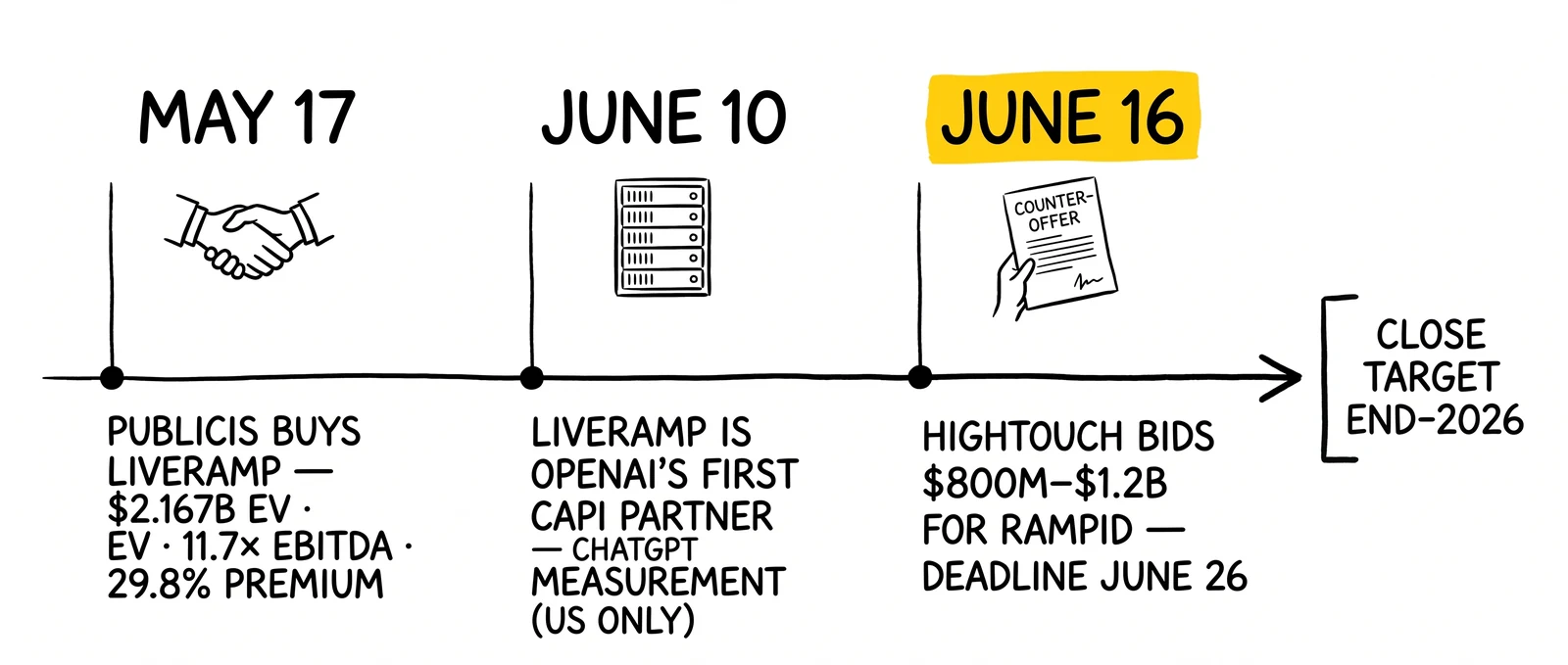

Publicis Groupe announced its $2.167 billion acquisition of LiveRamp on May 17, 2026, ending two decades of one identity-resolution vendor’s positioning as the neutral matching layer of the open ad ecosystem. Three weeks later, LiveRamp became OpenAI’s first independent ad-tech partner for ChatGPT conversion measurement. Six days after that, Hightouch made an $800 million to $1.2 billion unsolicited counter-offer for the identity assets. None of the coverage so far has worked through what this triple-event sequence means for the insurance, mortgage, and home-services lead aggregators whose ping-post infrastructure runs through that matching layer.

The Last Independent Just Became Captive

Publicis Groupe disclosed on May 17, 2026 that it had agreed to acquire LiveRamp Holdings for $38.50 per share in all-cash terms, an enterprise value of $2.167 billion and an equity value of $2.546 billion before subtracting $379 million in acquired net cash. The price represented a 29.8 percent premium to LiveRamp’s prior trading close, and the deal is targeted to close by the end of calendar 2026 subject to LiveRamp shareholder approval and regulatory clearance.

Arthur Sadoun, the Publicis chairman and chief executive, framed the deal in language designed for an audience that has stopped buying agency-acquisition press releases at face value. “LiveRamp fits perfectly into the architecture of our model, delivering more intelligent agents to accelerate our clients’ agentic business transformation,” Sadoun said in the announcement. The phrase that matters in that sentence is architecture – the Publicis pitch is not that LiveRamp is a service line bolted onto Epsilon, but that LiveRamp is the identity substrate on which the holding company’s agentic ad-buying systems will run. The press release went further, committing the combined entity to operate as a “neutral, interoperable platform” with “open access across the ecosystem” and “no customer prohibited from accessing or restricted in using” LiveRamp’s services.

That neutrality commitment is the load-bearing claim of the entire deal, and it is the claim the rest of the industry is now interrogating in public.

The lead-generation economy has a particular reason to care. Every CPL benchmark a publisher quotes to a buyer, every TCPA consent certificate routed through a TrustedForm or Jornaya passport, every PEWC-grade record of one-to-one consent eventually has to be matched to a person at the receiving end of the ping-post auction. That matching happens inside an identity-resolution graph. Until May 17, the largest open-ecosystem graph could plausibly be described as neutral with respect to the agency holding companies competing for downstream advertising dollars. After May 17, the largest open-ecosystem graph has a holding-company name attached.

LiveRamp itself was no stranger to acquisition risk. Through the post-cookie transition of 2022 to 2025, the company had positioned RampID as the open-ecosystem alternative to Google’s Privacy Sandbox cohort identifiers and Apple’s first-party walled-garden architecture. That positioning depended entirely on the perception that LiveRamp would not be acquired by a party whose interests competed with those of its customers. The company’s customers included Publicis competitors WPP, Omnicom, Interpublic, Dentsu, and Havas – every other agency holding company on the planet. The May 17 announcement made every one of those relationships structurally unstable on the same day.

What Publicis Actually Paid For

LiveRamp’s fiscal 2026 results – reported the same day as the acquisition announcement – give the analyst-grade arithmetic for the deal. Full-year revenue came in at $813 million, up 9 percent year over year against fiscal 2025’s $746 million (which itself grew 13 percent). Subscription revenue accounted for $614 million of the fiscal 2026 total. Non-GAAP operating income reached $182 million; adjusted EBITDA closed at $184.8 million. Annualized recurring revenue stood at $545 million across 846 direct customers, with 133 of those customers paying more than $1 million each in annual recurring revenue.

Applied against the $2.167 billion enterprise value, those numbers produce an EV/Revenue multiple of roughly 2.7x and an EV/Adjusted EBITDA multiple of roughly 11.7x. Both numbers are below the multiples that customer-data-platform and martech-SaaS comparables have commanded over the past three years. Snowflake-adjacent data tooling has traded at five to eight times forward revenue. Salesforce paid roughly 22x revenue for Slack in 2020 and roughly 19x revenue for Tableau in 2019. Even compressed 2024-2026 martech multiples have generally cleared the four-to-six-times revenue range for assets with comparable ARR durability.

The Publicis price reflects something other than aggressive bidding. It reflects the maturation of the identity-resolution category as a definable line item rather than a growth narrative, and it reflects the neutrality discount Publicis must absorb when an agency holding company buys a vendor previously marketed as independent. Some portion of LiveRamp’s customer base – the WPP and Omnicom client portfolios most obviously – represents revenue at risk the moment the deal closes. Publicis paid the multiple it paid because the implicit value of those exposed accounts had to be netted out of the price.

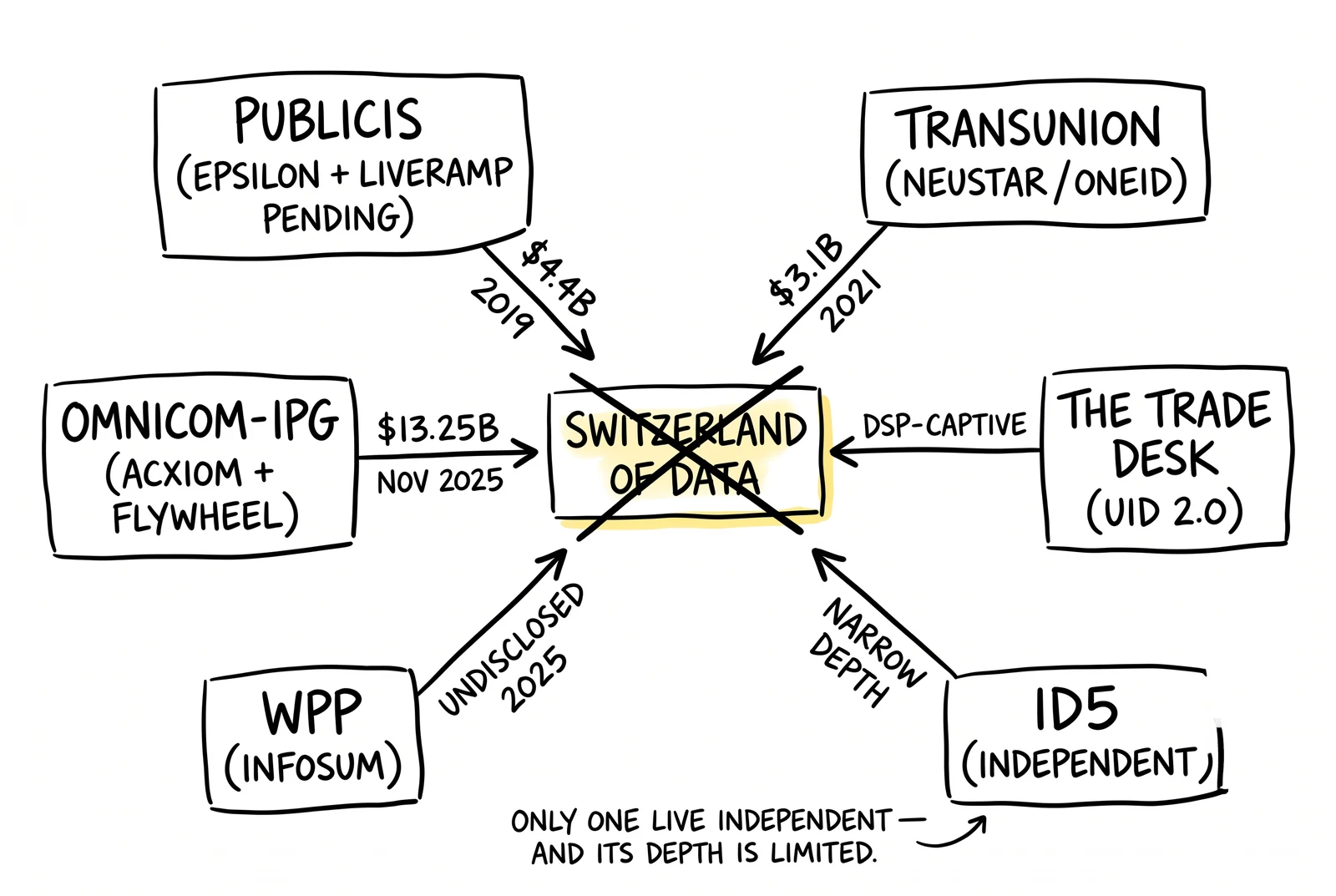

The comparable transactions in the same category track the same pricing logic.

| Transaction | Year | Deal Value | Acquirer Strategy |

|---|---|---|---|

| Publicis–Epsilon | 2019 | $4.4B | First identity-and-loyalty asset under Publicis Connected Intelligence |

| TransUnion–Neustar | 2021 | $3.1B | OneID identifier inside credit-bureau holdco |

| WPP–InfoSum | 2025 | undisclosed | Clean-room and federated-data capability for WPP Open |

| Omnicom–IPG (Acxiom inside) | Nov 26, 2025 close | $13.25B headline merger | Acxiom + Flywheel inside one agency holdco post-FTC consent order |

| Publicis–LiveRamp | Pending end-2026 | $2.167B EV | RampID identity layer captured by agency holdco |

Read across that table and a pattern emerges. Identity-resolution vendors have become roll-up targets for either credit bureaus (TransUnion–Neustar) or agency holding companies (Publicis–Epsilon, Omnicom–Acxiom-via-IPG, WPP–InfoSum, now Publicis–LiveRamp). The independent operating model is not surviving as a public-market category. Hightouch is the only credible alternative buyer profile because a vendor-funded composable CDP is the only acquirer that has a coherent reason to want to keep RampID neutral.

For the lead economy, the more important question is what category Publicis bought rather than what multiple. The press release identifies four LiveRamp assets explicitly: RampID, LiveRamp Connect, Data Collaboration, and the cross-channel measurement stack. Of those, RampID is the asset most directly relevant to lead-distribution infrastructure, because RampID is the identifier that matches an aggregator’s known offline consumer record to the online sessions an enterprise advertiser is paying to retarget. Connect is the activation rail that moves those matched audiences into demand-side platforms and walled-garden buyers. Lose either of those two assets to a Hightouch carve-out and the integrated value Publicis modeled into the price falls apart.

The OpenAI Wrinkle – When the Identity Layer Reaches Inside ChatGPT

On June 10, 2026 – twenty-four days after the Publicis acquisition announcement – LiveRamp disclosed that it had become the first independent ad-tech partner integrated into OpenAI’s Conversions API Hub. The integration covers ChatGPT advertising at launch and is United States only in the initial rollout. The mechanics are server-to-server: an advertiser hashes its purchase event data, sends the hashed records to LiveRamp, and LiveRamp passes the matched events to OpenAI’s measurement endpoint. ChatGPT ad delivery then has a closed-loop signal grounded in transactions rather than clicks.

Travis Clinger, LiveRamp’s chief connectivity officer, gave the framing in a Marketing Dive interview. “We expect our first advertiser to go live this week,” Clinger said of the rollout. He went further on the data value: transaction data flowing through the CAPI Hub is, in his words, “far more valuable than the click-based data” that has historically powered conversion measurement on the open web. The framing matters because it positions LiveRamp not as a vendor competing for ChatGPT measurement budget but as a co-architected component of how OpenAI plans to measure advertising at all.

For the lead economy, this is the moment the Publicis acquisition stops being an inside-the-holding-companies story and becomes a structural change in the attribution stack.

Consider the conversion path that matters for an insurance, mortgage, or home-services aggregator selling lead inventory into a national buyer in 2027. A consumer asks ChatGPT a research-stage question – say, comparing whole-life and term-life insurance products – and clicks through to an aggregator’s content page. The aggregator routes the lead via ping-post to a carrier buyer. The carrier converts the lead into a policy three weeks later. Under the old measurement architecture, the conversion was visible to the carrier’s CRM but not back-attributable to the ChatGPT session that initiated it. Under the new CAPI Hub architecture, the carrier’s policy event flows back through LiveRamp’s hashed-email match into the OpenAI measurement endpoint and updates ChatGPT’s understanding of which research-stage queries actually produce policies. ChatGPT’s ad delivery learns to favor those queries.

The implication is direct: ChatGPT now has a first-party server-side conversion signal that bypasses the entire click-attribution layer the open web has used since the early 2000s. That signal runs through LiveRamp – a vendor that as of June 10 had a $2.167 billion sale to Publicis pending. The same matching layer powering OpenAI’s transaction-grade attribution for ChatGPT advertising will, by the end of 2026, sit inside the agency holding company that competes for the same advertiser budget the carrier buyer is trying to allocate. The lead aggregator selling into that carrier has no leverage over either side of that arrangement and no visibility into how either side prices its services.

This connects directly to the conversion-premium analysis in the Adobe AI-traffic CPL/EPL recalibration piece, which laid out how AI-referred sessions are converting at a structural premium to non-AI traffic. What the LiveRamp–OpenAI integration adds is the measurement infrastructure that lets buyers price that premium accurately. Without server-side attribution, the AI conversion premium remains an Adobe Analytics aggregate. With server-side attribution flowing through a Publicis-affiliated identity layer, the premium becomes addressable at the individual campaign and individual buyer level – and that addressability accrues first to advertisers connected to the LiveRamp graph.

The OpenAI announcement is also the explanation for why Publicis was willing to close the deal at the 11.7x adjusted-EBITDA multiple rather than waiting for the market to soften. The CAPI Hub partnership was visible to Publicis well before the acquisition closed; the asset Publicis was buying included that partnership and the optionality it created. Looked at from that angle, the deal multiple looks less aggressive than the headline ratio suggests.

The Hightouch Counter and the RampID Carve-Out Question

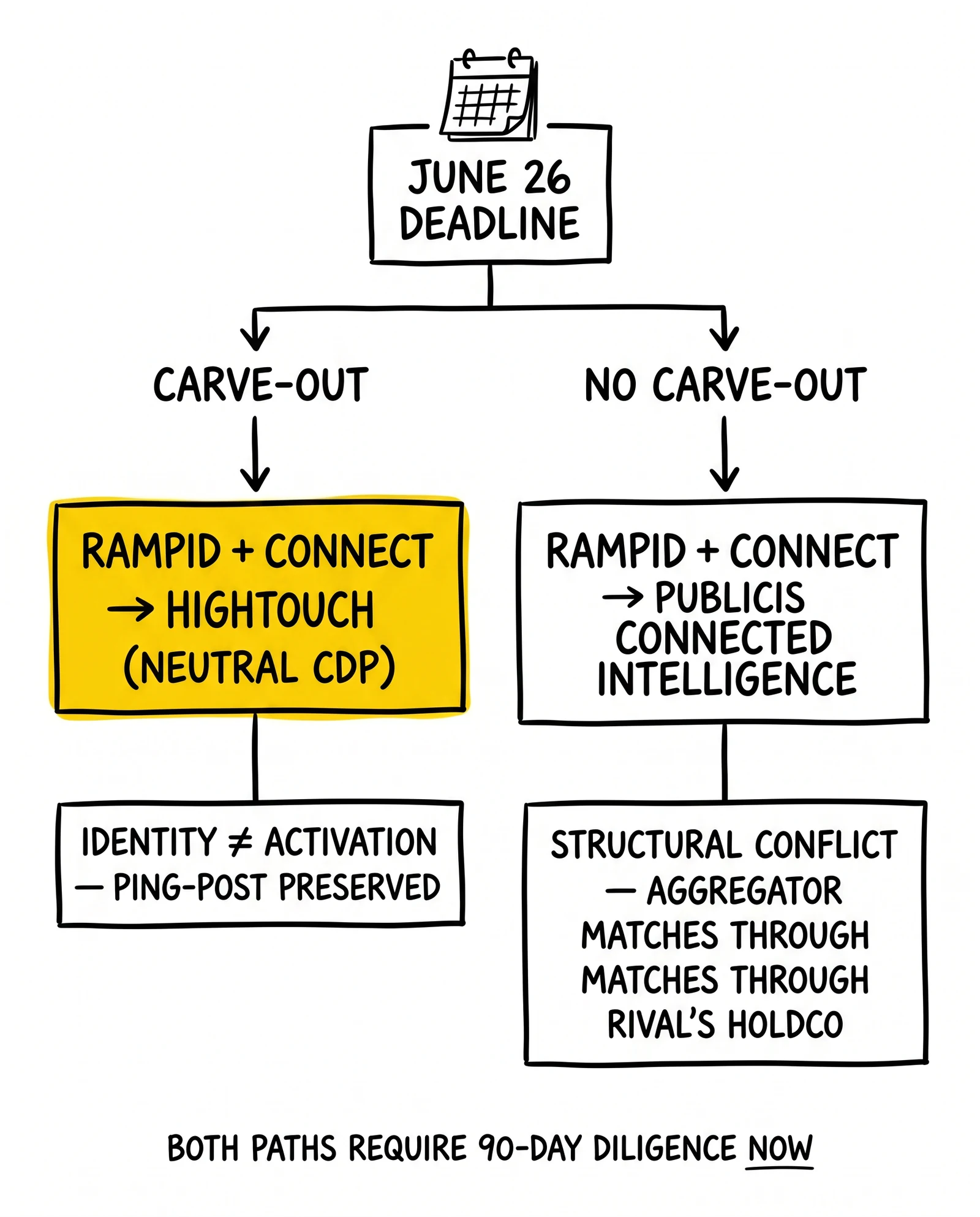

Six days after the OpenAI partnership disclosure, Axios reported on June 16, 2026 that Hightouch – the composable customer-data platform last valued at $2.75 billion after its April 2026 Series D led by Goldman Sachs and Bain Capital Ventures – had made an unsolicited offer to Publicis for RampID and LiveRamp Connect. The reported range was $800 million to $1.2 billion, structured as a combination of cash, stock, and debt. Hightouch set a deadline of June 26, 2026 for a response.

As of this article’s publication date, that deadline remains live. The next nineteen days will determine whether the Publicis acquisition closes as announced – bringing the integrated LiveRamp stack into the Publicis Connected Intelligence portfolio – or whether the identity layer gets carved out into an independent CDP-vendor home. The two outcomes have very different implications for the lead economy.

Walk the carve-out scenario first. Under a Hightouch acquisition of RampID and Connect, the identity-resolution layer would sit inside a vendor whose business model depends explicitly on remaining vendor-neutral – Hightouch makes money by activating customer data into whatever marketing destinations a client uses, which is a structurally different incentive from an agency holding company’s economics. Publicis would still close on the broader LiveRamp transaction but would receive a hollowed-out asset: the data-collaboration product line and the cross-channel measurement stack, without the foundational identity graph that powers them. That is not what Publicis underwrote when it agreed to the $38.50 per-share price, and the deal terms would presumably need to be renegotiated or the acquisition restructured.

Now walk the no-carve-out scenario. Publicis rejects the Hightouch offer or runs the clock past June 26, the original transaction closes in late 2026, and RampID and LiveRamp Connect operate inside a unit of Publicis Connected Intelligence alongside Epsilon. The neutrality language in the original press release becomes a stated operating principle inside an agency holding company, enforced by whatever governance Publicis chooses to establish and audited by whichever third party Publicis selects. That arrangement is the one named industry skeptics are calling unrealistic.

For lead distribution infrastructure, the carve-out outcome is materially better because it preserves the structural separation between identity and activation that ping-post auctions implicitly assume. The non-carve-out outcome creates a single holding company that operates both the identity-resolution layer between aggregator and carrier and the agencies whose insurance, mortgage, and home-services clients buy through that layer. That structural conflict does not resolve itself with neutrality language in a press release.

A practical implication for lead-distribution platforms and ping-post buyers: contracts coming up for renewal in the second half of 2026 should be drafted on the assumption that either outcome is possible. Boberdoo, LeadsPedia, and Phonexa-style routers depending on RampID for offline-to-online matching in onboarding flows should map their dependency explicitly so that a carve-out – or a non-carve-out – can be operationalized inside a 30-day window. Aggregators who treat the Hightouch deadline as a routine market event will find themselves twelve months out re-pricing CPLs to absorb terms changes they did not anticipate.

The other variable worth watching is the regulatory review. The Publicis acquisition is subject to antitrust clearance in the United States and the European Union; the Omnicom-IPG merger that closed November 26, 2025 was cleared by the FTC under a consent order issued June 23, 2025 that imposed conduct remedies on data-sharing across the merged entity. Whether the FTC views the LiveRamp deal as raising parallel concerns – and whether the EU Commission’s increased focus on ad-tech consolidation produces a structural remedy of its own – could itself precipitate the carve-out that Hightouch is offering to execute voluntarily.

Switzerland Is Dead – and There’s No Replacement

The phrase that captured the industry’s reaction came from Forrester’s Jay Pattisall and Joe Stanhope, writing on the firm’s blog within days of the May 17 announcement. “LiveRamp has been an industry iconoclast with its long-standing commitment to independence, the proverbial ‘Switzerland of data,’” they wrote. “Clients must be aware that absorption is the inevitable path in M&A, putting LiveRamp’s neutrality at risk in the long term.” The framing borrows from the centuries-old Swiss positioning as the neutral party in European political disputes – and the framing is a tell. The analysts are explicitly signaling that the neutrality claim is a marketing artifact rather than a structural property.

The named skeptics in the industry trade press echoed the framing in more concrete language. Mathieu Roche, the chief executive of ID5, told The Drum that “LiveRamp’s continued neutrality seems unrealistic” given the structural conflict. Tom Denford, the chief executive of ID Comms, characterized the situation in similar terms: “The exposure for competing holding companies is significant.” Charles Manning, the chief executive of Kochava, raised the trust question: “The risk is whether everyone still treats that infrastructure as neutral.” Each of those three voices represents a constituency – competing identity vendors, agency-buyer consultants, and adjacent measurement platforms – that has direct economic exposure to whether RampID remains usable for non-Publicis clients on terms equivalent to the ones they have today.

What makes the consolidation story particularly difficult for the lead economy is that there is no obvious replacement for the Switzerland-of-data positioning. Walk the alternatives. The Trade Desk’s Unified ID 2.0 is a DSP-controlled identifier, which is structurally captive on a different axis. ID5’s universal identifier is independent but lacks LiveRamp’s offline-to-online matching depth. The InfoSum clean-room technology is now owned by WPP. Acxiom is now inside Omnicom. Epsilon is already inside Publicis. Neustar is inside TransUnion. The list of plausible enterprise-grade open-ecosystem identity providers has effectively collapsed to one – LiveRamp – and that one is becoming captive within twelve months.

For a ping-post insurance lead aggregator selling into State Farm, Progressive, GEICO, and Allstate simultaneously, the consequence is structural. The matching layer between buyer and seller now sits inside a holding company – Publicis – that is competing for those carriers’ agency budgets. State Farm, for instance, has historically run portions of its national brand work through Publicis-aligned agency relationships; Progressive runs work through Wieden+Kennedy and Arnold; GEICO has long-standing relationships with The Martin Agency (now under IPG-via-Omnicom). The lead aggregator’s economic interest in the identity-resolution layer is straightforward – accurate offline-to-online matches at a low per-record cost – but that interest is now mediated by a holding company whose primary revenue line is selling agency services to the same carriers buying the aggregator’s leads. None of the existing master service agreements between aggregators and carriers anticipates that structural overlap.

The honest answer for an operator looking at the consolidated identity landscape is that the Switzerland positioning is gone and there is no replacement coming. The category has matured into an oligopoly of agency-owned and credit-bureau-owned graphs, and lead-economy operators have to plan their next three years inside that constraint rather than waiting for a new independent to emerge.

The Cannes Defection – WPP Announces It’s Done with LiveRamp

The clearest signal that the neutrality claim is not surviving contact with operational reality came from WPP. At Cannes Lions 2026, WPP chief executive Cindy Rose announced that the agency holding company would discontinue LiveRamp usage following the Publicis takeover. Marketing Dive reported the announcement in its interview with Travis Clinger; the LiveRamp executive’s response in that interview acknowledged the situation without disputing the underlying logic.

The reasoning behind the WPP decision is direct, and it does not require sophisticated analysis. WPP cannot route client data through identity infrastructure owned by a rival agency holding company. The risk is not necessarily that Publicis would misuse the data – the contractual terms can be drafted to constrain that behavior – but that Publicis would have unavoidable visibility into the patterns of WPP’s client activity that no contractual term can fully obscure. Spend patterns, audience composition, campaign timing, and onboarding cadences are all signals that a sophisticated holding company can extract from operational metadata even when the underlying customer records are encrypted. WPP made the rational call: do not put your operating signal in a competitor’s data center.

The downstream lesson for the lead economy is the same one. Multi-buyer lead aggregators – the operators selling the same inventory to State Farm, Progressive, GEICO, and Allstate simultaneously, or to Quicken Loans, Rocket Mortgage, and loanDepot simultaneously, or to multiple national home-services franchisors at once – are in a structurally analogous position to WPP. The matching layer they use for offline-to-online resolution sits between them and their buyers. If that matching layer is owned by a holding company that competes for their buyers’ upstream advertising spend, the aggregator is exposed in exactly the way WPP is exposed.

The practical translation is a vendor-dependency audit. The next 90 days should include explicit documentation of every place RampID matches are used in the aggregator’s onboarding, qualification, and routing logic – and an alternative matching path for each of those uses that does not require RampID. The alternative path may be more expensive on a per-match basis or have lower coverage. The cost is the insurance premium against a 2027 contract negotiation in which the LiveRamp pricing committee – now reporting to Publicis Connected Intelligence – informs the aggregator that match rates and per-record fees are being restructured.

WPP made the call publicly because WPP is large enough to absorb the operational cost and competitive enough with Publicis to derive marketing value from the announcement itself. Most lead aggregators will not make the call publicly, but the operational work of preparing for the call is the same regardless of who eventually announces it.

What This Means for TrustedForm, Jornaya, and Consent Capture

The Publicis-LiveRamp acquisition does not directly affect TrustedForm or Jornaya – those products operate inside ActiveProspect following the January 2026 acquisition of Verisk Marketing Solutions, and their core function is TCPA-grade consent capture rather than cross-domain identity resolution. The connection between the two stories, however, is structural and increasingly difficult to ignore.

The lead economy now runs on two consolidating layers that were independent five years ago. The consent-capture layer – TrustedForm and Jornaya inside ActiveProspect – sits between the lead-generation publisher and the lead-buying carrier or lender, certifying that the consumer’s express consent meets PEWC and TCPA standards at the moment the lead changes hands. The InfutorData consolidation analysis walked through what single-vendor concentration in that consent layer means for renewal leverage and pricing. The identity-resolution layer – RampID and Connect inside LiveRamp, soon inside Publicis – sits between the lead-buying enterprise and the downstream advertising stack the enterprise uses to recoup its lead acquisition cost. Both layers are now controlled by entities that have meaningful market power on terms changes.

Two implications follow for buyers and aggregators trying to forecast their cost structure across 2027 and 2028. First, TCPA-grade consent certificates need to be checked against which identity graph confirmed the lead match – the same TrustedForm passport routed through a RampID match versus an alternative identity provider produces different downstream economics because the cost of each piece of the chain compounds. Second, buyers should ask explicitly in onboarding and renewal cycles what identity-vendor terms changed post-acquisition. Even a six-month moratorium on price increases written into the original Publicis-LiveRamp press release – and there is no such moratorium publicly disclosed – would not address the structural conflict that becomes operational once the deal closes.

The deal multiple itself is the third implication. Publicis paid 11.7x adjusted EBITDA for LiveRamp; if that multiple persists as the comparable benchmark for identity-and-data-collaboration platforms, ActiveProspect – which now owns both the TrustedForm passport and the Jornaya LeadiD certificate after the Verisk Marketing Solutions acquisition – has a defensible valuation in the multi-billion-dollar range whenever its current ownership decides to test the public-market exit. Trestle, the consumer data platform spun out of the Versium and Infutor consolidation, has a similar profile. Any operator using either vendor should understand that the next M&A event in their stack is plausible rather than hypothetical.

Direct dependency by named lead aggregators – MediaAlpha, EverQuote, LendingTree, QuinStreet – on RampID is not established in public filings, and the article does not claim it as a reported fact. The structural exposure is the more general one: aggregators selling into enterprise buyers that use RampID for offline-to-online resolution operate one degree of separation away from the consolidation event. That exposure is real even where direct contractual dependency is not. The diligence question for an operator running a $100 million ARR aggregation business is whether the matching layer between the aggregator’s leads and the carriers’ downstream measurement runs through a holding-company-captive identifier – and that diligence question is now answerable, not hypothetical.

Pair that consent-and-identity diligence with the DNC scrubbing operator deep dive on federal and state rules and the picture becomes clearer. The compliance stack and the matching stack are both consolidating in the same window, into vendors that have parallel pricing leverage. Operators who treat the two consolidations as separate stories will be surprised when their 2027 renewal cycles surface terms changes from both vendors at once.

What Lead Operators Should Do in the Next 90 Days

The Hightouch deadline runs to June 26, and the deal itself is not expected to close until end of calendar 2026. The 90-day window between this article’s publication and the end of the third quarter is the cheapest time for an aggregator, publisher, or buyer-side operator to do the diligence work that becomes expensive once the close date approaches and contract-renewal cycles accelerate.

The action checklist is specific. First, audit identity-vendor terms for any post-acquisition change clauses. Most enterprise contracts include language that triggers on change-of-control events; the question is whether those clauses give the customer cancellation rights, repricing rights, or neither. Pull the LiveRamp master service agreement and any addendums signed in the past 24 months and have counsel read the change-of-control sections specifically.

Second, pressure-test ping-post routing assumptions against a Hightouch carve-out scenario. If RampID and Connect were to migrate to a Hightouch-owned subsidiary post June 26, what changes in the integration logic between the aggregator’s routing platform and the buyer’s identity-resolution endpoint? In most cases the answer is “very little in the technical integration, but everything in the contractual relationship” – and the contractual rewrite is the time-consuming work to do early.

Third, for buyers with multi-carrier or multi-lender dependencies, evaluate switching costs across identity providers explicitly. Map every place RampID is in use, then identify the alternative – ID5, The Trade Desk’s UID 2.0, an in-house deterministic match via the cookieless attribution stack, or a partner-sourced graph – that would have to fill the gap. Document the match-rate differential and the per-record cost differential between RampID and the alternative. That documentation is the artifact that gives the operator leverage in the next pricing conversation.

Fourth, track the June 26 Hightouch deadline. The outcome materially affects RampID independence and the structural shape of the deal. Operators who track the deadline and have a Plan A and Plan B drafted before June 26 will be operating ahead of the cycle; operators who treat the deadline as a trade-press footnote will be reading their counterparts’ decisions through public filings rather than acting on them.

Fifth, re-price ChatGPT-referred conversion data given the new CAPI Hub measurement path. The June 10 announcement gives a measurable signal that AI-referred sessions are about to have transaction-grade attribution flowing back through LiveRamp into OpenAI. That measurement upgrade should increase the realized EPL for ChatGPT-sourced inventory by mid-2027. Buyers who incorporate the expected EPL premium into their 2027 bid ceilings – and sellers who incorporate the same premium into their CPL pricing – will be operating on better information than counterparts who wait for the conversion data to validate the premium in market.

This is a 90-day checklist, not a 12-month roadmap. The point is that the structural change is in motion and the cost of preparing for it is meaningfully lower today than it will be in six months.

Key Takeaways

- Publicis announced the $2.167B LiveRamp acquisition on May 17, 2026 at $38.50 per share – a 29.8 percent premium, all cash, targeted to close end of calendar 2026 subject to shareholder and regulatory approval. The multiple is 2.7x EV/Revenue and 11.7x EV/Adjusted EBITDA against LiveRamp fiscal 2026 results.

- LiveRamp became OpenAI’s first independent ad-tech CAPI partner for ChatGPT measurement on June 10, 2026 – a US-only server-to-server integration that gives ChatGPT advertising a transaction-grade conversion signal flowing through what will become a Publicis-affiliated identity layer once the deal closes.

- Hightouch made an unsolicited $800M–$1.2B counter-offer for RampID and LiveRamp Connect on June 16, with a deadline of June 26, 2026. The carve-out outcome is materially better for lead-distribution infrastructure than the no-carve-out outcome because it preserves the structural separation between identity and activation that ping-post auctions implicitly assume.

- WPP CEO Cindy Rose announced at Cannes 2026 that the agency holding company would discontinue LiveRamp usage following the Publicis takeover. The reasoning applies one-for-one to multi-buyer lead aggregators selling into competing carriers, lenders, or franchisors.

- The identity-resolution category has consolidated into agency-holding-company-owned graphs (Epsilon, Acxiom, InfoSum, soon LiveRamp) and credit-bureau-owned graphs (Neustar inside TransUnion). The Switzerland-of-data positioning has no live public-market exemplar after May 17.

- The consent-capture layer (TrustedForm and Jornaya inside ActiveProspect since January 2026) and the identity-resolution layer (RampID inside Publicis pending end of 2026) are now both controlled by entities with meaningful pricing leverage at renewal cycles. Buyers should expect post-acquisition terms changes in both and price the vendor risk accordingly.

- A 90-day operator checklist covers: change-of-control audit of identity-vendor contracts, pressure-testing ping-post routing against a Hightouch carve-out scenario, mapping switching costs to ID5 or alternative graphs, tracking the June 26 Hightouch deadline, and re-pricing ChatGPT-referred conversion data for the new CAPI Hub measurement path.

- Direct dependency by named lead aggregators (MediaAlpha, EverQuote, LendingTree, QuinStreet) on RampID is not established in public filings. The structural exposure for any aggregator selling into RampID-using enterprise buyers is real even where direct contractual dependency is not – and the diligence is now answerable rather than hypothetical.

- The 11.7x EV/Adjusted EBITDA multiple Publicis paid is the analyst-grade pricing of identity infrastructure and a useful forward comparison for ActiveProspect or Trestle if either tests the public exit market. The maturation of the category as a pricing reference is itself the story under the story.

Sources

- Publicis to Acquire LiveRamp to Accelerate Data Co-Creation for Smarter Agents (Publicis Groupe press release, May 17 2026)

- LiveRamp 8-K Filing on the Publicis Acquisition (SEC EDGAR, May 17 2026)

- LiveRamp Announces Fourth Quarter and Fiscal Year 2026 Results (GlobeNewswire, May 17 2026)

- OpenAI’s ChatGPT Ads Get Their First Measurement Partner in LiveRamp (Digiday, June 10 2026)

- Unlocking Better Performance Optimization and Measurement for Marketers in ChatGPT (LiveRamp blog, June 10 2026)

- LiveRamp CEO Dishes on OpenAI Partnership, Looming Publicis Acquisition (Marketing Dive, June 2026)

- Scoop: Hightouch Offers Publicis $1.2B for RampID and Connect (Axios via Yahoo Finance, June 16 2026)

- Marketing Strategy: Publicis, LiveRamp, RampID, and the Data Industry’s Ad-Tech Reset (The Current, May 2026)

- The Exposure Is Significant – Inside the Implications of Publicis’s $2bn LiveRamp Deal (The Drum, May 2026)

- Publicis Acquires LiveRamp to Advance New Agentic AI Push (Forrester, May 2026)

- TransUnion Accelerates Growth of Identity-Based Solutions With Agreement to Acquire Neustar for $3.1 Billion (TransUnion newsroom, 2021)

- Omnicom 8-K on the Interpublic Merger Close (SEC EDGAR, November 26 2025)

- Publicis Acquires LiveRamp in a Major Shakeup for Indie Data Collaboration (AdExchanger, May 2026)