Three vendor moves inside ten weeks reframe the customer-data-platform category around AI agents – and the architecture choice carries cost, identity, and compliance consequences the broader coverage has not connected.

June 16 and June 17 Reframed the Category in 24 Hours

Databricks announced CustomerLake at the Data plus AI Summit on June 16, 2026, positioning the product as the company’s entry into the customer-data-platform category. HP, Circle K, AB InBev, and Getnet by Santander were named as private-preview customers. Co-founder and CEO Ali Ghodsi framed the launch with the line that marketing stops being a series of campaigns and becomes a continuous loop. Tasso Argyros, the former ActionIQ CEO who joined Databricks as VP of Engineering, leads the CustomerLake organization.

Twenty-four hours later, on June 17, BlueConic announced its acquisition of Blueshift. The combined entity reports more than 600 customers across the merged platforms. Deal terms were not disclosed in the press release. BlueConic CEO Melissa Murray Bailey and Blueshift CEO Vijay Chittoor framed the strategic rationale as giving AI agents the real-time behavioral context they need to decide and act, rather than separating the customer-data layer from the activation layer the way most CDP architectures historically did.

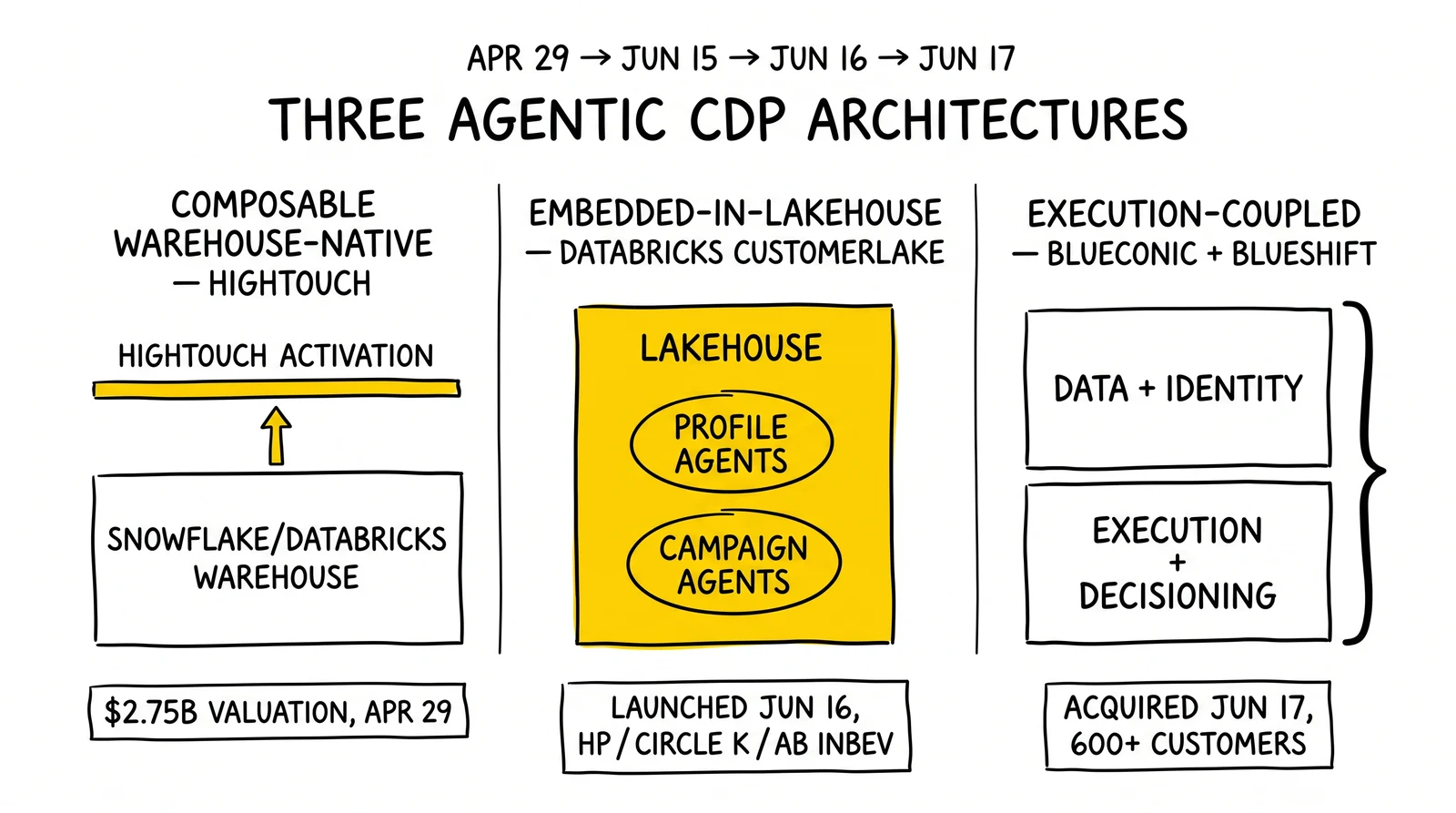

The two moves landed inside the same week and the same conference cycle. They are not coincidental. Hightouch had set the stage seven weeks earlier when it closed a $150 million Series D on April 29 at a $2.75 billion valuation, led by Goldman Sachs and Bain Capital Ventures with participation from Amplify, ICONIQ, Sapphire, and TD7. The Hightouch June 15 blog post titled “The Agentic CDP” was a category-definition exercise that anticipated the Databricks and BlueConic announcements arriving the same week.

For lead-generation operators, the strategic question is not whether the customer-data-platform category is being agentified – it is. The question is which of the three architectures now competing for the category – composable warehouse-native (Hightouch), embedded-in-lakehouse (Databricks), and execution-coupled (BlueConic plus Blueshift) – matches the operator’s routing latency, identity-resolution requirements, and TCPA-defensibility audit needs. The choice has cost and compliance consequences the broader martech coverage has not analyzed.

This article works through what each architecture commits to, what the cost-and-latency trade-offs look like for ping-post lead distribution, where identity resolution and consent capture intersect with agentic routing decisions, and the operator selection criteria that should anchor any agentic CDP procurement in the next two quarters.

What Databricks CustomerLake Actually Ships

CustomerLake launched into private preview on June 16, 2026 with four named customers spanning hardware (HP), convenience retail (Circle K), beverages (AB InBev), and financial services (Getnet by Santander). Databricks’ public framing of the product introduced two new terminology layers. Profile Agents run continuously on the Databricks Data Intelligence Platform to update customer attributes as new behavior data arrives, replacing the batched profile-update jobs traditional CDPs run on cron schedules. Campaign Agents wrap the activation logic in a continuous decisioning loop rather than the campaign-cycle batching most marketing teams have inherited from email-service-provider workflows.

The integration partner list at launch covered Adobe, Meta, Braze, Acxiom, Epsilon, The Trade Desk, LiveRamp, Iterable, Bloomreach, Snapchat, Magnite, TransUnion, Adstra, Twilio, Integral Ad Science, and Unity. The integration breadth signals two things. First, Databricks is not attempting to displace activation endpoints; it is positioning itself as the agentic decisioning layer that orchestrates which endpoint fires when. Second, the presence of TransUnion and Acxiom alongside LiveRamp on the partner list – three identity-resolution graphs across two competing holding companies after the Publicis-LiveRamp acquisition – suggests Databricks is staying out of the identity-resolution oligopoly consolidation question by integrating with all of them.

Argyros’s leadership matters more than the typical product-launch executive announcement. ActionIQ was one of the canonical SaaS CDPs of the prior generation; bringing its co-founder into a warehouse-native challenger signals that the architecture pivot is not theoretical. The implementation details that traditionally separated SaaS CDPs from warehouse-native challengers – identity resolution mechanics, activation queue management, profile-update semantics – are arriving inside CustomerLake with the operating discipline that built ActionIQ rather than as a green-field implementation.

The launch did not disclose pricing. Databricks operates on consumption-based billing across its broader Data Intelligence Platform, and CustomerLake will follow that pattern. The cost analysis sits in the architecture-level discussion below rather than in the launch announcement.

What BlueConic Plus Blueshift Actually Buys

The BlueConic acquisition of Blueshift announced June 17 combines two complementary capability layers rather than acquiring a competitor. BlueConic’s core platform handles customer-data ingestion, identity resolution, and profile management. Blueshift’s platform handles execution decisioning and cross-channel orchestration. Combined, the entity covers the full path from event capture through activation decision to channel send.

The strategic logic mirrors the question Databricks CustomerLake forces traditional SaaS CDPs to answer. If embedded-in-lakehouse architectures run continuous decisioning directly against the data warehouse, separating the data layer from the activation layer becomes a competitive disadvantage rather than a feature. Bailey and Chittoor’s joint framing of giving AI agents the real-time behavioral context they need to decide and act is the explicit response – the combined entity removes the round-trip between the data store and the activation engine that traditional two-vendor architectures impose.

The 600-customer combined base provides scale for the post-merger product roadmap. Deal terms were undisclosed, which signals either that the transaction structure included material non-cash consideration or that the parties chose not to telegraph price-per-customer-or-revenue economics. Industry coverage from MarTech.org framed the move as the SaaS-CDP cohort acquiring activation capability rather than ceding decisioning to data-platform-native challengers – the structural verdict on whether the warehouse-native architectures are winning is now being placed by SaaS-CDP capital allocators rather than by analysts.

What Hightouch Actually Did in April and June

The Hightouch story arrived in two parts that should not be conflated. The Series D closed April 29, 2026 at a $2.75 billion valuation with $150 million in primary capital, led by Goldman Sachs and Bain Capital Ventures. Participating investors included Amplify, ICONIQ, Sapphire, and TD7. The Series D documentation references existing operating metrics including the 2026 Gartner Magic Quadrant Leader recognition for Customer Data Platforms.

The June 15 “Agentic CDP” blog post is not a product launch. It is a category-positioning exercise that arrived the day before the Databricks CustomerLake launch and two days before the BlueConic-Blueshift acquisition. Read in sequence, the three events define a contested category. Hightouch staked the agentic CDP label on June 15. Databricks shipped an agentic CDP product on June 16. BlueConic acquired its way into an agentic CDP architecture on June 17.

Hightouch’s incumbent advantage in the composable warehouse-native architecture is operational maturity. The company has been shipping warehouse-native CDP capabilities for several years, accumulated customer references, and earned the Gartner Magic Quadrant Leader position. Treating the June 15 blog post as a Hightouch product pivot misreads what happened – Hightouch was already operating as a warehouse-native CDP and simply applied the agentic label to its existing positioning the week the term was crystallizing into a category descriptor.

Reported figures of $100 million-plus ARR and 100-percent-plus year-over-year growth two years running circulated through industry coverage but were not directly verified in Hightouch’s own public communications. Those metrics should be cited cautiously, with attribution to the secondary outlets rather than treated as Hightouch-confirmed financials.

Three Architectures, Three Cost Profiles

The architecture choice between warehouse-native composable, embedded-in-lakehouse, and execution-coupled translates into three distinct cost profiles that operators should model explicitly before committing.

Warehouse-native composable architecture, exemplified by Hightouch, runs activation logic directly against the customer data warehouse. The cost trade-off lands on compute. mParticle’s vendor-published analysis indicates that warehouse-native architectures running hourly profile refresh incur approximately 25 times the compute cost of daily refresh, and 5-minute sync intervals push compute to 50 times or more. The multipliers come from a SaaS-CDP vendor’s commercial analysis, so the specific numbers should be read directionally rather than as audited benchmarks. The structural insight is that warehouse-native architectures trade SaaS-CDP license fees for warehouse compute that scales nonlinearly with refresh frequency.

Embedded-in-lakehouse architecture, exemplified by Databricks CustomerLake, runs the agentic logic on the lakehouse itself. The advantage is that the agents have native access to the full data graph without round-trips. The cost question is consumption-based and depends on agent runtime against the underlying compute pool. Operators already running on Databricks for analytics workloads will absorb CustomerLake compute within their existing platform commitment rather than adding a new vendor line item. Operators not already on Databricks face the bundled cost of platform plus product.

Execution-coupled architecture, exemplified by the combined BlueConic plus Blueshift, separates the data layer from the activation layer through the integrated vendor relationship rather than through an architectural boundary. The pricing model remains SaaS-style per-record and per-message, sidestepping the warehouse-compute escalation that hits warehouse-native at high refresh frequency. The trade-off is that the data plumbing required to keep BlueConic in sync with the source customer warehouse imposes its own integration overhead.

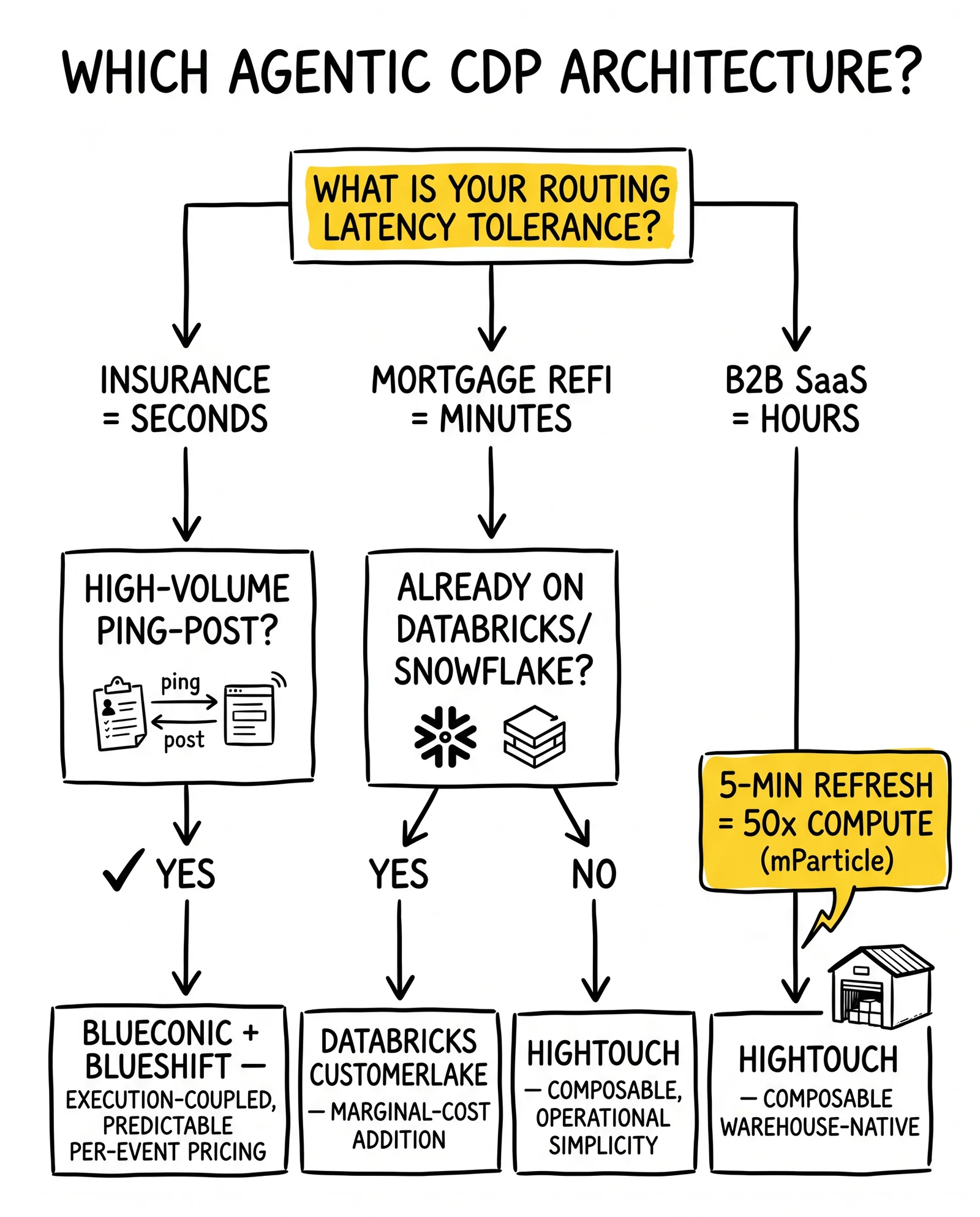

For ping-post lead distribution operating at sub-second SLAs and high event volumes, the warehouse-native compute economics make 5-minute refresh impractical without disciplined batching. The architecture choice should be modeled against actual event throughput and refresh frequency requirements before vendor selection. Operators running mid-volume lead-gen funnels with moderate refresh tolerance may favor Hightouch’s composable approach for the operational simplicity. High-volume ping-post operators with sub-second routing requirements may favor execution-coupled BlueConic-Blueshift architecture for the predictable per-event pricing. Databricks-native operations get CustomerLake as a marginal-cost addition to existing infrastructure commitment.

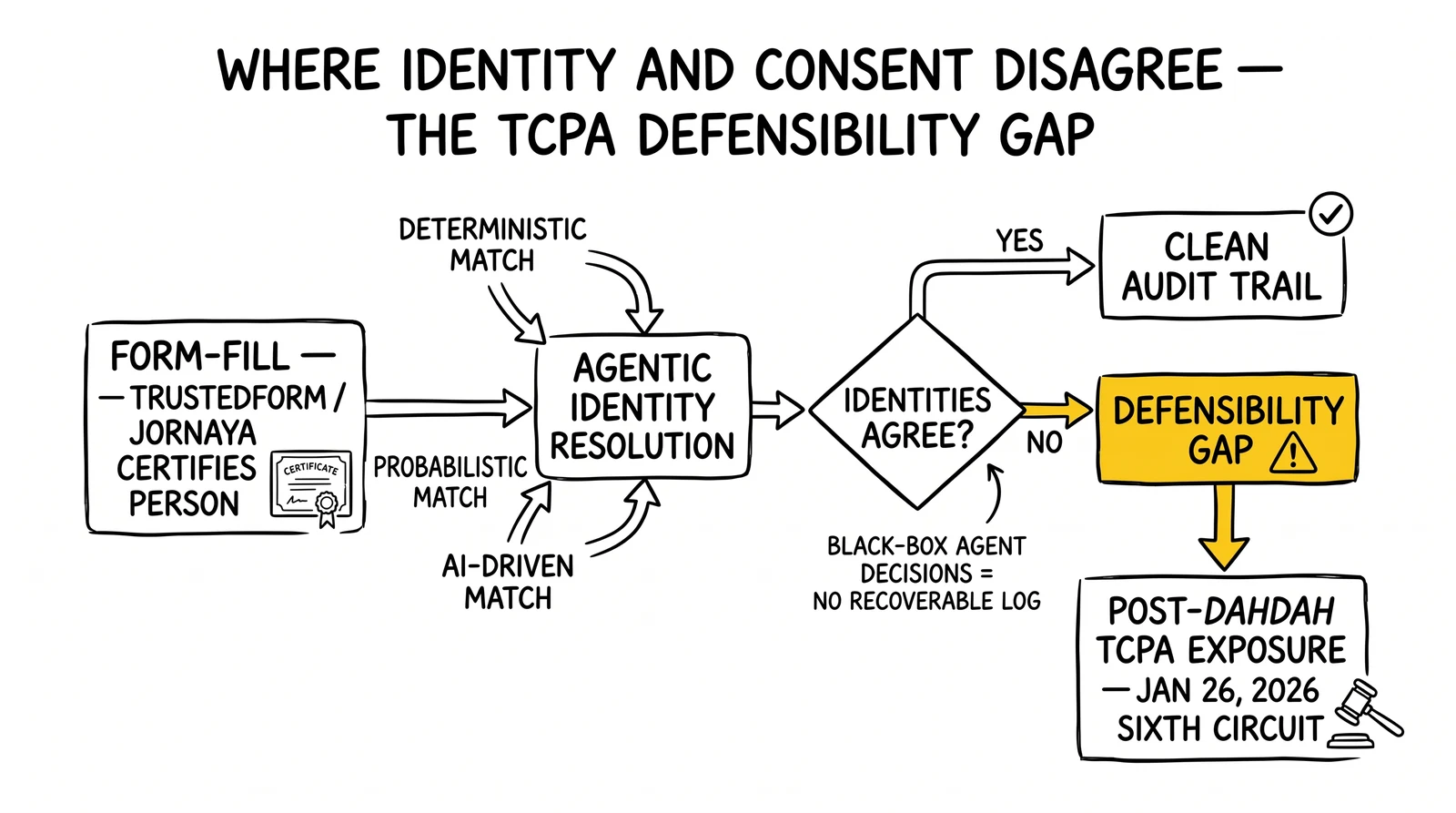

Identity Resolution Meets Agentic Activation Decisions

The customer-data-platform category has always sat next to the identity-resolution layer without owning it. Databricks CustomerLake’s launch introduced an Agentic Identity Resolution layer combining deterministic, probabilistic, and AI-driven matching. BlueConic plus Blueshift unifies first-party identity with execution decisioning across the merged platform. Hightouch leans on the customer data warehouse’s existing identity layer, typically Snowflake or Databricks.

For lead-generation operators, the identity layer is not optional infrastructure. TrustedForm and Jornaya certify which person fired the consent record. Post-conversion identity-resolution decisions about which prior visits, which subsequent purchases, and which downstream engagement events belong to the same person now run through agentic decisioning logic. When the identity layer that certified consent capture and the activation layer that decides which buyer receives the lead disagree on identity, the downstream consequences land on the consent record’s defensibility under TCPA.

The Sixth Circuit’s January 26, 2026 ruling in Dahdah v. Rocket Mortgage elevated form architecture to the load-bearing element of TCPA arbitration defense. The four-factor conspicuousness test attached defensibility to the form-level user experience at the moment of click. The agentic CDP shift extends the defensibility question past the form into the activation layer. A black-box agent routing decision without a recoverable human-readable audit trail creates defensibility gaps that the consent record alone cannot bridge.

Operators selecting agentic CDP infrastructure should require explainability logs as a contractual term. The specific log requirements should cover the identity-resolution decision (which deterministic matches were considered, which probabilistic confidence threshold cleared, which AI-driven decisions were made and on what input signal), the activation decision (which buyer was selected for the lead, which competing buyers were ranked, which fallback paths were available), and the audit-trail retention duration (sufficient to outlast the TCPA statute of limitations plus the operator’s typical legal-discovery window).

The vendor-side response to explainability requirements will vary. Databricks’ embedded-in-lakehouse architecture has native access to the underlying data and can produce comprehensive audit logs at low marginal cost. BlueConic-Blueshift’s execution-coupled architecture has tight control over the activation layer and can produce activation-decision audit logs cleanly. Hightouch’s composable warehouse-native architecture produces audit logs that depend on the underlying warehouse’s logging configuration, which means the operator’s existing warehouse instrumentation determines audit-trail quality. Each architecture is auditable; the operational lift required to make the audit defensible differs.

What This Means for Ping-Post Lead Distribution

Traditional ping-post lead distribution platforms – boberdoo, Phonexa, LeadsPedia, and the bespoke ping-post stacks running inside MediaAlpha, EverQuote, LendingTree, and QuinStreet – implemented routing logic on top of static profile data with periodic refresh. Agentic CDPs collapse the static-profile assumption. Profile attributes update continuously as new events arrive. Activation decisions re-score continuously as the profile updates.

The operational consequence for ping-post architecture is direct. If buyer-matching logic runs against profile data that updates nightly while CustomerLake re-scores every event in real time, the buyer-side decision is operating on stale data. The lead may have already entered an in-market window the static-profile router cannot see, or already exited one the router still treats as active. The mismatched cadence between continuous re-scoring and batched routing produces routing errors that compound across high-volume operations.

The vendor selection criteria for lead-gen operators should expand to include the routing-layer’s tolerance for upstream profile-update cadence. Operators running ping-post infrastructure on top of an agentic CDP should specify maximum acceptable latency between profile update and routing decision. The acceptable latency depends on vertical – insurance lead routing tolerates seconds; mortgage refinance tolerates minutes; B2B SaaS lead routing tolerates hours. The architecture choice should match the latency tolerance.

Cross-link to the lead distribution platforms comparison for the architectural landscape of the routing layer itself. The CDP architecture sits upstream of the routing decision and feeds the profile data the router consumes. Optimizing the routing layer without addressing the upstream profile-update cadence produces a routing layer that runs efficiently on stale data – operational efficiency in the wrong direction.

What Lead Operators Should Do in the Next 90 Days

The action surface is concrete and time-bounded. Five steps map the operator implementation arc.

First, map the current CDP architecture against the three-way classification. Is the operation running a traditional SaaS CDP (Segment, mParticle, Treasure Data), a composable warehouse-native architecture (Hightouch), an embedded data-platform stack (Databricks, Snowflake plus tooling), or a homegrown identity-and-activation layer? The architecture inventory determines which of the three June 2026 vendor moves applies as a competitive threat or upgrade path.

Second, model the cost of warehouse-native refresh frequency against actual event throughput. If the operation is high-volume ping-post running at sub-second routing SLAs, mPart’s vendor-biased 50x compute multiplier for 5-minute sync should be tested against the operator’s actual warehouse-compute pricing. The number may understate or overstate the operator-specific cost; the methodology of running the modeling exercise is the discipline that matters.

Third, audit identity-resolution dependencies and require explainability logging as a contract term during any vendor renegotiation. Post-Dahdah, the audit-trail through the activation layer is part of the TCPA defensibility surface, not adjacent to it. Vendors that cannot produce explainability logs covering identity-resolution decisions and activation decisions should be downgraded in vendor selection.

Fourth, evaluate whether the Brinker chrysalis framework’s “context engineer” role – covered in the State of Martech 2026 chrysalis analysis – needs an explicit job description inside the operation. Agentic CDPs assume someone curates the context the agents read. Operations without an explicit context-engineer function will see CDP investment underperform.

Fifth, watch the Q3 and Q4 2026 vendor cohort for further consolidation. The June 16 and June 17 announcements are not an end-state. Adobe, Salesforce, Microsoft, Snowflake, and Twilio Segment each have positioning decisions to make in the agentic CDP category. The pace of consolidation in the second half of 2026 will determine whether the three-architecture taxonomy persists or collapses into a two-architecture or one-architecture standard.

Key Takeaways

- Databricks CustomerLake launched June 16, 2026 at the Data plus AI Summit with HP, Circle K, AB InBev, and Getnet by Santander as private-preview customers. Tasso Argyros, the former ActionIQ co-founder and CEO, leads the product.

- BlueConic acquired Blueshift on June 17, 2026, combining identity and activation into a single execution layer. Deal terms were not disclosed. Combined entity reports 600-plus customers.

- Hightouch closed a $150 million Series D on April 29, 2026 at a $2.75 billion valuation. The June 15 “Agentic CDP” blog post is positioning rather than a product launch – Hightouch was already operating as a warehouse-native CDP and earned the 2026 Gartner Magic Quadrant Leader recognition.

- Three architectures now compete: composable warehouse-native (Hightouch), embedded-in-lakehouse (Databricks), execution-coupled (BlueConic plus Blueshift). The architecture choice carries cost, identity-resolution, and TCPA-defensibility consequences.

- Gartner forecasts that by 2030, 80 percent of net-new enterprise CDP deployments will be embedded in or composable with data platforms rather than purchased as standalone SaaS.

- Warehouse-native architectures running hourly profile refresh incur approximately 25x compute cost vs. daily refresh per mParticle’s vendor-biased analysis; 5-minute sync pushes compute to 50x or more. Read directionally, not as audited benchmarks.

- For ping-post lead distribution operating at sub-second SLAs, the architecture choice should be modeled against actual event throughput and refresh frequency requirements. High-volume operators may favor execution-coupled BlueConic-Blueshift; mid-volume operators may favor Hightouch’s composable approach.

- Post-Dahdah, the TCPA defensibility surface extends past the consent form into the activation layer. Operators should require explainability logs as a contract term covering identity-resolution decisions and activation decisions.

- The Q3 and Q4 2026 vendor cohort – Adobe, Salesforce, Microsoft, Snowflake, Twilio Segment – has positioning decisions that will determine whether the three-architecture taxonomy persists or consolidates further.

Sources

- Databricks – CustomerLake Launch Press Release (June 16, 2026)

- Databricks – Introducing CustomerLake Blog (June 16, 2026)

- BlueConic – Acquires Blueshift Press Release (June 17, 2026)

- Hightouch – Series D Funding Announcement (April 29, 2026)

- Hightouch – The Agentic CDP (June 15, 2026)

- MarTech.org – Databricks Unveils CustomerLake

- MarTech.org – BlueConic Acquires Blueshift

- CMSWire – Databricks Makes Its Martech Move

- mParticle – The Hidden Cost of Warehouse-Native