Pew measured what most operators suspected – adoption is now mainstream, trust is stalled, and the gap is monetizable for funnels that lean into it rather than around it.

June 17, 2026 – When Pew Settled the Adoption Question

Pew Research Center published Americans and AI 2026 on June 17, 2026. The report – full title Americans’ Views on AI Chatbots, Smart Devices and AI’s Impact – drew on the American Trends Panel survey of 5,119 US adults fielded February 17 to 23. The margin of error is ±1.6 percentage points. Pew is the closest the US gets to a Tier 1 consumer-sentiment research source, and the June 17 publication date establishes the data as the most current authoritative measurement of US adult AI use available.

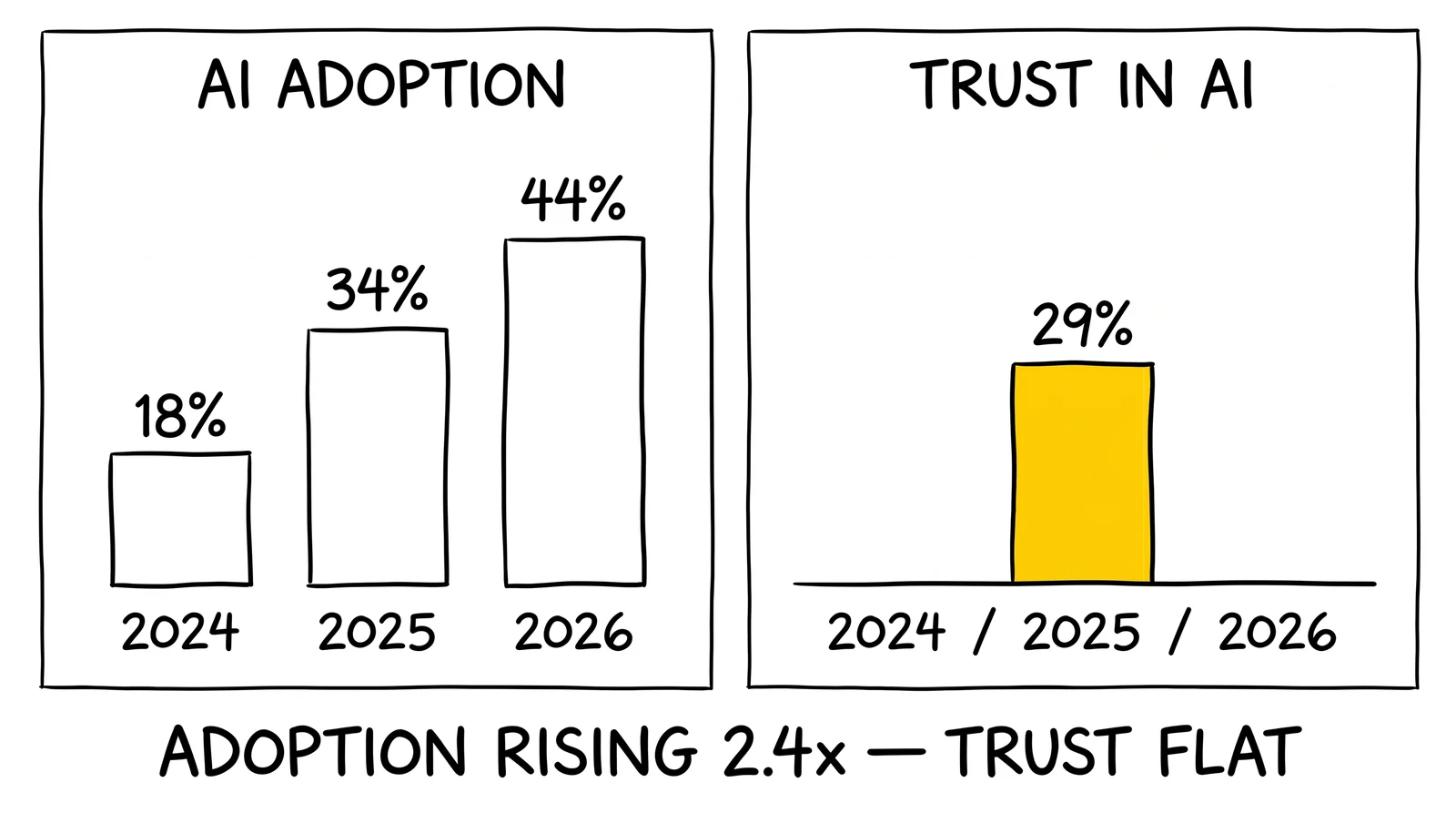

The headline numbers settle an adoption question that operators had been arguing with vendor-sponsored surveys for two years. Forty-four percent of US adults reported using ChatGPT – up from 18 percent in Pew’s 2023 measurement and 34 percent in the 2025 measurement. Forty-nine percent reported using AI chatbots more broadly. Sixty percent reported reading AI-generated summaries in search results. The adoption curve continues to compound rather than plateau.

The trust trajectory diverges sharply from the adoption trajectory. Only 29 percent of chatbot users say they have a lot or some trust in the information chatbots provide. The trust number has not meaningfully moved over the same window. The structural insight is that consumer AI use has moved from optional to mainstream while consumer trust in AI output has stalled at minority levels. Adoption is no longer a question; trust still is.

For lead-generation operators, the two trajectories combine into a translation problem. The discovery layer where buyers form initial vendor impressions is increasingly AI-mediated. The trust budget for the resulting AI output is bounded. Funnels that lean into AI without addressing trust under-deliver; funnels that close the trust loop quickly capture conversion premiums that the Adobe Q2 2026 data measures at 42 percent above non-AI baseline. The article works through what each cohort cut, vertical signal, and operator action means.

What Pew Actually Measured

The methodology bears specifics because the secondary coverage tends to round. The American Trends Panel is Pew’s nationally representative panel of US adults recruited through address-based sampling and maintained as an ongoing measurement instrument. The February 2026 wave covered 5,119 respondents, fielded February 17 to 23. The ±1.6 percentage-point margin applies at the full-sample level; cohort-level cuts carry larger error bands that Pew’s appendix tables document.

The adoption headline is the trajectory rather than the level. ChatGPT use among US adults grew from 18 percent in 2023 to 34 percent in 2025 to 44 percent in 2026. The June 2025 short-read on which the 34 percent figure was based is Pew’s prior reference point. The 2026 number reflects a 10-percentage-point absolute increase over the 12-month measurement gap, suggesting continued category expansion rather than late-adopter saturation. Broader chatbot use – including Microsoft Copilot, Google Gemini, Anthropic Claude, Meta AI, and Apple Intelligence alongside ChatGPT – reached 49 percent.

The intensity distribution among users matters as much as the headline adoption number. Twenty-four percent of chatbot users report daily use; 12 percent several times per day; 4 percent describe their use as almost constant. The use-case distribution shows 42 percent using chatbots for information search, 38 percent for work tasks, 20 percent for medical advice, and 20 percent for diet or fitness guidance. The medical and diet-or-fitness use cases are notable for lead-generation verticals – health insurance, weight-management programs, telehealth referrals, and supplements – because they indicate consumers are using chatbots inside high-trust-required decisions.

The AI-summary-reading number is the operator’s pre-funnel demand contraction data point. Sixty percent of US adults read AI-generated summaries in search results, which is the consumer-side mechanism behind the Forrester GTM Singularity pre-funnel demand contraction that operator-side traffic analytics have been documenting through 2025 and 2026. The buyer who reads the AI summary may not click through to the operator landing page; the operator’s analytics show traffic decline; the underlying behavior is the buyer learning the answer in the search surface.

The sentiment data lands hardest. Seventy-one percent of US adults believe AI advances will weaken personal data security. Only 16 percent expect a positive 20-year societal impact from AI. Sixty-three percent say AI is advancing too quickly for societal adjustment. These numbers move in the opposite direction from the adoption trajectory. Adoption is rising; sentiment is not.

The Age-Cohort Inversion

The demographic cuts produce the most operator-actionable signal. The 18-29 cohort uses chatbots at 66 percent and ChatGPT specifically at 61 percent. The 30-49 cohort uses chatbots at 61 percent and ChatGPT at 55 percent. The 50-64 cohort drops to 42 percent and 37 percent. The 65-plus cohort sits at 23 percent and 19 percent. The age-skew is steeper than most adopt-rate distributions.

The sentiment cut produces the inversion. The same 18-29 cohort that leads adoption also leads pessimism: 48 percent expect negative societal AI impact, the highest of any age group. The 65-plus cohort, with lowest adoption, also shows lowest predicted negative impact at the group level. The pattern is heaviest users seeing the costs most clearly while light users are less concerned.

The confidence-using-chatbots cut reinforces the pattern. Among 18-29 respondents, 31 percent describe themselves as extremely or very confident using chatbots. Among 65-plus, only 6 percent describe similar confidence. The cohort with highest skill is also the cohort with highest concern. Pew’s framing of this as a usage-with-eyes-open pattern is the analytical reframe – heavy use does not produce optimism; it produces sophisticated skepticism.

For lead-generation operators targeting the 18-29 cohort, the implication is that AI-novelty pitches under-perform. The cohort has already used the underlying tools and formed views about their limitations. Funnels that lead with transparency, control, and human-in-the-loop options will outperform funnels that lead with AI-mediated qualification or chatbot-only paths. Insurance shoppers in the 18-29 cohort, in particular, present the highest-value cohort for transparent funnel choreography because they combine high-intent search behavior with low patience for AI obfuscation.

The 30-49 cohort splits the difference on both adoption and sentiment, which makes it the broadest target for mixed-mode funnel designs. The 50-64 and 65-plus cohorts require traditional funnel mechanics for the foreseeable future – their AI adoption is rising but lags far behind the under-50 population, and any operator over-investing in AI-mediated mechanics for these cohorts will lose ground to operators running conventional landing pages with strong speed-to-callback.

The Trust Gap as Funnel Translation

The 29 percent chatbot trust number is the central data point for funnel design. It is not 0 percent – meaning AI is not categorically distrusted – but it is far below the 80-percent-and-up trust levels that funnels traditionally optimize against in branded consumer interactions. Operators designing funnels that route through AI layers should price the trust budget the AI layer consumes against the conversion benefit it produces.

The 71 percent expecting AI to weaken personal data security adds the compliance translation. Lead-generation funnels collecting first-party data – phone, email, address, financial information – face a buyer population that increasingly expects AI involvement and increasingly distrusts the data-handling implications. The funnel-design response is to over-invest in transparent data-handling disclosure rather than under-invest. Operators that lead with TrustedForm or Jornaya certificate display, explicit consent capture language, and visible privacy commitments will out-convert operators that quietly route data through unmarked AI layers.

Adobe’s Q2 2026 data provides the conversion-side measurement. AI-referred traffic to US retail sites grew 393 percent year-over-year in Q1 2026, and the resulting traffic converts 42 percent better than non-AI traffic on the same sites. The conversion premium reverses the prior year’s finding, when AI-referred traffic converted below baseline. The structural insight Adobe surfaced is that the AI layer is now acting as a qualification step – the buyer arrives pre-qualified by the chatbot interaction rather than as discovery traffic that needs to be qualified by the landing page.

The Pew and Adobe data combine to produce the operator translation. The AI-referred buyer arrives pre-qualified but skeptical of further AI mediation. The funnel-design implication is to close the qualification loop quickly through human-touch options rather than extending the AI layer further into the conversion path. Jump-to-callback placement, transparent data-handling, and explicit consent capture out-perform additional chatbot layers, automated questionnaires, or AI-mediated quote calculators in this population.

The compliance overlay matters. Post the Sixth Circuit’s January 26, 2026 ruling in Dahdah v. Rocket Mortgage, the form architecture itself is the load-bearing element of TCPA arbitration defense. The four-factor conspicuousness test – notice placement, button proximity, visual conspicuousness, dynamic scrolling – pairs naturally with the Pew sentiment data. Operators implementing the Dahdah-compliant form design are simultaneously addressing the consumer skepticism Pew measured. The same engineering effort delivers TCPA-defensibility and conversion-rate improvement against an AI-skeptical buyer population.

Vertical Confidence Inversion – Mortgage Versus Insurance

The vertical-specific surveys diverge from each other in ways the Pew baseline alone does not capture, and the divergence matters for operator funnel design.

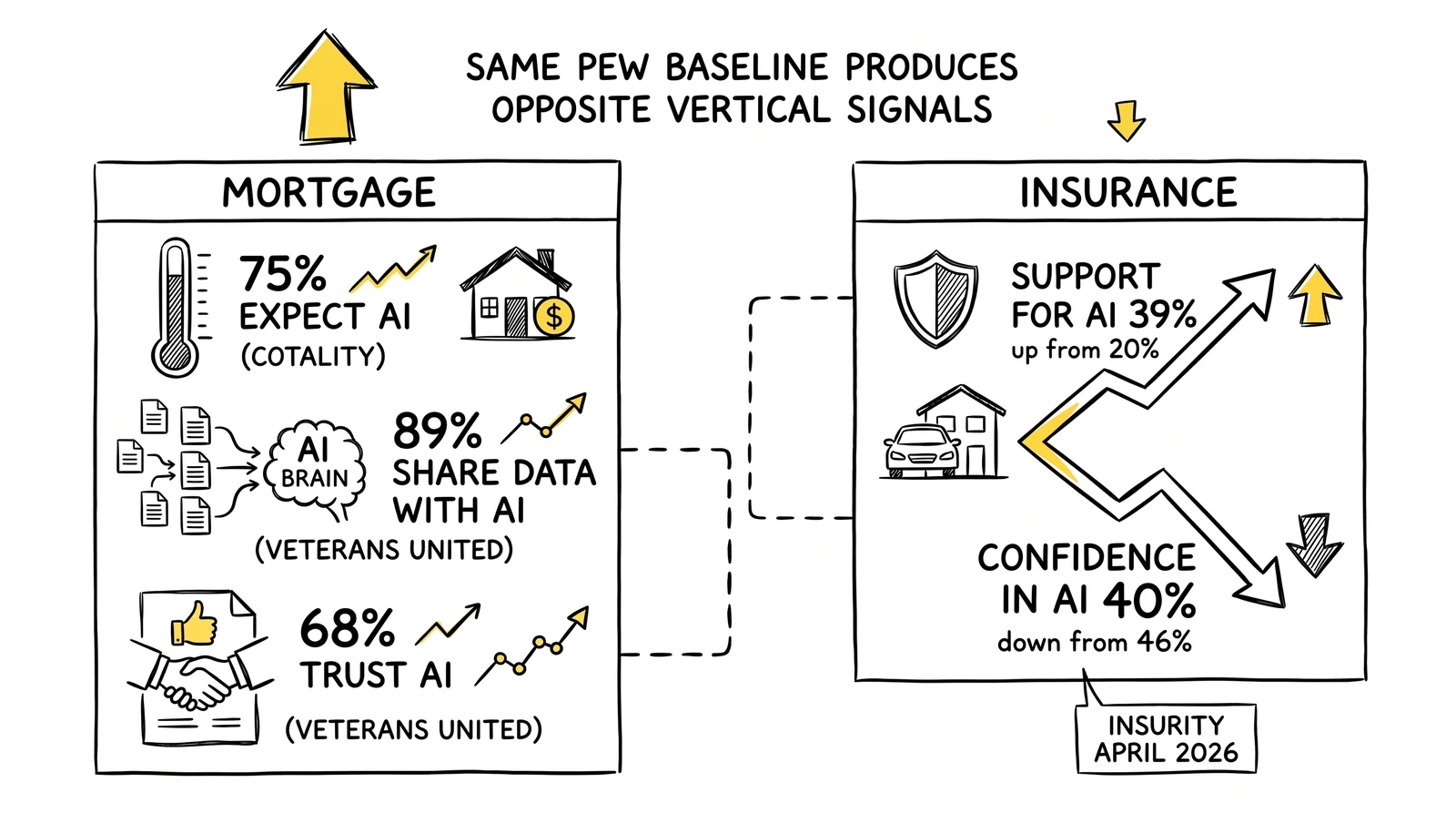

Cotality’s 2026 homebuyer survey found 75 percent of homebuyers expect AI in the mortgage process. NerdWallet’s 2026 Home Buyer Report found 48 percent of buyers had used or planned to use AI in homebuying. Veterans United reported 89 percent of buyers would share financial data with a lender AI and 68 percent trust mortgage AI information. The mortgage vertical shows consumer acceptance of AI mediation that runs notably above the Pew baseline trust of 29 percent. The structural reason is likely that mortgage decisions involve substantial information processing where AI assistance adds clear value, and the resulting prequalification produces meaningful buyer benefit (faster approval, clearer rate comparison).

Insurity’s April 2026 insurance industry survey produced opposite numbers. Consumer support for AI in insurance rose to 39 percent, up from 20 percent in 2025. But confidence in AI use fell to 40 percent, down from 46 percent in 2025. The insurance vertical shows rising acceptance of AI presence but declining confidence in AI competence – the opposite trajectory from mortgage. Digital Insurance’s parallel coverage documented the same inversion: customers want AI to be available but trust its specific use less than they did the prior year.

The funnel-design implication is vertical-specific. Mortgage funnels should lean into AI-assisted prequalification, AI-mediated rate comparison, and AI-driven document review, because the consumer cohort expects and accepts that mediation. Insurance funnels should lead with human-in-the-loop callback within the canonical five-minute window, with the AI layer present but explicitly secondary. The same lead converts under different funnel choreography depending on the vertical, and operators running multi-vertical funnel infrastructure should split their templating accordingly.

The home-services and solar verticals fall closer to the insurance cohort than to mortgage. Consumers shopping for HVAC replacement, roof repair, or solar installation make the decision rarely enough that they do not develop AI-evaluation comfort the way mortgage buyers do across a homebuying cycle. The funnel mechanics that work for these verticals favor the speed-to-human-callback model the bot detection and CAPTCHA infrastructure analysis framed for compliance defense, applied here as conversion optimization.

The B2B vertical convergence point comes from 6sense’s November 12, 2025 Buyer Experience Report, which found 94 percent of B2B buyers use large language models to summarize content during purchase evaluation and 58 percent of buyers engaged sellers earlier in the cycle to clarify AI-generated impressions. The 18-to-24-month consumer-AI trajectory Pew documented is the B2B side’s 9-to-12-month trajectory at higher intensity. The structural insight crosses populations.

The Conductor and Brinker Layer – Why GEO Matters More After Pew

Conductor’s April 20, 2026 AgentStack launch and the broader generative-engine-optimization category respond to the Pew adoption data directly. If 60 percent of US adults read AI summaries in search results and 49 percent use chatbots for information search, the operator’s competitive position in AI-mediated discovery surfaces is no longer an experimental SEO question. It is the discovery-layer position itself.

The chiefmartec State of Martech 2026 chrysalis framework named generative engine optimization as the reinvention of SEO. Pew’s June 17 data is the consumer-side validation that the reinvention is not speculative. The buyer population has shifted enough of its discovery behavior to AI-mediated surfaces that operators absent from those surfaces are losing pre-funnel attention at measurable rates.

The vertical lead-gen translation runs through the same chrysalis dimensions. Insurance and mortgage shopping queries that previously generated landing-page visits now increasingly resolve inside Perplexity, ChatGPT, Claude, and Gemini summary responses. The operator who structures its content for citation in the answer-engine surface captures the favorite-vendor slot before any form fill. The operator who optimizes only against traditional Google ranking captures progressively less of the discovery surface as the AI-summary share of search behavior grows.

Conductor’s reported 50-plus new logos in Q3 2025 including BlackRock and TD Bank, and the company’s reported greater-than-125-percent net revenue retention, signal that enterprise adoption of GEO-specific tooling is moving from experimental to budget-line-item status. For lead-gen verticals where the operator was previously the price-comparison surface – insurance comparison sites, mortgage prequalification platforms, solar quote aggregators – the question is whether the operator’s content is structured for citation in the AI-discovery layer or for click capture in the legacy click-based layer. The investment between the two is non-trivial; the alternative is gradual erosion of the discovery-surface position.

What Lead Operators Should Do in the Next 90 Days

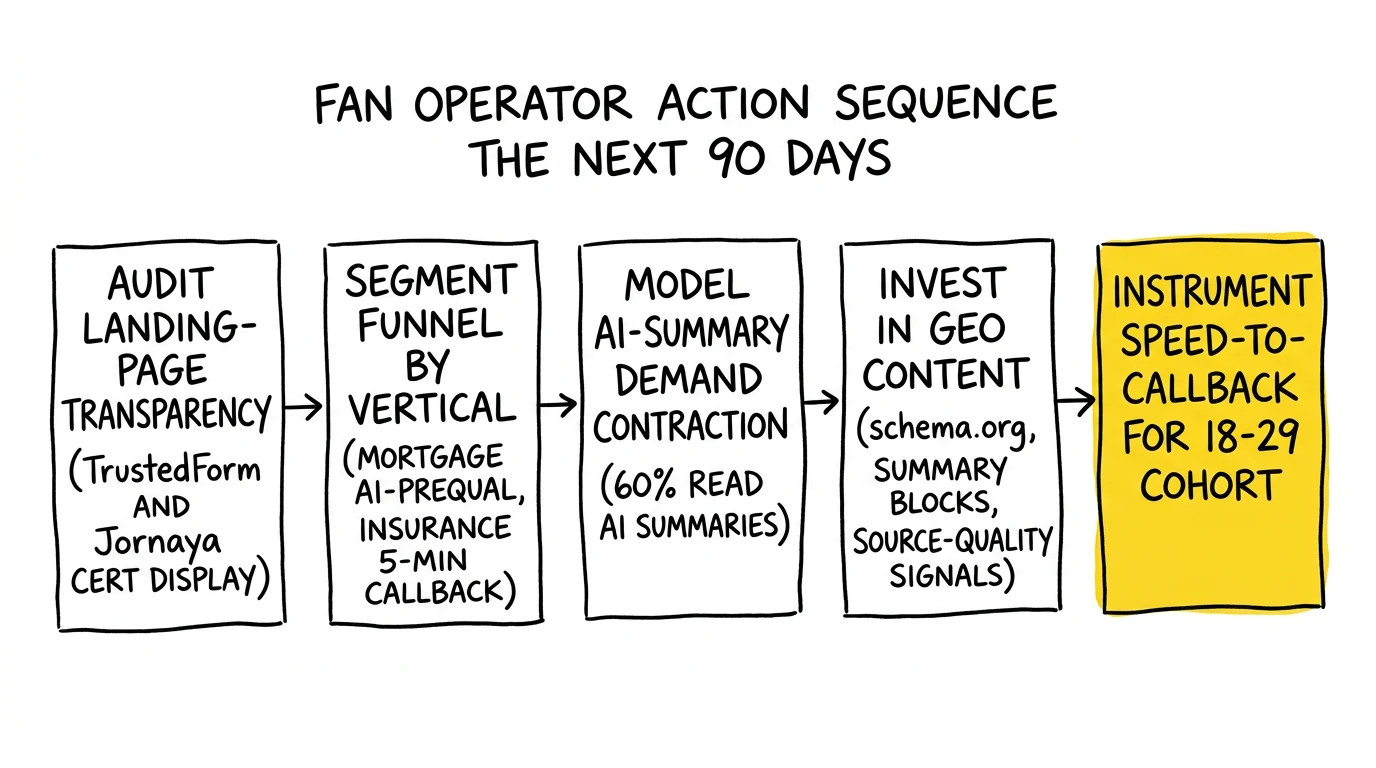

The action surface follows from the Pew data directly. Five steps map the implementation arc.

First, audit landing-page transparency against the Pew 71-percent data-security concern. Lead-gen forms that bury consent capture in fine print, route through unmarked AI qualification, or obscure TrustedForm and Jornaya certificate display underperform against the buyer population Pew measured. The audit should include visible cert display, explicit data-handling language, and explicit AI-involvement disclosure.

Second, segment funnel choreography by vertical against the consumer-confidence data. Mortgage funnels lean into AI-mediated prequalification per Cotality, NerdWallet, and Veterans United data. Insurance funnels lead with five-minute human-callback per Insurity data. Home-services and solar funnels follow the insurance pattern. Multi-vertical operators running shared funnel templates should split the templating.

Third, model the AI-summary-reading impact on pre-funnel demand. The 60 percent reading AI summaries connects to the Forrester GTM Singularity 20-to-30 percent pre-funnel demand contraction operator-side analysis. The funnel volume forecast for Q3 and Q4 2026 should price in continued discovery-surface migration rather than assume stable click-based search behavior.

Fourth, invest in GEO content structure. The operator’s landing pages, comparison content, and explainer assets should be structured for citation in answer-engine surfaces. Specific implementations include schema.org markup for Article and FAQPage entities, explicit summary blocks that answer the buyer’s question in the first sentence, and source-quality signals (author attribution, fact-check provenance, dated updates) that AI systems weight in citation decisions. Cross-reference the agentic-browser form-fraud analysis for the operational reality that AI agents now submit forms as well as read summaries.

Fifth, instrument speed-to-callback against the 18-29 cohort specifically. The cohort’s combination of heaviest adoption and highest skepticism makes it the prime conversion target for funnels that close the AI loop quickly. Sub-five-minute callback delivery, transparent AI-disclosure on the qualification step, and explicit consent capture pricing produce the strongest conversion outcomes against this cohort. The operator that nails the 18-29 funnel will own the cohort that grows into the 30-49 cohort over the next five years.

Key Takeaways

- Pew published Americans and AI 2026 on June 17, 2026, drawn from a 5,119-respondent American Trends Panel survey fielded February 17 to 23. Margin of error is ±1.6 percentage points.

- The three-point adoption trajectory for ChatGPT is 18 percent (2023), 34 percent (2025), 44 percent (2026). Broader AI chatbot use reached 49 percent.

- Trust in chatbot output stalled at 29 percent. Sixty percent of US adults read AI summaries in search results. Seventy-one percent expect AI to weaken personal data security.

- The 18-29 cohort uses chatbots at 66 percent and is also the most pessimistic at 48 percent expecting negative AI societal impact. The adoption-and-skepticism inversion is the signature pattern of the cohort.

- Adobe Q2 2026 data shows AI-referred traffic converting 42 percent better than non-AI traffic, reversing the prior year. The buyer arrives pre-qualified by the AI interaction.

- Mortgage vertical surveys (Cotality, NerdWallet, Veterans United) show consumer AI acceptance above Pew baseline. Insurance vertical surveys (Insurity, Digital Insurance) show declining AI confidence. Funnel choreography should split by vertical.

- 6sense’s November 12, 2025 B2B Buyer Experience Report found 94 percent of buyers use LLMs to summarize content during purchase evaluation. Consumer and B2B trajectories converge.

- Generative engine optimization is no longer experimental. Conductor reports 50-plus new enterprise logos in Q3 2025 including BlackRock and TD Bank, with greater-than-125-percent net revenue retention.

- The funnel design implication is to close the trust loop quickly through transparency, jump-to-callback, and explicit consent capture rather than extending the AI layer further into the conversion path.

Sources

- Pew Research Center – Americans and AI 2026 (June 17, 2026)

- Pew Research Center – How Opinions and Use of AI Differ by Age (June 17, 2026)

- Adobe – Q2 2026 AI Traffic Report

- Digital Commerce 360 – Adobe AI-Referred Traffic to Retail Sites Doubles in a Year

- 6sense – 2025 Buyer Experience Report

- NerdWallet – 2026 Home Buyer Report

- HousingWire – Cotality 2026 Homebuyer AI Survey

- National Mortgage News – 9 in 10 Buyers OK Sharing Financial Data with AI

- ProgramBusiness – Consumer Support for AI in Insurance Nearly Doubles

- Digital Insurance – Insurance Customers’ Trust in AI Fell to 40 Percent

- Conductor – Enterprise AgentStack Launch (April 20, 2026)