conditions where auction-stack volatility is plausible – is a hypothesis on top of the facts, not a direct consequence of them. This analysis separates the two and covers what to do with each.

Disclosure boundary

What Snap disclosed (factual): a 16% workforce reduction, a $500M+ annualized cost-base reduction targeted by H2 2026, and a 65%-plus AI-written share of new code at the company.

What this article infers (hypothesis): CPM and auction-stability effects on lead-gen inventory follow as scenarios – not direct, mechanically-caused outcomes – and the operator playbook below is conditional on those scenarios.

A Two-Sided Event for Snapchat Advertisers

On April 15, 2026, Snap Inc. CEO Evan Spiegel sent a staff memo announcing that the company would reduce headcount by approximately 1,000 employees – sixteen percent of its global workforce – and close roughly 300 open positions. The financial framing was straightforward: a more than $500 million reduction in annualized cost base by the second half of 2026, with U.S. employees receiving four months of severance, healthcare coverage, equity vesting, and transition support. The market reading was equally clean. Snap’s shares jumped about seven percent on the announcement, and analysts framed the reset as a margin story.

The detail that mattered for advertisers sat in the body of the memo, not the headline. Spiegel disclosed that AI now writes more than 65 percent of new code at Snap, and that small teams paired with AI tools have already driven the recent product progress on Snapchat+, the ad platform, and infrastructure. Read narrowly, this is a productivity claim. Read structurally, it is a disclosure that the engineering footprint underneath Snap’s auction, ranking, targeting, and pacing systems has changed in shape. The publisher side of the inventory marketers are buying now sits on a smaller human-engineering layer paired with a larger AI-generated-code layer.

For lead generation operators routing budget into Snapchat against Gen Z-tilted verticals – renter’s insurance, pet insurance, fintech checking accounts, gig-economy services, supplemental health policies – the announcement creates two scenarios worth modeling. On the cost side, Snap is on track to remove more than half a billion dollars of annual operating cost while protecting and accelerating ad-product velocity, a pattern that has historically correlated with more inventory at lower price points when platforms push for bookings velocity; the layoff event itself does not mechanically reduce CPM, but it is consistent with cheaper Gen Z inventory in Q2-Q3 2026. On the stability side, an auction stack maintained by a smaller engineering organization on a code base where two-thirds of new commits originate from AI tools is, on the margin, a less predictable auction stack. Auction outcomes that drift on the publisher side typically translate to CPL volatility on the buyer side; the size and direction of that translation is an operator hypothesis to monitor, not a guaranteed effect of the layoffs.

This analysis covers what changed on April 15, why the disclosure matters more than the layoff count, how the inventory math on Gen Z verticals re-prices in the Q2-Q3 2026 window, what the parallel Anthropic-overtakes-OpenAI shift means for the model writing the ad creative on the buyer side, and what concrete safeguards operators should install before entering the trough. The premise throughout is that Snapchat is becoming a tactical inventory window for the next two quarters, not a strategic platform shift, and the operator playbook is correspondingly tactical.

What Changed on April 15, 2026 – and Why the AI-Code Disclosure Matters More Than the Layoff Count

The headline number was 1,000 employees. The number that matters for ad buyers is sixty-five percent.

Spiegel’s memo, posted to the Snap newsroom under the title “Organizational Changes at Snap,” framed the reduction as a re-shape rather than a contraction. The company would continue investing in AR, AI, and advertiser products. Smaller, focused teams paired with AI agents would handle work that larger teams handled previously. The financial guideposts – more than $500 million in annualized run-rate savings by H2 2026 – were the kind of disclosure that let analysts re-model the margin trajectory in a single afternoon. The seven percent stock pop reflected that re-modeling.

The AI-code disclosure was the structural news. A publicly traded ad platform telling investors and advertisers that more than two-thirds of its new code is AI-written is, in April 2026, still a relatively rare disclosure. It signals three things that affect how the auction behaves for buyers. First, the rate at which Snap can ship ad-product changes – new objectives, new placements, new measurement endpoints, new bidding logic – is higher than the engineering-headcount math would suggest, because the AI-code layer compresses the cost of any individual product change. Second, the variance of those changes is higher, because AI-generated code without dense human review carries different bug profiles than human-written code, particularly in the kind of distributed-systems and ranking-model code paths that auction infrastructure depends on. Third, the cost of running the platform is structurally lower, which gives Snap room to compete on advertiser take rate and inventory pricing in ways that are difficult for higher-fixed-cost ad networks to match.

For an advertiser, the first effect is mostly positive – faster product iteration usually translates into better targeting and better measurement over a 12-to-24-month window. The second effect is mixed and operationally important – auction volatility creates both opportunities and risks within shorter time frames. The third effect is the inventory-pricing thesis that frames the rest of this analysis.

The savings math, translated into inventory terms

Snap reported revenue of $1.363 billion in Q1 2025 with full-year 2026 expected in the $7.2 billion range. Removing $500 million-plus from the annualized cost base against that revenue pool is a structural margin event that does not require revenue acceleration to be visible. What it does require, however, is sustained or growing booked ad demand to translate into the gross-margin narrative the stock priced. In a quarter when the engineering org is undergoing a sixteen percent reduction and a model-collaboration reset, the most reliable way Snap can sustain bookings is to lower friction for advertisers – looser eligibility on new objectives, expanded match rates on customer lists, faster auto-bidding ramp-up on cold accounts, and, when bookings velocity slows, lower clearing CPMs to absorb whatever budget elasticity exists in the advertiser base.

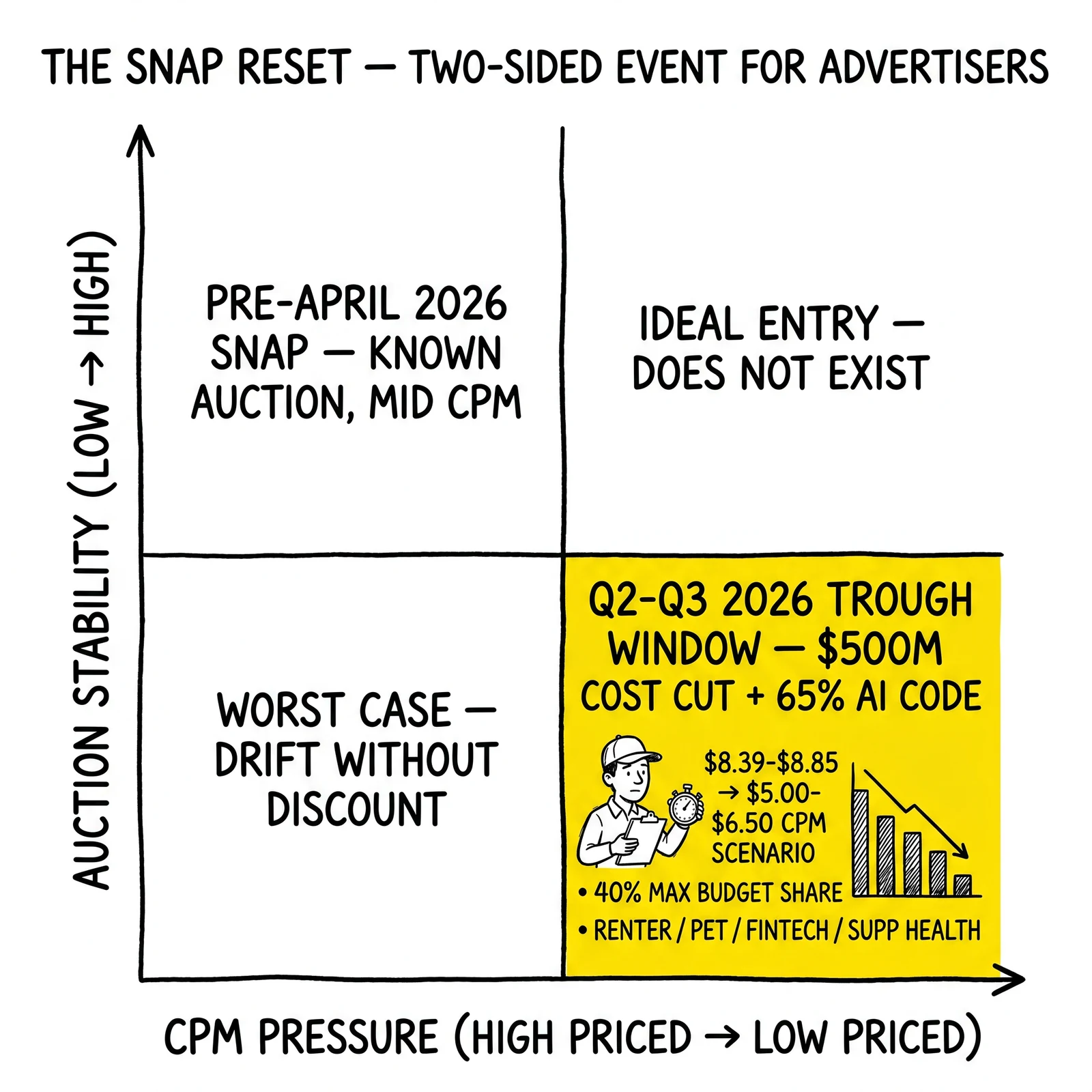

Industry CPM commentary published earlier in the year estimated Snapchat’s average CPM in the $8.39 to $8.85 range, well below Meta and TikTok benchmarks for comparable Gen Z reach. The April 15 announcement does not by itself drive that figure lower in any short-run measurable way. What it does do is widen the corridor in which the auction can clear at lower CPMs without violating Snap’s internal margin guardrails. Operators who model CPM as a single point estimate will miss the corridor. Operators who model CPM as a distribution and bid against the lower tail will find a window in Q2-Q3 2026 that did not previously exist.

The Anthropic / OpenAI overlay

The parallel shift in enterprise LLM market share matters here in a way that is not obvious from the news cycle. Per Menlo Ventures’ 2025 State of Generative AI in the Enterprise survey of nearly 500 enterprise AI decision-makers, Anthropic now commands roughly forty percent of enterprise LLM API spend, up from twelve percent in 2023. OpenAI’s share fell to twenty-seven percent over the same period from fifty percent in 2023. Crunchbase’s Q1 2026 data showed global venture funding hit $300 billion for the quarter with AI absorbing $242 billion – more than eighty percent of the total – and OpenAI ($122 billion), Anthropic ($30 billion), xAI ($20 billion), and Waymo ($16 billion) accounting for sixty-five percent of the quarter’s total. American Express’s April 16 acquisition of Hyper – a Sam Altman-backed AI expense-management startup – is one signal among many that enterprise budgets for AI tooling are being captured at the strategic-acquisition layer.

This matters for Snap advertisers in a specific way. The model that writes the creative an SDR or media buyer ships into Snap matters more – not less – when sixty-five percent of the publisher’s own code is AI-generated. The reason is asymmetric. If the Snap auction is increasingly driven by ranking and eligibility logic that itself originated in AI-coded systems, the creative artifacts that perform best are the ones whose own production pipeline shares structural priors with the platform’s ingestion logic. In practical terms, creative iterated through Anthropic’s Claude or OpenAI’s GPT family produces certain stylistic and structural patterns – copy density, hook placement, descriptive specificity, image-prompt syntax – that interact with whatever ranking system the platform runs. When both sides of the conversation are AI-mediated, the effective creative-iteration rate is higher than the human-mediated baseline. Operators on creative pipelines that still rely entirely on human-written copy and prompt-thin image generation are competing against operators whose pipelines are end-to-end AI-mediated, against an ad platform whose own code base is now AI-mediated.

The Anthropic-versus-OpenAI choice within that creative pipeline is not central to this article, but the fact that one is overtaking the other in enterprise share is the backdrop. The infrastructure decision underneath an operator’s creative testing framework compounds with the decisions that ad platforms like Snap are making about their own code base, in ways that the next twelve months will surface in performance data.

The Inventory Trough Scenario: Why Q2-Q3 2026 May Be a Tactical Window

Three independent forces, taken together, create a scenario in which Q2-Q3 2026 acts as a CPM trough on Snapchat for Gen Z-tilted lead generation verticals. Treating any one of them in isolation understates the scenario; treating the scenario as a guaranteed outcome of the layoffs misreads what the publisher disclosed. The trough framing below is a planning scenario, not a direct consequence of the April 15 announcement.

Force one: Snap’s cost base collapses against a sustained-or-growing revenue pool

The mechanical version of this argument runs as follows. Snap’s Q1 2025 revenue was $1.363 billion, up fourteen percent year-over-year. The company has communicated double-digit growth in advertising revenue over the next two years, with 2026 ad revenue projected in the $5.9 billion range. Removing more than $500 million of annualized cost – the figure Spiegel committed to in the April 15 memo – represents roughly seven percent of that revenue line dropping straight into operating margin if revenue stays on the projected slope. That is the analyst-facing math.

The advertiser-facing math is that any platform pursuing a margin expansion of that scale, on top of an engineering-headcount reduction of sixteen percent, has strong internal incentives to maintain bookings velocity. Bookings velocity at flat or rising CPMs requires demand that grows in line with inventory. Bookings velocity at flat demand and rising inventory requires CPMs to fall enough to clear the marginal impression. Snap’s audience engagement metrics – 477 million daily active users as of Q3 2025 with Gen Z reach exceeding ninety percent in core markets – suggest inventory growth is structural. The Q2-Q3 2026 window is exactly when the cost-cut savings will be visible in the income statement and when the platform will most want to demonstrate that the AI-code investment is producing both cost compression and bookings momentum. The CPM corridor widens in that window.

Force two: advertisers competing for Gen Z reach are diversifying off Meta and TikTok

The second force is parallel inventory dynamics on the platforms Snapchat competes with. Meta’s lead-quality dynamics are under sustained pressure, as documented in the 2026 collapse of Facebook lead-ad CPL stability, and TikTok continues to operate under a U.S. regulatory overhang that creates persistent advertiser-side risk discounting. Performance budgets that were comfortable concentrating on Meta and TikTok for Gen Z reach are now being asked to model alternative inventory sources. Snapchat is the most natural alternative on demographic fit alone – the platform’s 18-to-24 demographic concentration is structurally larger than Meta’s or TikTok’s on a comparable-reach basis.

The diversification flow does not, on its own, lower CPMs on Snap. It raises them in the absence of any other change. What it does do is bring incremental advertiser demand onto the platform precisely when Snap is most motivated to show that demand is sustainable. The intersection of those two flows – diversification-driven demand and cost-cut-driven inventory – is the trough geometry. The trough will not last, because as diversification-driven demand stabilizes, CPMs will normalize. But for the window in which Snap’s margin expansion is being publicly demonstrated and diversification flows are still ramping, the corridor is open.

Force three: the auction stability question

The third force runs in the opposite direction and is the reason the trough is a tactical window rather than a structural shift. An auction stack maintained by a smaller engineering organization on a code base where two-thirds of new commits originate from AI tools is more variable than the same stack maintained by a stable, larger human-engineering footprint. Operators who plan against the trough need to plan against the variance simultaneously.

The variance shows up in three places that matter for lead generation. First, eligibility logic – which audiences a campaign can reach, which lookalike sources match well, which custom-list match rates clear – is driven by code paths that change frequently as ad-product engineers ship updates. Second, pacing – how fast a campaign spends through its budget, whether it fronts-loads or back-loads, how it responds to mid-flight changes – is driven by code that interacts with both inventory supply and bidder-side demand. Third, attribution and event-quality scoring – which events Snap will count, how well the platform matches conversions back to impressions across iOS and post-cookie web – is driven by code that has historically been one of the more bug-prone areas of any ad platform.

Each of these three areas is more likely to drift in a code-base that is both shrinking on the human side and expanding on the AI side. None of those drifts, individually, is catastrophic for an operator. The combination is operationally consequential because the drifts can compound – a pacing change combined with an eligibility change combined with an attribution change can move CPL by an order of magnitude over a 72-hour window in ways that are hard to attribute back to any single cause.

The trough is real. The variance is also real. The operator move is to enter the trough with safeguards that contain the variance, not to enter the trough as if it were a stable opportunity.

The Verticals Where the Trough Math Works Best

Not every Gen Z-tilted lead generation vertical benefits equally from the Q2-Q3 2026 trough. Three verticals are structurally favored, and one is structurally challenged.

Renter’s insurance: structurally favored

Renter’s insurance is the cleanest fit. The product carries a low-friction quote action – typically a three-to-five-field form returning a sub-$15 monthly premium quote – and a clear consumer trigger in the form of move-in events, lease renewals, and roommate changes. Snapchat’s user base over-indexes on the demographic that is both renting at high rates and approaching the move-in trigger frequency more often than older cohorts. According to Snapchat’s own insurance-vertical research, Snapchatters are 1.4 times more likely than non-Snapchatters to be insurance policyowners, and two-thirds of daily users hold multiple policies.

The trough math works because the unit economics of renter’s insurance allow a wide CPL band. A renter’s policy with a roughly $180 annual premium and a multi-year retention curve can sustain a CPL in the $25 to $60 range without compressing carrier margin. At a Snapchat CPM in the $7 to $8 range with a one-to-two percent click-through rate and a five-to-ten percent on-page conversion rate, that CPL is achievable today on tightly targeted campaigns. If the trough produces clearing CPMs in the $5 to $6.50 range – a plausible scenario given the savings profile – the achievable CPL drops into the $18 to $42 band, opening the vertical to more aggressive bid postures from carriers. The relevant CPL benchmark range across major lead-gen verticals provides the comparison frame.

Pet insurance: structurally favored

Pet insurance carries a different consumer trigger profile – typically tied to new-pet adoption, vet visits, or breed-specific health concerns – but the demographic fit with Snapchat is strong. Younger pet-owning cohorts are over-indexed on the platform, and the quote action carries a similar low-friction profile to renter’s insurance. The vertical’s broader CPA dynamics, documented in the 2025 vertical CPA benchmarks, allow comfortable bid posture in the $40 to $90 CPL range for first-year-policy economics that frequently support those numbers. The trough adds a 15-to-25 percent improvement in achievable CPL on a vertical where margin already exists, which is the cleanest kind of arbitrage.

Fintech checking and supplemental health: structurally favored with caveats

Fintech checking-account acquisition and supplemental health products (accident, hospital indemnity, dental, vision) both fit the demographic and the trigger profile. The caveats on these verticals are regulatory rather than economic. Fintech faces persistent ad-account-policy review from Snap’s safety and integrity teams, particularly on copy that makes credit-related claims; supplemental health faces TCPA-adjacent disclosure requirements that interact with Snap’s ad-policy review. Operators in these verticals will benefit from the trough but need to plan around longer policy-review cycles than the cleaner insurance verticals will face.

The structurally challenged case: high-friction B2B

B2B lead generation aimed at decision-makers – particularly in software, professional services, or enterprise procurement categories – does not benefit from the Snap trough. The demographic mismatch is structural. The 18-to-34 user base on Snapchat concentrates in roles that are not procurement decision-makers for most B2B software categories, and the friction profile of B2B lead capture (longer forms, higher disqualification rates, longer sales cycles) does not compose well with Snapchat’s snackable creative format. Operators tempted to test Snap as a B2B channel during the trough will spend budget that does not return.

The pattern across the favored verticals: low-friction quote action, clear consumer trigger, demographic fit, unit economics that allow a CPL band that absorbs auction variance. The pattern in the challenged case: any one of those four conditions absent is usually disqualifying.

Auction Volatility: How to Enter the Trough Without Eating the Variance

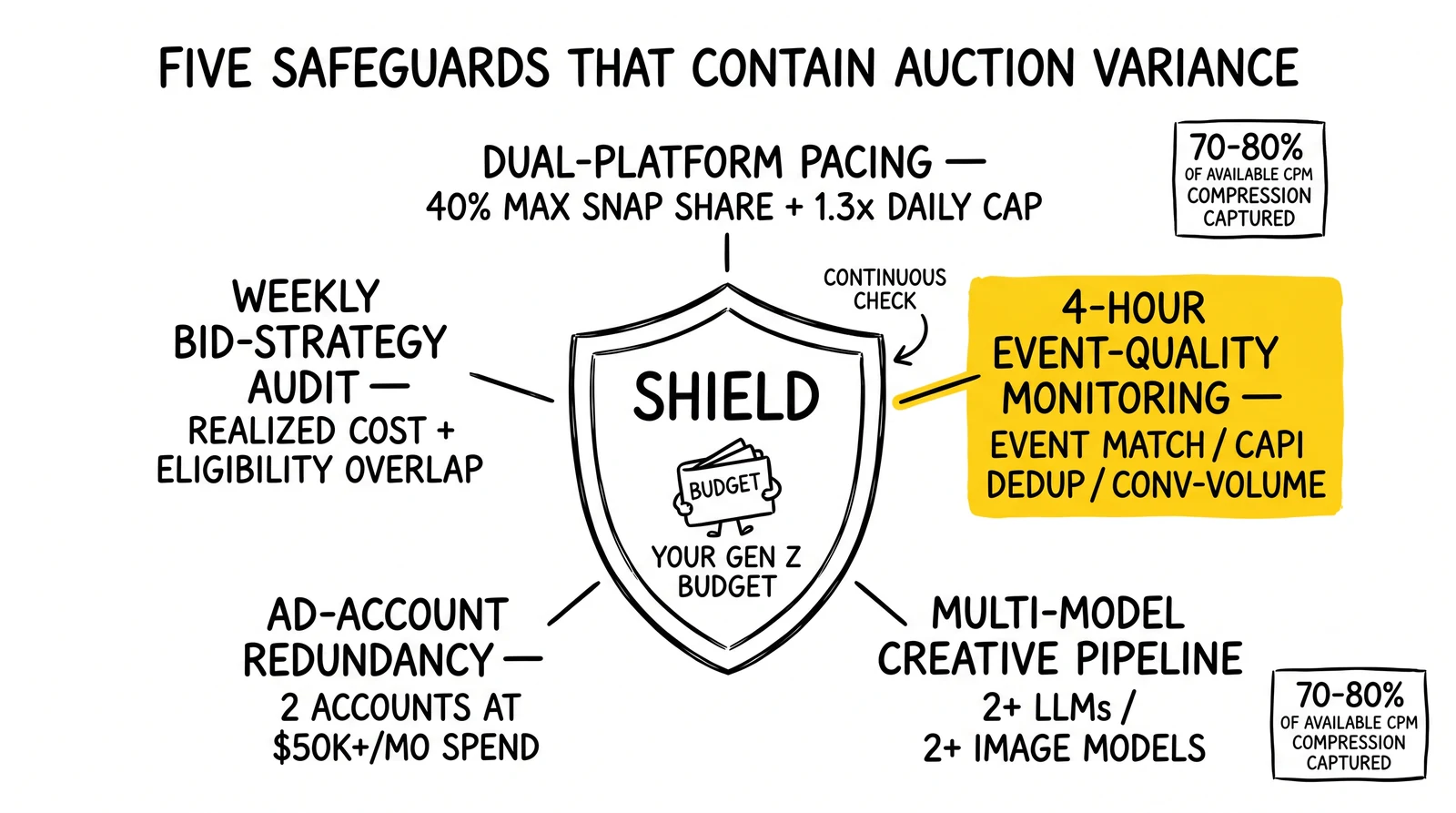

The trough is an opportunity. The variance from the AI-code-share disclosure is a risk that can erase the opportunity if it is not contained. Operators who enter the trough need a small set of operational safeguards that have specific defensive value against the kinds of auction drift that AI-code-driven instability tends to produce.

Safeguard one: dual-platform pacing, with hard daily caps

The first safeguard is to never run a Snap-trough campaign with budget concentration above forty percent of the vertical’s total daily spend. The reasoning is mechanical. If Snap’s pacing logic drifts in a way that front-loads the day’s budget – a common failure mode when bidding code paths get partially refactored – a campaign with sixty percent of daily budget on Snap will burn through its daily allocation in a window when conversion-volume systems may not have finished reporting back. By the time the operator notices, half a day of budget has cleared at distorted economics. A forty-percent ceiling on Snap with the rest of the budget on a pacing-stable channel – Meta, TikTok, or programmatic – limits the worst-case daily damage to a recoverable level.

Hard daily caps at the campaign level are a complement to the platform-share ceiling. Snap’s ad manager allows daily-spend caps that are enforced server-side. Operators frequently leave these set at default values that scale with the campaign budget; the trough strategy is to set them to roughly 1.3 times the planned daily spend, which contains overspend events from auction-drift failure modes without throttling normal pacing.

Safeguard two: event-quality monitoring on a 4-hour cycle

The second safeguard addresses attribution and event-quality drift. Snap’s conversion-event reporting passes through pixel and CAPI ingestion paths whose deduplication and matching logic is exactly the kind of code most likely to be modified in a high-AI-code-share environment. Operators who check event-quality metrics on a daily or weekly cadence will miss drifts that have already moved their CPL math by the time the metric is reviewed.

The defensive cadence is a 4-hour cycle on three metrics: event match quality (Snap’s own quality score for each conversion event, exposed in the events manager), CAPI deduplication rate (the percentage of pixel events that match a CAPI counterpart), and conversion-volume stability (the rolling 24-hour count of reported conversions versus the rolling 7-day average). Any of these three metrics moving by more than fifteen percent against the prior 24-hour baseline is a flag worth investigating before continuing to scale.

Safeguard three: creative pacing across multiple AI generators

The third safeguard is the creative-pipeline correlate of the AI-code disclosure. If the platform’s auction is now interacting with creative artifacts whose production pipeline is increasingly AI-mediated, an operator who runs creative produced by a single AI model – single LLM for copy, single diffusion model for image, single voiceover provider for audio – is concentrating creative-style risk in a way that did not matter as much when the auction’s own code base was human-engineered.

The defensive move is to ensure the creative pool active at any one time draws from at least two AI-copy sources (e.g., Claude and GPT) and at least two image-generation pipelines, and that creative tests rotate through these in a structured way rather than concentrating on whichever combination performed best in the most recent week. The reasoning is that auction-side drift can move the relative performance of different creative styles in ways that are hard to predict, and the operator who has trained the platform’s relevance models on a single creative style is more exposed to that drift than the operator whose models have been trained on a mixed pool. The structural framing for this is the dynamic creative optimization approach applied with explicit AI-pipeline diversity as one of the rotation dimensions.

Safeguard four: ad-account redundancy

The fourth safeguard is unglamorous but important. The April 15 reorganization affects, among other things, the engineering teams responsible for ad-policy enforcement and ad-account integrity systems. Operators who run a single ad account on Snap during a period of organizational change are exposed to enforcement-side drift in ways that can produce account-level disruptions that take days or weeks to resolve. The defensive posture is to maintain at least two active ad accounts on Snap for any vertical where the operator’s monthly Snap spend exceeds $50,000, with active campaigns running on both at all times. The cost is operational complexity. The benefit is that an enforcement event on one account does not stop spend velocity for the duration of the appeals process. The structural ad-account-bans prevention and recovery framework applies directly to this safeguard.

Safeguard five: weekly bid-strategy audit

The fifth safeguard is the weekly bid-strategy audit. Snap’s auto-bidding products – Goal-Based Bidding in particular – are the surface most likely to interact with AI-code-driven changes to the underlying ranking model, because they compress multiple platform decisions (eligibility, pacing, creative selection) into a single bidder-side abstraction. Operators relying on auto-bidding without auditing the realized bid distributions weekly will miss drifts in the underlying behavior that are visible in the data but invisible in the campaign-level summary.

The audit cadence is once weekly, on a fixed day, looking at the realized cost per result distribution against the target, the percentage of impressions clearing at or below the target bid, and the eligibility-overlap rate (what percentage of the targeted audience the platform actually reached). Drifts in these metrics correlate with auction-stack changes more reliably than headline CPL or CPC, and the lead time between an auction-stack change and a CPL change is typically two-to-four weeks, so the audit gives the operator enough warning to reposition.

The five safeguards together do not eliminate variance. They contain it. The expected outcome is that an operator running the trough strategy with these safeguards captures roughly seventy to eighty percent of the available CPM compression while limiting downside drift events to manageable two-to-three-day disruptions. The operator running the trough strategy without the safeguards will capture some of the upside but will lose some of it back in drift events that compound across attribution, pacing, and creative-relevance dimensions.

The AI Creative Pipeline: Why Anthropic Versus OpenAI Now Matters at the Buyer Layer

The Anthropic-overtakes-OpenAI shift at the enterprise LLM layer is not a Snap-specific story. It is a general-marketing-tech story whose specific application to Snapchat advertising is sharper than usual because of the publisher-side AI-code disclosure.

The shift, in numbers

Per Menlo Ventures’ 2025 enterprise AI survey, Anthropic’s enterprise LLM API spend share rose to forty percent from twelve percent in 2023. OpenAI’s share fell to twenty-seven percent from fifty percent. The reversal happened over roughly eighteen months and tracks closely with Anthropic’s improved coding-task performance and the maturation of its enterprise sales motion. OpenAI’s countervailing move – the ChatGPT Ads pilot that crossed $100 million ARR within six weeks of its January 16, 2026 launch and is now expanded to logged-out users – is a revenue story rather than an enterprise-API-share recovery story.

For an SDR or media buyer producing creative for Snapchat campaigns, the practical question is which model writes the copy and prompts the image generation, and how that decision interacts with platform performance. The answer is more nuanced than a model-leaderboard comparison.

The structural priors of each model

Claude (Anthropic) tends to produce copy that is structurally tighter, with denser specificity, fewer adverbial qualifiers, and a stronger preference for concrete claims over abstract benefit framing. The image-prompt outputs tend to be more descriptive and less formulaic. The hook density per character is generally higher, which matters in Snapchat’s swipeable ad format where the first 1.2 seconds of attention determine engagement.

GPT (OpenAI) tends to produce copy with broader range, more emotional register variation, and stronger performance on specific creative formats that have well-documented training-data patterns (testimonials, before-after structures, listicle-style ads). Image-prompt outputs are formulaic in a way that is sometimes a feature (consistent brand-style production) and sometimes a constraint (lower differentiation against the visual baseline).

Neither is uniformly better for Snapchat creative. The question is which performs better against a specific vertical’s customer cohort and a specific creative concept’s test design. The empirical answer requires testing, and the testing infrastructure is the second-order question.

The pipeline question

The structurally important point is that operators producing Snapchat creative through an AI pipeline at all – versus operators still producing creative through human-only or human-plus-template workflows – are operating with a creative-iteration rate that is roughly five-to-ten times higher per dollar of creative-production budget. The trough strategy works best when the operator can field a wide creative pool against the compressed-CPM window, because the pool’s variance gives the platform’s relevance models enough surface area to find the best-performing combinations within the trough’s time horizon.

The operator who concentrates creative production on a single AI model has the iteration rate but lacks the style variance. The operator who runs a multi-model pipeline – at least two LLMs and at least two image generators feeding a structured creative-test framework – has both. The Anthropic-versus-OpenAI choice is a tactical decision within that pipeline, not a strategic decision that determines whether the pipeline exists.

The decision interacts with another emerging variable, which is that the publisher’s own code is increasingly AI-mediated. If sixty-five percent of Snap’s new code is AI-written, the relevance and ranking models that serve creative are themselves shaped by AI tooling. Creative produced by aligned-style AI tooling tends to be ingested more cleanly than creative produced through orthogonal pipelines. This is not a determinative effect – human-written copy still performs strongly on many tests – but it is a margin effect that compounds over the trough’s two-quarter window.

Implementation Reality: What It Actually Takes to Capture the Trough

The strategic reframe is straightforward. The implementation is the part most operators will underestimate.

Resource requirements

Capturing the Q2-Q3 2026 Snap trough requires three resource investments most performance teams have not budgeted for. The first is platform engineering capacity to maintain the dual-platform pacing and event-quality monitoring described above. For most lead-gen operators, this is fifteen to thirty engineering days to build the monitoring dashboard, integrate Snap’s events-manager API with the operator’s existing reporting infrastructure, and configure the alert thresholds. Operators on a shared marketing-analytics stack will need a slightly larger build because the monitoring needs Snap-specific granularity.

The second is creative-production capacity at the multi-model pipeline level. An operator who currently runs creative through a single LLM and a single image generator needs to onboard at least one alternate provider in each category and structure a rotation framework. This is a four-to-six-week build with the bulk of the time going to brand-voice calibration on the second LLM and prompt-library extension on the second image model. Operators who underinvest here will find that their second-model creative performs systematically worse than their first-model creative, which is usually a calibration problem rather than a capability problem.

The third is media-buying-team capacity at the audit cadence. The five safeguards together require roughly four-to-eight hours per week per active vertical of senior-media-buyer attention. For an operator running three-to-five active verticals on Snap during the trough, this is one full-time-equivalent of senior-media-buyer time, or its outsourced equivalent. Operators who try to absorb this within existing media-buying capacity will find that the safeguards become formalities rather than functional checks, which defeats the purpose.

Timeline expectations

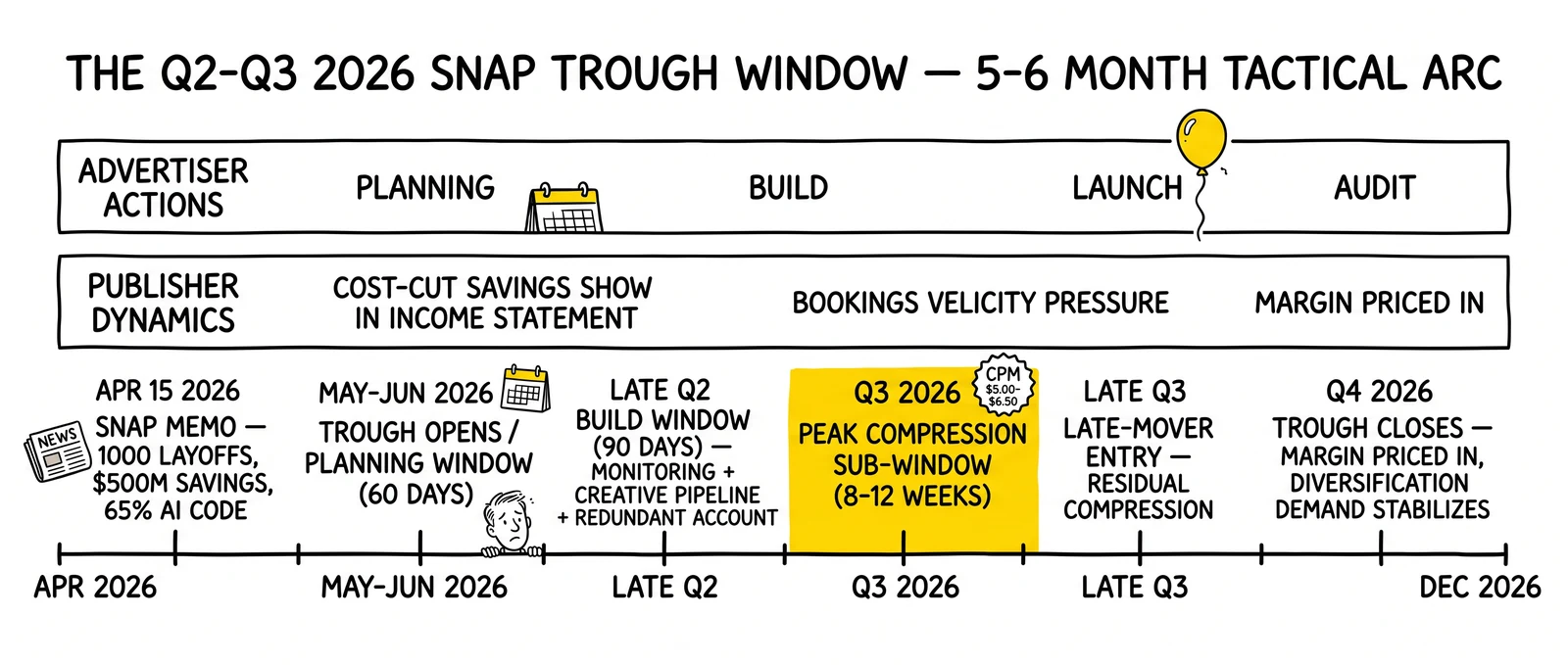

A realistic capture timeline for a mid-sized lead generation operator:

| Phase | Duration | Key Activities |

|---|---|---|

| Vertical selection and bid-band sizing | 7-14 days | Identify two-to-three favored verticals; size CPL bands; project trough-case unit economics |

| Monitoring infrastructure build | 15-30 days | Events-manager API integration; pacing dashboard; alert threshold configuration |

| Creative pipeline diversification | 28-42 days | Onboard second LLM; calibrate brand voice; extend prompt library; build rotation framework |

| Account redundancy setup | 7-14 days | Establish secondary ad account; pre-warm with low-spend campaigns; document escalation paths |

| Trough campaign launch | 14-21 days | Phase budget allocation; launch initial verticals; install five safeguards |

| Iteration and scale | Ongoing through Q3 2026 | Weekly audits; monthly creative-pipeline review; vertical expansion based on performance |

| Total elapsed time | 8-12 weeks | Conservative estimate for an operator without prior Snap-specific infrastructure |

Source: Composite of operator implementation patterns and platform-specific build requirements

The eight-to-twelve-week build is most of why the trough is a tactical window rather than a strategic shift. By the time an operator who started planning in early May is fully operational, the window will be in its later half. Operators who wait until the trough is visible in industry CPM data before starting the build will miss most of the available compression.

Common obstacles

Three obstacles consistently slow these builds. The first is creative-team resistance to multi-model pipelines. Creative teams that have invested in a primary LLM workflow tend to view alternate-model adoption as a capability question rather than a portfolio question. The framing that breaks through is to position the second model as risk diversification rather than capability comparison. The framing that fails is to position it as a head-to-head model evaluation, which produces a winner-takes-all decision that defeats the diversification purpose.

The second obstacle is finance-team friction on the redundant ad account. Maintaining two active ad accounts on Snap with low-utilization secondary spend reads, on a budget review, as inefficient. The framing that breaks through is to size the secondary account’s spend as insurance – typically two-to-five percent of the primary account’s spend – and to communicate the maximum-disruption scenario the redundancy protects against. The framing that fails is to bury the secondary account in the primary budget line, which guarantees it will be cut in the next budget cycle.

The third obstacle is the analytics-team load on the four-hour event-quality monitoring. The cadence is genuinely demanding for operators whose analytics teams are already at capacity. The framing that breaks through is to automate as much of the monitoring as possible and to escalate only on threshold violations rather than producing daily summary reports. The cadence question is not about the data; it is about the response time, and the analytics team’s load can be sized to the response-time requirement rather than the data-collection volume.

The implementation is non-trivial. The operators who complete it before the second half of Q2 2026 will run a five-to-six-month margin-capture window. The operators who do not will spend the trough watching their CPLs marginally improve and assuming that is the full available improvement, while the operators who built will be running CPLs ten-to-twenty percent below the partial-implementation operator’s CPL on the same inventory.

Future Implications: How the Snap Reset Reshapes Lead Generation Through 2027

The Snap announcement is one event in a sequence whose shape is already visible. Three trajectories matter.

Trajectory one: AI-code-share disclosures spread across the ad-platform stack

Snap is unlikely to be the only ad platform disclosing high AI-code shares. Meta, TikTok, X, Reddit, and Pinterest all run engineering organizations that are subject to the same productivity dynamics that Spiegel cited in the April 15 memo. Some of those platforms will make similar disclosures in 2026 earnings cycles. Others will execute the underlying shift without disclosing it explicitly. Either way, the auction-volatility and creative-pipeline-alignment considerations described in this article are platform-general rather than Snap-specific within an 18-month window.

The operator who builds the multi-model creative pipeline and the four-hour event-quality monitoring infrastructure for the Snap trough will find that the same infrastructure applies to whichever platform makes the next disclosure. The investment is platform-general even if the immediate trigger is platform-specific.

Trajectory two: enterprise LLM share concentrates further

The Anthropic-versus-OpenAI dynamic at the enterprise layer is unlikely to stabilize at the current 40-versus-27 split. Either Anthropic’s lead extends further as enterprise procurement standardizes on the lower-cost-per-quality leader, or OpenAI’s ads-revenue trajectory funds a sustained enterprise-API counter-investment that brings the share back. The resolution will likely be visible by Q4 2026 in the form of either pricing changes or enterprise-product-feature releases.

For lead generation operators, the implication is that the multi-model creative pipeline’s specific composition will need to be reviewed quarterly through 2026. The pipeline architecture is durable; the specific provider choices within it are not. Operators who build the pipeline as a generalized routing system that can swap providers without re-architecting are positioned for the post-resolution market regardless of which way the resolution goes.

Trajectory three: the inventory-source question gets sharper

Snap’s reset is one signal in a broader pattern of ad platforms differentiating on cost structure. Meta has been investing heavily in its own AI-code transition. TikTok continues to operate under a U.S. regulatory overhang that creates persistent uncertainty about its long-run inventory availability. ChatGPT Ads – which crossed $100 million ARR in six weeks per CNBC’s reporting and is now serving ads to logged-out users – represents a genuinely new inventory source whose performance characteristics are still being established. Programmatic display continues to absorb cookie-deprecation pressure. Connected TV continues to fragment.

The pattern is that the inventory-allocation question across paid channels is becoming more variable rather than less, and operators with rigid budget-allocation frameworks will systematically underperform operators with flexible allocation frameworks. The Snap trough is one instance of this broader pattern. There will be others – a Meta-specific window, a TikTok regulatory-resolution window, a ChatGPT Ads inventory-expansion window – within the next eighteen months. The operators who treat the Snap trough as a one-off arbitrage will miss the pattern. The operators who treat it as an instance of the broader inventory-volatility regime will build the operating capacity that captures each successive window.

Trajectory four: lead-quality dynamics and click-fraud surface

The fourth trajectory is the one that most operators will overlook. AI-code-driven changes to ad-platform infrastructure have historically correlated with click-fraud and bot-traffic dynamics that take six-to-twelve months to fully express in lead-quality metrics. The reasoning is that fraud detection, like ranking and pacing, sits in code paths that are AI-modified at high rates, and adversarial actors adapt to the code changes faster than the platform’s countermeasures stabilize.

Operators capturing the Snap trough need to maintain click-fraud detection and prevention infrastructure at higher sensitivity than baseline through Q3 2026, with explicit attention to the lead-quality patterns – match rates against carrier underwriting, contact rates by call center, dispute rates from buyers – that are the leading indicators of platform-side fraud-detection drift. Operators who skip this step risk capturing the CPM trough with leads whose downstream conversion economics have degraded enough to wipe out the CPM savings.

Key Takeaways

The April 15, 2026 Snap announcement is a two-sided event. The cost-base collapse – a $500 million-plus annualized savings target by H2 2026 against a sustained-or-growing revenue pool – points to a structurally wider CPM corridor on Snapchat through Q2-Q3 2026, with the most pronounced compression in low-friction Gen Z verticals: renter’s insurance, pet insurance, fintech checking, and supplemental health.

The 65 percent AI-code-share disclosure points to auction-side variance that operators need to plan against. Eligibility logic, pacing logic, and event-quality scoring are the three areas most likely to drift in a high-AI-code-share environment, and the variance compounds across them in ways that can move CPL by an order of magnitude over short windows if not contained.

Three verticals are structurally favored for the trough strategy: renter’s insurance, pet insurance, and fintech checking-account acquisition. Supplemental health is a fourth with regulatory caveats. B2B lead generation is structurally challenged regardless of the trough.

Five safeguards together contain the variance: dual-platform pacing with a 40 percent ceiling on Snap share of vertical spend, hard daily caps at 1.3x planned daily spend, four-hour event-quality monitoring on event-match-quality, CAPI deduplication, and conversion-volume stability metrics, multi-model creative pipelines with at least two LLMs and two image generators, and ad-account redundancy at $50,000 monthly Snap spend or above.

The Anthropic-overtakes-OpenAI shift at the enterprise LLM layer – Anthropic at roughly 40 percent enterprise API share versus OpenAI at 27 percent per Menlo Ventures – matters at the buyer-side creative pipeline because the same structural priors that shape a model’s output also interact with the relevance models on AI-coded ad platforms. The pipeline architecture is durable; the specific provider mix should be reviewed quarterly through 2026.

The implementation timeline is 8-to-12 weeks for an operator without prior Snap-specific infrastructure. Operators who wait until trough CPMs are visible in industry data before starting the build will miss most of the available compression. The window opens in Q2 2026, peaks somewhere in Q3 2026, and closes as Snap’s margin expansion is fully priced in and diversification-driven demand stabilizes against the new inventory equilibrium.

The Snap reset is not a one-off arbitrage. It is the first visible instance of a broader inventory-volatility regime in which AI-code-share disclosures, enterprise LLM share shifts, regulatory dynamics, and inventory-source fragmentation produce a sequence of platform-specific tactical windows over the next 18 months. Operators who build flexible inventory-allocation, creative-pipeline, and monitoring infrastructure for the Snap trough are building the operating capacity that captures each successive window.

For operators currently concentrating Gen Z budget on Meta and TikTok, the next sixty days are the planning window. The next ninety days are the build window. The first wave of operators capturing the trough will start posting visibly different CPL numbers somewhere in mid-to-late Q2 2026; by Q3, the late-mover cohort will be competing for what is left.

Frequently Asked Questions

What did Snap actually announce on April 15, 2026?

Snap CEO Evan Spiegel announced a workforce reduction of approximately 1,000 employees, or sixteen percent of global headcount, with at least 300 open positions also closed. The company communicated a more than $500 million reduction in annualized cost base by the second half of 2026, with U.S. employees receiving four months of severance, healthcare coverage, equity vesting, and transition support. The memo also disclosed that AI now writes more than 65 percent of new code at Snap and that smaller teams paired with AI tools have driven recent product progress on Snapchat+, the ad platform, and infrastructure. Snap shares jumped about seven percent on the announcement.

Why does the 65 percent AI-code-share disclosure matter more than the layoff count for advertisers?

The layoff count is a one-time margin event. The AI-code-share disclosure describes a structural change in how the platform’s auction, ranking, eligibility, pacing, and event-quality systems are maintained going forward. An auction stack maintained by a smaller engineering organization on a code base where two-thirds of new commits originate from AI tools is more variable than the same stack maintained by a stable, larger human-engineering footprint. The variance shows up in eligibility logic, pacing behavior, and attribution scoring – three areas that directly affect CPL on the buyer side. Operators who plan against the cost-base collapse without planning against the variance capture some of the upside but lose some of it back to drift events.

How big is the Q2-Q3 2026 CPM trough on Snapchat likely to be?

Industry CPM commentary published earlier in 2026 estimated Snapchat’s average CPM in the $8.39 to $8.85 range. The trough is unlikely to compress that figure uniformly across verticals; the compression will be concentrated in low-friction Gen Z verticals where Snap is most motivated to demonstrate bookings velocity. A plausible scenario range is clearing CPMs in the $5 to $6.50 band on tightly targeted Gen Z campaigns through Q3 2026, with the higher-friction or lower-demographic-fit segments seeing more modest one-to-three dollar reductions. The trough is real but is not uniform; vertical-level modeling matters more than platform-level modeling.

Which lead generation verticals benefit most from the trough?

Renter’s insurance, pet insurance, fintech checking-account acquisition, and supplemental health products (accident, hospital indemnity, dental, vision) are structurally favored. The pattern is low-friction quote action plus clear consumer trigger plus demographic fit plus unit economics that allow a CPL band wide enough to absorb auction variance. Renter’s insurance is the cleanest fit because the move-in trigger frequency on Snapchat’s user base is over-indexed and the policy’s annual premium supports a CPL range from approximately $25 to $60 with carrier-margin tolerance. Pet insurance carries a similar profile with a different trigger structure. B2B lead generation does not benefit because the demographic mismatch is structural.

How does the Anthropic-overtakes-OpenAI shift affect the buyer-side creative pipeline?

Per Menlo Ventures’ 2025 enterprise AI survey, Anthropic now commands roughly forty percent of enterprise LLM API spend, up from twelve percent in 2023, while OpenAI has fallen to twenty-seven percent from fifty percent. The shift matters for Snap advertisers because the model that writes the creative interacts with the relevance and ranking models on the publisher side, and those models are themselves increasingly AI-coded. Creative produced through aligned-style AI tooling tends to be ingested more cleanly than creative produced through orthogonal pipelines. The practical implication is that operators should run multi-model creative pipelines – at least two LLMs and at least two image generators feeding a structured creative-test framework – rather than concentrating creative production on a single model.

What concrete safeguards should operators install before entering the trough?

Five safeguards work together: a 40 percent ceiling on Snap’s share of any vertical’s daily spend so that pacing drift on Snap cannot eat more than a recoverable share of daily budget; hard daily caps set at approximately 1.3 times planned daily spend at the campaign level; four-hour event-quality monitoring on event-match-quality, CAPI deduplication rate, and rolling-24-hour conversion-volume stability against the 7-day average; multi-model creative pipelines with structured rotation rather than concentration on the highest-recent-performer combination; and ad-account redundancy at any vertical with monthly Snap spend above $50,000. None of these eliminates variance; together they contain it to roughly two-to-three-day disruptions rather than week-long degradations.

How does the American Express acquisition of Hyper relate to Snap advertisers?

The April 16, 2026 announcement that American Express would acquire Hyper, a Sam Altman-backed AI expense-management startup founded in 2022, is part of a broader pattern of enterprise budgets being captured at the strategic-acquisition layer for AI tooling. The deal is expected to close in Q2 2026. For Snap advertisers, the relevance is indirect but real. AmEx-Hyper is a signal that AI-mediated workflow tooling is being absorbed into the largest enterprise platforms at a pace that will affect how ad-buying teams source, evaluate, and deploy AI capabilities over the next 12-24 months. Operators who treat AI tooling as a portfolio of independently-procured point solutions will increasingly find themselves competing against operators using integrated stacks where the AI capabilities are bundled into the underlying enterprise platform.

What does the Q1 2026 venture funding data signal about ad-platform competition?

Per Crunchbase, Q1 2026 global venture funding hit $300 billion with AI absorbing $242 billion – over eighty percent of the quarterly total. Four of the five largest venture rounds ever closed in Q1 2026, with OpenAI ($122 billion), Anthropic ($30 billion), xAI ($20 billion), and Waymo ($16 billion) accounting for roughly sixty-five percent of the quarter’s total. The signal for ad-platform competition is that the AI infrastructure layer is being capitalized at a scale that compresses every downstream platform’s cost-of-capabilities. Snap’s ability to remove $500 million in annualized cost while accelerating product velocity is one expression of that compression. Other platforms will execute similar compressions on different timelines, which is part of why the inventory-volatility regime is broader than the Snap-specific story.

Is ChatGPT Ads a real alternative inventory source for lead generation?

ChatGPT Ads crossed $100 million ARR within six weeks of its January 16, 2026 pilot launch per CNBC, and the inventory has expanded to logged-out users. Roughly eighty-five percent of OpenAI’s free and Go users in the U.S. are eligible to see ads, but less than twenty percent are shown them on a daily basis, which means the inventory is supply-constrained even as demand has scaled rapidly. For lead generation operators, ChatGPT Ads is a real alternative inventory source for verticals where conversational discovery aligns with the consumer journey – high-consideration purchases, research-heavy verticals, B2B SaaS – but it is not a direct substitute for the demographic targeting precision that Snapchat offers on Gen Z verticals. Operators should treat the two as complementary rather than substitutable through 2026.

How long will the Snap trough last?

The trough opens in Q2 2026 as the cost-cut savings begin showing in the income statement and Snap is most motivated to demonstrate bookings velocity to support the margin narrative. It peaks somewhere in Q3 2026 when the savings are fully visible and diversification-driven demand from advertisers leaving Meta and TikTok is still ramping. It closes as the margin expansion is fully priced into the stock and diversification-driven demand stabilizes against the new inventory equilibrium. The realistic window is roughly five-to-six months from open to close, with the highest-compression sub-window being eight-to-twelve weeks in mid-Q3 2026. Operators who plan for a two-quarter capture window with phased budget allocation rather than front-loading will extract more total margin than operators who concentrate capture in the peak weeks.

What about Snap-specific click fraud and lead-quality risk during the trough?

Click fraud and bot-traffic dynamics historically correlate with AI-code-driven changes to ad-platform infrastructure on a six-to-twelve-month lag, because fraud-detection code paths are AI-modified at high rates and adversarial actors adapt faster than countermeasures stabilize. Operators capturing the Snap trough should maintain click-fraud detection and prevention infrastructure at higher sensitivity than baseline through Q3 2026, with explicit attention to lead-quality leading indicators: match rates against carrier underwriting, contact rates by call center, and dispute rates from buyers. A three-to-five-percent degradation in lead quality can erase the entire CPM savings on a vertical with tight unit economics, so the lead-quality monitoring is not optional alongside the CPM-capture strategy.

What does the implementation timeline look like for an operator without prior Snap infrastructure?

A realistic build timeline is 8-to-12 weeks broken into five parallel work streams. Vertical selection and bid-band sizing takes 7-14 days. Monitoring infrastructure build (events-manager API integration, pacing dashboard, alert thresholds) takes 15-30 days. Creative pipeline diversification (onboarding a second LLM, calibrating brand voice, extending the prompt library) takes 28-42 days. Account redundancy setup takes 7-14 days including pre-warming the secondary account with low-spend campaigns. Trough campaign launch with the five safeguards installed takes 14-21 days. The eight-to-twelve-week build is most of why the trough is a tactical window rather than a strategic shift. Operators who wait until trough CPMs are visible in industry CPM data before starting the build will be operational only in the trough’s later half, which is when the late-mover cohort begins competing for the residual compression.

Sources

Tier 1: Primary Company and Platform Sources

-

Snap Inc. Newsroom, “Organizational Changes at Snap,” Snap Newsroom, April 15, 2026 – https://newsroom.snap.com/organizational-changes-at-snap

-

Snapchat for Business, “The New Era of Insurance Buying on Snapchat,” Snapchat for Business Blog, accessed April 28, 2026 – https://forbusiness.snapchat.com/blog/swipe-up-for-coverage

-

Snapchat for Business, “Reach Gen Z and Millennials,” Snapchat for Business, accessed April 28, 2026 – https://forbusiness.snapchat.com/

Tier 2: Established Industry Research and Trade Press

-

CNBC, “Snap’s stock jumps on plans to axe 16% of its workforce citing AI efficiencies,” April 15, 2026 – https://www.cnbc.com/2026/04/15/snap-stock-layoffs-16-percent-workforce.html

-

TechCrunch, “Snap is cutting 1000 jobs, 16% of its workforce,” April 15, 2026 – https://techcrunch.com/2026/04/15/snap-is-cutting-1000-jobs-16-of-its-workforce/

-

Variety, “Snap Axing 1,000 Staffers, 16% of Headcount; CEO Evan Spiegel Cites AI as Helping Boost Efficiency for Smaller Teams,” April 15, 2026 – https://variety.com/2026/digital/news/snap-layoffs-snapchat-ceo-evan-spiegel-cites-ai-1236722228/

-

Deadline, “Snap Cutting 16% Of Full-Time Workforce; CEO Evan Spiegel Says AI Offers ‘New Way Of Working’,” April 15, 2026 – https://deadline.com/2026/04/snap-layoffs-ceo-evan-spiegel-ai-1236861335/

-

The Hollywood Reporter, “Layoffs Hit Snapchat Owner Snap as 1,000 Jobs Slashed,” April 15, 2026 – https://www.hollywoodreporter.com/business/business-news/snapchat-layoffs-100-jobs-ai-deployment-1236565059/

-

Fox Business, “Snapchat parent company cuts 1000 jobs in major AI-driven workforce restructuring,” April 2026 – https://www.foxbusiness.com/markets/snapchat-parent-company-cuts-1000-jobs-major-ai-driven-workforce-restructuring

-

TechRepublic, “Tech Layoffs Continue: Snap Cuts 1,000 Jobs, Citing ‘Rapid Advancements’ in AI,” April 2026 – https://www.techrepublic.com/article/news-snap-ai-layoffs-april-2026/

-

CNBC, “OpenAI ads pilot tops $100 million in ARR in under 2 months,” March 26, 2026 – https://www.cnbc.com/2026/03/26/openai-ads-pilot-tops-100-million-in-arr-in-under-2-months.html

-

Crunchbase News, “Q1 2026 Shatters Venture Funding Records As AI Boom Pushes Startup Investment To $300B,” April 2026 – https://news.crunchbase.com/venture/record-breaking-funding-ai-global-q1-2026/

-

Quartz, “American Express acquiring AI expense startup Hyper,” April 16, 2026 – https://qz.com/american-express-acquiring-hyper-ai-expense-startup-041626

-

Search Engine Land, “ChatGPT ads expand to logged-out users,” April 2026 – https://searchengineland.com/chatgpt-ads-expand-to-logged-out-users-475377

-

AdExchanger, “ChatGPT Ads Have Begun Showing Up For Logged-Out Users,” April 2026 – https://www.adexchanger.com/ai/chatgpt-ads-have-begun-showing-up-for-logged-out-users/

-

Yahoo Finance, “AI Startups Capture $242B As Global Funding Hits $300B In Q1 2026,” April 2026 – https://finance.yahoo.com/sectors/technology/articles/ai-startups-capture-242b-global-174530064.html

Tier 3: Industry and Vendor Statements

-

Menlo Ventures, “2025: The State of Generative AI in the Enterprise,” Menlo Ventures Research, 2026 – https://menlovc.com/2025-the-state-of-generative-ai-in-the-enterprise/

-

SmartyAds, “Social Media Ads Cost in 2025: Trends, CPM Benchmarks & Programmatic Alternatives,” 2026 – https://smartyads.com/blog/social-media-ads-cost

-

LeadsBridge, “How much do Snapchat ads cost?,” accessed April 28, 2026 – https://leadsbridge.com/blog/snapchat-ads-cost/

-

Social Champ, “Snapchat Statistics 2026: Key Data For Marketers,” 2026 – https://www.socialchamp.com/blog/snapchat-statistics/

-

The Social Shepherd, “25 Essential Snapchat Statistics You Need to Know in 2026,” 2026 – https://thesocialshepherd.com/blog/snapchat-statistics

-

Pulse Advertising, “Snapchat: The platform resurgence as AR and AI bets shape 2026,” 2026 – https://www.pulse-advertising.com/resources/social-media-news/snapchat-growth-2025-ar-strategy-2026-outlook/

Tier 4: Supporting Industry Commentary

-

Glass Almanac, “Snap Reveals 65% AI Code Use, $500M Savings And Specs Bet In 2026,” April 2026 – https://glassalmanac.com/snap-reveals-65-ai-code-use-500m-savings-and-specs-bet-in-2026-heres-why/

-

BigGo Finance, “Snap CEO Evan Spiegel: AI Wrote Two-Thirds of Our Code, and It’s a New Platform,” April 2026 – https://finance.biggo.com/news/d729fc3b211a3b85

-

Open The Magazine, “Snap Layoffs 2026: 1,000 Jobs Cut as AI Reshapes Snapchat Workforce, Costs and Profit Path,” April 2026 – https://openthemagazine.com/business/snap-shocks-tech-world-1000-jobs-cut-as-ai-takes-over-the-workforce

-

Quiver Quantitative, “American Express Acquires AI Startup Hyper Backed by OpenAI CEO Sam Altman,” April 16, 2026 – https://www.quiverquant.com/news/American+Express+Acquires+AI+Startup+Hyper+Backed+by+OpenAI+CEO+Sam+Altman

-

ExchangeWire, “Digest: ChatGPT Shows Ads to Logged-Out Users,” April 27, 2026 – https://www.exchangewire.com/blog/2026/04/27/digest-chatgpt-shows-ads-to-logged-out-users-norway-and-turkey-progress-with-plans-for-social-media-bans-meta-launches-instants-app/

Closing

The April 15, 2026 Snap announcement will be remembered, in most coverage, as a margin-expansion story – a sixteen-percent workforce cut, a $500 million annualized savings target, a seven-percent stock pop. That framing misses what actually happened for advertisers. The structural event was the disclosure that more than 65 percent of new code at the company is now AI-written, on top of an engineering footprint that just contracted by sixteen percent. The operational event was the opening of a CPM corridor on Gen Z-tilted lead generation verticals that will not stay open beyond Q3 2026. The lead generation operators who treat April 15 as a Snap-specific news cycle will spend the next two quarters on the same Meta-and-TikTok concentration that has been compressing their margins for eighteen months. The operators who treat it as the first instance of a broader inventory-volatility regime – and who build the multi-model creative pipelines, the four-hour event-quality monitoring, and the dual-platform pacing safeguards that the regime requires – will capture the trough on Snap, the next platform-specific window when it opens, and the one after that. The decision about which group to be in is being made now, in the next sixty days of planning and the next ninety days of build. The operators who arrive late will be competing for what is left.

Market data, platform announcements, and enterprise LLM share statistics reflect publicly reported conditions through April 28, 2026. Snapchat ad inventory pricing, ad-product configurations, and platform policies change continuously; verify current terms through Snap’s business-facing documentation before making operational decisions. This article provides general industry analysis and does not constitute legal, financial, or compliance advice. Consult qualified counsel for specific compliance questions related to consent disclosures, ad-platform policy interpretation, and click-fraud monitoring obligations.