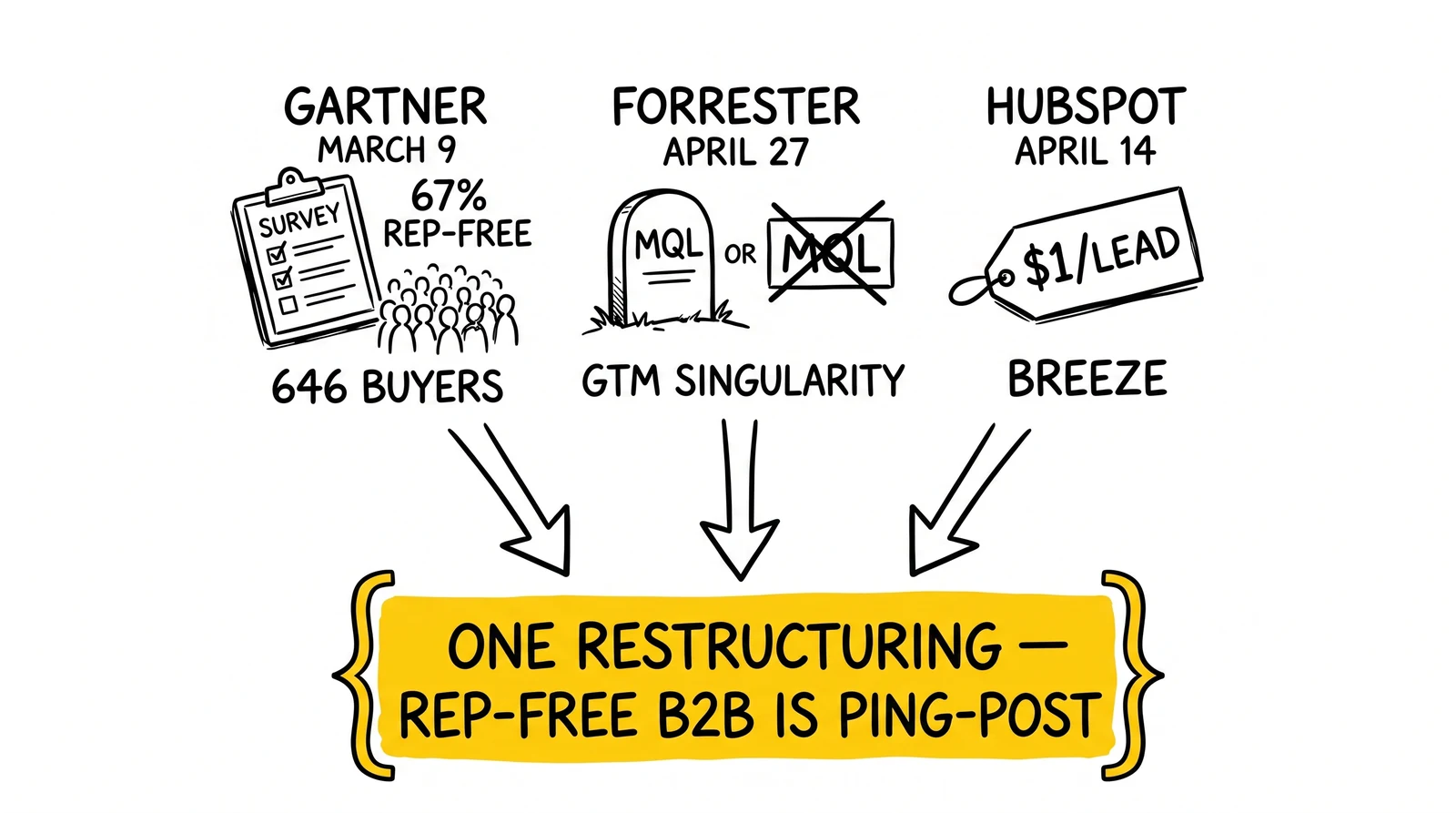

Three research firms named the same restructuring in three different ways within a single quarter – and the lead-generation industry already runs the architecture that comes next.

When Two-Thirds of Buyers Don’t Want a Sales Call

On March 9, 2026, Gartner published a sales survey finding that 67% of B2B buyers prefer a rep-free purchasing experience. The sample was 646 buyers, fielded in August and September 2025, with Gartner Sales Research as the survey vehicle and analyst Alyssa Cruz as the named lead. Six weeks later, Forrester launched its GTM Singularity research at the B2B Summit North America in Phoenix and described marketing-qualified-lead-driven go-to-market as structurally obsolete. Three weeks before Forrester’s keynote, on April 14, HubSpot announced that its Breeze prospecting agent would move to outcome-based pricing at $1 per qualified lead delivered.

Three independent signals. One quarter. One restructuring.

The Gartner finding is not the first time a research firm has reported that B2B buyers prefer fewer sales conversations. In 2019, Gartner published a comparable statistic about low-complexity purchases. Forrester has been tracking the decline of seller-led journeys since at least 2018. CEB’s Challenger Sale research, published in 2011, already documented that buyers were completing 57% of the purchase journey before contacting a vendor. The direction is not new. What is new in 2026 is the magnitude – two-thirds across the full B2B buying population – and the simultaneous arrival of a substitute for the rep.

That substitute is the AI agent.

The lead-generation economy, built over roughly two decades on the assumption that a captured contact would eventually talk to a salesperson, now has to plan against a contact who has no intention of doing so. The lead is still being captured. The handoff to a human seller is what no longer happens in two out of three buying journeys.

This analysis walks through the three signals individually, the structural pattern they describe together, and the operator question every lead seller and lead buyer should be running through their next 90-day plan: rep-free B2B procurement is, mechanically, a ping-post market – and the infrastructure to run it already exists inside the lead-aggregator industry. The strategic question is who closes the gap first – a lead aggregator extending into agent-mediated B2B procurement, or a CRM vendor extending into ping-post mechanics.

What Gartner Actually Measured

The Gartner survey methodology matters because the 67% figure has been miscited several times in secondary coverage. Gartner Sales Research fielded the survey across 646 B2B buyers between August and September 2025. The respondents were buyers who had completed a B2B purchase in the prior 12 months, with no industry restriction in the sampling frame. The full title of the published finding was that 67% of buyers prefer a rep-free experience “for at least part of their purchase.” The qualifier matters.

A literal reading is that 67% of buyers prefer to do some part of the journey without a rep – not that 67% of buyers refuse all rep contact across all purchases. The figure is, in effect, a measurement of which portion of the buyer journey has been digitally disintermediated. In 2019, Gartner reported a comparable preference at 75% – but that figure was restricted to low-complexity purchases. The 2026 figure applies across the full sample, including high-complexity enterprise deals.

Read against the 2019 benchmark, the directional reading is that the rep-free preference has expanded outward from low-complexity SKUs into the territory previously dominated by enterprise-grade rep-led selling. The 45% of buyers who told Gartner they had used artificial intelligence in a recent purchase is the operational driver. Buyers who summarize, compare, and shortlist with an AI tool have substituted that AI for the research conversations they previously had with sales engineers, customer success managers, and inside-sales representatives.

Secondary coverage by Demand Gen Report’s news brief on the survey carried the headline number cleanly. Digital Commerce 360’s March 17, 2026 follow-up analysis added context that lead-generation operators should pay attention to: the rep-free preference is uniform across industries that Digital Commerce 360 reports cover, including high-ticket B2B equipment, software, and financial services – categories where seller-led enablement has been the historical norm.

The miscite to watch for is the “75% rep-free” figure that has appeared in aggregator summaries during 2026. That number is the 2019 Gartner result, applied to low-complexity purchases. Operators should standardize on the 2026 Gartner Sales Research number – 67% across 646 buyers – and cite the March 9, 2026 press release as the source.

What Gartner did not measure, and what operators have to estimate locally, is the conversion-rate impact of the preference. A buyer who prefers a rep-free experience but still closes the deal converts. A buyer who refuses rep contact and disqualifies on their own does not. The 67% is a preference reading, not a conversion-rate reading. The translation into pipeline economics belongs to the operator, and the next four sections walk through that translation.

Forrester’s GTM Singularity Names MQL Obsolescence

Forrester launched the GTM Singularity research framework at the B2B Summit North America in Phoenix on April 27, 2026. The framework introduces what Forrester calls the ARC model – Augmented, Resilient, Collaborative – as the replacement for funnel-based, MQL-driven go-to-market. The keynote and supporting research materials describe marketing-qualified-lead obsession as structurally outdated. The specific claim is not that lead scoring stops; it is that scoring a single contact at a single moment in time misses the architecture of how B2B purchases now happen.

Augmented refers to AI augmentation across both buyer and seller workflows. A modern revenue motion has to assume the buyer is augmenting their research and decision-making with AI, and that the seller is augmenting their outreach and qualification with AI. Resilient refers to revenue motions that survive multi-stakeholder, multi-quarter buying cycles – the 22-person, 9-to-15-month enterprise deal. Collaborative refers to the alignment of marketing, sales, product, and customer success on shared revenue motion rather than handoff-based qualification gates.

Forrester’s October 28, 2025 Predictions report had already forecast the operational mechanism. The exact line: “at least one in five B2B sellers will be compelled to respond to AI-powered buyer agents with dynamically delivered counteroffers via seller-controlled agents.” Forrester separately reported that 61% of purchase influencers said their organization had implemented or planned to implement a private generative AI engine in 2026. These are the numbers behind the structural claim. If one in five sellers is responding to AI buyer agents, and 61% of buyer-side influencers are running private GenAI engines, then MQL flags against individual contacts capture a vanishing share of the actual decision-making activity.

The pattern is documented in the existing analysis of Forrester’s GTM Singularity research, which works through the implications for pre-funnel demand generation. The signal that lead-generation operators should specifically extract from the GTM Singularity framework is that the marketing-to-sales handoff – the qualification gate at which a lead becomes a sales-accepted opportunity – is being replaced. Forrester does not name a replacement KPI in the press materials. Pierre Herubel’s 2026 B2B Marketing Playbook proposes “qualified pipeline” as the operational alternative: alignment of marketing accountability with sales-recognized pipeline dollar value rather than contact-level qualification flags.

The Herubel reframe is consistent with what high-performing B2B revenue teams have already implemented, which is full-funnel attribution against revenue rather than contact-stage qualification. Chris Walker has spent years arguing that MQLs measure the wrong thing – that B2B revenue cannot be reverse-engineered from contact-stage tracking because most enterprise purchases originate in dark social, peer references, and pre-aware demand generation that contact tracking systematically misses. The 2026 Forrester GTM Singularity framework is the major-research-firm endorsement of an argument practitioners have been making since at least 2021.

The operator translation: if MQL is obsolete as a primary KPI, the question becomes what replaces it on the joint marketing-sales scorecard. Three candidates have emerged in 2026 boardroom conversations. First, qualified pipeline – the dollar-weighted opportunity-level reading Herubel favors. Second, agent-engaged accounts – the count of buying-network accounts that have had a measurable agent-mediated interaction with the seller’s content, demo environment, or pricing surface. Third, intent-confirmed leads – leads carrying a mandate token or equivalent verifiable-intent payload, which can be attributed to a downstream conversion event without contact-stage qualification gates.

Each of the three replaces the MQL at a different point in the funnel. None of them is yet standardized across the industry. Operators choosing among them in 2026 are essentially betting on which of the three will become the post-MQL primary KPI.

The 22-Stakeholder Buying Network Meets the Rep-Free Preference

Forrester’s January 21, 2026 State of Business Buying report measured the average B2B buying network at 22 individuals – 13 internal stakeholders inside the buying organization and 9 external influencers ranging from analysts and consultants to peer-network references and AI advisors. The same study reported that 94% of buyers use generative AI somewhere in the purchase process, and that 94% of buyers operating in groups of six or more report clear benefits from agentic assistance.

The two findings, paired against the Gartner 67% rep-free preference, point at a structural impossibility for rep-led enablement.

Twenty-two stakeholders is a number that breaks every traditional sales-development workflow. An SDR cohort responsible for outbound qualification cannot maintain warm coverage of 22 individuals per active opportunity across a portfolio of 50 or 100 simultaneous deals – that is more than 1,000 to 2,000 active relationships in any given quarter, with each relationship requiring a meaningful next touch. The math has never worked at that density. What used to make rep-led enablement viable in enterprise sales was that most of the 22 stakeholders were peripheral and the seller could focus on three to five “champions,” “decision makers,” and “economic buyers” identified through MEDDIC or similar qualification frameworks. The Gartner 67% rep-free finding is what breaks that compression.

If two-thirds of the buying network prefers no rep contact, the three-to-five “champion” cohort is no longer reliably the set of stakeholders the seller can actually reach. The decision authority may be precisely among the rep-resistant stakeholders. And if the buyer-side organization is using a private GenAI engine – as 61% of purchase influencers told Forrester – the buying group’s internal communication may be routed through that engine in ways the seller never sees. The seller’s view of the buying network is incomplete by design.

The lead-aggregator analogy is exact. Every “external influencer” in Forrester’s 9-person external cohort – every analyst, every consultant, every peer-network reference – is a node in the buying decision the rep does not see. Every lead that hits a comparison form on an aggregator-run site is precisely an instance of one of those external nodes acting on the buyer’s behalf. The aggregator industry has been building the infrastructure for cross-network buyer persuasion since the early 2000s. The B2B sales world is now arriving at the question.

Pierre Herubel’s 2026 playbook reframes the marketing-organization response as a shift from MQL-volume targets to qualified-pipeline targets coupled with multi-touch engagement of the buying network. The implementation pattern is dark-social attribution, peer-influencer activation through podcast and community programs, and content distribution architected for AI agent ingestion rather than human reader engagement. Each tactic is, mechanically, an attempt to reach the rep-resistant stakeholders without a rep.

Only AI agents persist across a 22-person buying network. A human seller cannot. A static piece of content cannot. A nurture sequence cannot. An AI agent capable of personalized engagement with each of the 22 stakeholders, sensitive to each stakeholder’s role in the decision, can. The Forrester October 2025 prediction that one in five sellers will respond to buyer agents with seller-controlled agents is the operational reading of this – the only way the seller scales coverage across the 22-person network is by deploying an agent that does it.

For lead-generation operators, the implication is that lead quality measurement against rep-mediated outreach is becoming obsolete in the same way the MQL is. A lead that converts under agent-mediated outreach is structurally different from a lead that converts under rep-mediated outreach, because the persuasion mechanics are different. Conversion-rate benchmarking has to be re-established within the next 12 to 18 months against agent-mediated outreach.

$1 per Lead – When HubSpot Adopted the Lead-Aggregator Pricing Model

On April 14, 2026, HubSpot moved its Breeze AI prospecting agent to outcome-based pricing at $1 per qualified lead delivered. The data layer behind the Breeze prospecting agent is Apollo, embedded as the underlying data provider. MarTech.org reported the pricing pivot, framing it as the first time a major CRM vendor priced its outbound automation against a per-lead unit cost. It is not, in fact, the first time anyone has priced lead generation per lead – the lead-aggregator industry has done so for two decades. It is the first time the pricing model crossed into a major CRM.

The number – $1 – is operationally interesting at three levels.

First, at a benchmark level, $1 is at the low end of the cost-per-lead range for high-volume comparison-shopping verticals in the lead-aggregator industry. Insurance comparison shopping at the discovery stage runs at single-digit-dollar CPLs in many sub-verticals. Solar discovery leads run higher, into the $20-to-$80 range depending on consent quality. Mortgage refinance pings can clear $40-to-$120 depending on borrower profile. A $1 lead is not a high-intent lead by aggregator standards; it is a top-of-funnel discovery contact. HubSpot Breeze’s $1 is comparable to a low-friction sign-up generated by a content-marketing landing page, not a transaction-ready quote-request from a long-form insurance form.

Second, at a budget-line level, the pricing pivot moves prospecting spend from a fixed SaaS subscription to a variable per-outcome cost. The CFO conversation changes. A CRM tier subscription that delivers prospecting was previously a fixed line item with seat counts as the scaling axis. The Breeze $1-per-lead pricing makes prospecting a variable cost scaling with lead volume. For revenue operations leaders, this means the prospecting budget can be unbounded if lead volume scales – and the budget approval process has to incorporate a usage-monitoring layer that the seat-based subscription did not require.

Third, at a competitive-pricing level, HubSpot/Apollo at $1 per qualified lead is now directly benchmarkable against MediaAlpha, EverQuote, QuinStreet, LendingTree, and every other lead-aggregator operator at the lead-unit level. The pure-play aggregators have spent decades building lead-quality SLAs – return policies, fraud screening, deduplication windows, consent capture certificates from TrustedForm or Jornaya. HubSpot/Apollo’s $1 leads will be evaluated against those SLAs by buyers who have run lead-aggregator inventory for years. The aggregator buyer who is asked to evaluate Breeze leads will run them through the same return-rate, contact-rate, and conversion-rate analysis they run on every other lead source.

The structural overlap is what creates the strategic question. The lead-aggregator industry serves financial services, insurance, home services, education, and several B2C verticals at scale. HubSpot/Apollo’s Breeze serves B2B SaaS, services, and several B2B verticals at scale. The verticals are mostly different. But where they overlap – financial services lead generation that combines B2B SaaS targeting with consumer pipeline, B2B fintech, B2B insurance distribution – HubSpot/Apollo at $1 per lead is now a direct competitor to pure-play aggregators.

The compliance dimension is the third lever. Lead-aggregator operators have built TCPA-compliant consent capture infrastructure since the One-to-One Consent rule cycle of 2024-2025. TrustedForm, Jornaya, and similar consent-capture vendors are tooling for agent-flagging in 2026. HubSpot/Apollo’s $1 leads – if they include consent-capture and call-recording for downstream telephony – have to comply with the same regulatory architecture. If they do not, the leads are priced below the floor that aggregator-grade consent capture would impose, and the cost differential is a regulatory exposure rather than a competitive advantage. The TCPA prior express written consent regime applies to whoever owns the marketing relationship at the point of contact, and lead-buyer due diligence in 2026 will not waive that requirement because HubSpot is the vendor.

Salesforce Agentforce and ZoomInfo Copilot Workspace are the parallel motions. Salesforce reports 6,000+ paid Agentforce deals as of early 2026, with Einstein SDR running buyer-mediated outreach and Einstein Sales Coach role-playing the buyer side in seller-training scenarios. ZoomInfo’s Copilot Workspace surfaces buying signals into Salesforce and HubSpot workflows from ZoomInfo’s intent-data inventory. The three vendors – Salesforce, HubSpot, ZoomInfo – represent the major CRM and intent-data platforms repositioning around agent-mediated prospecting in the same six-month window.

For the lead-aggregator industry, the strategic implication is convergence on the per-lead unit-economic frame. Buyers are now evaluating CRM-vendor leads against pure-play aggregator leads on the same unit-cost axis. The seller’s pricing power belongs to whoever has the better consent capture, lower return rate, higher contact rate, and higher conversion rate – not to whoever owns the CRM. The pure-play aggregators have a measurable two-decade head start on the unit-economic disciplines that this competition will be settled on.

Agent-to-Agent Procurement Is Structurally Ping-Post

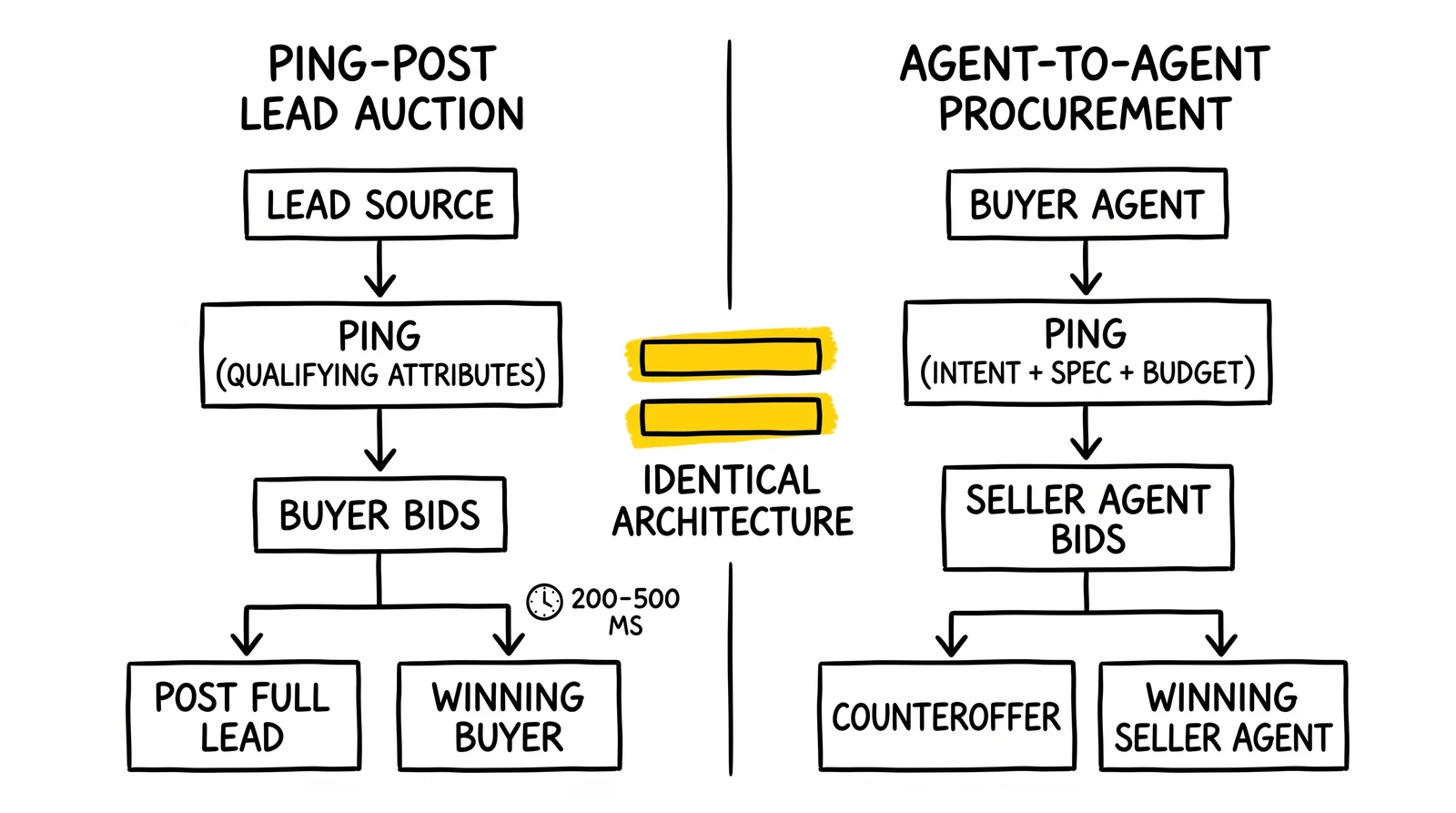

This is the analytical centerpiece. Forrester’s prediction that one in five B2B sellers will respond to AI buyer agents with seller-controlled agents in 2026 describes a market architecture without naming it. The market it describes is, mechanically, a ping-post market.

The ping-post architecture, documented in the existing analysis of ping-post systems for real-time lead auctions, works as follows. A lead source captures buyer intent – a quote request, a comparison-shopping form submission, a phone call. The lead source broadcasts a “ping” containing the qualifying attributes of the lead – geography, demographics, intent signals, consent provenance – to a set of pre-qualified buyers. Each buyer’s bidding system responds with a bid representing what the buyer will pay for the lead at those qualifying attributes. The highest qualifying bid wins; the lead source posts the full lead payload to the winning buyer. The cycle, in mature implementations, completes in 200 to 500 milliseconds.

Now substitute “buyer agent” for “lead source,” “seller agent” for “buyer,” and “RFP response” for “lead payload.” The architecture is identical. A buyer agent representing an organization captures the buyer’s intent – a software requirement, a service specification, a price ceiling. The buyer agent broadcasts a ping containing the qualifying attributes of the procurement event to a set of pre-qualified seller agents. Each seller agent’s bidding system responds with a proposal representing what the seller will offer at those qualifying attributes. The best qualifying proposal wins the buyer’s attention; the buyer agent advances to a deeper engagement with the winning seller agent.

Forrester’s “one in five sellers” prediction is the deployment-rate forecast for sellers running the seller-side bidding system. Gartner’s $15 trillion in agent-intermediated B2B procurement by 2028, presented by Daryl Plummer at Gartner IT Symposium/Xpo 2025 and summarized by Digital Commerce 360 on November 28, 2025, is the addressable-market forecast for the volume of procurement events flowing through these auctions. The 90% of B2B purchases figure attached to the same forecast is the procurement-penetration forecast.

The lead-aggregator industry has been running this auction architecture for roughly twenty years. The mature platforms – Boberdoo, Phonexa, LeadsPedia, Lead Distro AI, and several proprietary buyer-side bidding systems run by enterprise lead aggregators – have solved a series of infrastructure problems that CRM vendors retrofitting agent negotiation are about to discover. Sub-second auction latency. Buyer ranking algorithms that incorporate buyer-side conversion data into bid weighting. Deduplication windows that prevent a single lead from being sold to competing buyers within the same opportunity. Fraud screening against device fingerprints, IP reputation, and behavioral signals. Consent-capture certificates from TrustedForm and Jornaya that establish the regulatory provenance of the lead. Each is a multi-year engineering investment.

The agent-mediated B2B procurement market that Forrester and Gartner describe has the same engineering requirements. A buyer agent broadcasting an RFP-equivalent at scale will require sub-second seller-agent response, lest the buyer experience be degraded. Seller agents bidding into the auction will require a ranking algorithm sensitive to historical buyer-conversion-rate against the agent’s specific seller. Deduplication across competing seller agents – preventing the same buyer agent from advancing into closing motion with multiple sellers simultaneously – is a non-trivial protocol problem. Fraud screening against spoofed buyer agents, hallucinated intent signals, or out-of-mandate procurement events is a research-grade challenge. Consent and mandate capture, addressed in the existing analyses of the AP2 mandate framework and the Know Your Agent compliance approach, is the agent-mediated successor to TCPA consent capture.

The strategic point is this. CRM vendors retrofitting agent negotiation – Salesforce Agentforce, HubSpot Breeze, ZoomInfo Copilot Workspace – are arriving in a market whose infrastructure questions have been answered by ping-post operators since the mid-2000s. The Salesforce, HubSpot, and ZoomInfo engineering teams will solve those infrastructure questions, but they are years behind the lead-aggregator industry on the specific disciplines that operating a real-time auction at scale requires.

There is a reciprocal observation. The lead-aggregator industry has the auction infrastructure, but it does not have the buyer-agent integration and the seller-agent integration that the B2B agent-procurement market requires. The aggregator-platform players run buyer-side bidding through buyer-managed bid editors, not through autonomous AI agents acting on the buyer’s behalf. Extending into agent-mediated procurement requires extending the bid-management layer to accommodate autonomous agents, with the additional protocol surface that real-time auction technology architectures already pre-suppose.

Whichever of the two industries closes the integration gap first – CRM vendors building auction infrastructure, or lead aggregators building agent integration – sets the dominant architecture for agent-to-agent B2B procurement. The deeper analysis in the existing piece on agentic commerce and AI agents in lead generation walks through the protocol layer that both sides are racing to. The Gartner $15 trillion forecast and the Forrester one-in-five-sellers prediction are both signals about who wins that race.

What Changes for Lead Sellers in the Next Twelve Months

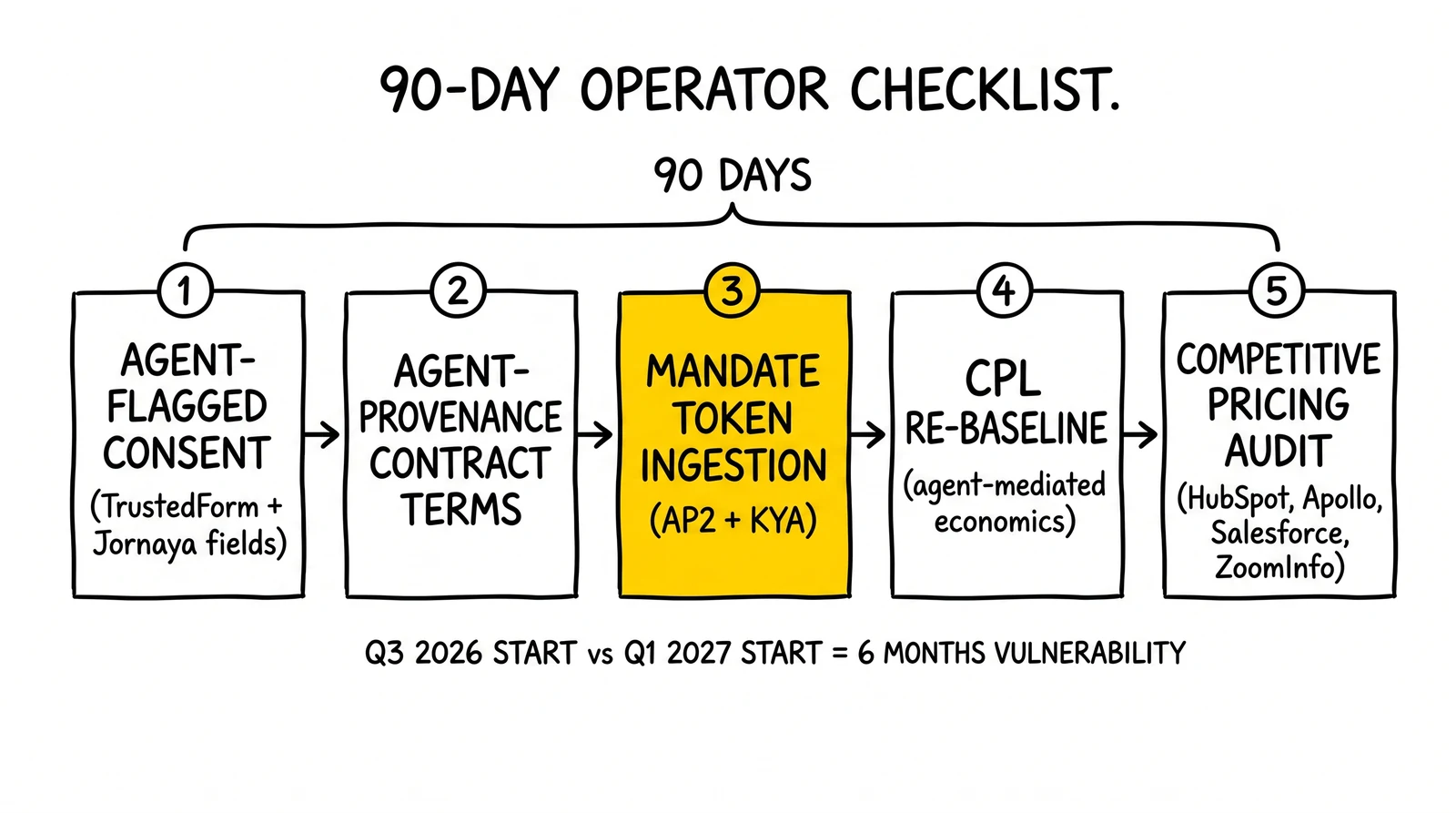

Five specific actions for lead-aggregator operators and lead sellers running B2B inventory.

First, add agent-mediated submission detection to the consent-capture stack. TrustedForm and Jornaya have announced agent-flagging transitions for 2026. The flagging fields identify, on the consent certificate, whether the form submission came from a human-typed interaction, an AI-agent-mediated interaction, or a hybrid pattern in which an agent prefilled the form and a human reviewed before submission. Downstream buyers – particularly those subject to the TCPA prior express written consent regime – will require the agent-flagging fields before accepting agent-originated leads. Operators should be testing the new fields in their lead-capture stack during the May-to-July 2026 window, before downstream buyers begin requiring them at contract level.

Second, renegotiate buyer contracts to flag agent-originated leads as a distinct provenance category. The return-rate, contact-rate, and conversion-rate benchmarks lead sellers have historically tracked are calculated against human-mediated lead flows. Agent-mediated leads have structurally different conversion characteristics – higher intent precision on attributes the buyer agent verified, potentially lower contact rates because the buyer agent may not have authorized a human-rep follow-up, and different qualifying-attribute distributions. The lead-buyer relationship has to distinguish agent-originated leads from human-originated leads in the price and SLA structure, or the contractual return-rate frame will misfire when buyer behavior diverges from historical baselines.

Third, build mandate-token ingestion under the AP2 and Know Your Agent frameworks. The detailed analyses of the AP2 mandate framework and the Know Your Agent TCPA-replacement architecture walk through the mandate-token structure that agent-mediated transactions carry. The mandate token is the cryptographic-equivalent of TCPA prior express written consent, attaching to the agent’s authority to act on the principal’s behalf and establishing the audit trail downstream regulators will examine. Operators have a 12-to-18-month window to retrofit mandate-token ingestion into the existing consent-capture stack before agent-originated lead flows become a meaningful share of total inventory.

Fourth, expect compression in single-touch CPL benchmarks as agent-mediated leads carry different conversion economics. The historical lead-aggregator CPL benchmarks – single-digit dollars at the discovery stage, $30-to-$120 at the quote-ready stage – were calibrated against human-mediated buyer journeys. Agent-mediated journeys compress the time-to-conversion (an AI buyer agent moves through the funnel faster than a human buyer) and potentially compress the per-lead value capture (the agent buyer may not pay the human-buyer’s premium for sales-engineering hand-holding). Operators should model a 10-to-25% downward pressure on single-touch CPLs in agent-heavy verticals over the next 18 months – directional planning, not a precise forecast, but a planning-floor for budgeting decisions.

Fifth, audit which CRM-priced-as-CPL competitors overlap with the operator’s buyer base. HubSpot Breeze at $1 per lead, Apollo’s data layer, Salesforce Agentforce’s 6,000+ paid deals, and ZoomInfo Copilot Workspace are now competing for the same B2B lead-generation budget that lead aggregators historically captured. The overlap is greatest in B2B SaaS, B2B fintech, B2B services, and several enterprise-software verticals. For verticals with overlap, the operator’s buyer-side procurement budgets are shifting from a fixed CRM subscription to a per-lead variable cost – and the operator’s pricing has to account for the competitive comparison the buyer will run between the operator’s per-lead offer and the CRM-vendor’s per-lead offer.

The 90-day operator checklist is, in short: consent-capture agent fields tested, buyer contracts re-papered with agent-provenance fields, mandate-token ingestion architected, CPL benchmarks re-baselined for agent-mediated flows, and competitive-pricing audit against HubSpot/Apollo/Salesforce/ZoomInfo completed. Each is implementable inside a quarter for an operationally mature aggregator. None is implementable inside a quarter without the engineering investment – the gap between an operator who starts in Q3 2026 and an operator who starts in Q1 2027 is roughly six months of competitive vulnerability.

What Changes for Lead Buyers

The buyer-side mirror is simpler in structure but harder in commitment.

If 67% of buyers reject sales-representative contact, the lead-buyer industry – lenders, insurance carriers, solar installers, attorneys, education-vertical recruiters, B2B services firms – faces a choice. Continue paying for leads that require a rep-led follow-up workflow, accepting that two-thirds of the leads will not engage with the rep, with conversion compressing on the human-mediated outreach. Or migrate to agent-driven outreach using Salesforce Agentforce, HubSpot Breeze, ZoomInfo Copilot Workspace, or a comparable agent-mediated engagement stack, replacing the human-rep follow-up motion with an agent-mediated motion that the rep-free preference does not disqualify.

The economic implication is a re-baselining of per-lead conversion benchmarks under agent-mediated outreach within the next 12 to 18 months. The legacy benchmarks – 8-to-15% lead-to-customer conversion in insurance, 2-to-4% in mortgage, sub-1% in many B2B verticals – were calibrated against rep-mediated follow-up. The agent-mediated benchmarks are not yet established at industry scale. The early signal from Salesforce Agentforce deployments, HubSpot Breeze pilots, and parallel ZoomInfo Copilot Workspace adoptions is that agent-mediated outreach has higher engagement rates (the buyer agent is more responsive to a seller agent than a human buyer is to a rep) but lower closing rates (the buyer agent is more analytical and less susceptible to relationship-building closing techniques). The net conversion outcome is, at the time of writing, in flux.

For lead-aggregator buyers running on legacy CPL contracts, the practical implication is that the price they pay for leads should reflect agent-mediated conversion economics within 18 months, and renewal cycles in 2026 and early 2027 are the negotiation window to lock in the price adjustment. For lead-aggregator buyers who are migrating to direct agent-mediated stack, the question is whether to maintain the aggregator-sourced inventory at all, or to consolidate spend into the agent-mediated tools. The answer is vertical-specific. Insurance discovery leads remain a vibrant aggregator-sourced market because the consumer side of insurance comparison does not yet flow through buyer agents at scale. Enterprise B2B SaaS leads are migrating to agent-mediated stacks faster, because both sides of the procurement are agent-augmented.

The strategic question for the lead buyer is, fundamentally, how much of their downstream conversion motion they want to operate as agent-mediated rather than rep-mediated. The Gartner 67% finding makes the floor visible – at least two-thirds of buyers prefer no rep contact, and that share will grow. The ceiling for agent-mediated conversion is being established empirically across 2026 deployments.

Key Takeaways

-

Gartner’s March 9, 2026 finding: 67% of B2B buyers prefer a rep-free purchasing experience. Sample of 646 buyers fielded August-September 2025 by Gartner Sales Research, analyst Alyssa Cruz. The figure means at least part of the purchase is preferred rep-free, across the full B2B sample – not restricted to low-complexity SKUs as in the 2019 75% finding. The decision implication is that rep-led enablement infrastructure has to be re-baselined against the rep-free majority, not the rep-engaging minority.

-

Forrester’s April 27, 2026 GTM Singularity report calls the marketing-qualified lead structurally obsolete. The ARC framework – Augmented, Resilient, Collaborative – replaces funnel-based marketing-to-sales handoffs with agent-augmented, multi-stakeholder, cross-functional revenue motions. Decision implication: replace MQL as the joint marketing-sales scorecard KPI with either qualified pipeline (Herubel-style), agent-engaged accounts, or intent-confirmed mandate-tokened leads within the next two planning cycles.

-

Forrester’s January 21, 2026 State of Business Buying measures the typical B2B buying network at 22 individuals – 13 internal, 9 external – with 94% using generative AI. Decision implication: rep-led enablement cannot cover the 22-node network. Cross-network persuasion has to happen through content architected for agent ingestion, peer-network influencer activation, and dark-social attribution rather than contact-stage MQL flags.

-

HubSpot’s April 14, 2026 Breeze pricing pivot moved prospecting to $1 per qualified lead delivered. Apollo as embedded data provider. Decision implication: the lead-aggregator pricing model has arrived inside the major CRM stack. Lead-aggregator operators face direct unit-economic comparison from HubSpot/Apollo and from Salesforce Agentforce’s 6,000+ paid deals; lead-buyer CFOs face a shift from fixed subscription to variable per-outcome cost in the prospecting line item.

-

Forrester’s October 28, 2025 prediction: at least one in five B2B sellers will respond to AI buyer agents with seller-controlled agents in 2026. 61% of purchase influencers told Forrester their organization has implemented or planned a private GenAI engine. Decision implication: agent-to-agent procurement is a 2026 deployment-grade pattern, not a 2028 forecast – sellers without an agent-mediated engagement layer in 2026 are competing against sellers who have one.

-

Gartner’s $15 trillion AI-agent-intermediated B2B procurement forecast by 2028, presented by Daryl Plummer at Gartner IT Symposium/Xpo 2025. Roughly 90% of B2B purchases. Decision implication: the directional forecast is a planning anchor for capital-allocation decisions in agent infrastructure. The precise timing varies by industry; the structural direction does not.

-

Gartner’s November 18, 2025 forecast: AI agents outnumber sellers by 10x by 2028, with fewer than 40% of sellers reporting productivity gains. Decision implication: agent deployment scales rapidly, but seller-side productivity returns from agents lag – the operational benefit of agent infrastructure does not materialize uniformly, and operators that wait for proof of productivity gains will be displaced by operators that absorb the early-adoption cost.

-

Agent-to-agent B2B procurement is, mechanically, a ping-post market. Buyer agents broadcast intent; seller agents bid; best qualifying bid wins. The lead-aggregator industry has run this architecture for two decades and has solved auction latency, fraud screening, deduplication, consent capture, and buyer ranking algorithms at scale. CRM vendors retrofitting agent negotiation are years behind on the auction-infrastructure disciplines.

-

The 90-day operator checklist: consent-capture agent fields, agent-provenance buyer contract terms, mandate-token ingestion under AP2 and Know Your Agent, CPL re-baselining for agent-mediated flows, competitive-pricing audit against HubSpot/Apollo/Salesforce/ZoomInfo. Each is implementable inside a quarter for an operationally mature aggregator; the six-month gap between Q3 2026 start and Q1 2027 start is the competitive-vulnerability window.

-

The 12-to-18-month re-baselining of agent-mediated conversion benchmarks is the lead-buyer equivalent. Legacy CPL contracts calibrated against rep-mediated conversion will misprice under agent-mediated conversion economics; renewal cycles in 2026 and early 2027 are the price-adjustment window.

Sources

-

Gartner – “Gartner Sales Survey Finds 67% of B2B Buyers Prefer a Rep-Free Experience,” press release, March 9, 2026. https://www.gartner.com/en/newsroom/press-releases/2026-03-09-gartner-sales-survey-finds-67-percent-of-b2b-buyers-prefer-a-rep-free-experience – 646-buyer sample, August-September 2025 fielding, analyst Alyssa Cruz.

-

Forrester – “Forrester: The GTM Singularity Is Collapsing Traditional Go-To-Market Approaches,” press release, April 27, 2026. https://www.forrester.com/press-newsroom/forrester-the-gtm-singularity-is-collapsing-traditional-go-to-market-approaches/ – ARC framework, B2B Summit North America launch.

-

Forrester – “Forrester 2026 B2B Marketing, Sales, and Product Predictions,” press release, October 28, 2025. https://www.forrester.com/press-newsroom/forrester-b2b-marketing-sales-product-2026-predictions/ – one-in-five sellers with seller agents, 61% private GenAI adoption.

-

Forrester – “Forrester 2026 The State of Business Buying,” press release, January 21, 2026. https://www.forrester.com/press-newsroom/forrester-2026-the-state-of-business-buying/ – 13 internal + 9 external = 22-person buying group, 94% GenAI usage.

-

Digital Commerce 360 – “Gartner: AI agents will drive $15 trillion in B2B purchases by 2028,” November 28, 2025. https://www.digitalcommerce360.com/2025/11/28/gartner-ai-agents-15-trillion-in-b2b-purchases-by-2028/ – Daryl Plummer at Gartner IT Symposium/Xpo 2025.

-

Gartner – “Gartner Predicts By 2028, AI Agents Will Outnumber Sellers by 10x, Yet Fewer Than 40% of Sellers Will Report AI Agents Improved Productivity,” press release, November 18, 2025. https://www.gartner.com/en/newsroom/press-releases/2025-11-18-gartner-predicts-by-2028-ai-agents-will-outnumber-sellers-by-10x-yet-fewer-than-40-percent-of-sellers-will-report-ai-agents-improved-productivity

-

MarTech – “HubSpot moves to outcome-based pricing for some Breeze AI agents,” April 14, 2026. https://martech.org/hubspot-moves-to-outcome-based-pricing-for-some-breeze-ai-agents/ – $1-per-qualified-lead Breeze pricing, Apollo data layer.

-

Salesforce – “Einstein Sales Agents Announcement.” https://www.salesforce.com/news/stories/einstein-sales-agents-announcement/ – 6,000+ paid Agentforce deals, Einstein SDR + Sales Coach.

-

ZoomInfo Investor Relations – “ZoomInfo Copilot Workspace: Complete Book of Business in One Workspace.” https://ir.zoominfo.com/news-releases/news-release-details/zoominfo-copilot-workspace-complete-book-business-one-workspace/ – agentic execution surfacing buying signals into Salesforce/HubSpot.

-

Demand Gen Report – “Gartner: 67% of B2B Buyers Prefer a Rep-Free Experience.” https://www.demandgenreport.com/industry-news/news-brief/gartner-67-of-b2b-buyers-prefer-a-rep-free-experience/52142/

-

Pierre Herubel – “The Full B2B Marketing Playbook for 2026,” Substack. https://pierreherubel.substack.com/p/the-full-b2b-marketing-playbook-for – qualified pipeline as MQL successor.